Childhood Insurance: Target Group Insured Person

Childhood Insurance: Target Group Insured Person

You might also like

- Marksheet PDFDocument2 pagesMarksheet PDFraman0% (2)

- Corporate Finance - PresentationDocument14 pagesCorporate Finance - Presentationguruprasadkudva83% (6)

- INSURANCEDocument28 pagesINSURANCEcharuNo ratings yet

- SAP Overview PresentationDocument19 pagesSAP Overview PresentationRajesh KumarNo ratings yet

- Term Life Insurance PolicyDocument4 pagesTerm Life Insurance PolicyShubham NamdevNo ratings yet

- Critical Years in The Programming of Life Insurance MeansDocument8 pagesCritical Years in The Programming of Life Insurance MeansRomz Ninz HernandezNo ratings yet

- Knowledge Center GlossaryDocument3 pagesKnowledge Center Glossarychezzter25No ratings yet

- Savings Assurance PlanDocument1 pageSavings Assurance Planrajeshdubey7No ratings yet

- Guarantee and OptionsDocument1 pageGuarantee and OptionsRashi JainNo ratings yet

- Types of Life Insurance PoliciesDocument21 pagesTypes of Life Insurance PoliciesDivya PillaiNo ratings yet

- Term Life Insurance FinalDocument10 pagesTerm Life Insurance FinalsearchingnobodyNo ratings yet

- Need For Life InsuranceDocument9 pagesNeed For Life InsuranceDeepak NayakNo ratings yet

- Product Summary:: Jeevan ChhayaDocument4 pagesProduct Summary:: Jeevan ChhayaSumit PandeyNo ratings yet

- Aviva Life InsuranceDocument3 pagesAviva Life InsuranceumashankarsinghNo ratings yet

- Life InsuranceDocument3 pagesLife Insuranceshailen2uNo ratings yet

- Children Insurance Plan: Presented byDocument23 pagesChildren Insurance Plan: Presented byRohit MalviyaNo ratings yet

- Tips While Buying A Child Education PlanDocument7 pagesTips While Buying A Child Education PlanJyotsana SachdevaNo ratings yet

- IDBI Federal Lifesurance Savings Insurance PlanDocument16 pagesIDBI Federal Lifesurance Savings Insurance PlanKumarniksNo ratings yet

- Life Insurance Products & Terms PDFDocument16 pagesLife Insurance Products & Terms PDFSuman SinhaNo ratings yet

- Irda - Hand Book On Life InsuranceDocument12 pagesIrda - Hand Book On Life InsuranceRajesh SinghNo ratings yet

- Life Insurance FAQsDocument3 pagesLife Insurance FAQsEdappon100% (2)

- eEASY Save FAQs PDFDocument6 pageseEASY Save FAQs PDFterrygohNo ratings yet

- What Is Life Insurance?Document11 pagesWhat Is Life Insurance?Ratul BanerjeeNo ratings yet

- Life Insurance:: Principles & Practices of Insurance Unit 3Document6 pagesLife Insurance:: Principles & Practices of Insurance Unit 3ashishsinghashishNo ratings yet

- Life Insurance HandbookDocument12 pagesLife Insurance HandbookChi MnuNo ratings yet

- Life Health and Disability 1Document47 pagesLife Health and Disability 1Muhammad ArshadNo ratings yet

- Module 3 - Insurance Transaction DocumentsDocument6 pagesModule 3 - Insurance Transaction DocumentsAshwinNo ratings yet

- AR Educare Advantage Insurance Plan 5 May 2014Document6 pagesAR Educare Advantage Insurance Plan 5 May 2014ÌmřańNo ratings yet

- I Don't Want To Postpone My Loved Ones' Aspirations: Bharti AXA Life Secure Income PlanDocument15 pagesI Don't Want To Postpone My Loved Ones' Aspirations: Bharti AXA Life Secure Income PlanSandhya AgrawalNo ratings yet

- Task 4Document6 pagesTask 4sahilNo ratings yet

- Investment Plan IncludesDocument4 pagesInvestment Plan IncludesNusrat IslamNo ratings yet

- Insurance & Risk ManagementDocument8 pagesInsurance & Risk ManagementJASONM22No ratings yet

