Download as pdf or txt

You might also like

- Our Rich Journey - Ultimate Financial Independence Budget PDFDocument3 pagesOur Rich Journey - Ultimate Financial Independence Budget PDFNabilAbbasi100% (1)

- Handling PresentmentsDocument16 pagesHandling PresentmentsAnthony Juice Gaston Bey100% (21)

- Study of NPA in IndiaDocument43 pagesStudy of NPA in IndiaKartik UdayarNo ratings yet

- Eversource Underground Specs WmaDocument58 pagesEversource Underground Specs WmaPj EstokNo ratings yet

- Trump Tax Case NY StateDocument23 pagesTrump Tax Case NY StateMichelle Lee100% (3)

- RECAPITALISATIONDocument9 pagesRECAPITALISATIONEmmanuel MensahNo ratings yet

- Asset Valuation An Its Effect On Financial Statement of Nigeria Deposit Money BankDocument30 pagesAsset Valuation An Its Effect On Financial Statement of Nigeria Deposit Money BankAFOLABI AZEEZ OLUWASEGUN100% (1)

- Economics - Ijecr - Efects of Capital Adequacy On TheDocument10 pagesEconomics - Ijecr - Efects of Capital Adequacy On TheTJPRC PublicationsNo ratings yet

- Determinnt of Banking Profitability - 2Document5 pagesDeterminnt of Banking Profitability - 2thaonguyenpeoctieuNo ratings yet

- Effects of Bank Specific Attributes On Capital Adequency of Listed Commercial Bank in Nigeria Chapter OneDocument34 pagesEffects of Bank Specific Attributes On Capital Adequency of Listed Commercial Bank in Nigeria Chapter OneUmar FarouqNo ratings yet

- Banking Sector Reforms in Bangladesh: Measures and Economic OutcomesDocument25 pagesBanking Sector Reforms in Bangladesh: Measures and Economic OutcomesFakhrul Islam RubelNo ratings yet

- Effect of Cash Management On The Financial Performance of Cooperative Banks in Rwanda: A Case of Zigma CSSDocument11 pagesEffect of Cash Management On The Financial Performance of Cooperative Banks in Rwanda: A Case of Zigma CSSjournalNo ratings yet

- The Determinants of Bank Capital RatiosDocument19 pagesThe Determinants of Bank Capital RatiosAbdou MariamaNo ratings yet

- Final ThesisDocument61 pagesFinal ThesisKeshav KafleNo ratings yet

- Measurement of Bank Profitability, Risk and Efficiency: The Case of The Commercial Bank of Eritrea and Housing and Commerce Bank of EritreaDocument9 pagesMeasurement of Bank Profitability, Risk and Efficiency: The Case of The Commercial Bank of Eritrea and Housing and Commerce Bank of EritreaYemi AdetayoNo ratings yet

- Analisa Performa BankDocument16 pagesAnalisa Performa BankLevramNo ratings yet

- Asset Quality As A Determinant of Commercial Banks Financial Performance in KenyaDocument12 pagesAsset Quality As A Determinant of Commercial Banks Financial Performance in KenyaAsegid GetachewNo ratings yet

- Liquidity Management and Commercial Banks' Profitability in NigeriaDocument16 pagesLiquidity Management and Commercial Banks' Profitability in NigeriaPrince KumarNo ratings yet

- Bank Capital, Deposits and Size Effects Onprofitability of Commercial Banks in NepalDocument74 pagesBank Capital, Deposits and Size Effects Onprofitability of Commercial Banks in NepalRajendra LamsalNo ratings yet

- Recapitalization and Banks Performance ADocument17 pagesRecapitalization and Banks Performance AGREEN FIELD AGRO HI- TECH SERVICES SANGAMNER.No ratings yet

- Reseae MisDocument5 pagesReseae MisSarah RuenNo ratings yet

- Credit Risk ManagementDocument41 pagesCredit Risk Managementkijiba50% (2)

- The Performances of Commercial Banks in Post-ConsolidationDocument12 pagesThe Performances of Commercial Banks in Post-ConsolidationharmedluvNo ratings yet

