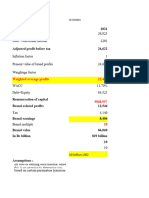

Dupont 1

Dupont 1

You might also like

- EVA Analysis: Case: Vyaderm PharmaceuticalsDocument56 pagesEVA Analysis: Case: Vyaderm Pharmaceuticalsjk kumarNo ratings yet

- Financial Analysis of - Toys "R" Us, Inc.Document30 pagesFinancial Analysis of - Toys "R" Us, Inc.Arabi AsadNo ratings yet

- 2007.10.29 Paulson Credit Crisis PresentationDocument34 pages2007.10.29 Paulson Credit Crisis Presentationadjk97No ratings yet

- 1) Permanent Audit File IndexDocument6 pages1) Permanent Audit File IndexPurnamaAjiNo ratings yet

- Chapter 2 Financial Statement and Cash Flow AnalysisDocument15 pagesChapter 2 Financial Statement and Cash Flow AnalysisKapil Singh RautelaNo ratings yet

- Dry Bulk Product Safety SOPDocument14 pagesDry Bulk Product Safety SOPWan Sek Choon100% (1)

- BCG Reigniting Radical Growth June 2019 Tcm9 222638Document33 pagesBCG Reigniting Radical Growth June 2019 Tcm9 222638sdadaaNo ratings yet

- Chap1 - BA211 Business CommunicationDocument5 pagesChap1 - BA211 Business Communicationkenozin272100% (2)

- Outlook For Corporate ProfitsDocument27 pagesOutlook For Corporate ProfitsDharmendra B MistryNo ratings yet

- Sales Growth Rate: Richard L. Keyser Chairman and Chief Executive OfficerDocument57 pagesSales Growth Rate: Richard L. Keyser Chairman and Chief Executive OfficerchabucaNo ratings yet

- Jeff 030109Document14 pagesJeff 030109Hummels1000No ratings yet

- Accounting: IncomeDocument7 pagesAccounting: IncomeAyesha AliNo ratings yet

- C C C C C C: O O O O O O O ODocument5 pagesC C C C C C: O O O O O O O OTon ThaoNo ratings yet

- Analysts 20030227Document41 pagesAnalysts 20030227gsameera676No ratings yet

- Amity Global Business School Amity Global Business School: Valuation ConceptsDocument36 pagesAmity Global Business School Amity Global Business School: Valuation ConceptssachinremaNo ratings yet

- Sampa Video SpreadsheetDocument4 pagesSampa Video SpreadsheetVarsha ShirsatNo ratings yet

- SWOT Analysis of Grasim Industries LTD (VSF Division) Presented To:-Presented By: - Prof. Nihit Jaiswal Rohit Bhat (MBA 3 Sem)Document51 pagesSWOT Analysis of Grasim Industries LTD (VSF Division) Presented To:-Presented By: - Prof. Nihit Jaiswal Rohit Bhat (MBA 3 Sem)Rohit BhatNo ratings yet

- Weekly Economic Financial Commentary JuneDocument8 pagesWeekly Economic Financial Commentary JunehellbustNo ratings yet

- DangerZone XPO 2016 05 16Document7 pagesDangerZone XPO 2016 05 16Michael Cano LombardoNo ratings yet

- FM11 CH 13 Mini-Case Old3Document14 pagesFM11 CH 13 Mini-Case Old3Wu Tian WenNo ratings yet

- Chandra Asri Earnings Update Q2 2021Document20 pagesChandra Asri Earnings Update Q2 2021Scriptlance 2012No ratings yet

- Data Analysis - ModellingDocument4 pagesData Analysis - ModellinganissamarissaaNo ratings yet

- PRESTIGE Annualreport-Fy-2021-2022Document308 pagesPRESTIGE Annualreport-Fy-2021-2022Ajit PatelNo ratings yet

- Case Study - Financial Statement AnaysisDocument8 pagesCase Study - Financial Statement Anaysisssimi137No ratings yet

