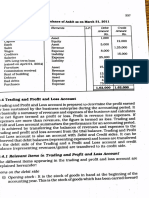

Blank Effects of Business Transactions in The Accounting Equation

Blank Effects of Business Transactions in The Accounting Equation

You might also like

- OutputDocument19 pagesOutputJohnson WilliamNo ratings yet

- Paper From Advance America Cash AdvanceDocument6 pagesPaper From Advance America Cash AdvanceJoyNo ratings yet

- Japan Land - Case StudyDocument2 pagesJapan Land - Case Studypriyaa0380% (10)

- Chapter 3 Market Opportunity Analysis and Consumer AnalysisDocument2 pagesChapter 3 Market Opportunity Analysis and Consumer AnalysisRonald Catapang88% (8)

- Case 4 Numi TeaDocument1 pageCase 4 Numi TeaRonald Catapang50% (2)

- Bessemer's Top 10 Laws For Being SaaS-yDocument11 pagesBessemer's Top 10 Laws For Being SaaS-yjon.byrum9105100% (4)

- The Accounting Equation (Financial Accounting)Document5 pagesThe Accounting Equation (Financial Accounting)RidwanAbirNo ratings yet

- Week 2-1 SlidesDocument30 pagesWeek 2-1 SlidesLIAW ANN YINo ratings yet

- Acct615 NjitDocument24 pagesAcct615 NjithjnNo ratings yet

- Ch.1: Accounting in Action (Cont'd)Document29 pagesCh.1: Accounting in Action (Cont'd)mariam raafatNo ratings yet

- Revision On Principle of Accounting: by Isb Academic TeamDocument37 pagesRevision On Principle of Accounting: by Isb Academic TeamDoan BùiNo ratings yet

- L2 - Accounting Equation & Transaction Analysis - Edited With AnsswerDocument39 pagesL2 - Accounting Equation & Transaction Analysis - Edited With AnsswerEslam SamyNo ratings yet

- Chapter3+4UsingT-Accounts 2Document37 pagesChapter3+4UsingT-Accounts 2الغيثيNo ratings yet

- Ch.2 - Recording Business Transactions (Pearson 6th Edition) - MHDocument56 pagesCh.2 - Recording Business Transactions (Pearson 6th Edition) - MHSamZhao100% (1)

- Analysis of Business TransactionsDocument21 pagesAnalysis of Business TransactionsDan Gideon Cariaga100% (1)

- Chapter 2 HINM 318Document41 pagesChapter 2 HINM 318MOHAMMAD BORENENo ratings yet

- Accounting Equation & Financial ReportingDocument36 pagesAccounting Equation & Financial ReportingAnelisa IvyNo ratings yet

- 01 PowerpointDocument64 pages01 PowerpointVave IsraelNo ratings yet

- Chapter 1 Notes - StudentDocument6 pagesChapter 1 Notes - StudentMia PerdueNo ratings yet

- Accounting Essentials Chapter 3 SynthesisDocument1 pageAccounting Essentials Chapter 3 SynthesisdaraNo ratings yet

- 5# 4 Accounting Equation (UnSolved) PDFDocument4 pages5# 4 Accounting Equation (UnSolved) PDFZaheer SwatiNo ratings yet

- Finance+Webinar 13.12.2022++updatedDocument42 pagesFinance+Webinar 13.12.2022++updatedJasmine ChoudharyNo ratings yet

- AccountingDocument67 pagesAccountinggunanNo ratings yet

- Accounting Equation 2023Document2 pagesAccounting Equation 2023Nishtha GargNo ratings yet

- Use The Accounting Equation To Analyze Business TransactionsDocument36 pagesUse The Accounting Equation To Analyze Business TransactionsPradeep GuptaNo ratings yet

- Accounting Equation: Fundamentals of ABM 1Document97 pagesAccounting Equation: Fundamentals of ABM 1ediwowNo ratings yet

- Ratio AnalysisDocument1 pageRatio AnalysisMuskan hamdevNo ratings yet

- Topic 2 Accounting Equation and StatementsDocument47 pagesTopic 2 Accounting Equation and StatementsNurul AfiqahNo ratings yet