- Forbes Life InvaderDocument19 pagesForbes Life Invaderapi-270707231No ratings yet

- 1Document6 pages1Lalosa Fritz Angela R.No ratings yet

- Life InsuranceDocument26 pagesLife Insurancevivek kant100% (1)

- PRUlink Protection Plus Account EBrochure EnglishDocument8 pagesPRUlink Protection Plus Account EBrochure EnglishjasonNo ratings yet

- Secure Income PlanDocument15 pagesSecure Income PlanSuyash PrasadNo ratings yet

- Product & ServiceDocument11 pagesProduct & ServicefarrukhNo ratings yet

- SBI LIFE INSURANCE - Smart Scholar Brochure V1Document16 pagesSBI LIFE INSURANCE - Smart Scholar Brochure V1Babujee K.NNo ratings yet

- Life Insurance ProductsDocument43 pagesLife Insurance ProductsinvaapNo ratings yet

- Life InsuranceDocument28 pagesLife Insurancejubaida khanamNo ratings yet

- Life Insurance Is A Contract Between The Policy Owner andDocument23 pagesLife Insurance Is A Contract Between The Policy Owner andshankarinadar100% (1)

- Unit - 3 Bilp Types of Life Insurance - Features - ConditionsDocument9 pagesUnit - 3 Bilp Types of Life Insurance - Features - ConditionsYashika GuptaNo ratings yet

- Reliance Life Care For You Plan: We Protect, We CareDocument25 pagesReliance Life Care For You Plan: We Protect, We CareBabujee K.NNo ratings yet

- Whole Life InsuranceDocument16 pagesWhole Life Insuranceemilda_samuel211No ratings yet

- Insuranace Notes - Bonus, Surrender, LoanDocument8 pagesInsuranace Notes - Bonus, Surrender, LoanManidevNo ratings yet

- Jagendra Kumar RenewedDocument7 pagesJagendra Kumar RenewedbcibaneNo ratings yet

- Life InsuranceDocument22 pagesLife Insuranceckchetankhatri967No ratings yet

- 1 Types of Life Insurance Plans & ULIPSDocument40 pages1 Types of Life Insurance Plans & ULIPSJaswanth Singh RajpurohitNo ratings yet

- FinanceDocument25 pagesFinanceShaun D'souzaNo ratings yet

- Insurance ....Document8 pagesInsurance ....SanyaNo ratings yet

- Super Cash GainDocument2 pagesSuper Cash GainElangovan PurushothamanNo ratings yet

- 8 (22) (Read-Only)Document54 pages8 (22) (Read-Only)Kookie ShresthaNo ratings yet

- Postal Life InsuranceDocument12 pagesPostal Life Insurancesupersaiyan_gohanNo ratings yet

- Assurance PlanDocument1 pageAssurance Planswetaagarwal2706No ratings yet

- Chapter - 1 Life & Health InsuranceDocument38 pagesChapter - 1 Life & Health InsurancehelloNo ratings yet

- Life Insurance ProductsDocument6 pagesLife Insurance ProductsBharani GogulaNo ratings yet

- Insurance Terms Glossary - Insurance Meaning of Terms - Deffinition of Insurance TerminologyDocument7 pagesInsurance Terms Glossary - Insurance Meaning of Terms - Deffinition of Insurance TerminologyGreg Alkovitz100% (1)

- Kotak Complete Cover Group PlanDocument7 pagesKotak Complete Cover Group PlanGens GeorgeNo ratings yet

- Textbook of Urgent Care Management: Chapter 9, Insurance Requirements for the Urgent Care CenterFrom EverandTextbook of Urgent Care Management: Chapter 9, Insurance Requirements for the Urgent Care CenterNo ratings yet

- The Basics of Life Insurance: The Answer to What Life Insurance is and How It Works: Personal Finance, #1From EverandThe Basics of Life Insurance: The Answer to What Life Insurance is and How It Works: Personal Finance, #1No ratings yet

- Comparative Analysis Under GST RegimeDocument5 pagesComparative Analysis Under GST RegimeAmita SinwarNo ratings yet

