Download as docx, pdf, or txt

You might also like

- MGFC10 Cheat SheetDocument5 pagesMGFC10 Cheat SheetĐức Hải NguyễnNo ratings yet

- hw#2 PDFDocument5 pageshw#2 PDFEkta VaswaniNo ratings yet

- Whelan PharmaceuticalsDocument1 pageWhelan PharmaceuticalsHe QIu0% (1)

- Long Beach City MGM'T Memo Advising New Civic Center (P3) Instead of City Hall Seismic RetrofitDocument5 pagesLong Beach City MGM'T Memo Advising New Civic Center (P3) Instead of City Hall Seismic RetrofitAnonymous 3qqTNAAOQNo ratings yet

- Homework Problem Set 1Document2 pagesHomework Problem Set 1SaiPraneethNo ratings yet

- HW 3 Answer KeyDocument2 pagesHW 3 Answer KeyHemabhimanyu MaddineniNo ratings yet

- 5Document26 pages5Kevin HaoNo ratings yet

- 101 Session FourDocument45 pages101 Session FourVinit PatelNo ratings yet

- Toon Eneco PDFDocument4 pagesToon Eneco PDFDHEEPIKANo ratings yet

- 8 GMM Comparative Case Study Balonia and BanchuriaDocument16 pages8 GMM Comparative Case Study Balonia and BanchuriaTina WuNo ratings yet

- Chapter 7Document24 pagesChapter 7Palos DoseNo ratings yet

- Kodak Funtime - Ans2 and 3Document2 pagesKodak Funtime - Ans2 and 3Shreeraj PawarNo ratings yet

- Solution To In-Class Quiz 2Document11 pagesSolution To In-Class Quiz 2Piyush SharmaNo ratings yet

- Solution To In-Class Quiz 2Document11 pagesSolution To In-Class Quiz 2Piyush SharmaNo ratings yet

- CAPITAL BUDGETING Ultratech Cements 2015Document87 pagesCAPITAL BUDGETING Ultratech Cements 2015Nair D Sravan50% (2)

- Midterm PracticeDocument7 pagesMidterm PracticeDoshi VaibhavNo ratings yet

- Practice Questions For Mid Term 2Document3 pagesPractice Questions For Mid Term 2md1sabeel1ansariNo ratings yet

- Midterm Practice SOLUTIONSDocument7 pagesMidterm Practice SOLUTIONSDoshi VaibhavNo ratings yet

- Gyaan Kosh Term 2: Competitive StrategyDocument23 pagesGyaan Kosh Term 2: Competitive StrategySatwik PandaNo ratings yet

- Gyaan Kosh: Global EconomicsDocument19 pagesGyaan Kosh: Global EconomicsU KUNALNo ratings yet

- Sample ProblemsDocument9 pagesSample ProblemsDoshi VaibhavNo ratings yet

- Marketing Decision Making: Gyaan Kosh Term 4Document18 pagesMarketing Decision Making: Gyaan Kosh Term 4Avi JainNo ratings yet

- MadmDocument9 pagesMadmRuchika SinghNo ratings yet

- GLEC Assignment-Country Report (Spain)Document15 pagesGLEC Assignment-Country Report (Spain)Sohil AggarwalNo ratings yet

- MKDM Gyan KoshDocument17 pagesMKDM Gyan KoshSatwik PandaNo ratings yet

- Business Statistic Linear Programming ExerciseDocument3 pagesBusiness Statistic Linear Programming ExerciseSimon Gee0% (2)

- Econ7073 2021.S1Document76 pagesEcon7073 2021.S1RebacaNo ratings yet

- BE - Pre Foundation Phase - Sample PaperDocument3 pagesBE - Pre Foundation Phase - Sample PaperJaved MohammedNo ratings yet

- Chapter 20Document93 pagesChapter 20Irina AlexandraNo ratings yet

- DMOP Homework 1 Q6Document1 pageDMOP Homework 1 Q6khushi kumariNo ratings yet

- Practice QuestionsDocument4 pagesPractice QuestionsAnyone SomeoneNo ratings yet

- CFINDocument10 pagesCFINAnuj AgarwalNo ratings yet

- MGECDocument8 pagesMGECSrishtiNo ratings yet

- Capital (Less: Drawings) 4,800,000 4,700,000 455,340: Liabilities Dec 1999 Dec 2000Document10 pagesCapital (Less: Drawings) 4,800,000 4,700,000 455,340: Liabilities Dec 1999 Dec 2000Aprajita RanjanNo ratings yet

