When To Sell: GM Breweries

When To Sell: GM Breweries

You might also like

- ICT One Trade Setup For Life Notes TinyVizsla-1Document3 pagesICT One Trade Setup For Life Notes TinyVizsla-1agathfuture100% (1)

- Algo Convention 2021 ScheduleDocument2 pagesAlgo Convention 2021 SchedulePhani KrishnaNo ratings yet

- Raymond Initiating CoverageDocument20 pagesRaymond Initiating Coveragenarayanan_rNo ratings yet

- Driving Growth: Revenue From Operations Ebitda PATDocument2 pagesDriving Growth: Revenue From Operations Ebitda PATBlueHexNo ratings yet

- Sheela Foam LTD - Initiaiting Coverage - 18092018 - 19!09!2018 - 08Document32 pagesSheela Foam LTD - Initiaiting Coverage - 18092018 - 19!09!2018 - 08Mansi Raut PatilNo ratings yet

- Below Expectations: UMW HoldingsDocument11 pagesBelow Expectations: UMW HoldingskufaizNo ratings yet

- Stock Performance of Obour Land For Food Industries (OLFI - EGY)Document1 pageStock Performance of Obour Land For Food Industries (OLFI - EGY)body.helal2001No ratings yet

- PMS Guide August 2019Document88 pagesPMS Guide August 2019HetanshNo ratings yet

- JK Cement: Key Financial Highlights (2018-19)Document1 pageJK Cement: Key Financial Highlights (2018-19)KpNo ratings yet

- Viacom Reports Second Quarter Results: Statement From Bob Bakish, President & CeoDocument14 pagesViacom Reports Second Quarter Results: Statement From Bob Bakish, President & CeoNickALiveNo ratings yet

- Vietnam Ho Chi Minh City Office Q2 2019 PDFDocument2 pagesVietnam Ho Chi Minh City Office Q2 2019 PDFNguyen Quang MinhNo ratings yet

- Paris Air Show Boeing 2019Document26 pagesParis Air Show Boeing 2019Sani SanjayaNo ratings yet

- Chugging Along: Reliance IndustriesDocument12 pagesChugging Along: Reliance IndustriesAshokNo ratings yet

- Berger Paints (India) Limited 21 QuarterUpdateDocument7 pagesBerger Paints (India) Limited 21 QuarterUpdatevikasaggarwal01No ratings yet

- Jakarta Retail 2q17Document2 pagesJakarta Retail 2q17ainia putriNo ratings yet

- Kantar Worldpanel FMCG Monitor Dec 2018 enDocument9 pagesKantar Worldpanel FMCG Monitor Dec 2018 enAnh Nguyen TranNo ratings yet

- Margin Concerns Should Take Precedence Over Improved OutlookDocument15 pagesMargin Concerns Should Take Precedence Over Improved Outlookashok yadavNo ratings yet

- Boi Asean q3 2015 BookletDocument27 pagesBoi Asean q3 2015 BookletSteven SutantoNo ratings yet

- Ambit Capital - Agri Inputs - Diverging Growth Rates (Sector Update) (POSITIVE)Document65 pagesAmbit Capital - Agri Inputs - Diverging Growth Rates (Sector Update) (POSITIVE)Davuluri OmprakashNo ratings yet

- Realty and The Second Wave: SpeakersDocument23 pagesRealty and The Second Wave: SpeakersAshutosh PatidarNo ratings yet

- FC Installment CardDocument1 pageFC Installment CardKristelNavarroNo ratings yet

- RHB Report My - Alliance Bank - Results Preview - 20190813 - RHB 92390246692298925d512480e5e00Document7 pagesRHB Report My - Alliance Bank - Results Preview - 20190813 - RHB 92390246692298925d512480e5e00Leow Ann HongNo ratings yet

- Pt. Gs Gold Shine Battery: Nama Karyawa: TRI HANDOKO Jabatan: Director Company Perform - Jan 19Document3 pagesPt. Gs Gold Shine Battery: Nama Karyawa: TRI HANDOKO Jabatan: Director Company Perform - Jan 19Nia TjhoaNo ratings yet

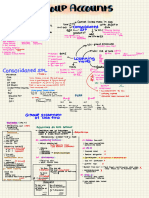

- Group Accounts BasicsDocument1 pageGroup Accounts BasicsVaishnavi ChaturvediNo ratings yet