- 6QQMN972 Lecture 8Document24 pages6QQMN972 Lecture 8yash.jiwaNo ratings yet

- Ta 12 Bab2Document9 pagesTa 12 Bab2BelaynehYitayewNo ratings yet

- John Sobredo - Summative AssessmentDocument2 pagesJohn Sobredo - Summative Assessmentsandra mae dulayNo ratings yet

- RAI Business Survey - Round 6 - OverallDocument7 pagesRAI Business Survey - Round 6 - OverallSriniNo ratings yet

- GEC State of The World FinalDocument17 pagesGEC State of The World Finalvivek0724bryantNo ratings yet

- ResumeDocument4 pagesResumeNasir AhmedNo ratings yet

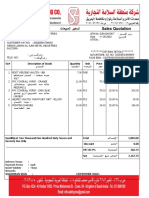

- Sales Quotation: Salesman Sign: Customer SignDocument1 pageSales Quotation: Salesman Sign: Customer SignjacobNo ratings yet

- Documents 4598779043Document5 pagesDocuments 4598779043edgar aboNo ratings yet

- CH 13Document80 pagesCH 13ddNo ratings yet

- Arf 1 Form-TnpgtaDocument12 pagesArf 1 Form-TnpgtaGnanam SekaranNo ratings yet

- Global Business Strategy: E Xplanatory Session 7: Strategy Formulation: Situation Analysis and Business StrategyDocument45 pagesGlobal Business Strategy: E Xplanatory Session 7: Strategy Formulation: Situation Analysis and Business StrategyAstridNo ratings yet

- KK NESAR Projects PVT LTD KK NESAR Projects PVT LTD KK NESAR Projects PVT LTD KK NESAR Projects PVT LTDDocument6 pagesKK NESAR Projects PVT LTD KK NESAR Projects PVT LTD KK NESAR Projects PVT LTD KK NESAR Projects PVT LTDsnairmNo ratings yet

- Batch Processing Using Sequential FilesDocument2 pagesBatch Processing Using Sequential FilesDaniel TadejaNo ratings yet

- Financial Markets - Week 4Document23 pagesFinancial Markets - Week 4gonzgd90No ratings yet

- Tapio Lappi-Seppälä - "Trust, Welfare and Political Economy"Document33 pagesTapio Lappi-Seppälä - "Trust, Welfare and Political Economy"Anonymous Yrp5vpfXNo ratings yet

- Quiz 1 Stratcost F Edited 1Document4 pagesQuiz 1 Stratcost F Edited 1Aeron Arroyo IINo ratings yet

- Solution Manual For Modern Advanced Accounting in Canada 9th Edition Darrell Herauf Murray HiltonDocument35 pagesSolution Manual For Modern Advanced Accounting in Canada 9th Edition Darrell Herauf Murray Hiltoncravingcoarctdbw6wNo ratings yet

- Markscheme November 2018 Global Politics Higher Level and Standard Level Paper 2Document13 pagesMarkscheme November 2018 Global Politics Higher Level and Standard Level Paper 2kakeguruiNo ratings yet

- Real Property Tax Audit With Management Comment and ExhibitsDocument29 pagesReal Property Tax Audit With Management Comment and ExhibitsDaily FreemanNo ratings yet

- Factors Affecting Development of Internet Banking in NepalDocument9 pagesFactors Affecting Development of Internet Banking in NepalMadridista KroosNo ratings yet

- FYBCOM Business Economics Sem IDocument116 pagesFYBCOM Business Economics Sem IDarshan Tajne100% (1)

- Strategic Supply Chain Management-The Case of Toyota UAEDocument23 pagesStrategic Supply Chain Management-The Case of Toyota UAEurbanus matiluNo ratings yet

- Theme 1 Sem 2 Educating Girls Is A Real LifesaverDocument5 pagesTheme 1 Sem 2 Educating Girls Is A Real LifesaverDobre_georgiana910% (1)

- Crams - 1Document28 pagesCrams - 1Janam AroraNo ratings yet

- Corporate Presentation (Company Update)Document39 pagesCorporate Presentation (Company Update)Shyam SunderNo ratings yet

- MBA (Integrated) - 5th - Year - 2022 - 23 - RDocument44 pagesMBA (Integrated) - 5th - Year - 2022 - 23 - Rchutiya collegeNo ratings yet

