TheCryptoCreditReport q2 2019

TheCryptoCreditReport q2 2019

You might also like

- UK Financial Regulations (Easily Understood) - Revision Guide For CeMap/CeFA 1 SampleDocument14 pagesUK Financial Regulations (Easily Understood) - Revision Guide For CeMap/CeFA 1 Sampleadetomiruksons100% (1)

- Mortgages (Easily Understood) - Revision Guide For CeMap 2Document14 pagesMortgages (Easily Understood) - Revision Guide For CeMap 2adetomiruksons100% (1)

- English Grammar Exercises With Answers For C2 - Part 2Document385 pagesEnglish Grammar Exercises With Answers For C2 - Part 2Rocio Licea100% (22)

- Were ETH and EOS Repeatedly Recycled During The EOS Initial Coin Offering?Document14 pagesWere ETH and EOS Repeatedly Recycled During The EOS Initial Coin Offering?ForkLogNo ratings yet

- Update To Doc 8335 - : Manual of Procedures For Operations Inspection, Certification and Continued SurveillanceDocument10 pagesUpdate To Doc 8335 - : Manual of Procedures For Operations Inspection, Certification and Continued SurveillanceAbdul Aziz Abdul HalimNo ratings yet

- RealEstateTech TracxnFeedReport 07feb2020 - 1581314460268 PDFDocument228 pagesRealEstateTech TracxnFeedReport 07feb2020 - 1581314460268 PDFRohan SanejaNo ratings yet

- The Cosmos HubDocument27 pagesThe Cosmos HubForkLogNo ratings yet

- Treasury Letter On Broker DefinitionDocument3 pagesTreasury Letter On Broker DefinitionForkLogNo ratings yet

- TSLA Q3 2021 Quarterly UpdateDocument27 pagesTSLA Q3 2021 Quarterly UpdateFred LamertNo ratings yet

- R19 Release HighlightsDocument94 pagesR19 Release HighlightsKhang Lương Ngọc100% (2)

- Week 4 Activity Identify The Element of Financial StatementDocument2 pagesWeek 4 Activity Identify The Element of Financial StatementMarlyn Lotivio100% (1)

- Bankers AcceptancesDocument36 pagesBankers AcceptancesAlexhCreditor100% (1)

- R18AMR ReleaseHighlights ClientDocument51 pagesR18AMR ReleaseHighlights Clientrodrigue christian toukamNo ratings yet

- BBC WhitepaperDocument30 pagesBBC WhitepaperKader Milano0% (1)

- R16AMR ReleaseHighlightsDocument27 pagesR16AMR ReleaseHighlightsHaseeb AkramNo ratings yet

- R19AMR ReleaseHighlights ClientDocument85 pagesR19AMR ReleaseHighlights ClientTing ohnNo ratings yet

- Individual Fund Factsheet: March 2019Document51 pagesIndividual Fund Factsheet: March 2019Ram GuggulNo ratings yet

- Explore: Scribd Upload A Document Search DocumentsDocument23 pagesExplore: Scribd Upload A Document Search Documentsajaygarg92No ratings yet

- Annual State of The Residential Mortgage Market in CanadaDocument43 pagesAnnual State of The Residential Mortgage Market in Canadaderailedcapitalism.comNo ratings yet

- Economic Reports 2007 08 NEWDocument164 pagesEconomic Reports 2007 08 NEWarjun kafleNo ratings yet

- Notable Deal TRX For Bank Mar24Document5 pagesNotable Deal TRX For Bank Mar24Hary AntoNo ratings yet

- The Dai Stablecoin System: WhitepaperDocument21 pagesThe Dai Stablecoin System: WhitepaperEnrique Barueco MikelarenaNo ratings yet

- The Dai Stablecoin System: WhitepaperDocument21 pagesThe Dai Stablecoin System: WhitepaperandrssssNo ratings yet

- Kobi Real Estate Fund 1 PPM 1Document182 pagesKobi Real Estate Fund 1 PPM 1veldanezNo ratings yet

- Alvexo-Trader's 2019 Playbook enDocument17 pagesAlvexo-Trader's 2019 Playbook enRui Gomes0% (1)

- Third Quarter 2009 Financial SupplementDocument34 pagesThird Quarter 2009 Financial SupplementasimfarrukhNo ratings yet

- Credit Derivative Report 2006 Exec SummaryDocument6 pagesCredit Derivative Report 2006 Exec SummaryHarsh SonawaneNo ratings yet

