Download as docx, pdf, or txt

You might also like

- Cfo Guidebook PDFDocument10 pagesCfo Guidebook PDFSrinivasa Rao AsuruNo ratings yet

- 2013 Pan European Private Equity Performance Benchmarks Study Evca Thomson Reuters Final VersionDocument28 pages2013 Pan European Private Equity Performance Benchmarks Study Evca Thomson Reuters Final VersionAbdullah HassanNo ratings yet

- Does Auditors' Reputation Discourage' Related-Party Transactions The French CaseDocument48 pagesDoes Auditors' Reputation Discourage' Related-Party Transactions The French CaseFelipe Augusto CuryNo ratings yet

- CinépolisDocument6 pagesCinépolismemowebberNo ratings yet

- Kenmore 385.19110 Sewing Machine ManualDocument83 pagesKenmore 385.19110 Sewing Machine ManualWendy HawaNo ratings yet

- Narrative Reporting DisclosuresDocument10 pagesNarrative Reporting DisclosuresMd. Abdul Momen JibonNo ratings yet

- SssssssDocument25 pagesSssssssdoiNo ratings yet

- A Transparency Disclosure Index Measuring Disclosures (Eng)Document31 pagesA Transparency Disclosure Index Measuring Disclosures (Eng)AndriNo ratings yet

- Liquidity, Solvency & Flexibility Analysis of 16 Manufacturing Organizations and Local NWC Management SystemDocument37 pagesLiquidity, Solvency & Flexibility Analysis of 16 Manufacturing Organizations and Local NWC Management SystemAli Abdullah Munna 1410788030No ratings yet

- Corporate Attributes and Audit Delay in Emerging Markets: Empirical Evidence From NigeriaDocument10 pagesCorporate Attributes and Audit Delay in Emerging Markets: Empirical Evidence From NigeriaNovi WulandariNo ratings yet

- JagjeetDocument23 pagesJagjeetprabhprabhNo ratings yet

- OECD Anti Bribery Convention Progress Report 2011 WebDocument94 pagesOECD Anti Bribery Convention Progress Report 2011 WebcorruptioncurrentsNo ratings yet

- Module 1 Research ToolsDocument5 pagesModule 1 Research ToolsnicoleNo ratings yet

- Jurnal IADocument6 pagesJurnal IAnovita kusumawatiNo ratings yet

- EY Transparency International Bribe Payers Index 2011 PDFDocument32 pagesEY Transparency International Bribe Payers Index 2011 PDFallesandro30No ratings yet

- E&YDocument11 pagesE&YPriyanka RadhaNo ratings yet

- Forensic Accounting and Auditing Techniques As A Tool For Fraud Prevention and Detection in Public ServiceDocument43 pagesForensic Accounting and Auditing Techniques As A Tool For Fraud Prevention and Detection in Public ServicerotimibukunmienochNo ratings yet

- EY Transparency Report 2012Document27 pagesEY Transparency Report 2012teddytopNo ratings yet

- Toshiba ForensicDocument19 pagesToshiba ForensicsuksesNo ratings yet

- Chapter OneDocument6 pagesChapter OneHenry BitrusNo ratings yet

- Predicting Corporate Bankruptcy Assignment 1Document8 pagesPredicting Corporate Bankruptcy Assignment 1Bharat Bhushan BhaskarNo ratings yet

- 3rd PartiesDocument63 pages3rd PartieskiubiuNo ratings yet

- Investing in India - Tax & Oct 2010Document101 pagesInvesting in India - Tax & Oct 2010Kapil KriplaniNo ratings yet

- Key Determinants of Capital Structure in Iran: 1.1 BackgroundDocument15 pagesKey Determinants of Capital Structure in Iran: 1.1 BackgroundAireeseNo ratings yet

- Corruption Perception Index (CPI) 2010Document4 pagesCorruption Perception Index (CPI) 2010Niam ChomskyNo ratings yet