- Merger and AkuisisiDocument35 pagesMerger and Akuisisidwi suhartantoNo ratings yet

- Operational ExcellenceDocument24 pagesOperational ExcellenceJonathan WenNo ratings yet

- Sample Questions - Mini-Test 1Document4 pagesSample Questions - Mini-Test 1sam heisenbergNo ratings yet

- FMDocument17 pagesFMRaghav Agarwal100% (3)

- Okta Q4FY22 Earnings Presentation 03.02.22Document59 pagesOkta Q4FY22 Earnings Presentation 03.02.22newscollectingNo ratings yet

- Hilton Colombo Annual Report 2018Document94 pagesHilton Colombo Annual Report 2018Angel MaNo ratings yet

- C - 2021MBA160 - Case ScenariosRBCDocument7 pagesC - 2021MBA160 - Case ScenariosRBCmohammedsuhaim abdul gafoorNo ratings yet

- A 2021MBA030 YuddhaveerSingh CaseScenariosRBCDocument7 pagesA 2021MBA030 YuddhaveerSingh CaseScenariosRBCmohammedsuhaim abdul gafoorNo ratings yet

- TFI InternationalDocument43 pagesTFI InternationalJenny QuachNo ratings yet

- Financial Management: Rajiv Srivastava - Dr. Anil Misra Solutions To Numerical ProblemsDocument9 pagesFinancial Management: Rajiv Srivastava - Dr. Anil Misra Solutions To Numerical ProblemsSakshi BaiwalNo ratings yet

- Wahyu Gunawan - Mid Exam Financial MGT - ENEMBA7Document15 pagesWahyu Gunawan - Mid Exam Financial MGT - ENEMBA7Rydo PrastariNo ratings yet

- Revista de IngenieríasDocument43 pagesRevista de IngenieríasJosé TinocoNo ratings yet

- 4 Completing The Accounting Cycle PartDocument1 page4 Completing The Accounting Cycle PartTalionNo ratings yet

- 1Q23 Earnings Presentation FINALDocument19 pages1Q23 Earnings Presentation FINALCesar AugustoNo ratings yet

- PCM Asia Pioneer FundDocument33 pagesPCM Asia Pioneer FundbessiebuNo ratings yet

- Briarcliffe The Private Credit Compass May 2023Document11 pagesBriarcliffe The Private Credit Compass May 2023NointingNo ratings yet

- Day1 Session 1-2 June 13, 2021Document42 pagesDay1 Session 1-2 June 13, 2021AKSHAY NANGIANo ratings yet

- 423430-1 - 11 Campbell-S-Ar WR SpreadDocument52 pages423430-1 - 11 Campbell-S-Ar WR SpreadPrakhar SinghaniaNo ratings yet

- It's Too Early To Call The End of The Reflation TradeDocument3 pagesIt's Too Early To Call The End of The Reflation TradeJesse100% (1)

- C Fund: Common Stock Index Investment FundDocument2 pagesC Fund: Common Stock Index Investment FundAustinNo ratings yet

- Payslip 2024-02-28Document2 pagesPayslip 2024-02-28elaNo ratings yet

- Annual Report 2020Document118 pagesAnnual Report 2020Albacore EnterprisesNo ratings yet

- C1 Sampa VideoDocument2 pagesC1 Sampa VideoBharadwaja ReddyNo ratings yet

- The Late Cycle Lament The Dual Economy Minsky Moments and Other ConcernsDocument14 pagesThe Late Cycle Lament The Dual Economy Minsky Moments and Other Concernsrchawdhry123No ratings yet

- Cost-Volume-Profit Relationships: Chapter SixDocument70 pagesCost-Volume-Profit Relationships: Chapter SixFadillah AhmadNo ratings yet

- q1 2019 Earnings Website PresentationDocument17 pagesq1 2019 Earnings Website PresentationTitoNo ratings yet

- Group 1 - Chapter 20 - Audit of Other Accounts in The Statement of Profit or Loss and Comprehensive IncomeDocument18 pagesGroup 1 - Chapter 20 - Audit of Other Accounts in The Statement of Profit or Loss and Comprehensive IncomeRhad Lester C. MaestradoNo ratings yet