- Apollo Global Management, LLC Nov Investor Presentation VFinalDocument40 pagesApollo Global Management, LLC Nov Investor Presentation VFinalneovaysburd5No ratings yet

- EnDocument44 pagesEnmoriNo ratings yet

- FIN 566 Lecture 1Document23 pagesFIN 566 Lecture 1mf-shroomNo ratings yet

- Banking - Citi - Original File1Document16 pagesBanking - Citi - Original File1Xiaochen TangNo ratings yet

- Erp Cloud Global CatalogDocument124 pagesErp Cloud Global Catalogmaha AhmedNo ratings yet

- M2M Finance PresentationDocument10 pagesM2M Finance PresentationjkNo ratings yet

- Newsletter - March 2011Document28 pagesNewsletter - March 2011Kim at MAREINo ratings yet

- The Blue Chips Spring 2019: Investor LetterDocument22 pagesThe Blue Chips Spring 2019: Investor LetterEthan ConroyNo ratings yet

- Capital Asset Investment: Strategy, Tactics and ToolsFrom EverandCapital Asset Investment: Strategy, Tactics and ToolsRating: 1 out of 5 stars1/5 (1)

- Why The Buy Side Should Buy Into The FX Global Code Speech by Andrew HauserDocument9 pagesWhy The Buy Side Should Buy Into The FX Global Code Speech by Andrew HauserHao WangNo ratings yet

- Markit CDS PrimerDocument31 pagesMarkit CDS Primermofeedwildali100% (1)

- Think and RecallDocument6 pagesThink and RecallRuben Sosing Leyba0% (1)

- Sologenic Ecosystem: Backed byDocument49 pagesSologenic Ecosystem: Backed byKsar O-dNo ratings yet

- Employee HandDocument36 pagesEmployee HandRiya BhattNo ratings yet

- Cornerstone - Fintech Adoption in The USDocument29 pagesCornerstone - Fintech Adoption in The USPriti VarmaNo ratings yet

- Cornerstone - Fintech Adoption in The USDocument29 pagesCornerstone - Fintech Adoption in The USPriti VarmaNo ratings yet

- List of Topics May 2023 SyllabusDocument3 pagesList of Topics May 2023 SyllabusnotredameofjolocollegeshsNo ratings yet

- Construction DeveloperDocument46 pagesConstruction DeveloperIhab Ramlawi100% (1)

- Cap Rate Rate ReportDocument207 pagesCap Rate Rate ReportO'Connor Associate0% (1)

- Brikram Real EstateDocument36 pagesBrikram Real EstatemrigendrarimalNo ratings yet

- WAW Products and Services Terms and ConditionsDocument31 pagesWAW Products and Services Terms and Conditionsmaverick_1901No ratings yet

- Where Dreams Come: ANNUAL REPORT 2016-17Document212 pagesWhere Dreams Come: ANNUAL REPORT 2016-17Udayraj PatilNo ratings yet

- Accounting Act 2Document2 pagesAccounting Act 2Vanessa Bianca Glace Viray BanagNo ratings yet

- XX Economics v1.2Document12 pagesXX Economics v1.2Paulo DuarteNo ratings yet

- Bank of America Q1 2009 SlidesDocument40 pagesBank of America Q1 2009 SlidesWall Street FollyNo ratings yet

- Collections 3.0: Bad Debt Collections: From Ugly Duckling To White SwanDocument16 pagesCollections 3.0: Bad Debt Collections: From Ugly Duckling To White SwanGarimaNo ratings yet

- Law - Insider - Carter Validus Mission Critical Reit Inc - DC 2775 Northwoods Parkway LLC Borrower To - Filed - 20 03 2012 - ContractDocument63 pagesLaw - Insider - Carter Validus Mission Critical Reit Inc - DC 2775 Northwoods Parkway LLC Borrower To - Filed - 20 03 2012 - ContractNavrita KaurNo ratings yet

- 5fc9071aa4646025ba202bbb - YIELD - WhitepaperDocument37 pages5fc9071aa4646025ba202bbb - YIELD - WhitepaperamandotarbiraNo ratings yet

- Analysis of The Banking IndustryDocument44 pagesAnalysis of The Banking Industryapi-712465541No ratings yet

- White Paper TPN v2.1Document22 pagesWhite Paper TPN v2.1Anonymous VbmkVpNo ratings yet

- The Hedge Fund Compliance and Risk Management Guide - PDF (PDFDrive)Document467 pagesThe Hedge Fund Compliance and Risk Management Guide - PDF (PDFDrive)Solange KansourouNo ratings yet

