MB0045 - Financial Management: Q.1 Write The Short Notes On

MB0045 - Financial Management: Q.1 Write The Short Notes On

You might also like

- Taxation SituationalDocument113 pagesTaxation SituationalDaryl Mae Mansay100% (1)

- Financial ManagementDocument65 pagesFinancial Managementshekharnishu96% (27)

- Assignment FMDocument10 pagesAssignment FMHams NcomNo ratings yet

- Literature ReviewDocument16 pagesLiterature Reviewধ্রুবজ্যোতি গোস্বামীNo ratings yet

- MB 0045 Set 1Document11 pagesMB 0045 Set 1Pardeep RohillaNo ratings yet

- Sample Compre Questions Financial ManagementDocument6 pagesSample Compre Questions Financial ManagementMark KevinNo ratings yet

- MB0045 - Financial ManagementDocument36 pagesMB0045 - Financial ManagementsatishdasariNo ratings yet

- Corporate Finance Assignment: Submitted byDocument8 pagesCorporate Finance Assignment: Submitted byRidhi KumariNo ratings yet

- What Is Weighted Average Cost of CapitalDocument12 pagesWhat Is Weighted Average Cost of CapitalVïñü MNNo ratings yet

- Explain The Objectives of Financial ManagementDocument4 pagesExplain The Objectives of Financial ManagementNishi Agarwal100% (1)

- Functions of Finance ManagerDocument5 pagesFunctions of Finance ManagerB112NITESH KUMAR SAHUNo ratings yet

- Assignment:-1: Core PapersDocument32 pagesAssignment:-1: Core PapersAnamikaNo ratings yet

- 2015@FM I CH 6-Capital BudgetingDocument16 pages2015@FM I CH 6-Capital BudgetingALEMU TADESSENo ratings yet

- Subject Code - MB0045: MB0045 - Financial Management - 4 CreditsDocument10 pagesSubject Code - MB0045: MB0045 - Financial Management - 4 CreditsHolySatan696No ratings yet

- Role of A Financial ManagerDocument15 pagesRole of A Financial ManagerAadi Jain -No ratings yet

- Financial ManagementDocument33 pagesFinancial ManagementAkash k.cNo ratings yet

- Sandesh Sir: Anuj NairDocument55 pagesSandesh Sir: Anuj NairAnuj NairNo ratings yet

- Business FinanceDocument91 pagesBusiness FinanceIStienei B. EdNo ratings yet

- Busifin Chapter 1Document36 pagesBusifin Chapter 1Ronald MojadoNo ratings yet

- FIN Ass MSE 13 AprilDocument5 pagesFIN Ass MSE 13 AprilHarshit gargNo ratings yet

- Master of Business Administration-MBA Semester 2 MB0045 - Financial Management - 4 CreditsDocument17 pagesMaster of Business Administration-MBA Semester 2 MB0045 - Financial Management - 4 CreditsMaulik ParekhNo ratings yet

- Exm - 32142 Finance ManagementDocument15 pagesExm - 32142 Finance Managementkalp ach50% (2)

- ShahanDocument84 pagesShahanDhanush47No ratings yet

- A Project On Capital StructureDocument62 pagesA Project On Capital StructurejagadeeshNo ratings yet

- Unit 1 Introduction To Financial ManagementDocument12 pagesUnit 1 Introduction To Financial ManagementPRIYA KUMARINo ratings yet

- Financial ManagementDocument26 pagesFinancial ManagementbassramiNo ratings yet

- Working CapitalDocument9 pagesWorking CapitalSahil PasrijaNo ratings yet

- Lecture 1 - Nature and Scope of Financial ManagementDocument6 pagesLecture 1 - Nature and Scope of Financial ManagementAli DoyoNo ratings yet

- Finance Compendium PartI DMS IIT DelhiDocument29 pagesFinance Compendium PartI DMS IIT Delhinikhilkp9718No ratings yet

