Download as docx, pdf, or txt

You might also like

- Articles of Incorporation and By-Laws of Religious FoundationDocument8 pagesArticles of Incorporation and By-Laws of Religious FoundationLenlen Nebria Castro100% (2)

- Paper Writeup - Honest TeaDocument2 pagesPaper Writeup - Honest Teakamalesh12340% (1)

- Class Notes Business Entities, The ChoicesDocument10 pagesClass Notes Business Entities, The ChoicesLydia.m. Asaba100% (1)

- List of Accredited Tourism Enterprises - NCRDocument3 pagesList of Accredited Tourism Enterprises - NCRRonald50% (2)

- TDS On Salaries - Income Tax Department, INDIADocument112 pagesTDS On Salaries - Income Tax Department, INDIAArnav MendirattaNo ratings yet

- All About Tax Deducted at Source (TDS) - Taxguru - inDocument11 pagesAll About Tax Deducted at Source (TDS) - Taxguru - inwaqtkeebaatein12No ratings yet

- BASICS OF TAXATION (Income Tax Ordinance, 1984) Updated Till Finance Act. 2013 by Prof. Mahbubur RahmanDocument14 pagesBASICS OF TAXATION (Income Tax Ordinance, 1984) Updated Till Finance Act. 2013 by Prof. Mahbubur RahmansaadmansheedyNo ratings yet

- TDS ElaboratedDocument80 pagesTDS ElaboratedAncyNo ratings yet

- Overview of TDS: by C.A. Manish JathliyaDocument21 pagesOverview of TDS: by C.A. Manish JathliyaHasan Babu KothaNo ratings yet

- Tds Law and Practice: Under Income Tax Act, 1961Document84 pagesTds Law and Practice: Under Income Tax Act, 1961Vaibhav ChauhanNo ratings yet

- TDS On SalariesDocument112 pagesTDS On Salariesbaalaji05No ratings yet

- Finance Act 1991Document6 pagesFinance Act 1991Govardhan VaranasiNo ratings yet

- The Rigours of TDS - An OverviewDocument31 pagesThe Rigours of TDS - An OverviewShaleenPatniNo ratings yet

- All About New TDS Section 194R and Section 194S - Taxguru - inDocument7 pagesAll About New TDS Section 194R and Section 194S - Taxguru - inParag Jain DugarNo ratings yet

- Chapter 12 Tds & TcsDocument28 pagesChapter 12 Tds & TcsRajNo ratings yet

- Introduction To TDS:-: Tax Deducted at SourceDocument3 pagesIntroduction To TDS:-: Tax Deducted at Sourcepadmanabha14No ratings yet

- TDS Under Sec 194A EtcDocument26 pagesTDS Under Sec 194A EtcDivyaNo ratings yet

- Tax Deduction at SourceDocument4 pagesTax Deduction at SourcevishalsidankarNo ratings yet

- Adjudication - Case (1) .Docx 1Document14 pagesAdjudication - Case (1) .Docx 1aliciag4342No ratings yet

- New Section 194Q Applicable From 1.7.2021Document14 pagesNew Section 194Q Applicable From 1.7.2021ramanmaharishiNo ratings yet

- TDS, TCS & Advance Payment of TaxDocument54 pagesTDS, TCS & Advance Payment of TaxFalak GoyalNo ratings yet

- TDS Under Sec 194A EtcDocument25 pagesTDS Under Sec 194A EtcGmd NizamNo ratings yet

- Section 192 Relatin Gto TDS On Salary - Section 192 Says That Every Person Who Is Responsible For Paying Any Income Chargeable Under The HeadDocument46 pagesSection 192 Relatin Gto TDS On Salary - Section 192 Says That Every Person Who Is Responsible For Paying Any Income Chargeable Under The HeadAtul SharmaNo ratings yet

- 195 Paper With PhotoDocument29 pages195 Paper With Photogrover_deepak18No ratings yet

- All About TDS Part 2Document9 pagesAll About TDS Part 2Animesh Kumar TilakNo ratings yet

- Delloite CIT (A) PDFDocument7 pagesDelloite CIT (A) PDFshashi vermaNo ratings yet