- The Tax-Free Exchange Loophole: How Real Estate Investors Can Profit from the 1031 ExchangeFrom EverandThe Tax-Free Exchange Loophole: How Real Estate Investors Can Profit from the 1031 ExchangeNo ratings yet

- Building B2B Applications with XML: A Resource GuideFrom EverandBuilding B2B Applications with XML: A Resource GuideRating: 5 out of 5 stars5/5 (1)

- How to Save Thousands of Dollars on Your Home MortgageFrom EverandHow to Save Thousands of Dollars on Your Home MortgageRating: 3 out of 5 stars3/5 (1)

- Robots, Androids and Animatrons, Second Edition: 12 Incredible Projects You Can BuildFrom EverandRobots, Androids and Animatrons, Second Edition: 12 Incredible Projects You Can BuildRating: 3 out of 5 stars3/5 (3)

- Tips & Traps When Buying A Condo, Co-op, or TownhouseFrom EverandTips & Traps When Buying A Condo, Co-op, or TownhouseRating: 3.5 out of 5 stars3.5/5 (4)

- LawsuitDocument16 pagesLawsuitForkLogNo ratings yet

- VoyagerDocument13 pagesVoyagerForkLogNo ratings yet

- United States District Court Southern District of New York United States of America - v. - James Zhong, Defendant. 22 Cr. 606 (PGG)Document37 pagesUnited States District Court Southern District of New York United States of America - v. - James Zhong, Defendant. 22 Cr. 606 (PGG)ForkLogNo ratings yet

- COM 2022 552 1 EN ACT Part1 v6Document23 pagesCOM 2022 552 1 EN ACT Part1 v6ForkLogNo ratings yet

- Daaml Act of 2022Document7 pagesDaaml Act of 2022ForkLogNo ratings yet

- TexasDocument11 pagesTexasForkLogNo ratings yet

- Economic Well-Being of U.S. Households in 2021: Research & AnalysisDocument98 pagesEconomic Well-Being of U.S. Households in 2021: Research & AnalysisForkLogNo ratings yet

- In Re Celsius Network LLCDocument20 pagesIn Re Celsius Network LLCForkLogNo ratings yet

- Terra LawsuitDocument72 pagesTerra LawsuitForkLogNo ratings yet

- United States District Court Eastern District of Kentucky Lexington DivisionDocument71 pagesUnited States District Court Eastern District of Kentucky Lexington DivisionForkLogNo ratings yet

- United States Strategy On Countering CorruptionDocument38 pagesUnited States Strategy On Countering CorruptionForkLogNo ratings yet

- Tesla, Inc.: United States Securities and Exchange Commission FORM 10-QDocument66 pagesTesla, Inc.: United States Securities and Exchange Commission FORM 10-QForkLogNo ratings yet

- U S D C: Nited Tates Istrict OurtDocument1 pageU S D C: Nited Tates Istrict OurtForkLogNo ratings yet

- Yellen Responses To Toomey QfrsDocument8 pagesYellen Responses To Toomey QfrsForkLogNo ratings yet

- Pub Semiannual Risk Perspective Fall 2021Document32 pagesPub Semiannual Risk Perspective Fall 2021ForkLogNo ratings yet

- 34 93489Document3 pages34 93489ForkLogNo ratings yet

- Updated Guidance VA VASPDocument111 pagesUpdated Guidance VA VASPForkLogNo ratings yet

- Financial Trend Analysis - Ransomware 508 FINALDocument17 pagesFinancial Trend Analysis - Ransomware 508 FINALForkLogNo ratings yet

- G7 Public Policy Principles For Retail CBDC FINALDocument27 pagesG7 Public Policy Principles For Retail CBDC FINALForkLogNo ratings yet

- E-HKD A Technical PerspectiveDocument50 pagesE-HKD A Technical PerspectiveForkLogNo ratings yet

- HB04474IDocument4 pagesHB04474IForkLogNo ratings yet

- Celsius Network LLC 2021AH00024Document12 pagesCelsius Network LLC 2021AH00024ForkLogNo ratings yet

- Subject: Unauthorized Access To Your Coinbase AccountDocument3 pagesSubject: Unauthorized Access To Your Coinbase AccountForkLogNo ratings yet

- See Securities Industry and Financial Markets Association, "2021 SIFMA Capital Markets Fact Book," Available IbidDocument10 pagesSee Securities Industry and Financial Markets Association, "2021 SIFMA Capital Markets Fact Book," Available IbidForkLogNo ratings yet

- Csa 20210923 21 330 Crypto Trading PlatformsDocument11 pagesCsa 20210923 21 330 Crypto Trading PlatformsForkLogNo ratings yet

