Download as xls, pdf, or txt

You might also like

- Chapter 6 - Financial AccountingDocument10 pagesChapter 6 - Financial AccountingLinh BùiNo ratings yet

- FM11 CH 12 Mini CaseDocument14 pagesFM11 CH 12 Mini CaseRahul Rathi100% (1)

- Methods of Payment in International TradeDocument18 pagesMethods of Payment in International Tradeshravan.bhumkar100% (1)

- NPV, Internal Rate of Return (IRR), and The Profitability Index (PI)Document24 pagesNPV, Internal Rate of Return (IRR), and The Profitability Index (PI)Sumbul JavedNo ratings yet

- FM16 Ch26 Tool KitDocument21 pagesFM16 Ch26 Tool KitAdamNo ratings yet

- 5 Property Discount Rate PassuggDocument21 pages5 Property Discount Rate PassuggLeon M. EggerNo ratings yet

- Final Exam Practice Papers SolutionsDocument31 pagesFinal Exam Practice Papers Solutionssamuel ngNo ratings yet

- Ch25 Tool KitDocument35 pagesCh25 Tool KitJITIN ARORANo ratings yet

- Ditta Shierlly Novierra - Minicase Conch Republic Electronics, Part 2Document36 pagesDitta Shierlly Novierra - Minicase Conch Republic Electronics, Part 2Ummaya MalikNo ratings yet

- Net Present Value and Other Investment RulesDocument34 pagesNet Present Value and Other Investment Ruleskristina niaNo ratings yet

- Net Present Value and Other Investment Rules: Mcgraw-Hill/IrwinDocument34 pagesNet Present Value and Other Investment Rules: Mcgraw-Hill/IrwinQUYÊN PHAN ĐÌNH PHƯƠNGNo ratings yet

- Ch26 Tool KitADocument21 pagesCh26 Tool KitARoy HemenwayNo ratings yet

- Chap 005Document34 pagesChap 005NazifahNo ratings yet

- NPV Yang DiperkirakanDocument34 pagesNPV Yang Diperkirakanalda warsidaNo ratings yet

- Net Present Value and Other Investment RulesDocument34 pagesNet Present Value and Other Investment RulesArviandi AntariksaNo ratings yet

- Chapter 05 Net Present Value and Other Investment Rules PDFDocument35 pagesChapter 05 Net Present Value and Other Investment Rules PDFWan Maulana AkbarNo ratings yet

- Project Evaluation TechniquesDocument30 pagesProject Evaluation TechniquesMujeeb KhanNo ratings yet

- Net Present Value and Other Investment Rules: Mcgraw-Hill/IrwinDocument32 pagesNet Present Value and Other Investment Rules: Mcgraw-Hill/IrwinASAD ULLAHNo ratings yet

- NPVDocument36 pagesNPVjohn onesmoNo ratings yet

- Real Options Teaching NotesDocument11 pagesReal Options Teaching NotesTwinkle ChettriNo ratings yet

- Some Alternative Investment Rules: Corporate FinanceDocument27 pagesSome Alternative Investment Rules: Corporate FinanceNguyễn Thùy LinhNo ratings yet

- Busn 233 CH 08Document101 pagesBusn 233 CH 08Pramod VasudevNo ratings yet

- S16 - Scenario Manager - NPV - ClassDocument11 pagesS16 - Scenario Manager - NPV - ClassABHAY VEER SINGHNo ratings yet

- Week 1 Homework Suggested Solution-1Document6 pagesWeek 1 Homework Suggested Solution-1Mr. JarmenNo ratings yet

- Risk Analysis, Real Options, and Capital BudgetingDocument32 pagesRisk Analysis, Real Options, and Capital BudgetinghaikalNo ratings yet

- Risk Analysis in Capital Investment DecisionsDocument57 pagesRisk Analysis in Capital Investment Decisionsanindya_kundu100% (1)

- Sensitivity Analysis: Mine Valuation - Spring 2016 1Document47 pagesSensitivity Analysis: Mine Valuation - Spring 2016 1pedroNo ratings yet

- CH 6 STDDocument49 pagesCH 6 STDKinjal ShethiaNo ratings yet

- Net Present Value and Other Investment RulesDocument30 pagesNet Present Value and Other Investment RulesSyedAunRazaRizviNo ratings yet

- Project A: Question 1 AnswerDocument6 pagesProject A: Question 1 AnswerShafiqUr RehmanNo ratings yet

- Chap5 ModifiedDocument42 pagesChap5 ModifiedRuba AwwadNo ratings yet

- Brealey - Principles of Corporate Finance - 13e - Chap05 - SMDocument11 pagesBrealey - Principles of Corporate Finance - 13e - Chap05 - SMpt94jykqvqNo ratings yet