- Fund Manager Report November 2019: NBP FundsDocument17 pagesFund Manager Report November 2019: NBP FundsTaha SaleemNo ratings yet

- CCL Products - Initiating Coverage - 09092019 - 11!09!2019 - 08Document29 pagesCCL Products - Initiating Coverage - 09092019 - 11!09!2019 - 08Amit PatelNo ratings yet

- US BN: Key Findings: Pe DealsDocument1 pageUS BN: Key Findings: Pe DealsethernalxNo ratings yet

- Tata Consultancy Services (TCS) : NeutralDocument8 pagesTata Consultancy Services (TCS) : Neutraltdog66No ratings yet

- Jiten SahuDocument36 pagesJiten SahuMirza Aftab BaigNo ratings yet

- Idr Bjfin@in 091115 105311Document68 pagesIdr Bjfin@in 091115 105311NikhilKapoor29No ratings yet

- Reduce: Bharti Infratel Bhin inDocument11 pagesReduce: Bharti Infratel Bhin inashok yadavNo ratings yet

- Automotive Axles LTDDocument25 pagesAutomotive Axles LTDLK CoolgirlNo ratings yet

- Avianca Holdings BTGPactual 2017Document7 pagesAvianca Holdings BTGPactual 2017Mateo MuñozNo ratings yet

- Annexure 1 SMDocument13 pagesAnnexure 1 SMNeeraj SinghNo ratings yet

- Massmart - Road To RecoveryDocument49 pagesMassmart - Road To RecoveryBusinessTech100% (2)

- Canara Robeco Small Cap Fund - NFO - Jan 2019Document35 pagesCanara Robeco Small Cap Fund - NFO - Jan 2019Rachana MakhijaNo ratings yet

- CB Industrial Product Berhad: Look To Better FY10 - 01/03/2010Document3 pagesCB Industrial Product Berhad: Look To Better FY10 - 01/03/2010Rhb InvestNo ratings yet

- Starbucks 2014 Investor Day - Financial OverviewDocument16 pagesStarbucks 2014 Investor Day - Financial OverviewCyn SyjucoNo ratings yet

- DH 847Document13 pagesDH 847rishab agarwalNo ratings yet

- 1Q18 Earnings Drop 49.9% Y/y On Lower Revenues, Below COL ForecastDocument6 pages1Q18 Earnings Drop 49.9% Y/y On Lower Revenues, Below COL ForecastMark Angelo BustosNo ratings yet

- MFIN Micrometer: (Data As of 31 March 2013)Document57 pagesMFIN Micrometer: (Data As of 31 March 2013)Diksha DuaNo ratings yet

- Escorts: Expectation of Significant Recovery Due To A Better Monsoon BuyDocument7 pagesEscorts: Expectation of Significant Recovery Due To A Better Monsoon BuynnsriniNo ratings yet

- Alembic Pharma - 4QFY19 - HDFC Sec-201905091034594285107Document10 pagesAlembic Pharma - 4QFY19 - HDFC Sec-201905091034594285107Ravikiran SuryanarayanamurthyNo ratings yet

- DHFL Corporate PPT q4 Fy17 PDFDocument52 pagesDHFL Corporate PPT q4 Fy17 PDFAkshay MehtaNo ratings yet

- Go Global - Vietnam - Final - May 10Document20 pagesGo Global - Vietnam - Final - May 10tran haNo ratings yet

- Hai-O Enterprise Berhad: MLM Division Slowdown Worse Than Expected - 30/09/2010Document3 pagesHai-O Enterprise Berhad: MLM Division Slowdown Worse Than Expected - 30/09/2010Rhb InvestNo ratings yet

- MDP - RatingsDocument4 pagesMDP - RatingsJeff SturgeonNo ratings yet

- Portfolio Analysis - FISHDocument1 pagePortfolio Analysis - FISHAkshay VrkNo ratings yet

- Pain Not Coming To An End Cut To Reduce: Bharti AirtelDocument17 pagesPain Not Coming To An End Cut To Reduce: Bharti AirtelAshokNo ratings yet

- Auto - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel BrokingDocument6 pagesAuto - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNo ratings yet

- IP SILO Results Note 171101Document6 pagesIP SILO Results Note 171101gloridoroNo ratings yet