- Department of The Treasury: WASHINGTON, D.C. 20220Document26 pagesDepartment of The Treasury: WASHINGTON, D.C. 20220ForkLogNo ratings yet

- World Cup QuizDocument2 pagesWorld Cup QuizEC Pisano RiggioNo ratings yet

- George Galloway - The Return of PoliticsDocument2 pagesGeorge Galloway - The Return of PoliticsricardonunoNo ratings yet

- Essay 1Document3 pagesEssay 1api-607929863No ratings yet

- Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument16 pagesDate Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing Balancevedhasai198No ratings yet

- Analysis Essay (SFA)Document1 pageAnalysis Essay (SFA)saihtookhantkyaw22No ratings yet

- The Paralympic Games Is A Major International MultiDocument1 pageThe Paralympic Games Is A Major International MultiKamaRaj SundaramoorthyNo ratings yet

- William Shakespeare's SonnetsDocument5 pagesWilliam Shakespeare's Sonnetsgabryela22No ratings yet

- Paula Martinez V. Victorino Baganus, GR No. 9438 Jayward Z. BacoDocument47 pagesPaula Martinez V. Victorino Baganus, GR No. 9438 Jayward Z. BacoLaindei Lou TorredaNo ratings yet

- Sales Trading Resume TemplateDocument1 pageSales Trading Resume TemplateBlake ZhangNo ratings yet

- Gifted Identification MatrixDocument2 pagesGifted Identification MatrixMike EskilsonNo ratings yet

- Exchange RateDocument27 pagesExchange RateGabriel SimNo ratings yet

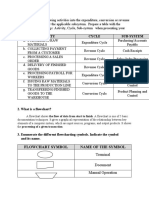

- Activity Cycle Sub-System: Flowchart Symbol Name of The SymbolDocument3 pagesActivity Cycle Sub-System: Flowchart Symbol Name of The SymbolALLIAH CARL MANUELLE PASCASIONo ratings yet

- ApplicationformDocument2 pagesApplicationformSharafat AliNo ratings yet

- Raising A Child - From Age 3-17, School Costs Rs 30LDocument2 pagesRaising A Child - From Age 3-17, School Costs Rs 30LBeru RazaNo ratings yet

- 65 Royale Homes Mktg. Corp. v. Fidel P. Alcantara, G.R. No. 195190, July 28, 2014Document30 pages65 Royale Homes Mktg. Corp. v. Fidel P. Alcantara, G.R. No. 195190, July 28, 2014joyeduardoNo ratings yet

- Thesis Report On BreastfeedingDocument7 pagesThesis Report On Breastfeedingiinlutvff100% (2)

- DOH-HHRDB Healthcare Workers (Physicians)Document41 pagesDOH-HHRDB Healthcare Workers (Physicians)VERA FilesNo ratings yet

- Fundamental Powers of The StateDocument82 pagesFundamental Powers of The StateNiñaNo ratings yet

- Kofax Installation GuideDocument258 pagesKofax Installation GuideCharles ObodoNo ratings yet

- What Is Strategic Positioning?Document8 pagesWhat Is Strategic Positioning?Michael YohannesNo ratings yet

- ADMISSION 2020-21 ADMISSION 2020-21 ADMISSION 2020-21 Deposit Slip Deposit SlipDocument2 pagesADMISSION 2020-21 ADMISSION 2020-21 ADMISSION 2020-21 Deposit Slip Deposit SlipJahanzeb Ahmed SoomroNo ratings yet

- Ra 7431Document12 pagesRa 7431Ricardo EdanoNo ratings yet

- MATH PROJECT TOPIC 2 (Income Tax)Document7 pagesMATH PROJECT TOPIC 2 (Income Tax)avinamakadiaNo ratings yet

- Micro ReviewDocument134 pagesMicro ReviewNiki NourNo ratings yet

- FingerplaysDocument5 pagesFingerplaysAmy Heavner0% (1)

- The Conquistadors Always Start From The South in Square 28 and On The Track The Aztecs Always Start in Square 13Document9 pagesThe Conquistadors Always Start From The South in Square 28 and On The Track The Aztecs Always Start in Square 13Joshua ReyesNo ratings yet

- The Wedding at Ghostmoor Castle: A Play by Beat Brodbeck CharactersDocument20 pagesThe Wedding at Ghostmoor Castle: A Play by Beat Brodbeck Characterscatalina muñozNo ratings yet