- 4 4 Analysis of Financial StatementsDocument41 pages4 4 Analysis of Financial StatementskartiktrivediNo ratings yet

- Long-Term Financial Planning: Fundamentals of Corporate FinanceDocument17 pagesLong-Term Financial Planning: Fundamentals of Corporate FinanceMuh BilalNo ratings yet

- ch01 2Document21 pagesch01 2Jigar PatelNo ratings yet

- Service Charges Popcorn Service ProviderDocument3 pagesService Charges Popcorn Service ProviderRajesh SharmaNo ratings yet

- Brand Valuation MethodsDocument23 pagesBrand Valuation MethodsvroommNo ratings yet

- Bci Ex (S) 00024129Document1 pageBci Ex (S) 00024129planetamundo2017No ratings yet

- FMUEDocument5 pagesFMUERushali ParmarNo ratings yet

- Chapter 2 FS and Transaction Analysis PDFDocument53 pagesChapter 2 FS and Transaction Analysis PDFleen mercadoNo ratings yet

- Practice Session - 14 - MayDocument18 pagesPractice Session - 14 - MayprabhuNo ratings yet

- Analysis of The Organizational Reorientation of The ABB GroupDocument34 pagesAnalysis of The Organizational Reorientation of The ABB GroupJayesh PatilNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- Operational Profitability: Systematic Approaches for Continuous ImprovementFrom EverandOperational Profitability: Systematic Approaches for Continuous ImprovementNo ratings yet

- Destiny Luck FengShuiDocument2 pagesDestiny Luck FengShuiWan Sek ChoonNo ratings yet

- Discovery LearningDocument12 pagesDiscovery LearningWan Sek ChoonNo ratings yet

- Neoclassical Economics: Economic Science, To DistinguishDocument35 pagesNeoclassical Economics: Economic Science, To DistinguishWan Sek ChoonNo ratings yet

- This Was The Winning Quote From Fred Dales, Microsoft Corp. in Redmond WADocument4 pagesThis Was The Winning Quote From Fred Dales, Microsoft Corp. in Redmond WAWan Sek ChoonNo ratings yet

- Dudjom RinpocheDocument8 pagesDudjom RinpocheWan Sek ChoonNo ratings yet

- Case Study Module Understanding Transport ChainDocument16 pagesCase Study Module Understanding Transport ChainWan Sek ChoonNo ratings yet

- Defect CornerDocument2 pagesDefect CornerWan Sek ChoonNo ratings yet

- Daily Cycle Weekly Cycle Monthly Cycle: ST NDDocument1 pageDaily Cycle Weekly Cycle Monthly Cycle: ST NDWan Sek ChoonNo ratings yet

- From The Attracting Genuine Abundance On-Line CourseDocument2 pagesFrom The Attracting Genuine Abundance On-Line CourseWan Sek ChoonNo ratings yet

- Model For Continuous Learning: Think 6 ResultsDocument2 pagesModel For Continuous Learning: Think 6 ResultsWan Sek ChoonNo ratings yet

- Challenges of Implementing 9001 2000Document5 pagesChallenges of Implementing 9001 2000Wan Sek ChoonNo ratings yet

- Buying A HouseDocument8 pagesBuying A HouseWan Sek ChoonNo ratings yet

- Chinese New Year Customs and TraditionsDocument21 pagesChinese New Year Customs and TraditionsWan Sek Choon100% (2)

- For The Company Blues: A Pocket Guide For LeadersDocument35 pagesFor The Company Blues: A Pocket Guide For LeadersWan Sek ChoonNo ratings yet

- Chief Learning ManagersDocument2 pagesChief Learning ManagersWan Sek ChoonNo ratings yet

- Challenges Developing Learning OrgDocument6 pagesChallenges Developing Learning OrgWan Sek ChoonNo ratings yet