- Scenario & Sensitivity AnalysisDocument4 pagesScenario & Sensitivity AnalysisYasir RahimNo ratings yet

- IrrDocument5 pagesIrrMohmet SaitNo ratings yet

- Chap 007Document32 pagesChap 007NazifahNo ratings yet

- Answers To Problem Sets: Net Present Value and Other Investment CriteriaDocument9 pagesAnswers To Problem Sets: Net Present Value and Other Investment CriteriaTracywongNo ratings yet

- Laura Leticia López Aguilar Activiti 1 Capital BudgetingDocument2 pagesLaura Leticia López Aguilar Activiti 1 Capital BudgetingLets A LopezNo ratings yet

- Chapter - 5 Capital BudgetingDocument9 pagesChapter - 5 Capital BudgetingShuvro RahmanNo ratings yet

- NPV and IRRDocument45 pagesNPV and IRRicejanicewongNo ratings yet

- Full Updated Solution of The Finance Mid TermDocument12 pagesFull Updated Solution of The Finance Mid TermAhmed Ezzat Ali100% (1)

- 5 - NPV vs. Internal Rate of Return (IRR)Document7 pages5 - NPV vs. Internal Rate of Return (IRR)Josh AckmanNo ratings yet

- Assignment 2 Group 101 291018Document9 pagesAssignment 2 Group 101 291018Linh ChiNo ratings yet

- Lecture 2Document10 pagesLecture 2Na ViNo ratings yet

- Capital Budgeting WorkShop 2 2020-1Document3 pagesCapital Budgeting WorkShop 2 2020-1Valentina Barreto Puerta0% (1)

- UMGC Finance HW #4Document9 pagesUMGC Finance HW #4Kimora BrockNo ratings yet

- Future Value of MoneyDocument11 pagesFuture Value of Moneyaymanmomani2111No ratings yet

- Chapter 2 - How To Calculate Present ValuesDocument21 pagesChapter 2 - How To Calculate Present ValuesTrọng PhạmNo ratings yet

- 8.1. Investment Criteria: Year Cash Flow PVDocument11 pages8.1. Investment Criteria: Year Cash Flow PVMichelle Miranda HernándezNo ratings yet

- Capital Budgeting 3Document16 pagesCapital Budgeting 3Varun TandonNo ratings yet

- MKM704 - Finance For Marketers - Lab 4 Solution: MKM704 - DR Page 1 of 3 02/18/2022 at 22:03:08Document3 pagesMKM704 - Finance For Marketers - Lab 4 Solution: MKM704 - DR Page 1 of 3 02/18/2022 at 22:03:08VarunNo ratings yet

- 2.1 - Swaps, Bridge To SwapsDocument56 pages2.1 - Swaps, Bridge To SwapscutehibouxNo ratings yet

- The Time Value of MoneyDocument69 pagesThe Time Value of Moneymarine19.vedelNo ratings yet

- Bond ValuationDocument17 pagesBond ValuationMatthew RyanNo ratings yet

- MM 5007 - Financial Management - Mid Term PDFDocument33 pagesMM 5007 - Financial Management - Mid Term PDFA. HanifahNo ratings yet

- Assignment 1 (Final Edition)Document62 pagesAssignment 1 (Final Edition)Sameer AsifNo ratings yet

- Some Alternative Investment RulesDocument32 pagesSome Alternative Investment RulesI Gede Artha WijayaNo ratings yet

- 120 16 Chapter 17 TimeValueofMoneyDocument12 pages120 16 Chapter 17 TimeValueofMoneyHrvoje ErorNo ratings yet

- Capital Budgeting: Part I Investment CriteriaDocument49 pagesCapital Budgeting: Part I Investment Criteriarani namdevNo ratings yet

- IRR and PaybackDocument10 pagesIRR and Paybackkfir goldburdNo ratings yet

- Penghitungan Pertemuan #9Document2 pagesPenghitungan Pertemuan #9yamatoNo ratings yet

- Time Value of Money NotesDocument16 pagesTime Value of Money NotesAssassin Panda14No ratings yet

- Math Practice Simplified: Money & Measurement (Book K): Applying Skills to Problems Dealing with Money and MeasurementFrom EverandMath Practice Simplified: Money & Measurement (Book K): Applying Skills to Problems Dealing with Money and MeasurementNo ratings yet

- Applying Total Quality ManagementDocument6 pagesApplying Total Quality ManagementRand Al-akamNo ratings yet

- Chap 028Document12 pagesChap 028Rand Al-akam100% (1)