- Illustrating The Accounting Equation: Background Information For LearnersDocument6 pagesIllustrating The Accounting Equation: Background Information For LearnersMarlyn LotivioNo ratings yet

- Professional Accounting PackageDocument72 pagesProfessional Accounting PackageAnmol poudelNo ratings yet

- CFAB Accounting Chap02 Accounting EquationDocument38 pagesCFAB Accounting Chap02 Accounting EquationHoa NguyễnNo ratings yet

- Chapter 7 The Accounting EquationDocument20 pagesChapter 7 The Accounting EquationMylene Salvador100% (1)

- Financial Accounting I: Winter 2020-Lecture "2"Document32 pagesFinancial Accounting I: Winter 2020-Lecture "2"Malak RabieNo ratings yet

- Accounting ProcessDocument13 pagesAccounting ProcessXiavNo ratings yet

- Chapter 2 Accounting ElementsDocument40 pagesChapter 2 Accounting ElementsVivek GargNo ratings yet

- Lecture02-Introduction To AccountingDocument38 pagesLecture02-Introduction To Accounting錢永健No ratings yet

- Work Book XI-CommerceDocument92 pagesWork Book XI-CommerceTariq IqbalNo ratings yet

- CHAPTER 5 The Accounting EquationDocument35 pagesCHAPTER 5 The Accounting EquationKyla BallesterosNo ratings yet

- Training Financial AccountingDocument23 pagesTraining Financial AccountingSara PiccioliNo ratings yet

- Double Entry System & Accounting Equation: by - Mrs. Dilshad D. JalnawallaDocument34 pagesDouble Entry System & Accounting Equation: by - Mrs. Dilshad D. JalnawallaTufail GanaieNo ratings yet

- Accounts, Accountants and AccrualsDocument20 pagesAccounts, Accountants and Accrualsjcmail999446No ratings yet

- 3-THEORY AND APPLICATION OF ACCOUNTING EQUALITY (Morning Shift) (1) - 3Document24 pages3-THEORY AND APPLICATION OF ACCOUNTING EQUALITY (Morning Shift) (1) - 3ScribdTranslationsNo ratings yet

- Lecture Slides - Chapter 1 2Document69 pagesLecture Slides - Chapter 1 2Nhi BuiNo ratings yet

- Chapter Lecture - RemovedDocument43 pagesChapter Lecture - RemovedCJ MacasioNo ratings yet

- Financial Accounting 188 Canva CPT 2-3Document7 pagesFinancial Accounting 188 Canva CPT 2-3marizanne krugerNo ratings yet

- 1.6 Accounting EquationDocument8 pages1.6 Accounting EquationAbijit GudaNo ratings yet

- Chapter Accounting EquationDocument24 pagesChapter Accounting Equationpriyam.200409No ratings yet

- What Is Accounting?: Is A Process of Three Activities: Identifying Recording CommunicatingDocument41 pagesWhat Is Accounting?: Is A Process of Three Activities: Identifying Recording CommunicatingMd. Haseeb KhanNo ratings yet

- Basic Accounting EquationDocument42 pagesBasic Accounting Equationlily smithNo ratings yet

- 1st Assignment - 2023Document15 pages1st Assignment - 2023harmanchahalNo ratings yet

- BBFA1103 Topic 3 Accounting Cycle - NoteDocument13 pagesBBFA1103 Topic 3 Accounting Cycle - Noteknea9999No ratings yet

- Accounting ConceptDocument1 pageAccounting ConceptNISHANTH P CHOYAL 2228512No ratings yet

- AfM 0 - Introduction, Transaction Recognition, AccountsDocument30 pagesAfM 0 - Introduction, Transaction Recognition, AccountsjaymursalieNo ratings yet

- BASIC ACCOUNTING PRACTICE - MISSING AMOUNTS-4Document14 pagesBASIC ACCOUNTING PRACTICE - MISSING AMOUNTS-4randel10caneteNo ratings yet

- Chapter 7 The Accounting Equation RevisedDocument21 pagesChapter 7 The Accounting Equation RevisedJesseca JosafatNo ratings yet