- British Yearbook of International Law 1977 Crawford 93 182Document90 pagesBritish Yearbook of International Law 1977 Crawford 93 182irony91No ratings yet

Download as pdf or txt

You might also like

- UK Financial Regulations (Easily Understood) - Revision Guide For CeMap/CeFA 1 SampleDocument14 pagesUK Financial Regulations (Easily Understood) - Revision Guide For CeMap/CeFA 1 Sampleadetomiruksons100% (1)

- Mortgages (Easily Understood) - Revision Guide For CeMap 2Document14 pagesMortgages (Easily Understood) - Revision Guide For CeMap 2adetomiruksons100% (1)

- English Grammar Exercises With Answers For C2 - Part 2Document385 pagesEnglish Grammar Exercises With Answers For C2 - Part 2Rocio Licea100% (22)

- Were ETH and EOS Repeatedly Recycled During The EOS Initial Coin Offering?Document14 pagesWere ETH and EOS Repeatedly Recycled During The EOS Initial Coin Offering?ForkLogNo ratings yet

- Update To Doc 8335 - : Manual of Procedures For Operations Inspection, Certification and Continued SurveillanceDocument10 pagesUpdate To Doc 8335 - : Manual of Procedures For Operations Inspection, Certification and Continued SurveillanceAbdul Aziz Abdul HalimNo ratings yet

- RealEstateTech TracxnFeedReport 07feb2020 - 1581314460268 PDFDocument228 pagesRealEstateTech TracxnFeedReport 07feb2020 - 1581314460268 PDFRohan SanejaNo ratings yet

- The Cosmos HubDocument27 pagesThe Cosmos HubForkLogNo ratings yet

- Treasury Letter On Broker DefinitionDocument3 pagesTreasury Letter On Broker DefinitionForkLogNo ratings yet

- TSLA Q3 2021 Quarterly UpdateDocument27 pagesTSLA Q3 2021 Quarterly UpdateFred LamertNo ratings yet

- R19 Release HighlightsDocument94 pagesR19 Release HighlightsKhang Lương Ngọc100% (2)

- Week 4 Activity Identify The Element of Financial StatementDocument2 pagesWeek 4 Activity Identify The Element of Financial StatementMarlyn Lotivio100% (1)

- Bankers AcceptancesDocument36 pagesBankers AcceptancesAlexhCreditor100% (1)

- R18AMR ReleaseHighlights ClientDocument51 pagesR18AMR ReleaseHighlights Clientrodrigue christian toukamNo ratings yet

- BBC WhitepaperDocument30 pagesBBC WhitepaperKader Milano0% (1)

- R16AMR ReleaseHighlightsDocument27 pagesR16AMR ReleaseHighlightsHaseeb AkramNo ratings yet

- R19AMR ReleaseHighlights ClientDocument85 pagesR19AMR ReleaseHighlights ClientTing ohnNo ratings yet

- Individual Fund Factsheet: March 2019Document51 pagesIndividual Fund Factsheet: March 2019Ram GuggulNo ratings yet

- Explore: Scribd Upload A Document Search DocumentsDocument23 pagesExplore: Scribd Upload A Document Search Documentsajaygarg92No ratings yet

- Annual State of The Residential Mortgage Market in CanadaDocument43 pagesAnnual State of The Residential Mortgage Market in Canadaderailedcapitalism.comNo ratings yet

- Economic Reports 2007 08 NEWDocument164 pagesEconomic Reports 2007 08 NEWarjun kafleNo ratings yet

- Notable Deal TRX For Bank Mar24Document5 pagesNotable Deal TRX For Bank Mar24Hary AntoNo ratings yet

- The Dai Stablecoin System: WhitepaperDocument21 pagesThe Dai Stablecoin System: WhitepaperEnrique Barueco MikelarenaNo ratings yet

- The Dai Stablecoin System: WhitepaperDocument21 pagesThe Dai Stablecoin System: WhitepaperandrssssNo ratings yet

- Kobi Real Estate Fund 1 PPM 1Document182 pagesKobi Real Estate Fund 1 PPM 1veldanezNo ratings yet

- Alvexo-Trader's 2019 Playbook enDocument17 pagesAlvexo-Trader's 2019 Playbook enRui Gomes0% (1)

- Third Quarter 2009 Financial SupplementDocument34 pagesThird Quarter 2009 Financial SupplementasimfarrukhNo ratings yet

- Credit Derivative Report 2006 Exec SummaryDocument6 pagesCredit Derivative Report 2006 Exec SummaryHarsh SonawaneNo ratings yet