- Brochure Write UpDocument1 pageBrochure Write UpWan Sek ChoonNo ratings yet

- Statement of Financial Position (Balance Sheet) Test BankDocument4 pagesStatement of Financial Position (Balance Sheet) Test BankJhazz100% (1)

- Arun LamsalDocument50 pagesArun LamsalSmith TiwariNo ratings yet

- Bank of AmericaDocument20 pagesBank of AmericaSingh Gurminder100% (2)

- Toaz - Info Far Vol 2 Chapter 22 25docx PRDocument22 pagesToaz - Info Far Vol 2 Chapter 22 25docx PRVivialyn PalimpingNo ratings yet

- Annual Report PT SieradDocument249 pagesAnnual Report PT SieradNadia IndrianiNo ratings yet

- Chapter 18: Ratio Analysis: Rohit AgarwalDocument3 pagesChapter 18: Ratio Analysis: Rohit Agarwalbcom100% (1)

- Account Titles Trial Balance Adjustment DR CR DR: Vang Management ServicesDocument9 pagesAccount Titles Trial Balance Adjustment DR CR DR: Vang Management ServicesMutia WardaniNo ratings yet

- Summer Training Report at "Financial Performance Analysis With Ratio Analysis With Reference To South Eastern Coal Fields Limited" Bilaspur (C.G.)Document35 pagesSummer Training Report at "Financial Performance Analysis With Ratio Analysis With Reference To South Eastern Coal Fields Limited" Bilaspur (C.G.)Sanskar YadavNo ratings yet

- Chapter06 TestBankDocument50 pagesChapter06 TestBankannie100% (1)

- EASEMYTRIP - Investor Presentation - 06-Feb-23Document26 pagesEASEMYTRIP - Investor Presentation - 06-Feb-23Karan GoelNo ratings yet

- DG Khan Cement Financial StatementsDocument8 pagesDG Khan Cement Financial StatementsAsad BumbiaNo ratings yet

- 1 Chapter 5 Internal Reconstruction PDFDocument22 pages1 Chapter 5 Internal Reconstruction PDFAbhiramNo ratings yet

- Fa Chapt 1-3Document63 pagesFa Chapt 1-3sushNo ratings yet

- Rajiv Talreja Workshop - 18-06-23Document88 pagesRajiv Talreja Workshop - 18-06-23Venkat KamatamNo ratings yet

- Q4-FY23/FY23: Earnings PresentationDocument17 pagesQ4-FY23/FY23: Earnings PresentationGurjeevNo ratings yet

- The Hutchinson Whampoa Case - CLASS 18, BINDING BONDS Marco PattiDocument5 pagesThe Hutchinson Whampoa Case - CLASS 18, BINDING BONDS Marco PattiMarco PattiNo ratings yet

- Makalah Paper Noun Phrase (English Economy)Document11 pagesMakalah Paper Noun Phrase (English Economy)Ines AlissaNo ratings yet

- CCPSDocument2 pagesCCPSelitevaluation2022No ratings yet

- 11Document4 pages11William LanzuelaNo ratings yet

- Ch16 Practice Quiz ProblemsDocument14 pagesCh16 Practice Quiz ProblemswarrenmertzNo ratings yet

- Compare Genp KLKDocument4 pagesCompare Genp KLKJing Sheng QuakNo ratings yet

- UniSwap (18L - (0910, 1055, 1016) )Document19 pagesUniSwap (18L - (0910, 1055, 1016) )RafayGhafoorNo ratings yet

- Answer KeyDocument52 pagesAnswer KeyDevonNo ratings yet

- Imp. A.O MCQDocument19 pagesImp. A.O MCQNadir AhmedNo ratings yet

- Jawaban Case 1 CH 8Document4 pagesJawaban Case 1 CH 8Azim JamalNo ratings yet

- Iamu Posho MillDocument37 pagesIamu Posho MillOCHIENG NICHOLASNo ratings yet

- Financial Accounting I SemesterDocument25 pagesFinancial Accounting I SemesterBhaskar KrishnappaNo ratings yet