- Accounting Equation and Transaction AnalysisDocument6 pagesAccounting Equation and Transaction AnalysisRR SarkarNo ratings yet

- Clase 14 ITAM Financial Statements & Models Otoño 2017Document25 pagesClase 14 ITAM Financial Statements & Models Otoño 2017Gabriel Ruiz HerreraNo ratings yet

- Accounting C2 Lesson 2 PDFDocument6 pagesAccounting C2 Lesson 2 PDFJake ShimNo ratings yet

- Chapter 2 FinalDocument60 pagesChapter 2 FinalAna María Del CerroNo ratings yet

- Principle of Accounting 1Document25 pagesPrinciple of Accounting 1Quỳnh Trang NguyễnNo ratings yet

- Accounting Part 1Document2 pagesAccounting Part 1Nabeel SiddiquiNo ratings yet

- Bsoa 3 2 Fundamental of AccountingDocument15 pagesBsoa 3 2 Fundamental of AccountingAzalea CruzNo ratings yet

- 4ACCN002W Lecture 2 - TaggedDocument47 pages4ACCN002W Lecture 2 - Taggedredwaanmo19No ratings yet

- Accounting Grade 10 - 12 How To Teach Acc EquationDocument11 pagesAccounting Grade 10 - 12 How To Teach Acc Equationnkambulentokozo55No ratings yet

- Podar International School: 1. Introduction To AccountingDocument3 pagesPodar International School: 1. Introduction To AccountingDhairya AilaniNo ratings yet

- MarketingDocument2 pagesMarketingRonald CatapangNo ratings yet

- Case 5.1 China's Me GenerationDocument1 pageCase 5.1 China's Me GenerationRonald Catapang100% (1)

- Case 8 Why Social Media Advertising Is Set To Explode in The Next 3 YearsDocument2 pagesCase 8 Why Social Media Advertising Is Set To Explode in The Next 3 YearsRonald CatapangNo ratings yet

- Case 2Document1 pageCase 2Ronald CatapangNo ratings yet

- Case 6 Green As A Status SymbolDocument2 pagesCase 6 Green As A Status SymbolRonald CatapangNo ratings yet

- Nature and Concept of ManagementDocument28 pagesNature and Concept of ManagementRonald Catapang100% (1)

- Latihan Soal Pertemuan Ke-6Document15 pagesLatihan Soal Pertemuan Ke-6gloria rachelNo ratings yet

- Rural Godown SchemeDocument5 pagesRural Godown SchemeBhaskaran VenkatesanNo ratings yet

- DBA 5005 Strategic Investment and Financing DecisionsDocument263 pagesDBA 5005 Strategic Investment and Financing DecisionsShrividhyaNo ratings yet

- Trade Finance Letter of Credit (Buy & Sell) in SAP Treasury: BackgroundDocument15 pagesTrade Finance Letter of Credit (Buy & Sell) in SAP Treasury: BackgroundDillip Kumar mallickNo ratings yet

- Industry ProfileDocument26 pagesIndustry ProfileVish SolankiNo ratings yet

- BioMass Business Match-Making CatalogueDocument58 pagesBioMass Business Match-Making Catalogueknizam13No ratings yet

- SITXFIN003Document2 pagesSITXFIN003ozdiploma assignmentsNo ratings yet

- Futurpreneur Cash Flow Template EN 09.08.2022 1Document10 pagesFuturpreneur Cash Flow Template EN 09.08.2022 1Alex VelascoNo ratings yet

- Government of Telangana: PAYSLIP:-MAR-2021Document3 pagesGovernment of Telangana: PAYSLIP:-MAR-2021siva sankar ReddyNo ratings yet

- This Time: Q & A Woods SquareDocument19 pagesThis Time: Q & A Woods SquareChen YishengNo ratings yet

- Chapter 4 Lecture NotesDocument30 pagesChapter 4 Lecture NotesStacy SMNo ratings yet

- Capital Investment Factors - UST2021Document19 pagesCapital Investment Factors - UST2021Ey B0ssNo ratings yet

- Uncertainty, Data & Judgement: Extra ExercisesDocument53 pagesUncertainty, Data & Judgement: Extra ExercisesSergio GoldinNo ratings yet