- MBA-608 (CF) DoneDocument10 pagesMBA-608 (CF) DonekushNo ratings yet

- Meaning of Financial ManagementDocument6 pagesMeaning of Financial ManagementMar JinitaNo ratings yet

- Finance Assignment 1Document10 pagesFinance Assignment 1khushbu mohanNo ratings yet

- Working Capital Management, Its Importance and Implication On ProfitabilityDocument49 pagesWorking Capital Management, Its Importance and Implication On ProfitabilitySesco WemNo ratings yet

- Introduction To The Financial Management: Thursday, May 3, 2007Document8 pagesIntroduction To The Financial Management: Thursday, May 3, 2007Praveen KumarNo ratings yet

- Chapter 1 Scope and Objectives of Financial Management 2Document19 pagesChapter 1 Scope and Objectives of Financial Management 2Pandit Niraj Dilip SharmaNo ratings yet

- MB0045 - Mba 2 SemDocument19 pagesMB0045 - Mba 2 SemacorneleoNo ratings yet

- Topic OneDocument15 pagesTopic OnechelseaNo ratings yet

- FM1.1 IntroductionDocument4 pagesFM1.1 IntroductionnehaasinghhNo ratings yet

- Corporate FinanceDocument7 pagesCorporate FinanceShafqat HossainNo ratings yet

- Financial Management B-Part 5th SEMDocument44 pagesFinancial Management B-Part 5th SEMarunpradeep795No ratings yet

- FM Reading MaterialDocument12 pagesFM Reading MaterialTaransh ANo ratings yet

- Working Capital: Concepts of Working Capital Gross Working Capital (GWC)Document37 pagesWorking Capital: Concepts of Working Capital Gross Working Capital (GWC)Manisha SharmaNo ratings yet

- Bba FM Notes Unit IDocument15 pagesBba FM Notes Unit Iyashasvigupta.thesironaNo ratings yet

- MFDocument6 pagesMFJS Gowri NandiniNo ratings yet

- Module 1Document19 pagesModule 1Vasudha SrivatsaNo ratings yet

- Functions of Financial ManagementDocument5 pagesFunctions of Financial ManagementAthar KhanNo ratings yet

- ACCN09B Strategic Cost Management 1: For Use As Instructional Materials OnlyDocument3 pagesACCN09B Strategic Cost Management 1: For Use As Instructional Materials OnlyAdrienne Nicole MercadoNo ratings yet

- Functions/Objectives of Financial ManagementDocument7 pagesFunctions/Objectives of Financial ManagementRahul WaniNo ratings yet

- Financial ManagementDocument14 pagesFinancial ManagementMru SurveNo ratings yet

- Financial Management KangraDocument12 pagesFinancial Management Kangramanik_chand_patnaikNo ratings yet

- Scope and Objectives of Financial ManagementDocument20 pagesScope and Objectives of Financial ManagementAnkur Aggarwal100% (1)

- Financial Management Economics For Finance 1679035282Document135 pagesFinancial Management Economics For Finance 1679035282Alaka BelkudeNo ratings yet

- Mb0045 Financial ManagementDocument242 pagesMb0045 Financial ManagementAnkit ChawlaNo ratings yet

- Business Opportunity Thinking: Building a Sustainable, Diversified BusinessFrom EverandBusiness Opportunity Thinking: Building a Sustainable, Diversified BusinessNo ratings yet

- Analytical Corporate Valuation: Fundamental Analysis, Asset Pricing, and Company ValuationFrom EverandAnalytical Corporate Valuation: Fundamental Analysis, Asset Pricing, and Company ValuationNo ratings yet

- Dividend Investing: Passive Income and Growth Investing for BeginnersFrom EverandDividend Investing: Passive Income and Growth Investing for BeginnersNo ratings yet

- Report 1-3 - Nabil BankDocument33 pagesReport 1-3 - Nabil BankSalım RaıŋNo ratings yet

- IMF Lending: When Can A Country Borrow From The IMF?Document5 pagesIMF Lending: When Can A Country Borrow From The IMF?Ram KumarNo ratings yet