- Afar QuestionsDocument16 pagesAfar Questionspopsie tulalianNo ratings yet

Download as pdf or txt

You might also like

- EVA Analysis: Case: Vyaderm PharmaceuticalsDocument56 pagesEVA Analysis: Case: Vyaderm Pharmaceuticalsjk kumarNo ratings yet

- Financial Analysis of - Toys "R" Us, Inc.Document30 pagesFinancial Analysis of - Toys "R" Us, Inc.Arabi AsadNo ratings yet

- 2007.10.29 Paulson Credit Crisis PresentationDocument34 pages2007.10.29 Paulson Credit Crisis Presentationadjk97No ratings yet

- 1) Permanent Audit File IndexDocument6 pages1) Permanent Audit File IndexPurnamaAjiNo ratings yet

- Chapter 2 Financial Statement and Cash Flow AnalysisDocument15 pagesChapter 2 Financial Statement and Cash Flow AnalysisKapil Singh RautelaNo ratings yet

- Dry Bulk Product Safety SOPDocument14 pagesDry Bulk Product Safety SOPWan Sek Choon100% (1)

- BCG Reigniting Radical Growth June 2019 Tcm9 222638Document33 pagesBCG Reigniting Radical Growth June 2019 Tcm9 222638sdadaaNo ratings yet

- Chap1 - BA211 Business CommunicationDocument5 pagesChap1 - BA211 Business Communicationkenozin272100% (2)

- Outlook For Corporate ProfitsDocument27 pagesOutlook For Corporate ProfitsDharmendra B MistryNo ratings yet

- Sales Growth Rate: Richard L. Keyser Chairman and Chief Executive OfficerDocument57 pagesSales Growth Rate: Richard L. Keyser Chairman and Chief Executive OfficerchabucaNo ratings yet

- Jeff 030109Document14 pagesJeff 030109Hummels1000No ratings yet

- Accounting: IncomeDocument7 pagesAccounting: IncomeAyesha AliNo ratings yet

- C C C C C C: O O O O O O O ODocument5 pagesC C C C C C: O O O O O O O OTon ThaoNo ratings yet

- Analysts 20030227Document41 pagesAnalysts 20030227gsameera676No ratings yet

- Amity Global Business School Amity Global Business School: Valuation ConceptsDocument36 pagesAmity Global Business School Amity Global Business School: Valuation ConceptssachinremaNo ratings yet

- Sampa Video SpreadsheetDocument4 pagesSampa Video SpreadsheetVarsha ShirsatNo ratings yet

- SWOT Analysis of Grasim Industries LTD (VSF Division) Presented To:-Presented By: - Prof. Nihit Jaiswal Rohit Bhat (MBA 3 Sem)Document51 pagesSWOT Analysis of Grasim Industries LTD (VSF Division) Presented To:-Presented By: - Prof. Nihit Jaiswal Rohit Bhat (MBA 3 Sem)Rohit BhatNo ratings yet

- Weekly Economic Financial Commentary JuneDocument8 pagesWeekly Economic Financial Commentary JunehellbustNo ratings yet

- DangerZone XPO 2016 05 16Document7 pagesDangerZone XPO 2016 05 16Michael Cano LombardoNo ratings yet

- FM11 CH 13 Mini-Case Old3Document14 pagesFM11 CH 13 Mini-Case Old3Wu Tian WenNo ratings yet

- Chandra Asri Earnings Update Q2 2021Document20 pagesChandra Asri Earnings Update Q2 2021Scriptlance 2012No ratings yet

- Data Analysis - ModellingDocument4 pagesData Analysis - ModellinganissamarissaaNo ratings yet

- PRESTIGE Annualreport-Fy-2021-2022Document308 pagesPRESTIGE Annualreport-Fy-2021-2022Ajit PatelNo ratings yet

- Case Study - Financial Statement AnaysisDocument8 pagesCase Study - Financial Statement Anaysisssimi137No ratings yet

- Merger and AkuisisiDocument35 pagesMerger and Akuisisidwi suhartantoNo ratings yet