- CH 21Document7 pagesCH 21Rand Al-akamNo ratings yet

- Chapter 13: Capital Structure and Leverage Comprehensive/Spreadsheet Problem 1Document26 pagesChapter 13: Capital Structure and Leverage Comprehensive/Spreadsheet Problem 1Rand Al-akamNo ratings yet

- Required: Using These Data, Construct The December 31, Year 5 Balance Sheet For Your AnalysisDocument3 pagesRequired: Using These Data, Construct The December 31, Year 5 Balance Sheet For Your AnalysisJARED DARREN ONGNo ratings yet

- Hedging Cash Balance UncertaintiesDocument11 pagesHedging Cash Balance UncertaintiesAditya100% (1)

- International Banking: Department of MBLDocument7 pagesInternational Banking: Department of MBLnurulbibmNo ratings yet

- Bonds Market in PakistanDocument26 pagesBonds Market in PakistanSumanSohailNo ratings yet

- AXIS Bank RTGS & NEFT FormDocument11 pagesAXIS Bank RTGS & NEFT FormNeha JunejaNo ratings yet

- SaaS Capital Overview 2018 PDFDocument2 pagesSaaS Capital Overview 2018 PDFAnonymous 68LoXZHRHiNo ratings yet

- Chapter 4: Bond Market Instruments: Financial Markets and Institutions Chapter 4 1Document49 pagesChapter 4: Bond Market Instruments: Financial Markets and Institutions Chapter 4 1AykaNo ratings yet

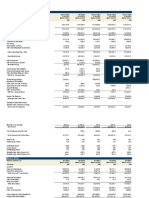

- Currency INR INR INR INR INR: Income StatementDocument26 pagesCurrency INR INR INR INR INR: Income StatementNikhil BhatiaNo ratings yet

- Pre FinalDocument8 pagesPre Finalpdmallari12No ratings yet

- Part Time Jobs For High School Students: Maninder Singh 10th Oct, 2019Document3 pagesPart Time Jobs For High School Students: Maninder Singh 10th Oct, 2019Maninder SinghNo ratings yet

- Module 03 - Financial ForecastingDocument59 pagesModule 03 - Financial ForecastingEUNICE LAYNE AGCONo ratings yet

- Quiz 1Document9 pagesQuiz 1Czarhiena SantiagoNo ratings yet

- Maths Mania # 053: DIRECTIONS: For The Following Questions, Four Options Are Given. Choose The Correct OptionDocument3 pagesMaths Mania # 053: DIRECTIONS: For The Following Questions, Four Options Are Given. Choose The Correct OptionTUSHAR JALANNo ratings yet

- Bizmanualz Finance Policies and Procedures SampleDocument9 pagesBizmanualz Finance Policies and Procedures SampleYe PhoneNo ratings yet

- Investments Questions For Review of Key Topics: Question 8-1Document85 pagesInvestments Questions For Review of Key Topics: Question 8-1kean ebeoNo ratings yet

- LUXTRADEDocument2 pagesLUXTRADEBigmanNo ratings yet

- R&R Swot PestleDocument5 pagesR&R Swot Pestle4696506No ratings yet

- Net Worth Summary: Enter Your Name HereDocument9 pagesNet Worth Summary: Enter Your Name HereKalaisejiane AthmalingameNo ratings yet

- Investment & Gambling: Asst - Prof .Seena Alappatt Dept of Management StudiesDocument24 pagesInvestment & Gambling: Asst - Prof .Seena Alappatt Dept of Management Studiesseena15No ratings yet

- Ankita Final Report On RDCDocument97 pagesAnkita Final Report On RDCMayank SarpadadiyaNo ratings yet

- Nikhat ParveenDocument87 pagesNikhat ParveenHarshit KashyapNo ratings yet

- Activity Fund Manual 2023-24Document20 pagesActivity Fund Manual 2023-24Kevan DunkelbergNo ratings yet

- 10 Chapter 3Document42 pages10 Chapter 3SANJU8795No ratings yet

- Sapm 4Document12 pagesSapm 4Sweet tripathiNo ratings yet

- Profit Sharing AhmadimadoDocument11 pagesProfit Sharing AhmadimadoGalauMarkumNo ratings yet

- 5th Week Assignment of Advanced Academic WritingDocument10 pages5th Week Assignment of Advanced Academic Writing1988inggrisNo ratings yet

- Does PPP Eliminate Concerns About Long Term Exchange Rate RiskDocument1 pageDoes PPP Eliminate Concerns About Long Term Exchange Rate Risktrilocksp SinghNo ratings yet

- Commercial Invoice Pakistan.Document1 pageCommercial Invoice Pakistan.hikamuddin38No ratings yet