Download as docx, pdf, or txt

You might also like

- Marksheet PDFDocument2 pagesMarksheet PDFraman0% (2)

- Corporate Finance - PresentationDocument14 pagesCorporate Finance - Presentationguruprasadkudva83% (6)

- INSURANCEDocument28 pagesINSURANCEcharuNo ratings yet

- SAP Overview PresentationDocument19 pagesSAP Overview PresentationRajesh KumarNo ratings yet

- Term Life Insurance PolicyDocument4 pagesTerm Life Insurance PolicyShubham NamdevNo ratings yet

- Critical Years in The Programming of Life Insurance MeansDocument8 pagesCritical Years in The Programming of Life Insurance MeansRomz Ninz HernandezNo ratings yet

- Knowledge Center GlossaryDocument3 pagesKnowledge Center Glossarychezzter25No ratings yet

- Savings Assurance PlanDocument1 pageSavings Assurance Planrajeshdubey7No ratings yet

- Guarantee and OptionsDocument1 pageGuarantee and OptionsRashi JainNo ratings yet

- Types of Life Insurance PoliciesDocument21 pagesTypes of Life Insurance PoliciesDivya PillaiNo ratings yet

- Term Life Insurance FinalDocument10 pagesTerm Life Insurance FinalsearchingnobodyNo ratings yet

- Need For Life InsuranceDocument9 pagesNeed For Life InsuranceDeepak NayakNo ratings yet

- Product Summary:: Jeevan ChhayaDocument4 pagesProduct Summary:: Jeevan ChhayaSumit PandeyNo ratings yet

- Aviva Life InsuranceDocument3 pagesAviva Life InsuranceumashankarsinghNo ratings yet

- Life InsuranceDocument3 pagesLife Insuranceshailen2uNo ratings yet

- Children Insurance Plan: Presented byDocument23 pagesChildren Insurance Plan: Presented byRohit MalviyaNo ratings yet

- Tips While Buying A Child Education PlanDocument7 pagesTips While Buying A Child Education PlanJyotsana SachdevaNo ratings yet

- IDBI Federal Lifesurance Savings Insurance PlanDocument16 pagesIDBI Federal Lifesurance Savings Insurance PlanKumarniksNo ratings yet

- Life Insurance Products & Terms PDFDocument16 pagesLife Insurance Products & Terms PDFSuman SinhaNo ratings yet

- Irda - Hand Book On Life InsuranceDocument12 pagesIrda - Hand Book On Life InsuranceRajesh SinghNo ratings yet

- Life Insurance FAQsDocument3 pagesLife Insurance FAQsEdappon100% (2)

- eEASY Save FAQs PDFDocument6 pageseEASY Save FAQs PDFterrygohNo ratings yet

- What Is Life Insurance?Document11 pagesWhat Is Life Insurance?Ratul BanerjeeNo ratings yet

- Life Insurance:: Principles & Practices of Insurance Unit 3Document6 pagesLife Insurance:: Principles & Practices of Insurance Unit 3ashishsinghashishNo ratings yet

- Life Insurance HandbookDocument12 pagesLife Insurance HandbookChi MnuNo ratings yet

- Life Health and Disability 1Document47 pagesLife Health and Disability 1Muhammad ArshadNo ratings yet

- Module 3 - Insurance Transaction DocumentsDocument6 pagesModule 3 - Insurance Transaction DocumentsAshwinNo ratings yet

- AR Educare Advantage Insurance Plan 5 May 2014Document6 pagesAR Educare Advantage Insurance Plan 5 May 2014ÌmřańNo ratings yet

- I Don't Want To Postpone My Loved Ones' Aspirations: Bharti AXA Life Secure Income PlanDocument15 pagesI Don't Want To Postpone My Loved Ones' Aspirations: Bharti AXA Life Secure Income PlanSandhya AgrawalNo ratings yet

- Task 4Document6 pagesTask 4sahilNo ratings yet

- Investment Plan IncludesDocument4 pagesInvestment Plan IncludesNusrat IslamNo ratings yet