- 05 Task Performance 1-BADocument3 pages05 Task Performance 1-BATyron Franz AnoricoNo ratings yet

- Pas 40 Concept MapDocument1 pagePas 40 Concept MapJohn Steve VasalloNo ratings yet

- Operating Budget DiscussionDocument3 pagesOperating Budget DiscussionDavin DavinNo ratings yet

- KELOMPOK 5 (CHAPTER 17) RevDocument40 pagesKELOMPOK 5 (CHAPTER 17) Revnandya rizkyNo ratings yet

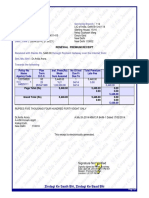

- Renewal Premium Receipt: Collecting Branch: E-Mail: Phone: Transaction No.: Date (Time) : Servicing BranchDocument1 pageRenewal Premium Receipt: Collecting Branch: E-Mail: Phone: Transaction No.: Date (Time) : Servicing BranchAnirudh AroraNo ratings yet

- Optimal Capital StructureDocument13 pagesOptimal Capital StructureScarlet SalongaNo ratings yet

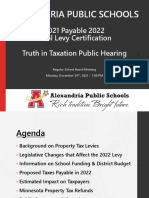

- Alexandria Public Schools Tax LevyDocument74 pagesAlexandria Public Schools Tax LevyinforumdocsNo ratings yet

- PRTC-FINAL PB - Answer Key 10.21 PDFDocument38 pagesPRTC-FINAL PB - Answer Key 10.21 PDFLuna VNo ratings yet

- Form PDF 197504840210823Document9 pagesForm PDF 197504840210823jassramgarhia2812No ratings yet

- Tax Card For Tax Year 2019Document1 pageTax Card For Tax Year 2019Kinglovefriend100% (1)

- Nidhi Patni: ORK Xperience Senior Risk Analyst Aug 2020 - PresentDocument1 pageNidhi Patni: ORK Xperience Senior Risk Analyst Aug 2020 - PresentNidhiPatniNo ratings yet

- BPI Family Savings V AvenidoDocument10 pagesBPI Family Savings V AvenidoBrian TomasNo ratings yet

- IND As 104Document33 pagesIND As 104shalu salamNo ratings yet

- Bank Final AccountDocument11 pagesBank Final AccountKadam KartikeshNo ratings yet

- Bac MQ2 1Document3 pagesBac MQ2 1JESSON VILLANo ratings yet

- Annual ReporDocument177 pagesAnnual ReporShakir EbrahimiNo ratings yet

- Questions With AnswersDocument8 pagesQuestions With AnswersAwadhesh SinghNo ratings yet

- Fundamentals of Accountancy, Business and Management 1: Teddy B. GanDocument25 pagesFundamentals of Accountancy, Business and Management 1: Teddy B. GanWindelyn IliganNo ratings yet

- COMFAR III Reference ManualDocument412 pagesCOMFAR III Reference Manualstarx95100% (1)

- CRM RBCDocument14 pagesCRM RBCKarthik ArumughamNo ratings yet

- Hyperinflation in Germany, 1914-1923: (This Article Is Excerpted From The Book .)Document10 pagesHyperinflation in Germany, 1914-1923: (This Article Is Excerpted From The Book .)hipsterzNo ratings yet

- Report of Investigation: Burns Philp and Co LTDDocument41 pagesReport of Investigation: Burns Philp and Co LTDa_bleem_userNo ratings yet

- Merger and AccutionDocument3 pagesMerger and Accutionankit6233No ratings yet

- Audit Prob InvestmentDocument5 pagesAudit Prob InvestmentANGIE BERNAL100% (1)

- Municipality of Guipos: Republic of The Philippines Province of Zamboanga de SurDocument21 pagesMunicipality of Guipos: Republic of The Philippines Province of Zamboanga de SurMelvinson Loui Polenzo SarcaugaNo ratings yet