- A Comparison of Financial Performance in The Banking Sector: Some Evidence From Pakistani Commercial BanksDocument14 pagesA Comparison of Financial Performance in The Banking Sector: Some Evidence From Pakistani Commercial Banks007mbsNo ratings yet

- An Investigation Into The Determinants of Cost Efficiency in The Zambian Banking SectorDocument45 pagesAn Investigation Into The Determinants of Cost Efficiency in The Zambian Banking SectorKemi OlojedeNo ratings yet

- Determinants of Commercial Banks Efficiency: Evidence From Selected Commercial Banks of EthiopiaDocument6 pagesDeterminants of Commercial Banks Efficiency: Evidence From Selected Commercial Banks of EthiopiaJASH MATHEWNo ratings yet

- Banking RegulationDocument16 pagesBanking RegulationPst W C PetersNo ratings yet

- Research ProposalDocument2 pagesResearch ProposalFasika JrNo ratings yet

- Effect 0f Corporate Governance On Financial Performance of Deposit Money Banks inDocument17 pagesEffect 0f Corporate Governance On Financial Performance of Deposit Money Banks inTaylon SimõesNo ratings yet

- Impact of Diversification, Competition and Regulation On Banks Risk Taking: Evidence From Asian Emerging EconomiesDocument61 pagesImpact of Diversification, Competition and Regulation On Banks Risk Taking: Evidence From Asian Emerging EconomiesAfsheenNo ratings yet

- Cost Efficiency of Ghana'S Banking Industry: A Panel Data AnalysisDocument19 pagesCost Efficiency of Ghana'S Banking Industry: A Panel Data AnalysisA TUNo ratings yet

- MPRA Paper 112482Document24 pagesMPRA Paper 112482Hafiz Muhammad SaleemNo ratings yet

- 1 PBDocument8 pages1 PBGizachewNo ratings yet

- A Comparison of Financial Performance in The Banking SectorDocument12 pagesA Comparison of Financial Performance in The Banking SectorandoraphNo ratings yet

- Factors Affecting Profitability of CommeDocument11 pagesFactors Affecting Profitability of Commesheleme garomsaNo ratings yet

- Chapter One: 1.1. Back Ground of The StudyDocument46 pagesChapter One: 1.1. Back Ground of The StudyBobasa S AhmedNo ratings yet

- Mahmud Rani FriendDocument25 pagesMahmud Rani FriendMOHAMMED ABDULMALIKNo ratings yet

- Working Capital Management and Cash Holdings of Banks in GhanaDocument12 pagesWorking Capital Management and Cash Holdings of Banks in GhanaManpreet Kaur VirkNo ratings yet

- Project Work On Banking & InsuranceDocument13 pagesProject Work On Banking & InsuranceKR MinistryNo ratings yet

- The Impact of Banking Consolidation On The Economic Development of NigeriaDocument8 pagesThe Impact of Banking Consolidation On The Economic Development of NigeriaShahbaz MerajNo ratings yet

- Ahmad 2008 Determinant CARDocument20 pagesAhmad 2008 Determinant CARGufranNo ratings yet

- Relationship Between Credit Risk Management and Financial Performance: Empirical Evidence From Microfinance Banks in KenyaDocument28 pagesRelationship Between Credit Risk Management and Financial Performance: Empirical Evidence From Microfinance Banks in KenyaCatherine AteNo ratings yet

- Performance Evaluation of Banking Sector in Pakistan: An Application of BankometerDocument6 pagesPerformance Evaluation of Banking Sector in Pakistan: An Application of BankometertafakharhasnainNo ratings yet

- Paper For VEAM 2019Document33 pagesPaper For VEAM 2019DungNguyenTienNo ratings yet

- Mahlet Fikiru ThesisDocument66 pagesMahlet Fikiru ThesisYohannes KassaNo ratings yet

- Assessing The Performance of Islamic Banks: Some Evidence From The Middle EastDocument10 pagesAssessing The Performance of Islamic Banks: Some Evidence From The Middle EasthaindhaindNo ratings yet