- Apollo Global Management, LLC Nov Investor Presentation VFinalDocument40 pagesApollo Global Management, LLC Nov Investor Presentation VFinalneovaysburd5No ratings yet

- EnDocument44 pagesEnmoriNo ratings yet

- FIN 566 Lecture 1Document23 pagesFIN 566 Lecture 1mf-shroomNo ratings yet

- Banking - Citi - Original File1Document16 pagesBanking - Citi - Original File1Xiaochen TangNo ratings yet

- Erp Cloud Global CatalogDocument124 pagesErp Cloud Global Catalogmaha AhmedNo ratings yet

- M2M Finance PresentationDocument10 pagesM2M Finance PresentationjkNo ratings yet

- Newsletter - March 2011Document28 pagesNewsletter - March 2011Kim at MAREINo ratings yet

- The Blue Chips Spring 2019: Investor LetterDocument22 pagesThe Blue Chips Spring 2019: Investor LetterEthan ConroyNo ratings yet

- Capital Asset Investment: Strategy, Tactics and ToolsFrom EverandCapital Asset Investment: Strategy, Tactics and ToolsRating: 1 out of 5 stars1/5 (1)

- Why The Buy Side Should Buy Into The FX Global Code Speech by Andrew HauserDocument9 pagesWhy The Buy Side Should Buy Into The FX Global Code Speech by Andrew HauserHao WangNo ratings yet

- Markit CDS PrimerDocument31 pagesMarkit CDS Primermofeedwildali100% (1)

- Think and RecallDocument6 pagesThink and RecallRuben Sosing Leyba0% (1)

- Sologenic Ecosystem: Backed byDocument49 pagesSologenic Ecosystem: Backed byKsar O-dNo ratings yet

- Employee HandDocument36 pagesEmployee HandRiya BhattNo ratings yet

- Cornerstone - Fintech Adoption in The USDocument29 pagesCornerstone - Fintech Adoption in The USPriti VarmaNo ratings yet

- Cornerstone - Fintech Adoption in The USDocument29 pagesCornerstone - Fintech Adoption in The USPriti VarmaNo ratings yet

- List of Topics May 2023 SyllabusDocument3 pagesList of Topics May 2023 SyllabusnotredameofjolocollegeshsNo ratings yet

- Construction DeveloperDocument46 pagesConstruction DeveloperIhab Ramlawi100% (1)

- Cap Rate Rate ReportDocument207 pagesCap Rate Rate ReportO'Connor Associate0% (1)

- Brikram Real EstateDocument36 pagesBrikram Real EstatemrigendrarimalNo ratings yet

- WAW Products and Services Terms and ConditionsDocument31 pagesWAW Products and Services Terms and Conditionsmaverick_1901No ratings yet

- Where Dreams Come: ANNUAL REPORT 2016-17Document212 pagesWhere Dreams Come: ANNUAL REPORT 2016-17Udayraj PatilNo ratings yet

- Accounting Act 2Document2 pagesAccounting Act 2Vanessa Bianca Glace Viray BanagNo ratings yet

- XX Economics v1.2Document12 pagesXX Economics v1.2Paulo DuarteNo ratings yet

- Bank of America Q1 2009 SlidesDocument40 pagesBank of America Q1 2009 SlidesWall Street FollyNo ratings yet

- Collections 3.0: Bad Debt Collections: From Ugly Duckling To White SwanDocument16 pagesCollections 3.0: Bad Debt Collections: From Ugly Duckling To White SwanGarimaNo ratings yet

- Law - Insider - Carter Validus Mission Critical Reit Inc - DC 2775 Northwoods Parkway LLC Borrower To - Filed - 20 03 2012 - ContractDocument63 pagesLaw - Insider - Carter Validus Mission Critical Reit Inc - DC 2775 Northwoods Parkway LLC Borrower To - Filed - 20 03 2012 - ContractNavrita KaurNo ratings yet

- 5fc9071aa4646025ba202bbb - YIELD - WhitepaperDocument37 pages5fc9071aa4646025ba202bbb - YIELD - WhitepaperamandotarbiraNo ratings yet

- Analysis of The Banking IndustryDocument44 pagesAnalysis of The Banking Industryapi-712465541No ratings yet

- White Paper TPN v2.1Document22 pagesWhite Paper TPN v2.1Anonymous VbmkVpNo ratings yet

- The Hedge Fund Compliance and Risk Management Guide - PDF (PDFDrive)Document467 pagesThe Hedge Fund Compliance and Risk Management Guide - PDF (PDFDrive)Solange KansourouNo ratings yet