- Amway (M) Holdings Berhad (Malaysia) : Look Forward To 2010 - 24/02/2010Document3 pagesAmway (M) Holdings Berhad (Malaysia) : Look Forward To 2010 - 24/02/2010Rhb InvestNo ratings yet

- Override - AOL Trading Tools v3.51 (Cost-Market Value Overide)Document101 pagesOverride - AOL Trading Tools v3.51 (Cost-Market Value Overide)Erjohn PapaNo ratings yet

- Mps LTD: Moderate Topline Growth, Margins Impacted Due To Stronger RupeeDocument6 pagesMps LTD: Moderate Topline Growth, Margins Impacted Due To Stronger RupeeAbhijit TripathiNo ratings yet

- FSM Islamic Managed Portfolio: ConservativeDocument1 pageFSM Islamic Managed Portfolio: ConservativePhua Kien HanNo ratings yet

- Mansa-X KES Fact Sheet Q1 2023Document1 pageMansa-X KES Fact Sheet Q1 2023KevinNo ratings yet

- RC 2020 Winning Presentation University of SydneyDocument21 pagesRC 2020 Winning Presentation University of SydneySaksham KalraNo ratings yet

- Bajaj Auto: Spectacular Set of NumbersDocument4 pagesBajaj Auto: Spectacular Set of Numberssabharwalssss7313No ratings yet

- Sundaram Finance - Q4FY23 Result Update - 15062023 - 15!06!2023 - 11Document9 pagesSundaram Finance - Q4FY23 Result Update - 15062023 - 15!06!2023 - 11Sanjeedeep Mishra , 315No ratings yet

- Learning Brochures OPMDocument18 pagesLearning Brochures OPMratan203No ratings yet

- FTF AsitDocument25 pagesFTF Asitratan203100% (2)

- NPS Contribution Form PDFDocument1 pageNPS Contribution Form PDFratan203No ratings yet

- DB Structure Pivot EtcDocument14 pagesDB Structure Pivot Etcratan203No ratings yet

- SCMA 632 SyllabusDocument1 pageSCMA 632 Syllabusratan203No ratings yet

- Exponential SmoothingDocument5 pagesExponential Smoothingratan203No ratings yet

- National Pension System (NPS) : Subscriber Registration Form (All Citizen Model) eNPS FormDocument5 pagesNational Pension System (NPS) : Subscriber Registration Form (All Citizen Model) eNPS Formratan203No ratings yet

- Reliance Capital (RELCAP) : Businesses Growing, Return Ratios ImprovingDocument15 pagesReliance Capital (RELCAP) : Businesses Growing, Return Ratios Improvingratan203No ratings yet

- Aksharchem Annual Report 2011-12Document53 pagesAksharchem Annual Report 2011-12ratan203No ratings yet

- M3665 MathGambing TalkDocument26 pagesM3665 MathGambing Talkratan203No ratings yet

- Q4FY17 Earnings Report Reliance Capital LTD: Operating Income Ppop PAT Margin Net ProfitDocument5 pagesQ4FY17 Earnings Report Reliance Capital LTD: Operating Income Ppop PAT Margin Net Profitratan203No ratings yet

- TCS Buyback Opportunity To Earn Around 13% in 3 Months (62% Annualized)Document4 pagesTCS Buyback Opportunity To Earn Around 13% in 3 Months (62% Annualized)ratan203No ratings yet

- Fortis Healthcare: Performance In-Line With ExpectationsDocument13 pagesFortis Healthcare: Performance In-Line With Expectationsratan203No ratings yet

- Fortis Healthcare: Performance In-Line With ExpectationsDocument13 pagesFortis Healthcare: Performance In-Line With Expectationsratan203No ratings yet

- Piramal Ar Full 2015 16 PDFDocument292 pagesPiramal Ar Full 2015 16 PDFratan203No ratings yet

- Piramal Enterprises Limited Investor Presentation Nov 2016 20161108025005Document74 pagesPiramal Enterprises Limited Investor Presentation Nov 2016 20161108025005ratan203No ratings yet

- PPAPAnnual Report2014 15Document76 pagesPPAPAnnual Report2014 15ratan203No ratings yet