- 1256-Article Text-2169-1-10-20180126 PDFDocument7 pages1256-Article Text-2169-1-10-20180126 PDFAndiarfanNo ratings yet

- Productivity Growth in Europe: Policy Research Working Paper 6425Document43 pagesProductivity Growth in Europe: Policy Research Working Paper 6425ilinri@gmail.comNo ratings yet

- (Sony) Position Paper FINALDocument18 pages(Sony) Position Paper FINALMelissa LawNo ratings yet

- INFOSYSDocument9 pagesINFOSYSSai VasudevanNo ratings yet

- Financial Performance of Five Sector of Indian EconomyDocument16 pagesFinancial Performance of Five Sector of Indian EconomyPraveen AgarwalNo ratings yet

- Analisis Altman (Z-Score) Untuk Mengukur Potensi Kebangkrutan Perusahaan Rokok Dan FarmasiDocument23 pagesAnalisis Altman (Z-Score) Untuk Mengukur Potensi Kebangkrutan Perusahaan Rokok Dan FarmasiFitri UtariNo ratings yet

- EJEFAS 32 12 Nisam UradilaDocument14 pagesEJEFAS 32 12 Nisam UradilaIlma Mudrov-HusanovićNo ratings yet

- Creative Accounting Practices: Ethical Challenges in Nigerian Corporate EnvironmentDocument15 pagesCreative Accounting Practices: Ethical Challenges in Nigerian Corporate Environmentadewale abiodunNo ratings yet

- (Sony) Presentation Slides 30marchDocument20 pages(Sony) Presentation Slides 30marchMelissa LawNo ratings yet

- Malaysia'S Outward Foreign Affiliates Statistics: Norul Anisa Abu Safran and Hasnul Hadi JamaliDocument14 pagesMalaysia'S Outward Foreign Affiliates Statistics: Norul Anisa Abu Safran and Hasnul Hadi JamaliHusnaanaNo ratings yet

- EY Audit Committee Bulletin Issue 5 October 2013Document16 pagesEY Audit Committee Bulletin Issue 5 October 2013Euglena VerdeNo ratings yet

- Dessalegn Getie MihretDocument13 pagesDessalegn Getie MihretMadner FarzNo ratings yet

- The Factors That Affect Shares' ReturnDocument13 pagesThe Factors That Affect Shares' ReturnCahMbelingNo ratings yet

- Brooks Complete ProjectDocument112 pagesBrooks Complete ProjectFaith MoneyNo ratings yet

- ICAI SeminarDocument74 pagesICAI Seminarks9650No ratings yet

- Corporate Governance in India: Rajesh Chakrabarti William L. Megginson Pradeep K. YadavDocument24 pagesCorporate Governance in India: Rajesh Chakrabarti William L. Megginson Pradeep K. YadavmanupalanNo ratings yet

- Risk Intelligent Proxy Disclosures 2011Document10 pagesRisk Intelligent Proxy Disclosures 2011Kristian Van TuilNo ratings yet

- Impact of Board Independence On Financial Reporting Quality of Pharmaceutical Companies in NigeriaDocument5 pagesImpact of Board Independence On Financial Reporting Quality of Pharmaceutical Companies in NigeriaaijbmNo ratings yet

- Ranking India's Transnational CompaniesDocument9 pagesRanking India's Transnational CompaniesdualballersNo ratings yet

- FRC Key Facts and Trends in The Accountancy Profession August 2022Document74 pagesFRC Key Facts and Trends in The Accountancy Profession August 2022elsofi713No ratings yet

- Chapter One: - Introduction - Statement of The Research Problem - Aim and Objective of The Study - Research QuestionsDocument22 pagesChapter One: - Introduction - Statement of The Research Problem - Aim and Objective of The Study - Research QuestionssandyNo ratings yet

- Analisis Prediksi Potensi Resiko Fraudulent Financial Statement Melalui Fraud Score ModelDocument14 pagesAnalisis Prediksi Potensi Resiko Fraudulent Financial Statement Melalui Fraud Score ModelZhafirah Nabilah SaryNo ratings yet