- Insurance & Risk ManagementDocument8 pagesInsurance & Risk ManagementJASONM22No ratings yet

- Forbes Life InvaderDocument19 pagesForbes Life Invaderapi-270707231No ratings yet

- 1Document6 pages1Lalosa Fritz Angela R.No ratings yet

- Life InsuranceDocument26 pagesLife Insurancevivek kant100% (1)

- PRUlink Protection Plus Account EBrochure EnglishDocument8 pagesPRUlink Protection Plus Account EBrochure EnglishjasonNo ratings yet

- Secure Income PlanDocument15 pagesSecure Income PlanSuyash PrasadNo ratings yet

- Product & ServiceDocument11 pagesProduct & ServicefarrukhNo ratings yet

- SBI LIFE INSURANCE - Smart Scholar Brochure V1Document16 pagesSBI LIFE INSURANCE - Smart Scholar Brochure V1Babujee K.NNo ratings yet

- Life Insurance ProductsDocument43 pagesLife Insurance ProductsinvaapNo ratings yet

- Life InsuranceDocument28 pagesLife Insurancejubaida khanamNo ratings yet

- Life Insurance Is A Contract Between The Policy Owner andDocument23 pagesLife Insurance Is A Contract Between The Policy Owner andshankarinadar100% (1)

- Unit - 3 Bilp Types of Life Insurance - Features - ConditionsDocument9 pagesUnit - 3 Bilp Types of Life Insurance - Features - ConditionsYashika GuptaNo ratings yet

- Reliance Life Care For You Plan: We Protect, We CareDocument25 pagesReliance Life Care For You Plan: We Protect, We CareBabujee K.NNo ratings yet

- Whole Life InsuranceDocument16 pagesWhole Life Insuranceemilda_samuel211No ratings yet

- Insuranace Notes - Bonus, Surrender, LoanDocument8 pagesInsuranace Notes - Bonus, Surrender, LoanManidevNo ratings yet

- Jagendra Kumar RenewedDocument7 pagesJagendra Kumar RenewedbcibaneNo ratings yet

- Life InsuranceDocument22 pagesLife Insuranceckchetankhatri967No ratings yet

- 1 Types of Life Insurance Plans & ULIPSDocument40 pages1 Types of Life Insurance Plans & ULIPSJaswanth Singh RajpurohitNo ratings yet

- FinanceDocument25 pagesFinanceShaun D'souzaNo ratings yet

- Insurance ....Document8 pagesInsurance ....SanyaNo ratings yet

- Super Cash GainDocument2 pagesSuper Cash GainElangovan PurushothamanNo ratings yet

- 8 (22) (Read-Only)Document54 pages8 (22) (Read-Only)Kookie ShresthaNo ratings yet

- Postal Life InsuranceDocument12 pagesPostal Life Insurancesupersaiyan_gohanNo ratings yet

- Assurance PlanDocument1 pageAssurance Planswetaagarwal2706No ratings yet

- Chapter - 1 Life & Health InsuranceDocument38 pagesChapter - 1 Life & Health InsurancehelloNo ratings yet

- Life Insurance ProductsDocument6 pagesLife Insurance ProductsBharani GogulaNo ratings yet

- Insurance Terms Glossary - Insurance Meaning of Terms - Deffinition of Insurance TerminologyDocument7 pagesInsurance Terms Glossary - Insurance Meaning of Terms - Deffinition of Insurance TerminologyGreg Alkovitz100% (1)

- Kotak Complete Cover Group PlanDocument7 pagesKotak Complete Cover Group PlanGens GeorgeNo ratings yet

- Textbook of Urgent Care Management: Chapter 9, Insurance Requirements for the Urgent Care CenterFrom EverandTextbook of Urgent Care Management: Chapter 9, Insurance Requirements for the Urgent Care CenterNo ratings yet

- The Basics of Life Insurance: The Answer to What Life Insurance is and How It Works: Personal Finance, #1From EverandThe Basics of Life Insurance: The Answer to What Life Insurance is and How It Works: Personal Finance, #1No ratings yet

- Comparative Analysis Under GST RegimeDocument5 pagesComparative Analysis Under GST RegimeAmita SinwarNo ratings yet