- Sir Philip KotlerDocument2 pagesSir Philip KotlerBALRAJNo ratings yet

- Business in Action 6th Edition Bovee Solutions ManualDocument16 pagesBusiness in Action 6th Edition Bovee Solutions ManualAshleyJonescapsr100% (10)

- Kinesis WhitepaperDocument25 pagesKinesis WhitepaperR-K-MNo ratings yet

- Leveraged Buyouts in IndiaDocument60 pagesLeveraged Buyouts in IndiaParang MehtaNo ratings yet

- DPR Cashew AgartalaDocument18 pagesDPR Cashew AgartalaSiddu RhNo ratings yet

- Chapter 5Document3 pagesChapter 5karen weeNo ratings yet

- Media Planning and StrategyDocument31 pagesMedia Planning and StrategyjaydmpatelNo ratings yet

- Historical VAR Calculation ExampleDocument17 pagesHistorical VAR Calculation ExampleAbhinav JainNo ratings yet

- Business Management Notes PDFDocument63 pagesBusiness Management Notes PDFRofhiwa RamahalaNo ratings yet

- Kenneth Shaleen Technical Analysis and Options StrategiesDocument238 pagesKenneth Shaleen Technical Analysis and Options StrategiesAlexandre Navarro100% (1)

- Competitive Strategies of Investment Banks - FIN 433 - SEC-07Document22 pagesCompetitive Strategies of Investment Banks - FIN 433 - SEC-07Jannatul TrishiNo ratings yet

- Cost of Capital - HimaksheeDocument38 pagesCost of Capital - HimaksheeHimakshee BhagawatiNo ratings yet

- 12 Days of Joy: Countdown ToDocument1 page12 Days of Joy: Countdown ToCynthia GonzalezNo ratings yet

- Science and Technology Competitiveness Rankings of The Philippines (2012 - 2018)Document39 pagesScience and Technology Competitiveness Rankings of The Philippines (2012 - 2018)Hani SalazarNo ratings yet

- 2 Grade 7 TLE Environment and MarketDocument31 pages2 Grade 7 TLE Environment and Marketmegumi deniegaNo ratings yet

- Coffee Shops Thesis WIT With InstrumentDocument50 pagesCoffee Shops Thesis WIT With InstrumentJullienne PasaporteNo ratings yet

- 12 OnScreen B1 Quiz 6BDocument2 pages12 OnScreen B1 Quiz 6BМануляк ЛевNo ratings yet

- Fin 416 Exam 2 Spring 2012Document4 pagesFin 416 Exam 2 Spring 2012fakeone23No ratings yet

- CRM 9.0 Customer Data ModelDocument1 pageCRM 9.0 Customer Data ModelVinay KuchanaNo ratings yet

- Government of Telangana - Indian School of Business TRI Entrepreneurship Programme Detailed Project Report Submitted by Name: Student NumberDocument20 pagesGovernment of Telangana - Indian School of Business TRI Entrepreneurship Programme Detailed Project Report Submitted by Name: Student Numbersoma naikNo ratings yet

- GST and Indirect TaxDocument5 pagesGST and Indirect Taxsarthak13112004No ratings yet

- Review For ADMS 1000 Final ExamDocument8 pagesReview For ADMS 1000 Final ExamYork Exams67% (3)

- Applied Economics-Q3-Module-5Document17 pagesApplied Economics-Q3-Module-5Jomar BenedicoNo ratings yet

- Money Banking and The Financial System 3rd Edition Hubbard Test BankDocument39 pagesMoney Banking and The Financial System 3rd Edition Hubbard Test Bankelizabethbauermddiqznotwsf100% (16)

- Value Chain in Health Care IndustryDocument20 pagesValue Chain in Health Care IndustrydddddeeeeeNo ratings yet

- Innovative Lesson Plan CommerceDocument6 pagesInnovative Lesson Plan CommerceREMYA RAMACHANDRAN NAIR100% (3)

- Production and Cost Analysis: Trogo, Cyryll Ice Diamante, Rickony Huerto, AndreaDocument49 pagesProduction and Cost Analysis: Trogo, Cyryll Ice Diamante, Rickony Huerto, AndreaJohn Stephen EusebioNo ratings yet

- Prospects & Future of Integrated Marketing Communication Techniques in Global Marketing ServicesDocument6 pagesProspects & Future of Integrated Marketing Communication Techniques in Global Marketing ServicesarcherselevatorsNo ratings yet

