Download as docx, pdf, or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5823)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (898)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (823)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- AIDOT Company Introduction EngDocument17 pagesAIDOT Company Introduction EngdaoltaNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Tugas Teknik Kuantitatif Linear Programming: DiketahuiDocument7 pagesTugas Teknik Kuantitatif Linear Programming: DiketahuiGustia AmeliaNo ratings yet

- Dokumen - Pub Sbas For The Frcstramporth Examination A Companion To Postgraduate Orthopaedics Candidates Guide 1stnbsped 1108789978 9781108789974 1108803644 9781108803649 9781108846790Document646 pagesDokumen - Pub Sbas For The Frcstramporth Examination A Companion To Postgraduate Orthopaedics Candidates Guide 1stnbsped 1108789978 9781108789974 1108803644 9781108803649 9781108846790sharan sambhwani0% (2)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Boring & Cone Penetration test-JSA-01Document3 pagesBoring & Cone Penetration test-JSA-01Akash Shukla67% (3)

- Russell 2006Document9 pagesRussell 2006a.guptaNo ratings yet

- Intergrator ManualDocument381 pagesIntergrator ManualFeri BullenkNo ratings yet

- Journal of Clinical NeuroscienceDocument5 pagesJournal of Clinical NeuroscienceNeurobites ESLNo ratings yet

- Virtual Lab Tour Format - AgsaldaDocument2 pagesVirtual Lab Tour Format - AgsaldaEj AgsaldaNo ratings yet

- Complaint. ECF (00022320)Document41 pagesComplaint. ECF (00022320)Rick KarlinNo ratings yet

- A. Won: A. Sentencing (Subject + Predicate + Object + Complement)Document7 pagesA. Won: A. Sentencing (Subject + Predicate + Object + Complement)Denny AfriliadiNo ratings yet

- Amnestic DisordersDocument15 pagesAmnestic DisordersMaicah ShaneNo ratings yet

- Ama ListDocument12 pagesAma ListSANJAY SINGHNo ratings yet

- Jamii Cover: Type of PlansDocument2 pagesJamii Cover: Type of PlansERICK ODIPONo ratings yet

- Educational Approaches For Children With AutismDocument31 pagesEducational Approaches For Children With AutismSaradha Priyadarshini100% (2)

- Asian Medical SystemsDocument12 pagesAsian Medical SystemsReggie ThorpeNo ratings yet

- Paggamot Sa Gitna NG PaggahasaDocument4 pagesPaggamot Sa Gitna NG PaggahasaOmar AculanNo ratings yet

- Establish Quality StandardsTTLMDocument15 pagesEstablish Quality StandardsTTLMwendi mesele100% (3)

- Open Letter To Minister Tell Re COVID-19 in Prisons - April 2, 2020Document4 pagesOpen Letter To Minister Tell Re COVID-19 in Prisons - April 2, 2020Thomas PillerNo ratings yet

- Endocrine Physiology / Part OneDocument46 pagesEndocrine Physiology / Part OneSherwan R Shal100% (1)

- School Form 2 (SF2) Daily Attendance Report of LearnersDocument11 pagesSchool Form 2 (SF2) Daily Attendance Report of LearnersArt DollosaNo ratings yet

- Causes of Suicide Among The Youths: April 2020Document17 pagesCauses of Suicide Among The Youths: April 2020Bhagyashree DhamaleNo ratings yet

- Bone Tissue EngineeringDocument352 pagesBone Tissue EngineeringKeri Gobin SamarooNo ratings yet

- Boatmaster's SyllabusDocument15 pagesBoatmaster's SyllabusAnonymous ycFeyuLAtNo ratings yet

- 10 Minute Workout PDFDocument20 pages10 Minute Workout PDFPianoGuyNo ratings yet

- Cover Letter - Wellington ManagementDocument1 pageCover Letter - Wellington ManagementAnas HadiNo ratings yet

- Bibliotherapy: Books As TherapyDocument33 pagesBibliotherapy: Books As TherapyNOR AZIRA BINTI AZIZ MoeNo ratings yet

- Drug Dose CalculationDocument50 pagesDrug Dose CalculationSwaraj SKNo ratings yet

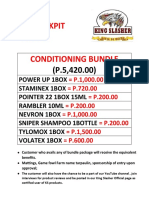

- Texas Cockpit Arena Conditioning BundleDocument4 pagesTexas Cockpit Arena Conditioning BundleHanna Sobreviñas AmanteNo ratings yet

- Laurie Ritchie, Blueprint For Learning: Constructing College Couirse To Facilitate, Assess and Document Learning Sterling VA: Stylus, 2006Document4 pagesLaurie Ritchie, Blueprint For Learning: Constructing College Couirse To Facilitate, Assess and Document Learning Sterling VA: Stylus, 2006Joel Lim Zamora0% (1)

- BENJAMIN, Harry - Better Sight Without Glasses (1962) PDFDocument115 pagesBENJAMIN, Harry - Better Sight Without Glasses (1962) PDFKhoerNo ratings yet