- Impact of Liquidity On Profitability of NMBDocument28 pagesImpact of Liquidity On Profitability of NMBkanchan BogatiNo ratings yet

- AFBRupd PDFDocument9 pagesAFBRupd PDFhasan mdNo ratings yet

- Anand Final ReportDocument89 pagesAnand Final ReportAnand Mishra100% (1)

- Chapter One 1.1 Background of The StudyDocument6 pagesChapter One 1.1 Background of The StudyChidi EmmanuelNo ratings yet

- Ijaeb+ (1 4) +2770-2785Document16 pagesIjaeb+ (1 4) +2770-2785WahyuNo ratings yet

- Factors Affecting Profitabilityof Commercial Banksin EthiopiaDocument12 pagesFactors Affecting Profitabilityof Commercial Banksin EthiopiaDev JesusNo ratings yet

- Article On SecuritizationDocument15 pagesArticle On SecuritizationKashif GulzarNo ratings yet

- The Effects of Deposits Mobilization On Financial Performance in Commercial Banks in Rwanda. A Case of Equity Bank Rwanda Limited PDFDocument28 pagesThe Effects of Deposits Mobilization On Financial Performance in Commercial Banks in Rwanda. A Case of Equity Bank Rwanda Limited PDFJohn FrancisNo ratings yet

- Asset Quality and Bank Performance: A Study of Commercial Banks in NigeriaDocument6 pagesAsset Quality and Bank Performance: A Study of Commercial Banks in NigeriabajujuNo ratings yet

- Capital AdeqancyDocument15 pagesCapital Adeqancyanon_614457836No ratings yet

- CapDocument2 pagesCapDrKhalid A ChishtyNo ratings yet

- Dissertation On Impact of Capital Structure On ProfitabilityDocument5 pagesDissertation On Impact of Capital Structure On ProfitabilityWriteMyPaperForMeUKNo ratings yet

- Chapter One 1.0 1.1 Background of The StudyDocument17 pagesChapter One 1.0 1.1 Background of The StudyEkoh EnduranceNo ratings yet

- Financial Performance Evaluation of Some Selected Jordanian Commercial BanksDocument14 pagesFinancial Performance Evaluation of Some Selected Jordanian Commercial BanksAtiaTahiraNo ratings yet

- Literature ReviewDocument8 pagesLiterature ReviewHesbon MiyogoNo ratings yet

- Influence of Financial Depth On Financial Performance of Commercial Banks in RwandaDocument12 pagesInfluence of Financial Depth On Financial Performance of Commercial Banks in RwandaJohn PaulNo ratings yet

- EIB Working Papers 2019/10 - Structural and cyclical determinants of access to finance: Evidence from EgyptFrom EverandEIB Working Papers 2019/10 - Structural and cyclical determinants of access to finance: Evidence from EgyptNo ratings yet

- T R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)From EverandT R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)No ratings yet

- C S M I: E S A, I USA: Ointegration and Tock Arket Nterdependence Vidence From Outh Frica Ndia and TheDocument11 pagesC S M I: E S A, I USA: Ointegration and Tock Arket Nterdependence Vidence From Outh Frica Ndia and Theanon_614457836No ratings yet

- Capital Adequacy Ratio As Performance Indicator of Banking Sector in India-An Analytical Study of Selected BanksDocument7 pagesCapital Adequacy Ratio As Performance Indicator of Banking Sector in India-An Analytical Study of Selected Banksanon_614457836No ratings yet

- South Asia WP 031Document83 pagesSouth Asia WP 031anon_614457836No ratings yet

- Consumer Behaviour: Segmentation, Targeting and Positioning of Dairy MilkDocument11 pagesConsumer Behaviour: Segmentation, Targeting and Positioning of Dairy Milkanon_614457836No ratings yet

- Capital AdeqancyDocument15 pagesCapital Adeqancyanon_614457836No ratings yet

- HP InternDocument31 pagesHP Internanon_61445783650% (2)

- Management Lessons From MahabarataDocument7 pagesManagement Lessons From Mahabarataanon_614457836No ratings yet