Download as pdf or txt

You might also like

- ICT One Trade Setup For Life Notes TinyVizsla-1Document3 pagesICT One Trade Setup For Life Notes TinyVizsla-1agathfuture100% (1)

- Algo Convention 2021 ScheduleDocument2 pagesAlgo Convention 2021 SchedulePhani KrishnaNo ratings yet

- Raymond Initiating CoverageDocument20 pagesRaymond Initiating Coveragenarayanan_rNo ratings yet

- Driving Growth: Revenue From Operations Ebitda PATDocument2 pagesDriving Growth: Revenue From Operations Ebitda PATBlueHexNo ratings yet

- Sheela Foam LTD - Initiaiting Coverage - 18092018 - 19!09!2018 - 08Document32 pagesSheela Foam LTD - Initiaiting Coverage - 18092018 - 19!09!2018 - 08Mansi Raut PatilNo ratings yet

- Below Expectations: UMW HoldingsDocument11 pagesBelow Expectations: UMW HoldingskufaizNo ratings yet

- Stock Performance of Obour Land For Food Industries (OLFI - EGY)Document1 pageStock Performance of Obour Land For Food Industries (OLFI - EGY)body.helal2001No ratings yet

- PMS Guide August 2019Document88 pagesPMS Guide August 2019HetanshNo ratings yet

- JK Cement: Key Financial Highlights (2018-19)Document1 pageJK Cement: Key Financial Highlights (2018-19)KpNo ratings yet

- Viacom Reports Second Quarter Results: Statement From Bob Bakish, President & CeoDocument14 pagesViacom Reports Second Quarter Results: Statement From Bob Bakish, President & CeoNickALiveNo ratings yet

- Vietnam Ho Chi Minh City Office Q2 2019 PDFDocument2 pagesVietnam Ho Chi Minh City Office Q2 2019 PDFNguyen Quang MinhNo ratings yet

- Paris Air Show Boeing 2019Document26 pagesParis Air Show Boeing 2019Sani SanjayaNo ratings yet

- Chugging Along: Reliance IndustriesDocument12 pagesChugging Along: Reliance IndustriesAshokNo ratings yet

- Berger Paints (India) Limited 21 QuarterUpdateDocument7 pagesBerger Paints (India) Limited 21 QuarterUpdatevikasaggarwal01No ratings yet

- Jakarta Retail 2q17Document2 pagesJakarta Retail 2q17ainia putriNo ratings yet

- Kantar Worldpanel FMCG Monitor Dec 2018 enDocument9 pagesKantar Worldpanel FMCG Monitor Dec 2018 enAnh Nguyen TranNo ratings yet

- Margin Concerns Should Take Precedence Over Improved OutlookDocument15 pagesMargin Concerns Should Take Precedence Over Improved Outlookashok yadavNo ratings yet

- Boi Asean q3 2015 BookletDocument27 pagesBoi Asean q3 2015 BookletSteven SutantoNo ratings yet

- Ambit Capital - Agri Inputs - Diverging Growth Rates (Sector Update) (POSITIVE)Document65 pagesAmbit Capital - Agri Inputs - Diverging Growth Rates (Sector Update) (POSITIVE)Davuluri OmprakashNo ratings yet

- Realty and The Second Wave: SpeakersDocument23 pagesRealty and The Second Wave: SpeakersAshutosh PatidarNo ratings yet

- FC Installment CardDocument1 pageFC Installment CardKristelNavarroNo ratings yet

- RHB Report My - Alliance Bank - Results Preview - 20190813 - RHB 92390246692298925d512480e5e00Document7 pagesRHB Report My - Alliance Bank - Results Preview - 20190813 - RHB 92390246692298925d512480e5e00Leow Ann HongNo ratings yet

- Pt. Gs Gold Shine Battery: Nama Karyawa: TRI HANDOKO Jabatan: Director Company Perform - Jan 19Document3 pagesPt. Gs Gold Shine Battery: Nama Karyawa: TRI HANDOKO Jabatan: Director Company Perform - Jan 19Nia TjhoaNo ratings yet

- Group Accounts BasicsDocument1 pageGroup Accounts BasicsVaishnavi ChaturvediNo ratings yet