- SyllabusDocument2 pagesSyllabusS SivakamiNo ratings yet

- Cost Production Ethyl AcetateDocument14 pagesCost Production Ethyl Acetateshalmiaida50% (2)

Download as docx, pdf, or txt

You might also like

- Taxation SituationalDocument113 pagesTaxation SituationalDaryl Mae Mansay100% (1)

- Financial ManagementDocument65 pagesFinancial Managementshekharnishu96% (27)

- Assignment FMDocument10 pagesAssignment FMHams NcomNo ratings yet

- Literature ReviewDocument16 pagesLiterature Reviewধ্রুবজ্যোতি গোস্বামীNo ratings yet

- MB 0045 Set 1Document11 pagesMB 0045 Set 1Pardeep RohillaNo ratings yet

- Sample Compre Questions Financial ManagementDocument6 pagesSample Compre Questions Financial ManagementMark KevinNo ratings yet

- MB0045 - Financial ManagementDocument36 pagesMB0045 - Financial ManagementsatishdasariNo ratings yet

- Corporate Finance Assignment: Submitted byDocument8 pagesCorporate Finance Assignment: Submitted byRidhi KumariNo ratings yet

- What Is Weighted Average Cost of CapitalDocument12 pagesWhat Is Weighted Average Cost of CapitalVïñü MNNo ratings yet

- Explain The Objectives of Financial ManagementDocument4 pagesExplain The Objectives of Financial ManagementNishi Agarwal100% (1)

- Functions of Finance ManagerDocument5 pagesFunctions of Finance ManagerB112NITESH KUMAR SAHUNo ratings yet

- Assignment:-1: Core PapersDocument32 pagesAssignment:-1: Core PapersAnamikaNo ratings yet

- 2015@FM I CH 6-Capital BudgetingDocument16 pages2015@FM I CH 6-Capital BudgetingALEMU TADESSENo ratings yet

- Subject Code - MB0045: MB0045 - Financial Management - 4 CreditsDocument10 pagesSubject Code - MB0045: MB0045 - Financial Management - 4 CreditsHolySatan696No ratings yet

- Role of A Financial ManagerDocument15 pagesRole of A Financial ManagerAadi Jain -No ratings yet

- Financial ManagementDocument33 pagesFinancial ManagementAkash k.cNo ratings yet

- Sandesh Sir: Anuj NairDocument55 pagesSandesh Sir: Anuj NairAnuj NairNo ratings yet

- Business FinanceDocument91 pagesBusiness FinanceIStienei B. EdNo ratings yet

- Busifin Chapter 1Document36 pagesBusifin Chapter 1Ronald MojadoNo ratings yet

- FIN Ass MSE 13 AprilDocument5 pagesFIN Ass MSE 13 AprilHarshit gargNo ratings yet

- Master of Business Administration-MBA Semester 2 MB0045 - Financial Management - 4 CreditsDocument17 pagesMaster of Business Administration-MBA Semester 2 MB0045 - Financial Management - 4 CreditsMaulik ParekhNo ratings yet

- Exm - 32142 Finance ManagementDocument15 pagesExm - 32142 Finance Managementkalp ach50% (2)

- ShahanDocument84 pagesShahanDhanush47No ratings yet

- A Project On Capital StructureDocument62 pagesA Project On Capital StructurejagadeeshNo ratings yet

- Unit 1 Introduction To Financial ManagementDocument12 pagesUnit 1 Introduction To Financial ManagementPRIYA KUMARINo ratings yet

- Financial ManagementDocument26 pagesFinancial ManagementbassramiNo ratings yet

- Working CapitalDocument9 pagesWorking CapitalSahil PasrijaNo ratings yet

- Lecture 1 - Nature and Scope of Financial ManagementDocument6 pagesLecture 1 - Nature and Scope of Financial ManagementAli DoyoNo ratings yet

- Finance Compendium PartI DMS IIT DelhiDocument29 pagesFinance Compendium PartI DMS IIT Delhinikhilkp9718No ratings yet