- Fa2 Mock Test 2Document7 pagesFa2 Mock Test 2Sayed Zain Shah100% (1)

- Formalities in Land LawDocument4 pagesFormalities in Land LawCalum Parfitt100% (1)

- November 11Document2 pagesNovember 11brendamanganaanNo ratings yet

- De Soto PaperDocument8 pagesDe Soto PaperireqNo ratings yet

- Midterm: Insurance Law Compilation: Based On The Book of Aquino (3rd Ed., 2018) and de Leon (12th Ed., 2019)Document1 pageMidterm: Insurance Law Compilation: Based On The Book of Aquino (3rd Ed., 2018) and de Leon (12th Ed., 2019)Joesil Dianne SempronNo ratings yet

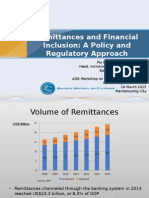

- Remittances and Financial Inclusion: A Policy and Regulatory ApproachDocument19 pagesRemittances and Financial Inclusion: A Policy and Regulatory ApproachAsian Development Bank ConferencesNo ratings yet

- Manuel T de Guia CasesDocument3 pagesManuel T de Guia CasesDelsie Falculan100% (1)

- FFS and CFSDocument28 pagesFFS and CFSAnuj DhamaNo ratings yet

- Nigerian AMCON UpdateDocument7 pagesNigerian AMCON UpdateOluwatosin AdesinaNo ratings yet

- BrandonstruebingresumeDocument1 pageBrandonstruebingresumeapi-355199093No ratings yet

- Factors To Consider When Choosing A School: A Guide Before Using The GI BillDocument9 pagesFactors To Consider When Choosing A School: A Guide Before Using The GI BillChristian MousseauNo ratings yet

- Evangelista vs. Alto Surety & Insurance Co., Inc. G.R. No. L-11139 April 23, 1958Document23 pagesEvangelista vs. Alto Surety & Insurance Co., Inc. G.R. No. L-11139 April 23, 1958Sally OgotNo ratings yet

- Why Look at Debt Settlement Over Bankruptcy - Debt Settlement BookletDocument62 pagesWhy Look at Debt Settlement Over Bankruptcy - Debt Settlement BookletDave FalveyNo ratings yet

- Study of NPA by Ajinkya (3) FinalDocument70 pagesStudy of NPA by Ajinkya (3) FinalAnjali ShuklaNo ratings yet

- Attachment RBI Notification P2P LendingDocument2 pagesAttachment RBI Notification P2P LendingHsjjxnwkNo ratings yet

- FABM 2 Third Quarter Test ReviewerDocument5 pagesFABM 2 Third Quarter Test ReviewergracehelenNo ratings yet

- Dezrezlegal Additional Fees Sheet Sept 2022Document3 pagesDezrezlegal Additional Fees Sheet Sept 2022will2222No ratings yet

- Philip Green CVDocument8 pagesPhilip Green CVPhilip GreenNo ratings yet

- BPI v. SanchezDocument3 pagesBPI v. SanchezMatanglawin RunnersNo ratings yet

- PWC Guide Financing Transactions Debt Equity Second Edition 2015Document333 pagesPWC Guide Financing Transactions Debt Equity Second Edition 2015aniket100% (2)

- Financial Markets and Institutions ch01Document36 pagesFinancial Markets and Institutions ch01Mashrur Rahman ArnabNo ratings yet

- Parties To Negotiable InstrumentDocument25 pagesParties To Negotiable InstrumentTeja RaviNo ratings yet

- 110 PDFDocument288 pages110 PDFSuresh BattaNo ratings yet

- Cup 5 (RFBT)Document2 pagesCup 5 (RFBT)Hannah AbeloNo ratings yet

- HOA Post Registration RequirementsDocument3 pagesHOA Post Registration RequirementsYerffej OrenetroNo ratings yet

- Mortgage and Amortization: Lesson 11Document14 pagesMortgage and Amortization: Lesson 11귀여워gwiyowoNo ratings yet