- Fund Manager Report November 2019: NBP FundsDocument17 pagesFund Manager Report November 2019: NBP FundsTaha SaleemNo ratings yet

- CCL Products - Initiating Coverage - 09092019 - 11!09!2019 - 08Document29 pagesCCL Products - Initiating Coverage - 09092019 - 11!09!2019 - 08Amit PatelNo ratings yet

- US BN: Key Findings: Pe DealsDocument1 pageUS BN: Key Findings: Pe DealsethernalxNo ratings yet

- Tata Consultancy Services (TCS) : NeutralDocument8 pagesTata Consultancy Services (TCS) : Neutraltdog66No ratings yet

- Jiten SahuDocument36 pagesJiten SahuMirza Aftab BaigNo ratings yet

- Idr Bjfin@in 091115 105311Document68 pagesIdr Bjfin@in 091115 105311NikhilKapoor29No ratings yet

- Reduce: Bharti Infratel Bhin inDocument11 pagesReduce: Bharti Infratel Bhin inashok yadavNo ratings yet

- Automotive Axles LTDDocument25 pagesAutomotive Axles LTDLK CoolgirlNo ratings yet

- Avianca Holdings BTGPactual 2017Document7 pagesAvianca Holdings BTGPactual 2017Mateo MuñozNo ratings yet

- Annexure 1 SMDocument13 pagesAnnexure 1 SMNeeraj SinghNo ratings yet

- Massmart - Road To RecoveryDocument49 pagesMassmart - Road To RecoveryBusinessTech100% (2)

- Canara Robeco Small Cap Fund - NFO - Jan 2019Document35 pagesCanara Robeco Small Cap Fund - NFO - Jan 2019Rachana MakhijaNo ratings yet

- CB Industrial Product Berhad: Look To Better FY10 - 01/03/2010Document3 pagesCB Industrial Product Berhad: Look To Better FY10 - 01/03/2010Rhb InvestNo ratings yet

- Starbucks 2014 Investor Day - Financial OverviewDocument16 pagesStarbucks 2014 Investor Day - Financial OverviewCyn SyjucoNo ratings yet

- DH 847Document13 pagesDH 847rishab agarwalNo ratings yet

- 1Q18 Earnings Drop 49.9% Y/y On Lower Revenues, Below COL ForecastDocument6 pages1Q18 Earnings Drop 49.9% Y/y On Lower Revenues, Below COL ForecastMark Angelo BustosNo ratings yet

- MFIN Micrometer: (Data As of 31 March 2013)Document57 pagesMFIN Micrometer: (Data As of 31 March 2013)Diksha DuaNo ratings yet

- Escorts: Expectation of Significant Recovery Due To A Better Monsoon BuyDocument7 pagesEscorts: Expectation of Significant Recovery Due To A Better Monsoon BuynnsriniNo ratings yet

- Alembic Pharma - 4QFY19 - HDFC Sec-201905091034594285107Document10 pagesAlembic Pharma - 4QFY19 - HDFC Sec-201905091034594285107Ravikiran SuryanarayanamurthyNo ratings yet

- DHFL Corporate PPT q4 Fy17 PDFDocument52 pagesDHFL Corporate PPT q4 Fy17 PDFAkshay MehtaNo ratings yet

- Go Global - Vietnam - Final - May 10Document20 pagesGo Global - Vietnam - Final - May 10tran haNo ratings yet

- Hai-O Enterprise Berhad: MLM Division Slowdown Worse Than Expected - 30/09/2010Document3 pagesHai-O Enterprise Berhad: MLM Division Slowdown Worse Than Expected - 30/09/2010Rhb InvestNo ratings yet

- MDP - RatingsDocument4 pagesMDP - RatingsJeff SturgeonNo ratings yet

- Portfolio Analysis - FISHDocument1 pagePortfolio Analysis - FISHAkshay VrkNo ratings yet

- Pain Not Coming To An End Cut To Reduce: Bharti AirtelDocument17 pagesPain Not Coming To An End Cut To Reduce: Bharti AirtelAshokNo ratings yet

- Auto - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel BrokingDocument6 pagesAuto - Company Profile, Performance Update, Balance Sheet & Key Ratios - Angel Brokingmoisha sharmaNo ratings yet

- IP SILO Results Note 171101Document6 pagesIP SILO Results Note 171101gloridoroNo ratings yet