- MBA-608 (CF) DoneDocument10 pagesMBA-608 (CF) DonekushNo ratings yet

- Meaning of Financial ManagementDocument6 pagesMeaning of Financial ManagementMar JinitaNo ratings yet

- Finance Assignment 1Document10 pagesFinance Assignment 1khushbu mohanNo ratings yet

- Working Capital Management, Its Importance and Implication On ProfitabilityDocument49 pagesWorking Capital Management, Its Importance and Implication On ProfitabilitySesco WemNo ratings yet

- Introduction To The Financial Management: Thursday, May 3, 2007Document8 pagesIntroduction To The Financial Management: Thursday, May 3, 2007Praveen KumarNo ratings yet

- Chapter 1 Scope and Objectives of Financial Management 2Document19 pagesChapter 1 Scope and Objectives of Financial Management 2Pandit Niraj Dilip SharmaNo ratings yet

- MB0045 - Mba 2 SemDocument19 pagesMB0045 - Mba 2 SemacorneleoNo ratings yet

- Topic OneDocument15 pagesTopic OnechelseaNo ratings yet

- FM1.1 IntroductionDocument4 pagesFM1.1 IntroductionnehaasinghhNo ratings yet

- Corporate FinanceDocument7 pagesCorporate FinanceShafqat HossainNo ratings yet

- Financial Management B-Part 5th SEMDocument44 pagesFinancial Management B-Part 5th SEMarunpradeep795No ratings yet

- FM Reading MaterialDocument12 pagesFM Reading MaterialTaransh ANo ratings yet

- Working Capital: Concepts of Working Capital Gross Working Capital (GWC)Document37 pagesWorking Capital: Concepts of Working Capital Gross Working Capital (GWC)Manisha SharmaNo ratings yet

- Bba FM Notes Unit IDocument15 pagesBba FM Notes Unit Iyashasvigupta.thesironaNo ratings yet

- MFDocument6 pagesMFJS Gowri NandiniNo ratings yet

- Module 1Document19 pagesModule 1Vasudha SrivatsaNo ratings yet

- Functions of Financial ManagementDocument5 pagesFunctions of Financial ManagementAthar KhanNo ratings yet

- ACCN09B Strategic Cost Management 1: For Use As Instructional Materials OnlyDocument3 pagesACCN09B Strategic Cost Management 1: For Use As Instructional Materials OnlyAdrienne Nicole MercadoNo ratings yet

- Functions/Objectives of Financial ManagementDocument7 pagesFunctions/Objectives of Financial ManagementRahul WaniNo ratings yet

- Financial ManagementDocument14 pagesFinancial ManagementMru SurveNo ratings yet

- Financial Management KangraDocument12 pagesFinancial Management Kangramanik_chand_patnaikNo ratings yet

- Scope and Objectives of Financial ManagementDocument20 pagesScope and Objectives of Financial ManagementAnkur Aggarwal100% (1)

- Financial Management Economics For Finance 1679035282Document135 pagesFinancial Management Economics For Finance 1679035282Alaka BelkudeNo ratings yet

- Mb0045 Financial ManagementDocument242 pagesMb0045 Financial ManagementAnkit ChawlaNo ratings yet

- Business Opportunity Thinking: Building a Sustainable, Diversified BusinessFrom EverandBusiness Opportunity Thinking: Building a Sustainable, Diversified BusinessNo ratings yet

- Analytical Corporate Valuation: Fundamental Analysis, Asset Pricing, and Company ValuationFrom EverandAnalytical Corporate Valuation: Fundamental Analysis, Asset Pricing, and Company ValuationNo ratings yet

- Dividend Investing: Passive Income and Growth Investing for BeginnersFrom EverandDividend Investing: Passive Income and Growth Investing for BeginnersNo ratings yet

- Report 1-3 - Nabil BankDocument33 pagesReport 1-3 - Nabil BankSalım RaıŋNo ratings yet