- The Tax-Free Exchange Loophole: How Real Estate Investors Can Profit from the 1031 ExchangeFrom EverandThe Tax-Free Exchange Loophole: How Real Estate Investors Can Profit from the 1031 ExchangeNo ratings yet

- Building B2B Applications with XML: A Resource GuideFrom EverandBuilding B2B Applications with XML: A Resource GuideRating: 5 out of 5 stars5/5 (1)

- How to Save Thousands of Dollars on Your Home MortgageFrom EverandHow to Save Thousands of Dollars on Your Home MortgageRating: 3 out of 5 stars3/5 (1)

- Robots, Androids and Animatrons, Second Edition: 12 Incredible Projects You Can BuildFrom EverandRobots, Androids and Animatrons, Second Edition: 12 Incredible Projects You Can BuildRating: 3 out of 5 stars3/5 (3)

- Tips & Traps When Buying A Condo, Co-op, or TownhouseFrom EverandTips & Traps When Buying A Condo, Co-op, or TownhouseRating: 3.5 out of 5 stars3.5/5 (4)

- LawsuitDocument16 pagesLawsuitForkLogNo ratings yet

- VoyagerDocument13 pagesVoyagerForkLogNo ratings yet

- United States District Court Southern District of New York United States of America - v. - James Zhong, Defendant. 22 Cr. 606 (PGG)Document37 pagesUnited States District Court Southern District of New York United States of America - v. - James Zhong, Defendant. 22 Cr. 606 (PGG)ForkLogNo ratings yet

- COM 2022 552 1 EN ACT Part1 v6Document23 pagesCOM 2022 552 1 EN ACT Part1 v6ForkLogNo ratings yet

- Daaml Act of 2022Document7 pagesDaaml Act of 2022ForkLogNo ratings yet

- TexasDocument11 pagesTexasForkLogNo ratings yet

- Economic Well-Being of U.S. Households in 2021: Research & AnalysisDocument98 pagesEconomic Well-Being of U.S. Households in 2021: Research & AnalysisForkLogNo ratings yet

- In Re Celsius Network LLCDocument20 pagesIn Re Celsius Network LLCForkLogNo ratings yet

- Terra LawsuitDocument72 pagesTerra LawsuitForkLogNo ratings yet

- United States District Court Eastern District of Kentucky Lexington DivisionDocument71 pagesUnited States District Court Eastern District of Kentucky Lexington DivisionForkLogNo ratings yet

- United States Strategy On Countering CorruptionDocument38 pagesUnited States Strategy On Countering CorruptionForkLogNo ratings yet

- Tesla, Inc.: United States Securities and Exchange Commission FORM 10-QDocument66 pagesTesla, Inc.: United States Securities and Exchange Commission FORM 10-QForkLogNo ratings yet

- U S D C: Nited Tates Istrict OurtDocument1 pageU S D C: Nited Tates Istrict OurtForkLogNo ratings yet

- Yellen Responses To Toomey QfrsDocument8 pagesYellen Responses To Toomey QfrsForkLogNo ratings yet

- Pub Semiannual Risk Perspective Fall 2021Document32 pagesPub Semiannual Risk Perspective Fall 2021ForkLogNo ratings yet

- 34 93489Document3 pages34 93489ForkLogNo ratings yet

- Updated Guidance VA VASPDocument111 pagesUpdated Guidance VA VASPForkLogNo ratings yet

- Financial Trend Analysis - Ransomware 508 FINALDocument17 pagesFinancial Trend Analysis - Ransomware 508 FINALForkLogNo ratings yet

- G7 Public Policy Principles For Retail CBDC FINALDocument27 pagesG7 Public Policy Principles For Retail CBDC FINALForkLogNo ratings yet

- E-HKD A Technical PerspectiveDocument50 pagesE-HKD A Technical PerspectiveForkLogNo ratings yet

- HB04474IDocument4 pagesHB04474IForkLogNo ratings yet

- Celsius Network LLC 2021AH00024Document12 pagesCelsius Network LLC 2021AH00024ForkLogNo ratings yet

- Subject: Unauthorized Access To Your Coinbase AccountDocument3 pagesSubject: Unauthorized Access To Your Coinbase AccountForkLogNo ratings yet

- See Securities Industry and Financial Markets Association, "2021 SIFMA Capital Markets Fact Book," Available IbidDocument10 pagesSee Securities Industry and Financial Markets Association, "2021 SIFMA Capital Markets Fact Book," Available IbidForkLogNo ratings yet