- Gat Sample Test 01 PDFDocument23 pagesGat Sample Test 01 PDFAamir Ali SeelroNo ratings yet

- CH-1 Advanced FADocument54 pagesCH-1 Advanced FAamogneNo ratings yet

- o CQWyh NZa PVQK 8 WDocument4 pageso CQWyh NZa PVQK 8 WHimanshuNo ratings yet

- Billing of Revenue or Income: Name: Jean Rose T. Bustamante Bsma - 3Document4 pagesBilling of Revenue or Income: Name: Jean Rose T. Bustamante Bsma - 3Jean Rose Tabagay BustamanteNo ratings yet

- Leland Blank, Anthony Tarquin-Engineering Economy-McGraw-Hill Science - Engineering - Math (2011) - 107-114Document8 pagesLeland Blank, Anthony Tarquin-Engineering Economy-McGraw-Hill Science - Engineering - Math (2011) - 107-114ATEH ARMSTRONG AKOTEHNo ratings yet

- Annexure To Trading & Demat Account Opening Form: Power of Attorney (This Document Is Voluntary)Document3 pagesAnnexure To Trading & Demat Account Opening Form: Power of Attorney (This Document Is Voluntary)Consultant NowFoundationNo ratings yet

- Brochure Infodev Incubation Training Nov13 PDFDocument34 pagesBrochure Infodev Incubation Training Nov13 PDFSusiraniNo ratings yet

- Law of EquityDocument17 pagesLaw of EquityAnkitaSharma100% (2)

- RHB CapitalDocument93 pagesRHB CapitalJames WarrenNo ratings yet

- New Government Accounting System NGASDocument20 pagesNew Government Accounting System NGASIsiah Jarrett Trinidad Abille100% (1)

- 582912020511776rpos PDFDocument3 pages582912020511776rpos PDFKarthik sankarNo ratings yet

- Mixed Log Normal Volatility Model OpenGammaDocument9 pagesMixed Log Normal Volatility Model OpenGammamshchetkNo ratings yet

- 1.isidore EkpeDocument27 pages1.isidore Ekpe9415351296No ratings yet

Download as docx, pdf, or txt

You might also like

- OutputDocument19 pagesOutputJohnson WilliamNo ratings yet

- Paper From Advance America Cash AdvanceDocument6 pagesPaper From Advance America Cash AdvanceJoyNo ratings yet

- Japan Land - Case StudyDocument2 pagesJapan Land - Case Studypriyaa0380% (10)

- Chapter 3 Market Opportunity Analysis and Consumer AnalysisDocument2 pagesChapter 3 Market Opportunity Analysis and Consumer AnalysisRonald Catapang88% (8)

- Case 4 Numi TeaDocument1 pageCase 4 Numi TeaRonald Catapang50% (2)

- Bessemer's Top 10 Laws For Being SaaS-yDocument11 pagesBessemer's Top 10 Laws For Being SaaS-yjon.byrum9105100% (4)

- The Accounting Equation (Financial Accounting)Document5 pagesThe Accounting Equation (Financial Accounting)RidwanAbirNo ratings yet

- Week 2-1 SlidesDocument30 pagesWeek 2-1 SlidesLIAW ANN YINo ratings yet

- Acct615 NjitDocument24 pagesAcct615 NjithjnNo ratings yet

- Ch.1: Accounting in Action (Cont'd)Document29 pagesCh.1: Accounting in Action (Cont'd)mariam raafatNo ratings yet

- Revision On Principle of Accounting: by Isb Academic TeamDocument37 pagesRevision On Principle of Accounting: by Isb Academic TeamDoan BùiNo ratings yet

- L2 - Accounting Equation & Transaction Analysis - Edited With AnsswerDocument39 pagesL2 - Accounting Equation & Transaction Analysis - Edited With AnsswerEslam SamyNo ratings yet

- Chapter3+4UsingT-Accounts 2Document37 pagesChapter3+4UsingT-Accounts 2الغيثيNo ratings yet