- Operational ExcellenceDocument24 pagesOperational ExcellenceJonathan WenNo ratings yet

- Sample Questions - Mini-Test 1Document4 pagesSample Questions - Mini-Test 1sam heisenbergNo ratings yet

- FMDocument17 pagesFMRaghav Agarwal100% (3)

- Okta Q4FY22 Earnings Presentation 03.02.22Document59 pagesOkta Q4FY22 Earnings Presentation 03.02.22newscollectingNo ratings yet

- Hilton Colombo Annual Report 2018Document94 pagesHilton Colombo Annual Report 2018Angel MaNo ratings yet

- C - 2021MBA160 - Case ScenariosRBCDocument7 pagesC - 2021MBA160 - Case ScenariosRBCmohammedsuhaim abdul gafoorNo ratings yet

- A 2021MBA030 YuddhaveerSingh CaseScenariosRBCDocument7 pagesA 2021MBA030 YuddhaveerSingh CaseScenariosRBCmohammedsuhaim abdul gafoorNo ratings yet

- TFI InternationalDocument43 pagesTFI InternationalJenny QuachNo ratings yet

- Financial Management: Rajiv Srivastava - Dr. Anil Misra Solutions To Numerical ProblemsDocument9 pagesFinancial Management: Rajiv Srivastava - Dr. Anil Misra Solutions To Numerical ProblemsSakshi BaiwalNo ratings yet

- Wahyu Gunawan - Mid Exam Financial MGT - ENEMBA7Document15 pagesWahyu Gunawan - Mid Exam Financial MGT - ENEMBA7Rydo PrastariNo ratings yet

- Revista de IngenieríasDocument43 pagesRevista de IngenieríasJosé TinocoNo ratings yet

- 4 Completing The Accounting Cycle PartDocument1 page4 Completing The Accounting Cycle PartTalionNo ratings yet

- 1Q23 Earnings Presentation FINALDocument19 pages1Q23 Earnings Presentation FINALCesar AugustoNo ratings yet

- PCM Asia Pioneer FundDocument33 pagesPCM Asia Pioneer FundbessiebuNo ratings yet

- Briarcliffe The Private Credit Compass May 2023Document11 pagesBriarcliffe The Private Credit Compass May 2023NointingNo ratings yet

- Day1 Session 1-2 June 13, 2021Document42 pagesDay1 Session 1-2 June 13, 2021AKSHAY NANGIANo ratings yet

- 423430-1 - 11 Campbell-S-Ar WR SpreadDocument52 pages423430-1 - 11 Campbell-S-Ar WR SpreadPrakhar SinghaniaNo ratings yet

- It's Too Early To Call The End of The Reflation TradeDocument3 pagesIt's Too Early To Call The End of The Reflation TradeJesse100% (1)

- C Fund: Common Stock Index Investment FundDocument2 pagesC Fund: Common Stock Index Investment FundAustinNo ratings yet

- Payslip 2024-02-28Document2 pagesPayslip 2024-02-28elaNo ratings yet

- Annual Report 2020Document118 pagesAnnual Report 2020Albacore EnterprisesNo ratings yet

- C1 Sampa VideoDocument2 pagesC1 Sampa VideoBharadwaja ReddyNo ratings yet

- The Late Cycle Lament The Dual Economy Minsky Moments and Other ConcernsDocument14 pagesThe Late Cycle Lament The Dual Economy Minsky Moments and Other Concernsrchawdhry123No ratings yet

- Cost-Volume-Profit Relationships: Chapter SixDocument70 pagesCost-Volume-Profit Relationships: Chapter SixFadillah AhmadNo ratings yet

- q1 2019 Earnings Website PresentationDocument17 pagesq1 2019 Earnings Website PresentationTitoNo ratings yet

- Group 1 - Chapter 20 - Audit of Other Accounts in The Statement of Profit or Loss and Comprehensive IncomeDocument18 pagesGroup 1 - Chapter 20 - Audit of Other Accounts in The Statement of Profit or Loss and Comprehensive IncomeRhad Lester C. MaestradoNo ratings yet