- Amway (M) Holdings Berhad (Malaysia) : Look Forward To 2010 - 24/02/2010Document3 pagesAmway (M) Holdings Berhad (Malaysia) : Look Forward To 2010 - 24/02/2010Rhb InvestNo ratings yet

- Override - AOL Trading Tools v3.51 (Cost-Market Value Overide)Document101 pagesOverride - AOL Trading Tools v3.51 (Cost-Market Value Overide)Erjohn PapaNo ratings yet

- Mps LTD: Moderate Topline Growth, Margins Impacted Due To Stronger RupeeDocument6 pagesMps LTD: Moderate Topline Growth, Margins Impacted Due To Stronger RupeeAbhijit TripathiNo ratings yet

- FSM Islamic Managed Portfolio: ConservativeDocument1 pageFSM Islamic Managed Portfolio: ConservativePhua Kien HanNo ratings yet

- Mansa-X KES Fact Sheet Q1 2023Document1 pageMansa-X KES Fact Sheet Q1 2023KevinNo ratings yet

- RC 2020 Winning Presentation University of SydneyDocument21 pagesRC 2020 Winning Presentation University of SydneySaksham KalraNo ratings yet

- Bajaj Auto: Spectacular Set of NumbersDocument4 pagesBajaj Auto: Spectacular Set of Numberssabharwalssss7313No ratings yet

- Sundaram Finance - Q4FY23 Result Update - 15062023 - 15!06!2023 - 11Document9 pagesSundaram Finance - Q4FY23 Result Update - 15062023 - 15!06!2023 - 11Sanjeedeep Mishra , 315No ratings yet

- Learning Brochures OPMDocument18 pagesLearning Brochures OPMratan203No ratings yet

- FTF AsitDocument25 pagesFTF Asitratan203100% (2)

- NPS Contribution Form PDFDocument1 pageNPS Contribution Form PDFratan203No ratings yet

- DB Structure Pivot EtcDocument14 pagesDB Structure Pivot Etcratan203No ratings yet

- SCMA 632 SyllabusDocument1 pageSCMA 632 Syllabusratan203No ratings yet

- Exponential SmoothingDocument5 pagesExponential Smoothingratan203No ratings yet

- National Pension System (NPS) : Subscriber Registration Form (All Citizen Model) eNPS FormDocument5 pagesNational Pension System (NPS) : Subscriber Registration Form (All Citizen Model) eNPS Formratan203No ratings yet

- Reliance Capital (RELCAP) : Businesses Growing, Return Ratios ImprovingDocument15 pagesReliance Capital (RELCAP) : Businesses Growing, Return Ratios Improvingratan203No ratings yet

- Aksharchem Annual Report 2011-12Document53 pagesAksharchem Annual Report 2011-12ratan203No ratings yet

- M3665 MathGambing TalkDocument26 pagesM3665 MathGambing Talkratan203No ratings yet

- Q4FY17 Earnings Report Reliance Capital LTD: Operating Income Ppop PAT Margin Net ProfitDocument5 pagesQ4FY17 Earnings Report Reliance Capital LTD: Operating Income Ppop PAT Margin Net Profitratan203No ratings yet

- TCS Buyback Opportunity To Earn Around 13% in 3 Months (62% Annualized)Document4 pagesTCS Buyback Opportunity To Earn Around 13% in 3 Months (62% Annualized)ratan203No ratings yet

- Fortis Healthcare: Performance In-Line With ExpectationsDocument13 pagesFortis Healthcare: Performance In-Line With Expectationsratan203No ratings yet

- Fortis Healthcare: Performance In-Line With ExpectationsDocument13 pagesFortis Healthcare: Performance In-Line With Expectationsratan203No ratings yet

- Piramal Ar Full 2015 16 PDFDocument292 pagesPiramal Ar Full 2015 16 PDFratan203No ratings yet

- Piramal Enterprises Limited Investor Presentation Nov 2016 20161108025005Document74 pagesPiramal Enterprises Limited Investor Presentation Nov 2016 20161108025005ratan203No ratings yet

- PPAPAnnual Report2014 15Document76 pagesPPAPAnnual Report2014 15ratan203No ratings yet

- Sir Philip KotlerDocument2 pagesSir Philip KotlerBALRAJNo ratings yet

- Business in Action 6th Edition Bovee Solutions ManualDocument16 pagesBusiness in Action 6th Edition Bovee Solutions ManualAshleyJonescapsr100% (10)