- Ch.2 - Recording Business Transactions (Pearson 6th Edition) - MHDocument56 pagesCh.2 - Recording Business Transactions (Pearson 6th Edition) - MHSamZhao100% (1)

- Analysis of Business TransactionsDocument21 pagesAnalysis of Business TransactionsDan Gideon Cariaga100% (1)

- Chapter 2 HINM 318Document41 pagesChapter 2 HINM 318MOHAMMAD BORENENo ratings yet

- Accounting Equation & Financial ReportingDocument36 pagesAccounting Equation & Financial ReportingAnelisa IvyNo ratings yet

- 01 PowerpointDocument64 pages01 PowerpointVave IsraelNo ratings yet

- Chapter 1 Notes - StudentDocument6 pagesChapter 1 Notes - StudentMia PerdueNo ratings yet

- Accounting Essentials Chapter 3 SynthesisDocument1 pageAccounting Essentials Chapter 3 SynthesisdaraNo ratings yet

- 5# 4 Accounting Equation (UnSolved) PDFDocument4 pages5# 4 Accounting Equation (UnSolved) PDFZaheer SwatiNo ratings yet

- Finance+Webinar 13.12.2022++updatedDocument42 pagesFinance+Webinar 13.12.2022++updatedJasmine ChoudharyNo ratings yet

- AccountingDocument67 pagesAccountinggunanNo ratings yet

- Accounting Equation 2023Document2 pagesAccounting Equation 2023Nishtha GargNo ratings yet

- Use The Accounting Equation To Analyze Business TransactionsDocument36 pagesUse The Accounting Equation To Analyze Business TransactionsPradeep GuptaNo ratings yet

- Accounting Equation: Fundamentals of ABM 1Document97 pagesAccounting Equation: Fundamentals of ABM 1ediwowNo ratings yet

- Ratio AnalysisDocument1 pageRatio AnalysisMuskan hamdevNo ratings yet

- Topic 2 Accounting Equation and StatementsDocument47 pagesTopic 2 Accounting Equation and StatementsNurul AfiqahNo ratings yet

- Illustrating The Accounting Equation: Background Information For LearnersDocument6 pagesIllustrating The Accounting Equation: Background Information For LearnersMarlyn LotivioNo ratings yet

- Professional Accounting PackageDocument72 pagesProfessional Accounting PackageAnmol poudelNo ratings yet

- CFAB Accounting Chap02 Accounting EquationDocument38 pagesCFAB Accounting Chap02 Accounting EquationHoa NguyễnNo ratings yet

- Chapter 7 The Accounting EquationDocument20 pagesChapter 7 The Accounting EquationMylene Salvador100% (1)

- Financial Accounting I: Winter 2020-Lecture "2"Document32 pagesFinancial Accounting I: Winter 2020-Lecture "2"Malak RabieNo ratings yet

- Accounting ProcessDocument13 pagesAccounting ProcessXiavNo ratings yet

- Chapter 2 Accounting ElementsDocument40 pagesChapter 2 Accounting ElementsVivek GargNo ratings yet

- Lecture02-Introduction To AccountingDocument38 pagesLecture02-Introduction To Accounting錢永健No ratings yet

- Work Book XI-CommerceDocument92 pagesWork Book XI-CommerceTariq IqbalNo ratings yet

- CHAPTER 5 The Accounting EquationDocument35 pagesCHAPTER 5 The Accounting EquationKyla BallesterosNo ratings yet

- Training Financial AccountingDocument23 pagesTraining Financial AccountingSara PiccioliNo ratings yet

- Double Entry System & Accounting Equation: by - Mrs. Dilshad D. JalnawallaDocument34 pagesDouble Entry System & Accounting Equation: by - Mrs. Dilshad D. JalnawallaTufail GanaieNo ratings yet

- Accounts, Accountants and AccrualsDocument20 pagesAccounts, Accountants and Accrualsjcmail999446No ratings yet

- 3-THEORY AND APPLICATION OF ACCOUNTING EQUALITY (Morning Shift) (1) - 3Document24 pages3-THEORY AND APPLICATION OF ACCOUNTING EQUALITY (Morning Shift) (1) - 3ScribdTranslationsNo ratings yet