- 4 4 Analysis of Financial StatementsDocument41 pages4 4 Analysis of Financial StatementskartiktrivediNo ratings yet

- Long-Term Financial Planning: Fundamentals of Corporate FinanceDocument17 pagesLong-Term Financial Planning: Fundamentals of Corporate FinanceMuh BilalNo ratings yet

- ch01 2Document21 pagesch01 2Jigar PatelNo ratings yet

- Service Charges Popcorn Service ProviderDocument3 pagesService Charges Popcorn Service ProviderRajesh SharmaNo ratings yet

- Brand Valuation MethodsDocument23 pagesBrand Valuation MethodsvroommNo ratings yet

- Bci Ex (S) 00024129Document1 pageBci Ex (S) 00024129planetamundo2017No ratings yet

- FMUEDocument5 pagesFMUERushali ParmarNo ratings yet

- Chapter 2 FS and Transaction Analysis PDFDocument53 pagesChapter 2 FS and Transaction Analysis PDFleen mercadoNo ratings yet

- Practice Session - 14 - MayDocument18 pagesPractice Session - 14 - MayprabhuNo ratings yet

- Analysis of The Organizational Reorientation of The ABB GroupDocument34 pagesAnalysis of The Organizational Reorientation of The ABB GroupJayesh PatilNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- Operational Profitability: Systematic Approaches for Continuous ImprovementFrom EverandOperational Profitability: Systematic Approaches for Continuous ImprovementNo ratings yet

- Destiny Luck FengShuiDocument2 pagesDestiny Luck FengShuiWan Sek ChoonNo ratings yet

- Discovery LearningDocument12 pagesDiscovery LearningWan Sek ChoonNo ratings yet

- Neoclassical Economics: Economic Science, To DistinguishDocument35 pagesNeoclassical Economics: Economic Science, To DistinguishWan Sek ChoonNo ratings yet

- This Was The Winning Quote From Fred Dales, Microsoft Corp. in Redmond WADocument4 pagesThis Was The Winning Quote From Fred Dales, Microsoft Corp. in Redmond WAWan Sek ChoonNo ratings yet

- Dudjom RinpocheDocument8 pagesDudjom RinpocheWan Sek ChoonNo ratings yet

- Case Study Module Understanding Transport ChainDocument16 pagesCase Study Module Understanding Transport ChainWan Sek ChoonNo ratings yet

- Defect CornerDocument2 pagesDefect CornerWan Sek ChoonNo ratings yet

- Daily Cycle Weekly Cycle Monthly Cycle: ST NDDocument1 pageDaily Cycle Weekly Cycle Monthly Cycle: ST NDWan Sek ChoonNo ratings yet

- From The Attracting Genuine Abundance On-Line CourseDocument2 pagesFrom The Attracting Genuine Abundance On-Line CourseWan Sek ChoonNo ratings yet

- Model For Continuous Learning: Think 6 ResultsDocument2 pagesModel For Continuous Learning: Think 6 ResultsWan Sek ChoonNo ratings yet

- Challenges of Implementing 9001 2000Document5 pagesChallenges of Implementing 9001 2000Wan Sek ChoonNo ratings yet

- Buying A HouseDocument8 pagesBuying A HouseWan Sek ChoonNo ratings yet

- Chinese New Year Customs and TraditionsDocument21 pagesChinese New Year Customs and TraditionsWan Sek Choon100% (2)

- For The Company Blues: A Pocket Guide For LeadersDocument35 pagesFor The Company Blues: A Pocket Guide For LeadersWan Sek ChoonNo ratings yet

- Chief Learning ManagersDocument2 pagesChief Learning ManagersWan Sek ChoonNo ratings yet

- Challenges Developing Learning OrgDocument6 pagesChallenges Developing Learning OrgWan Sek ChoonNo ratings yet

- Brochure Write UpDocument1 pageBrochure Write UpWan Sek ChoonNo ratings yet

- Statement of Financial Position (Balance Sheet) Test BankDocument4 pagesStatement of Financial Position (Balance Sheet) Test BankJhazz100% (1)