- TDS Under Section 194C: Press Releases Blog PostsDocument4 pagesTDS Under Section 194C: Press Releases Blog PostsBalu Mahendra SusarlaNo ratings yet

- Tax Deducted at Source IMPORTANT POINTSDocument2 pagesTax Deducted at Source IMPORTANT POINTSnABSAMNNo ratings yet

- Tax-Free Exchanges That Are Not Subject To Income Tax, Capital Gains Tax, Documentary Stamp Tax And/or Value-Added Tax, As The Case May BeDocument7 pagesTax-Free Exchanges That Are Not Subject To Income Tax, Capital Gains Tax, Documentary Stamp Tax And/or Value-Added Tax, As The Case May BeJouhara ObeñitaNo ratings yet

- TDS Presentation - Ca Zalak Parikh - 14.05.2022Document22 pagesTDS Presentation - Ca Zalak Parikh - 14.05.2022zalak jintanwalaNo ratings yet

- Corporate Tax PlanningDocument8 pagesCorporate Tax PlanningTumie Lets0% (1)

- Bar On Direct Demand Against Deductee - Jus in Re Bar On Direct Demand Against Deductee - Jus in ReDocument3 pagesBar On Direct Demand Against Deductee - Jus in Re Bar On Direct Demand Against Deductee - Jus in Reabc defNo ratings yet

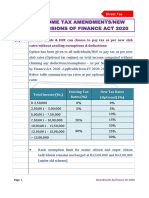

- Income Tax Amendments/New Provisions of Finance Act 2020Document46 pagesIncome Tax Amendments/New Provisions of Finance Act 2020shubhamworkNo ratings yet

- Tds Amendements Via Finance Bill 2020Document12 pagesTds Amendements Via Finance Bill 2020ABHISHEKNo ratings yet

- Direct Tax Proposals 2019 (No. 2) - 1Document16 pagesDirect Tax Proposals 2019 (No. 2) - 1Namita Agarwal KediaNo ratings yet

- Tax Deducted at Source - I: KPPM & AssociatesDocument63 pagesTax Deducted at Source - I: KPPM & AssociatesSaksham JoshiNo ratings yet

- Module 1 E - Filing of ReturnsDocument8 pagesModule 1 E - Filing of Returnsshivani singhNo ratings yet

- Circular No. 285 Dated 21-10-1980Document1 pageCircular No. 285 Dated 21-10-1980Sayan MajumdarNo ratings yet

- Deduction, Collection & Recovery of TaxesDocument143 pagesDeduction, Collection & Recovery of TaxesjyotiNo ratings yet

- QUESTION: I Own A Commercial Building Giving Me A Rent of Rs. 4 Lakhs A Month. TheDocument3 pagesQUESTION: I Own A Commercial Building Giving Me A Rent of Rs. 4 Lakhs A Month. TheCma Saurabh AroraNo ratings yet

- Section 195 and Form 15CBDocument53 pagesSection 195 and Form 15CBVALTIM09No ratings yet

- Naya' Form 3Cd: 1. Non-Compliance With Provisions of Tax Deduction at Source (Clause 27) : Delays andDocument6 pagesNaya' Form 3Cd: 1. Non-Compliance With Provisions of Tax Deduction at Source (Clause 27) : Delays andrakeshca1No ratings yet

- What Is IncomeDocument6 pagesWhat Is Incomenaman guptaNo ratings yet

- Decoding Indian Union BudgetDocument6 pagesDecoding Indian Union BudgetkumarNo ratings yet

- Non Resident Tax Withholding Section 195: CA Kapil Goel FCA LLB Advocate Delhi High Court 9910272806Document71 pagesNon Resident Tax Withholding Section 195: CA Kapil Goel FCA LLB Advocate Delhi High Court 9910272806HemanthKumarNo ratings yet

- TaxationDocument9 pagesTaxationRohit SoniNo ratings yet

- TDS On Real Estate IndustryDocument5 pagesTDS On Real Estate IndustryKirti SanghaviNo ratings yet