- Lecture Slides - Chapter 1 2Document69 pagesLecture Slides - Chapter 1 2Nhi BuiNo ratings yet

- Chapter Lecture - RemovedDocument43 pagesChapter Lecture - RemovedCJ MacasioNo ratings yet

- Financial Accounting 188 Canva CPT 2-3Document7 pagesFinancial Accounting 188 Canva CPT 2-3marizanne krugerNo ratings yet

- 1.6 Accounting EquationDocument8 pages1.6 Accounting EquationAbijit GudaNo ratings yet

- Chapter Accounting EquationDocument24 pagesChapter Accounting Equationpriyam.200409No ratings yet

- What Is Accounting?: Is A Process of Three Activities: Identifying Recording CommunicatingDocument41 pagesWhat Is Accounting?: Is A Process of Three Activities: Identifying Recording CommunicatingMd. Haseeb KhanNo ratings yet

- Basic Accounting EquationDocument42 pagesBasic Accounting Equationlily smithNo ratings yet

- 1st Assignment - 2023Document15 pages1st Assignment - 2023harmanchahalNo ratings yet

- BBFA1103 Topic 3 Accounting Cycle - NoteDocument13 pagesBBFA1103 Topic 3 Accounting Cycle - Noteknea9999No ratings yet

- Accounting ConceptDocument1 pageAccounting ConceptNISHANTH P CHOYAL 2228512No ratings yet

- AfM 0 - Introduction, Transaction Recognition, AccountsDocument30 pagesAfM 0 - Introduction, Transaction Recognition, AccountsjaymursalieNo ratings yet

- BASIC ACCOUNTING PRACTICE - MISSING AMOUNTS-4Document14 pagesBASIC ACCOUNTING PRACTICE - MISSING AMOUNTS-4randel10caneteNo ratings yet

- Chapter 7 The Accounting Equation RevisedDocument21 pagesChapter 7 The Accounting Equation RevisedJesseca JosafatNo ratings yet

- Accounting Equation and Transaction AnalysisDocument6 pagesAccounting Equation and Transaction AnalysisRR SarkarNo ratings yet

- Clase 14 ITAM Financial Statements & Models Otoño 2017Document25 pagesClase 14 ITAM Financial Statements & Models Otoño 2017Gabriel Ruiz HerreraNo ratings yet

- Accounting C2 Lesson 2 PDFDocument6 pagesAccounting C2 Lesson 2 PDFJake ShimNo ratings yet

- Chapter 2 FinalDocument60 pagesChapter 2 FinalAna María Del CerroNo ratings yet

- Principle of Accounting 1Document25 pagesPrinciple of Accounting 1Quỳnh Trang NguyễnNo ratings yet

- Accounting Part 1Document2 pagesAccounting Part 1Nabeel SiddiquiNo ratings yet

- Bsoa 3 2 Fundamental of AccountingDocument15 pagesBsoa 3 2 Fundamental of AccountingAzalea CruzNo ratings yet

- 4ACCN002W Lecture 2 - TaggedDocument47 pages4ACCN002W Lecture 2 - Taggedredwaanmo19No ratings yet

- Accounting Grade 10 - 12 How To Teach Acc EquationDocument11 pagesAccounting Grade 10 - 12 How To Teach Acc Equationnkambulentokozo55No ratings yet

- Podar International School: 1. Introduction To AccountingDocument3 pagesPodar International School: 1. Introduction To AccountingDhairya AilaniNo ratings yet

- MarketingDocument2 pagesMarketingRonald CatapangNo ratings yet

- Case 5.1 China's Me GenerationDocument1 pageCase 5.1 China's Me GenerationRonald Catapang100% (1)

- Case 8 Why Social Media Advertising Is Set To Explode in The Next 3 YearsDocument2 pagesCase 8 Why Social Media Advertising Is Set To Explode in The Next 3 YearsRonald CatapangNo ratings yet

- Case 2Document1 pageCase 2Ronald CatapangNo ratings yet

- Case 6 Green As A Status SymbolDocument2 pagesCase 6 Green As A Status SymbolRonald CatapangNo ratings yet