- Arun LamsalDocument50 pagesArun LamsalSmith TiwariNo ratings yet

- Bank of AmericaDocument20 pagesBank of AmericaSingh Gurminder100% (2)

- Toaz - Info Far Vol 2 Chapter 22 25docx PRDocument22 pagesToaz - Info Far Vol 2 Chapter 22 25docx PRVivialyn PalimpingNo ratings yet

- Annual Report PT SieradDocument249 pagesAnnual Report PT SieradNadia IndrianiNo ratings yet

- Chapter 18: Ratio Analysis: Rohit AgarwalDocument3 pagesChapter 18: Ratio Analysis: Rohit Agarwalbcom100% (1)

- Account Titles Trial Balance Adjustment DR CR DR: Vang Management ServicesDocument9 pagesAccount Titles Trial Balance Adjustment DR CR DR: Vang Management ServicesMutia WardaniNo ratings yet

- Summer Training Report at "Financial Performance Analysis With Ratio Analysis With Reference To South Eastern Coal Fields Limited" Bilaspur (C.G.)Document35 pagesSummer Training Report at "Financial Performance Analysis With Ratio Analysis With Reference To South Eastern Coal Fields Limited" Bilaspur (C.G.)Sanskar YadavNo ratings yet

- Chapter06 TestBankDocument50 pagesChapter06 TestBankannie100% (1)

- EASEMYTRIP - Investor Presentation - 06-Feb-23Document26 pagesEASEMYTRIP - Investor Presentation - 06-Feb-23Karan GoelNo ratings yet

- DG Khan Cement Financial StatementsDocument8 pagesDG Khan Cement Financial StatementsAsad BumbiaNo ratings yet

- 1 Chapter 5 Internal Reconstruction PDFDocument22 pages1 Chapter 5 Internal Reconstruction PDFAbhiramNo ratings yet

- Fa Chapt 1-3Document63 pagesFa Chapt 1-3sushNo ratings yet

- Rajiv Talreja Workshop - 18-06-23Document88 pagesRajiv Talreja Workshop - 18-06-23Venkat KamatamNo ratings yet

- Q4-FY23/FY23: Earnings PresentationDocument17 pagesQ4-FY23/FY23: Earnings PresentationGurjeevNo ratings yet

- The Hutchinson Whampoa Case - CLASS 18, BINDING BONDS Marco PattiDocument5 pagesThe Hutchinson Whampoa Case - CLASS 18, BINDING BONDS Marco PattiMarco PattiNo ratings yet

- Makalah Paper Noun Phrase (English Economy)Document11 pagesMakalah Paper Noun Phrase (English Economy)Ines AlissaNo ratings yet

- CCPSDocument2 pagesCCPSelitevaluation2022No ratings yet

- 11Document4 pages11William LanzuelaNo ratings yet

- Ch16 Practice Quiz ProblemsDocument14 pagesCh16 Practice Quiz ProblemswarrenmertzNo ratings yet

- Compare Genp KLKDocument4 pagesCompare Genp KLKJing Sheng QuakNo ratings yet

- UniSwap (18L - (0910, 1055, 1016) )Document19 pagesUniSwap (18L - (0910, 1055, 1016) )RafayGhafoorNo ratings yet

- Answer KeyDocument52 pagesAnswer KeyDevonNo ratings yet

- Imp. A.O MCQDocument19 pagesImp. A.O MCQNadir AhmedNo ratings yet

- Jawaban Case 1 CH 8Document4 pagesJawaban Case 1 CH 8Azim JamalNo ratings yet

- Iamu Posho MillDocument37 pagesIamu Posho MillOCHIENG NICHOLASNo ratings yet

- Financial Accounting I SemesterDocument25 pagesFinancial Accounting I SemesterBhaskar KrishnappaNo ratings yet

- Afar QuestionsDocument16 pagesAfar Questionspopsie tulalianNo ratings yet