- The Firm's Approach To Pollution ControlDocument1 pageThe Firm's Approach To Pollution ControlSean Chris ConsonNo ratings yet

- Practice Questions For Tutorial Solutions 3 - 2020 - Section BDocument8 pagesPractice Questions For Tutorial Solutions 3 - 2020 - Section BtanNo ratings yet

- Scotts Miracle GroDocument10 pagesScotts Miracle GromsarojiniNo ratings yet

- Pricing Answers PDFDocument12 pagesPricing Answers PDFvineel kumarNo ratings yet

- Decision Models and Optimization: Sample-Endterm-with SolutionsDocument6 pagesDecision Models and Optimization: Sample-Endterm-with SolutionsYash NyatiNo ratings yet

- Abhishek 2 - Asset Id 1945007Document3 pagesAbhishek 2 - Asset Id 1945007Abhishek SinghNo ratings yet

- 456 - Muskan - Valbani - Homework 4Document4 pages456 - Muskan - Valbani - Homework 4Muskan ValbaniNo ratings yet

- ME Problem Set-5Document6 pagesME Problem Set-5Akash DeepNo ratings yet

- Launching of BMW Z3 RoadsterDocument15 pagesLaunching of BMW Z3 RoadsterPriyesh WankhedeNo ratings yet

- Neewee Intro Solution 2021-04-06 HCHDocument79 pagesNeewee Intro Solution 2021-04-06 HCHtelegenicsNo ratings yet

- Macro Questions 1Document9 pagesMacro Questions 1Vipul RanjanNo ratings yet

- Decision Models and Optimization: Indian School of Business Assignment 4Document8 pagesDecision Models and Optimization: Indian School of Business Assignment 4NANo ratings yet

- Set 1Document2 pagesSet 1Jephthah Bansah0% (1)

- HWDocument6 pagesHWaarushiNo ratings yet

- Analyzing Project Cash Flows: T 0 T 1 Through T 10 AssumptionsDocument46 pagesAnalyzing Project Cash Flows: T 0 T 1 Through T 10 AssumptionsHana NadhifaNo ratings yet

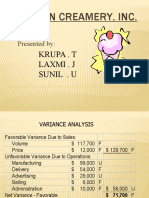

- Boston Creamery CaseDocument9 pagesBoston Creamery Caselion_heart3001100% (1)

- Ques 1. How Hard Do You Think Installing Otisline Was in 1990?Document1 pageQues 1. How Hard Do You Think Installing Otisline Was in 1990?Rashmi RanjanNo ratings yet

- Bharat Rasayan StockDocument8 pagesBharat Rasayan StockajaynkotiNo ratings yet

- ME Problem Set-IIIDocument2 pagesME Problem Set-IIIDivi KhareNo ratings yet

- GEMS TDDocument4 pagesGEMS TDMarissa BradleyNo ratings yet

- Analysis of PolysarDocument84 pagesAnalysis of PolysarParthMairNo ratings yet

- Economics 8Document20 pagesEconomics 8Carlo WidjajaNo ratings yet

- Sample Problems-DMOPDocument5 pagesSample Problems-DMOPChakri MunagalaNo ratings yet

- Colorscope IncDocument14 pagesColorscope IncShashi ShekharNo ratings yet

- Accounting For The Intel Pentium Chip Flaw - QuestionsDocument1 pageAccounting For The Intel Pentium Chip Flaw - QuestionsShaheen MalikNo ratings yet

- Managerial AccountingDocument23 pagesManagerial AccountingErum AnwerNo ratings yet

- Management Sheet 1 (Decision Making Assignment)Document6 pagesManagement Sheet 1 (Decision Making Assignment)Dalia EhabNo ratings yet

- Tutorial 5 - CHAPTER 9 - QDocument13 pagesTutorial 5 - CHAPTER 9 - QThuỳ PhạmNo ratings yet

- Module 3 SCMDocument9 pagesModule 3 SCMKhai LaNo ratings yet

- Vol - 3 - Rise of Unicorn Startups PDFDocument2 pagesVol - 3 - Rise of Unicorn Startups PDFPiyush SharmaNo ratings yet