- IMF Lending: When Can A Country Borrow From The IMF?Document5 pagesIMF Lending: When Can A Country Borrow From The IMF?Ram KumarNo ratings yet

- 05 Task Performance 1-BADocument3 pages05 Task Performance 1-BATyron Franz AnoricoNo ratings yet

- Pas 40 Concept MapDocument1 pagePas 40 Concept MapJohn Steve VasalloNo ratings yet

- Operating Budget DiscussionDocument3 pagesOperating Budget DiscussionDavin DavinNo ratings yet

- KELOMPOK 5 (CHAPTER 17) RevDocument40 pagesKELOMPOK 5 (CHAPTER 17) Revnandya rizkyNo ratings yet

- Renewal Premium Receipt: Collecting Branch: E-Mail: Phone: Transaction No.: Date (Time) : Servicing BranchDocument1 pageRenewal Premium Receipt: Collecting Branch: E-Mail: Phone: Transaction No.: Date (Time) : Servicing BranchAnirudh AroraNo ratings yet

- Optimal Capital StructureDocument13 pagesOptimal Capital StructureScarlet SalongaNo ratings yet

- Alexandria Public Schools Tax LevyDocument74 pagesAlexandria Public Schools Tax LevyinforumdocsNo ratings yet

- PRTC-FINAL PB - Answer Key 10.21 PDFDocument38 pagesPRTC-FINAL PB - Answer Key 10.21 PDFLuna VNo ratings yet

- Form PDF 197504840210823Document9 pagesForm PDF 197504840210823jassramgarhia2812No ratings yet

- Tax Card For Tax Year 2019Document1 pageTax Card For Tax Year 2019Kinglovefriend100% (1)

- Nidhi Patni: ORK Xperience Senior Risk Analyst Aug 2020 - PresentDocument1 pageNidhi Patni: ORK Xperience Senior Risk Analyst Aug 2020 - PresentNidhiPatniNo ratings yet

- BPI Family Savings V AvenidoDocument10 pagesBPI Family Savings V AvenidoBrian TomasNo ratings yet

- IND As 104Document33 pagesIND As 104shalu salamNo ratings yet

- Bank Final AccountDocument11 pagesBank Final AccountKadam KartikeshNo ratings yet

- Bac MQ2 1Document3 pagesBac MQ2 1JESSON VILLANo ratings yet

- Annual ReporDocument177 pagesAnnual ReporShakir EbrahimiNo ratings yet

- Questions With AnswersDocument8 pagesQuestions With AnswersAwadhesh SinghNo ratings yet

- Fundamentals of Accountancy, Business and Management 1: Teddy B. GanDocument25 pagesFundamentals of Accountancy, Business and Management 1: Teddy B. GanWindelyn IliganNo ratings yet

- COMFAR III Reference ManualDocument412 pagesCOMFAR III Reference Manualstarx95100% (1)

- CRM RBCDocument14 pagesCRM RBCKarthik ArumughamNo ratings yet

- Hyperinflation in Germany, 1914-1923: (This Article Is Excerpted From The Book .)Document10 pagesHyperinflation in Germany, 1914-1923: (This Article Is Excerpted From The Book .)hipsterzNo ratings yet

- Report of Investigation: Burns Philp and Co LTDDocument41 pagesReport of Investigation: Burns Philp and Co LTDa_bleem_userNo ratings yet

- Merger and AccutionDocument3 pagesMerger and Accutionankit6233No ratings yet

- Audit Prob InvestmentDocument5 pagesAudit Prob InvestmentANGIE BERNAL100% (1)

- Municipality of Guipos: Republic of The Philippines Province of Zamboanga de SurDocument21 pagesMunicipality of Guipos: Republic of The Philippines Province of Zamboanga de SurMelvinson Loui Polenzo SarcaugaNo ratings yet

- SyllabusDocument2 pagesSyllabusS SivakamiNo ratings yet

- Cost Production Ethyl AcetateDocument14 pagesCost Production Ethyl Acetateshalmiaida50% (2)