- Financial Ratios and Stock Prices: Consistency or Discrepancy? Longitudinal Comparison Between Uae and UsaDocument10 pagesFinancial Ratios and Stock Prices: Consistency or Discrepancy? Longitudinal Comparison Between Uae and UsaDhanushka RajapakshaNo ratings yet

- 2020 - Moral Development As The Influencer of Fraud DetectionDocument11 pages2020 - Moral Development As The Influencer of Fraud DetectionDulcianeFortesNo ratings yet

- Pourali (2013)Document6 pagesPourali (2013)Dhira Syenna AnindittaNo ratings yet

- Accounting QuestionsDocument6 pagesAccounting QuestionsMashNo ratings yet

- Equity Research With Financial Modelling: Qualitative AnalysisDocument2 pagesEquity Research With Financial Modelling: Qualitative AnalysisanuNo ratings yet

- Jurnal - Deviana Febrianti (1021710015)Document11 pagesJurnal - Deviana Febrianti (1021710015)Phuttry 'itHu' UthhieNo ratings yet

- Determinants of Firm Performance: A Comparison of European CountriesDocument7 pagesDeterminants of Firm Performance: A Comparison of European CountriesSanti WuNo ratings yet

- Study On Intrinsic Value of PseDocument84 pagesStudy On Intrinsic Value of PseApoorv MudgilNo ratings yet

- 2013 TRAC EmergingMarketMultinationals enDocument55 pages2013 TRAC EmergingMarketMultinationals enmartaqlNo ratings yet

- Damagum and Chima PDFDocument14 pagesDamagum and Chima PDFchimaemmanuelNo ratings yet

- IT3 Topics Students 1Document9 pagesIT3 Topics Students 1Kimberly MaragañasNo ratings yet

- Derivatives Use and Financial Instrument Disclosure in The Extractives IndustryDocument29 pagesDerivatives Use and Financial Instrument Disclosure in The Extractives IndustrySon Go HanNo ratings yet

- Non Financial Reporting StandardDocument9 pagesNon Financial Reporting StandardAgustinus SiregarNo ratings yet

- Audit Committee and Timeliness of Financial ReportsDocument13 pagesAudit Committee and Timeliness of Financial ReportsAlexander Decker100% (1)

- The Board of Directors and Audit Committee Guide to Fiduciary Responsibilities: Ten Crtical Steps to Protecting Yourself and Your OrganizationFrom EverandThe Board of Directors and Audit Committee Guide to Fiduciary Responsibilities: Ten Crtical Steps to Protecting Yourself and Your OrganizationNo ratings yet

- EIB Group Survey on Investment and Investment Finance 2019: EU overviewFrom EverandEIB Group Survey on Investment and Investment Finance 2019: EU overviewNo ratings yet

- Lahore Grammar School: Candidate Name Date SectionDocument7 pagesLahore Grammar School: Candidate Name Date SectionShehroze Ali JanNo ratings yet

- Lahore Grammar School: Candidate Name Date SectionDocument3 pagesLahore Grammar School: Candidate Name Date SectionShehroze Ali Jan50% (2)

- 7110 Principles of Accounts: MARK SCHEME For The May/June 2008 Question PaperDocument8 pages7110 Principles of Accounts: MARK SCHEME For The May/June 2008 Question PaperShehroze Ali JanNo ratings yet

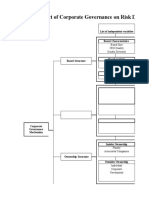

- Impact of Corporate Governance On Risk Disclosure: List of Independent VariablesDocument5 pagesImpact of Corporate Governance On Risk Disclosure: List of Independent VariablesShehroze Ali JanNo ratings yet

- CIR v. Palanca, G.R. No. L-16626, October 29, 1966, 18 SCRA 496Document3 pagesCIR v. Palanca, G.R. No. L-16626, October 29, 1966, 18 SCRA 496SophiaFrancescaEspinosaNo ratings yet