- Air FranceDocument1 pageAir FrancePiyush SharmaNo ratings yet

- Group Assignment 3 Due by Tuesday (29) 11 PMDocument1 pageGroup Assignment 3 Due by Tuesday (29) 11 PMPiyush SharmaNo ratings yet

- Dmop CaseDocument3 pagesDmop CasePiyush SharmaNo ratings yet

- Grocery Gateway Simulated Demand DataDocument44 pagesGrocery Gateway Simulated Demand DataPiyush SharmaNo ratings yet

- Grocery GatewayDocument5 pagesGrocery GatewayPiyush SharmaNo ratings yet

- Chapter 9 Managing The Office & ReportsDocument21 pagesChapter 9 Managing The Office & ReportsAlexander ZhangNo ratings yet

- ExamplesDocument2 pagesExamplesCrina Elena AndriesNo ratings yet

- AE - Group 1 - Research PaperDocument86 pagesAE - Group 1 - Research Paperadarose romaresNo ratings yet

- TGDocument53 pagesTGEllaine Pearl AlmillaNo ratings yet

- Besanko and Braeutigam Microeconomics 4 PDFDocument33 pagesBesanko and Braeutigam Microeconomics 4 PDFSteve Schmear100% (3)

- Carlyle Towers Chronicle Dec 2016Document13 pagesCarlyle Towers Chronicle Dec 2016Lee HernlyNo ratings yet

- CFO Chief Operating Officer in Minneapolis ST Paul MN Resume William HansenDocument3 pagesCFO Chief Operating Officer in Minneapolis ST Paul MN Resume William HansenWilliamHansenNo ratings yet

- Gilbert 19 2005 FinalDocument18 pagesGilbert 19 2005 FinalBharat SavajiyaniNo ratings yet

- Planning and Budgetng.: Course: Introduction To FinancialDocument38 pagesPlanning and Budgetng.: Course: Introduction To FinancialMichaelNo ratings yet

- Sample Problems Variance Analysis PDFDocument1 pageSample Problems Variance Analysis PDFAdrian MontemayorNo ratings yet

- Nadig Press Newspaper Chicago June 19 2013 EditionDocument20 pagesNadig Press Newspaper Chicago June 19 2013 EditionchicagokenjiNo ratings yet

- Non Profit Business PlanDocument7 pagesNon Profit Business Planandre beaureau100% (1)

- Credit Suisse Hikes PHL GDPDocument5 pagesCredit Suisse Hikes PHL GDPIann CajNo ratings yet

- CH 12Document3 pagesCH 12ghsoub777No ratings yet

- The Budget StoryDocument23 pagesThe Budget Storyaira nialaNo ratings yet

- Management AccountingDocument304 pagesManagement AccountingRomi Anton100% (2)

- World Bank OBBDocument60 pagesWorld Bank OBBHanisah AbdulRahmanNo ratings yet

- AP Budget Speech EnglishDocument61 pagesAP Budget Speech EnglishRaghu Ram100% (1)

- Business Plan TheoryDocument72 pagesBusiness Plan TheoryNaishadh BhattNo ratings yet

- Monetary Policy of IndiaDocument31 pagesMonetary Policy of IndiaSopan JenaNo ratings yet

- Contractual Claims References Version 7Document301 pagesContractual Claims References Version 7SSalma70100% (13)

- OverallReport 2007 05 PDFDocument88 pagesOverallReport 2007 05 PDFJean Monique Oabel-TolentinoNo ratings yet

- 0000 - 000saudi Aramco GIDocument12 pages0000 - 000saudi Aramco GIRaheel Ahmed75% (8)

- Vidya Guru Banking NotesDocument20 pagesVidya Guru Banking NotesGaurav ShahNo ratings yet

- Customer Journey Mapping: Guide For PractitionersDocument16 pagesCustomer Journey Mapping: Guide For PractitionersAngie Castro VivancoNo ratings yet

- Bestway Cement Managerial AccountingDocument17 pagesBestway Cement Managerial AccountingArsalan RafiqueNo ratings yet

- Standard Costing MdiDocument4 pagesStandard Costing MdiAbhineet Kumar0% (1)

- The Role of Managerial Accounting in The Management ProcessDocument5 pagesThe Role of Managerial Accounting in The Management ProcessBufan Ioana-DianaNo ratings yet