- Nature and Concept of ManagementDocument28 pagesNature and Concept of ManagementRonald Catapang100% (1)

- Latihan Soal Pertemuan Ke-6Document15 pagesLatihan Soal Pertemuan Ke-6gloria rachelNo ratings yet

- Rural Godown SchemeDocument5 pagesRural Godown SchemeBhaskaran VenkatesanNo ratings yet

- DBA 5005 Strategic Investment and Financing DecisionsDocument263 pagesDBA 5005 Strategic Investment and Financing DecisionsShrividhyaNo ratings yet

- Trade Finance Letter of Credit (Buy & Sell) in SAP Treasury: BackgroundDocument15 pagesTrade Finance Letter of Credit (Buy & Sell) in SAP Treasury: BackgroundDillip Kumar mallickNo ratings yet

- Industry ProfileDocument26 pagesIndustry ProfileVish SolankiNo ratings yet

- BioMass Business Match-Making CatalogueDocument58 pagesBioMass Business Match-Making Catalogueknizam13No ratings yet

- SITXFIN003Document2 pagesSITXFIN003ozdiploma assignmentsNo ratings yet

- Futurpreneur Cash Flow Template EN 09.08.2022 1Document10 pagesFuturpreneur Cash Flow Template EN 09.08.2022 1Alex VelascoNo ratings yet

- Government of Telangana: PAYSLIP:-MAR-2021Document3 pagesGovernment of Telangana: PAYSLIP:-MAR-2021siva sankar ReddyNo ratings yet

- This Time: Q & A Woods SquareDocument19 pagesThis Time: Q & A Woods SquareChen YishengNo ratings yet

- Chapter 4 Lecture NotesDocument30 pagesChapter 4 Lecture NotesStacy SMNo ratings yet

- Capital Investment Factors - UST2021Document19 pagesCapital Investment Factors - UST2021Ey B0ssNo ratings yet

- Uncertainty, Data & Judgement: Extra ExercisesDocument53 pagesUncertainty, Data & Judgement: Extra ExercisesSergio GoldinNo ratings yet

- Gat Sample Test 01 PDFDocument23 pagesGat Sample Test 01 PDFAamir Ali SeelroNo ratings yet

- CH-1 Advanced FADocument54 pagesCH-1 Advanced FAamogneNo ratings yet

- o CQWyh NZa PVQK 8 WDocument4 pageso CQWyh NZa PVQK 8 WHimanshuNo ratings yet

- Billing of Revenue or Income: Name: Jean Rose T. Bustamante Bsma - 3Document4 pagesBilling of Revenue or Income: Name: Jean Rose T. Bustamante Bsma - 3Jean Rose Tabagay BustamanteNo ratings yet

- Leland Blank, Anthony Tarquin-Engineering Economy-McGraw-Hill Science - Engineering - Math (2011) - 107-114Document8 pagesLeland Blank, Anthony Tarquin-Engineering Economy-McGraw-Hill Science - Engineering - Math (2011) - 107-114ATEH ARMSTRONG AKOTEHNo ratings yet

- Annexure To Trading & Demat Account Opening Form: Power of Attorney (This Document Is Voluntary)Document3 pagesAnnexure To Trading & Demat Account Opening Form: Power of Attorney (This Document Is Voluntary)Consultant NowFoundationNo ratings yet

- Brochure Infodev Incubation Training Nov13 PDFDocument34 pagesBrochure Infodev Incubation Training Nov13 PDFSusiraniNo ratings yet

- Law of EquityDocument17 pagesLaw of EquityAnkitaSharma100% (2)

- RHB CapitalDocument93 pagesRHB CapitalJames WarrenNo ratings yet

- New Government Accounting System NGASDocument20 pagesNew Government Accounting System NGASIsiah Jarrett Trinidad Abille100% (1)

- 582912020511776rpos PDFDocument3 pages582912020511776rpos PDFKarthik sankarNo ratings yet

- Mixed Log Normal Volatility Model OpenGammaDocument9 pagesMixed Log Normal Volatility Model OpenGammamshchetkNo ratings yet

- 1.isidore EkpeDocument27 pages1.isidore Ekpe9415351296No ratings yet