- Csa 20210923 21 330 Crypto Trading PlatformsDocument11 pagesCsa 20210923 21 330 Crypto Trading PlatformsForkLogNo ratings yet

- Department of The Treasury: WASHINGTON, D.C. 20220Document26 pagesDepartment of The Treasury: WASHINGTON, D.C. 20220ForkLogNo ratings yet

- World Cup QuizDocument2 pagesWorld Cup QuizEC Pisano RiggioNo ratings yet

- George Galloway - The Return of PoliticsDocument2 pagesGeorge Galloway - The Return of PoliticsricardonunoNo ratings yet

- Essay 1Document3 pagesEssay 1api-607929863No ratings yet

- Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument16 pagesDate Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing Balancevedhasai198No ratings yet

- Analysis Essay (SFA)Document1 pageAnalysis Essay (SFA)saihtookhantkyaw22No ratings yet

- The Paralympic Games Is A Major International MultiDocument1 pageThe Paralympic Games Is A Major International MultiKamaRaj SundaramoorthyNo ratings yet

- William Shakespeare's SonnetsDocument5 pagesWilliam Shakespeare's Sonnetsgabryela22No ratings yet

- Paula Martinez V. Victorino Baganus, GR No. 9438 Jayward Z. BacoDocument47 pagesPaula Martinez V. Victorino Baganus, GR No. 9438 Jayward Z. BacoLaindei Lou TorredaNo ratings yet

- Sales Trading Resume TemplateDocument1 pageSales Trading Resume TemplateBlake ZhangNo ratings yet

- Gifted Identification MatrixDocument2 pagesGifted Identification MatrixMike EskilsonNo ratings yet

- Exchange RateDocument27 pagesExchange RateGabriel SimNo ratings yet

- Activity Cycle Sub-System: Flowchart Symbol Name of The SymbolDocument3 pagesActivity Cycle Sub-System: Flowchart Symbol Name of The SymbolALLIAH CARL MANUELLE PASCASIONo ratings yet

- ApplicationformDocument2 pagesApplicationformSharafat AliNo ratings yet

- Raising A Child - From Age 3-17, School Costs Rs 30LDocument2 pagesRaising A Child - From Age 3-17, School Costs Rs 30LBeru RazaNo ratings yet

- 65 Royale Homes Mktg. Corp. v. Fidel P. Alcantara, G.R. No. 195190, July 28, 2014Document30 pages65 Royale Homes Mktg. Corp. v. Fidel P. Alcantara, G.R. No. 195190, July 28, 2014joyeduardoNo ratings yet

- Thesis Report On BreastfeedingDocument7 pagesThesis Report On Breastfeedingiinlutvff100% (2)

- DOH-HHRDB Healthcare Workers (Physicians)Document41 pagesDOH-HHRDB Healthcare Workers (Physicians)VERA FilesNo ratings yet

- Fundamental Powers of The StateDocument82 pagesFundamental Powers of The StateNiñaNo ratings yet

- Kofax Installation GuideDocument258 pagesKofax Installation GuideCharles ObodoNo ratings yet

- What Is Strategic Positioning?Document8 pagesWhat Is Strategic Positioning?Michael YohannesNo ratings yet

- ADMISSION 2020-21 ADMISSION 2020-21 ADMISSION 2020-21 Deposit Slip Deposit SlipDocument2 pagesADMISSION 2020-21 ADMISSION 2020-21 ADMISSION 2020-21 Deposit Slip Deposit SlipJahanzeb Ahmed SoomroNo ratings yet

- Ra 7431Document12 pagesRa 7431Ricardo EdanoNo ratings yet

- MATH PROJECT TOPIC 2 (Income Tax)Document7 pagesMATH PROJECT TOPIC 2 (Income Tax)avinamakadiaNo ratings yet

- Micro ReviewDocument134 pagesMicro ReviewNiki NourNo ratings yet

- FingerplaysDocument5 pagesFingerplaysAmy Heavner0% (1)

- The Conquistadors Always Start From The South in Square 28 and On The Track The Aztecs Always Start in Square 13Document9 pagesThe Conquistadors Always Start From The South in Square 28 and On The Track The Aztecs Always Start in Square 13Joshua ReyesNo ratings yet

- The Wedding at Ghostmoor Castle: A Play by Beat Brodbeck CharactersDocument20 pagesThe Wedding at Ghostmoor Castle: A Play by Beat Brodbeck Characterscatalina muñozNo ratings yet

- British Yearbook of International Law 1977 Crawford 93 182Document90 pagesBritish Yearbook of International Law 1977 Crawford 93 182irony91No ratings yet