- Corporate Social Responsibility Voluntary GuidelinesDocument7 pagesCorporate Social Responsibility Voluntary GuidelinesVishwesh KoundilyaNo ratings yet

- Billenness SubpoenaDocument39 pagesBillenness SubpoenapbgristNo ratings yet

- 091 Nielson and Company V Lepanto Consolidated MiningDocument2 pages091 Nielson and Company V Lepanto Consolidated MiningjoyceNo ratings yet

- Official List: 4657 Trading SessionDocument12 pagesOfficial List: 4657 Trading SessionEric Selase EdiforNo ratings yet

- Chap12 (Capital Budgeting and Estimating Cash Flows) VanHorne&Brigham, CabreaDocument4 pagesChap12 (Capital Budgeting and Estimating Cash Flows) VanHorne&Brigham, CabreaClaudine DuhapaNo ratings yet

- Strategic Analysis of DOW ChemicalDocument3 pagesStrategic Analysis of DOW ChemicalLindsey A.No ratings yet

- JMC College of LawDocument12 pagesJMC College of LawJhay-r Bayotlang IINo ratings yet

- Term PaperDocument17 pagesTerm PaperSiva Krishna Reddy NallamilliNo ratings yet

- Solution 1Document5 pagesSolution 1frq qqrNo ratings yet

- TOMS Case StudyDocument12 pagesTOMS Case StudyLauren Conrad-Williams0% (1)

- Digest For Fernandez Vs Dela RosaDocument2 pagesDigest For Fernandez Vs Dela RosaJenifer PaglinawanNo ratings yet

- Nokia Growing Cash MountainDocument2 pagesNokia Growing Cash MountainSu_Neil100% (4)

- 1 - 1st September 2007 (010907)Document4 pages1 - 1st September 2007 (010907)Chaanakya_cuimNo ratings yet

- 3001 158280581 00 000 PyDocument3 pages3001 158280581 00 000 PyCvNo ratings yet

- Audit of Cash & BankDocument55 pagesAudit of Cash & BankIscandar Pacasum DisamburunNo ratings yet

- HRD Pragati 25-8-2009Document80 pagesHRD Pragati 25-8-2009Vinod ShelakeNo ratings yet

- The Secret of Indigos Consistent ProfitsDocument1 pageThe Secret of Indigos Consistent Profitshimsh4u321No ratings yet

- Montieth & Company Insider Trading Study Release 1-16-13Document3 pagesMontieth & Company Insider Trading Study Release 1-16-13Erin FuchsNo ratings yet

- Income Tax Chapter 4Document7 pagesIncome Tax Chapter 4Anton LauretaNo ratings yet

- Application For Financing: Legal Name of Business: Date Est.: Trade Name: Physical AddressDocument3 pagesApplication For Financing: Legal Name of Business: Date Est.: Trade Name: Physical AddressadnanstudNo ratings yet

- Pokémon Trading Card GameDocument13 pagesPokémon Trading Card Gamesigne.soderstrom17850% (1)

- Career Research - Docx Raj (1) .Docx 123 FinalDocument7 pagesCareer Research - Docx Raj (1) .Docx 123 FinalGuri RandhawaNo ratings yet

- African Queen: Airline Interview: Ethiopian AirlinesDocument4 pagesAfrican Queen: Airline Interview: Ethiopian AirlinesMLR123No ratings yet

- 2018-10-01 Harper S Bazaar Singapore PDFDocument188 pages2018-10-01 Harper S Bazaar Singapore PDFRoxinaNo ratings yet

- SIDBI PresentationDocument34 pagesSIDBI PresentationNarendra KumarNo ratings yet

- Wins Mathew Current Location: Doha, Qatar Contact Number:+ (974) 50442321Document3 pagesWins Mathew Current Location: Doha, Qatar Contact Number:+ (974) 50442321Wins Mathew VaniyapurackalNo ratings yet