- 6QQMN972 Lecture 8Document24 pages6QQMN972 Lecture 8yash.jiwaNo ratings yet

- Ta 12 Bab2Document9 pagesTa 12 Bab2BelaynehYitayewNo ratings yet

- John Sobredo - Summative AssessmentDocument2 pagesJohn Sobredo - Summative Assessmentsandra mae dulayNo ratings yet

- RAI Business Survey - Round 6 - OverallDocument7 pagesRAI Business Survey - Round 6 - OverallSriniNo ratings yet

- GEC State of The World FinalDocument17 pagesGEC State of The World Finalvivek0724bryantNo ratings yet

- ResumeDocument4 pagesResumeNasir AhmedNo ratings yet

- Sales Quotation: Salesman Sign: Customer SignDocument1 pageSales Quotation: Salesman Sign: Customer SignjacobNo ratings yet

- Documents 4598779043Document5 pagesDocuments 4598779043edgar aboNo ratings yet

- CH 13Document80 pagesCH 13ddNo ratings yet

- Arf 1 Form-TnpgtaDocument12 pagesArf 1 Form-TnpgtaGnanam SekaranNo ratings yet

- Global Business Strategy: E Xplanatory Session 7: Strategy Formulation: Situation Analysis and Business StrategyDocument45 pagesGlobal Business Strategy: E Xplanatory Session 7: Strategy Formulation: Situation Analysis and Business StrategyAstridNo ratings yet

- KK NESAR Projects PVT LTD KK NESAR Projects PVT LTD KK NESAR Projects PVT LTD KK NESAR Projects PVT LTDDocument6 pagesKK NESAR Projects PVT LTD KK NESAR Projects PVT LTD KK NESAR Projects PVT LTD KK NESAR Projects PVT LTDsnairmNo ratings yet

- Batch Processing Using Sequential FilesDocument2 pagesBatch Processing Using Sequential FilesDaniel TadejaNo ratings yet

- Financial Markets - Week 4Document23 pagesFinancial Markets - Week 4gonzgd90No ratings yet

- Tapio Lappi-Seppälä - "Trust, Welfare and Political Economy"Document33 pagesTapio Lappi-Seppälä - "Trust, Welfare and Political Economy"Anonymous Yrp5vpfXNo ratings yet

- Quiz 1 Stratcost F Edited 1Document4 pagesQuiz 1 Stratcost F Edited 1Aeron Arroyo IINo ratings yet

- Solution Manual For Modern Advanced Accounting in Canada 9th Edition Darrell Herauf Murray HiltonDocument35 pagesSolution Manual For Modern Advanced Accounting in Canada 9th Edition Darrell Herauf Murray Hiltoncravingcoarctdbw6wNo ratings yet

- Markscheme November 2018 Global Politics Higher Level and Standard Level Paper 2Document13 pagesMarkscheme November 2018 Global Politics Higher Level and Standard Level Paper 2kakeguruiNo ratings yet

- Real Property Tax Audit With Management Comment and ExhibitsDocument29 pagesReal Property Tax Audit With Management Comment and ExhibitsDaily FreemanNo ratings yet

- Factors Affecting Development of Internet Banking in NepalDocument9 pagesFactors Affecting Development of Internet Banking in NepalMadridista KroosNo ratings yet

- FYBCOM Business Economics Sem IDocument116 pagesFYBCOM Business Economics Sem IDarshan Tajne100% (1)

- Strategic Supply Chain Management-The Case of Toyota UAEDocument23 pagesStrategic Supply Chain Management-The Case of Toyota UAEurbanus matiluNo ratings yet

- Theme 1 Sem 2 Educating Girls Is A Real LifesaverDocument5 pagesTheme 1 Sem 2 Educating Girls Is A Real LifesaverDobre_georgiana910% (1)

- Crams - 1Document28 pagesCrams - 1Janam AroraNo ratings yet

- Corporate Presentation (Company Update)Document39 pagesCorporate Presentation (Company Update)Shyam SunderNo ratings yet

- MBA (Integrated) - 5th - Year - 2022 - 23 - RDocument44 pagesMBA (Integrated) - 5th - Year - 2022 - 23 - Rchutiya collegeNo ratings yet