- Kinesis WhitepaperDocument25 pagesKinesis WhitepaperR-K-MNo ratings yet

- Leveraged Buyouts in IndiaDocument60 pagesLeveraged Buyouts in IndiaParang MehtaNo ratings yet

- DPR Cashew AgartalaDocument18 pagesDPR Cashew AgartalaSiddu RhNo ratings yet

- Chapter 5Document3 pagesChapter 5karen weeNo ratings yet

- Media Planning and StrategyDocument31 pagesMedia Planning and StrategyjaydmpatelNo ratings yet

- Historical VAR Calculation ExampleDocument17 pagesHistorical VAR Calculation ExampleAbhinav JainNo ratings yet

- Business Management Notes PDFDocument63 pagesBusiness Management Notes PDFRofhiwa RamahalaNo ratings yet

- Kenneth Shaleen Technical Analysis and Options StrategiesDocument238 pagesKenneth Shaleen Technical Analysis and Options StrategiesAlexandre Navarro100% (1)

- Competitive Strategies of Investment Banks - FIN 433 - SEC-07Document22 pagesCompetitive Strategies of Investment Banks - FIN 433 - SEC-07Jannatul TrishiNo ratings yet

- Cost of Capital - HimaksheeDocument38 pagesCost of Capital - HimaksheeHimakshee BhagawatiNo ratings yet

- 12 Days of Joy: Countdown ToDocument1 page12 Days of Joy: Countdown ToCynthia GonzalezNo ratings yet

- Science and Technology Competitiveness Rankings of The Philippines (2012 - 2018)Document39 pagesScience and Technology Competitiveness Rankings of The Philippines (2012 - 2018)Hani SalazarNo ratings yet

- 2 Grade 7 TLE Environment and MarketDocument31 pages2 Grade 7 TLE Environment and Marketmegumi deniegaNo ratings yet

- Coffee Shops Thesis WIT With InstrumentDocument50 pagesCoffee Shops Thesis WIT With InstrumentJullienne PasaporteNo ratings yet

- 12 OnScreen B1 Quiz 6BDocument2 pages12 OnScreen B1 Quiz 6BМануляк ЛевNo ratings yet

- Fin 416 Exam 2 Spring 2012Document4 pagesFin 416 Exam 2 Spring 2012fakeone23No ratings yet

- CRM 9.0 Customer Data ModelDocument1 pageCRM 9.0 Customer Data ModelVinay KuchanaNo ratings yet

- Government of Telangana - Indian School of Business TRI Entrepreneurship Programme Detailed Project Report Submitted by Name: Student NumberDocument20 pagesGovernment of Telangana - Indian School of Business TRI Entrepreneurship Programme Detailed Project Report Submitted by Name: Student Numbersoma naikNo ratings yet

- GST and Indirect TaxDocument5 pagesGST and Indirect Taxsarthak13112004No ratings yet

- Review For ADMS 1000 Final ExamDocument8 pagesReview For ADMS 1000 Final ExamYork Exams67% (3)

- Applied Economics-Q3-Module-5Document17 pagesApplied Economics-Q3-Module-5Jomar BenedicoNo ratings yet

- Money Banking and The Financial System 3rd Edition Hubbard Test BankDocument39 pagesMoney Banking and The Financial System 3rd Edition Hubbard Test Bankelizabethbauermddiqznotwsf100% (16)

- Value Chain in Health Care IndustryDocument20 pagesValue Chain in Health Care IndustrydddddeeeeeNo ratings yet

- Innovative Lesson Plan CommerceDocument6 pagesInnovative Lesson Plan CommerceREMYA RAMACHANDRAN NAIR100% (3)

- Production and Cost Analysis: Trogo, Cyryll Ice Diamante, Rickony Huerto, AndreaDocument49 pagesProduction and Cost Analysis: Trogo, Cyryll Ice Diamante, Rickony Huerto, AndreaJohn Stephen EusebioNo ratings yet

- Prospects & Future of Integrated Marketing Communication Techniques in Global Marketing ServicesDocument6 pagesProspects & Future of Integrated Marketing Communication Techniques in Global Marketing ServicesarcherselevatorsNo ratings yet