- Section 139Document7 pagesSection 139dhanishta906No ratings yet

- Section 194J: Fees For Professional or Technical ServicesDocument24 pagesSection 194J: Fees For Professional or Technical ServicesSAURABH TIBREWALNo ratings yet

- Tax Deducted at SourceDocument20 pagesTax Deducted at Sourceaditisrivastava0511No ratings yet

- Recent Amendments in TDS Under Income Tax - TVM BR CPE 03.09.2022Document64 pagesRecent Amendments in TDS Under Income Tax - TVM BR CPE 03.09.2022sushant980No ratings yet

- TAX Definition - : Tax Is A Compulsory Contribution Imposed by The Government On ItsDocument22 pagesTAX Definition - : Tax Is A Compulsory Contribution Imposed by The Government On ItsSayanm MittalNo ratings yet

- Deferred Tax-Accounting Standard-22-Accounting For Taxes On IncomeDocument6 pagesDeferred Tax-Accounting Standard-22-Accounting For Taxes On IncomerlpolyfabsmaheshNo ratings yet

- Advance Learning On TDS Under Section 194-I and 194-C: MeaningDocument52 pagesAdvance Learning On TDS Under Section 194-I and 194-C: MeaningTejTejuNo ratings yet

- TDS Under Section 194R – Brief Analysis - Taxguru - inDocument4 pagesTDS Under Section 194R – Brief Analysis - Taxguru - inAbhishek GuptaNo ratings yet

- Latest Circulars, Notifications and Press Releases: 2. This Notification Shall Come Into Force From The 1Document0 pagesLatest Circulars, Notifications and Press Releases: 2. This Notification Shall Come Into Force From The 1Ketan ThakkarNo ratings yet

- TDS - TCSDocument55 pagesTDS - TCSBeing HumaneNo ratings yet

- TAX 2 Group 1 Handout PDFDocument6 pagesTAX 2 Group 1 Handout PDFMi-young SunNo ratings yet

- CA-Ashok-Mehta - PPT - Income TaxDocument88 pagesCA-Ashok-Mehta - PPT - Income TaxAbinash DasNo ratings yet

- S 206C (1H) – Updated - Taxguru - inDocument11 pagesS 206C (1H) – Updated - Taxguru - inHEMANT PARMARNo ratings yet

- 1040 Exam Prep: Module I: The Form 1040 FormulaFrom Everand1040 Exam Prep: Module I: The Form 1040 FormulaRating: 1 out of 5 stars1/5 (3)

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- Naresh Chandra Commitee 2002 - Presentation To Be Taken For Class Seminar.Document26 pagesNaresh Chandra Commitee 2002 - Presentation To Be Taken For Class Seminar.sambhu_nNo ratings yet

- CSR Project @@@Document54 pagesCSR Project @@@Harry GaikwadNo ratings yet

- CENGAGE LearningDocument27 pagesCENGAGE LearningAnthony Moreno RodríguezNo ratings yet

- Reflection PaperDocument2 pagesReflection PaperAnamaria BucilăNo ratings yet

- 3005 150024159 00 000 PDFDocument3 pages3005 150024159 00 000 PDFDeepak MeenaNo ratings yet

- Dettol Launches Ad War Against VimDocument2 pagesDettol Launches Ad War Against VimHARRYROX91No ratings yet

- JPIA PLV Directory 1st Sem AY 18 19 BSA 1 4Document5 pagesJPIA PLV Directory 1st Sem AY 18 19 BSA 1 4Shin NizeNo ratings yet

- Commentary Power Words TemplateDocument12 pagesCommentary Power Words TemplateJohn Johnstone100% (1)

- Les CopaqueDocument13 pagesLes CopaqueMakcik HananNo ratings yet

- Akuntansi ManajemenDocument68 pagesAkuntansi ManajemeninspekturaNo ratings yet

- Reviewer ParcorpDocument2 pagesReviewer ParcorpLyka TejadaNo ratings yet

- List of Employment Agencies Under Surveillance - Singapore Job AgencyDocument5 pagesList of Employment Agencies Under Surveillance - Singapore Job Agencyyuly120% (1)

- Working Capital AnalysisDocument20 pagesWorking Capital Analysisaneek100% (1)

- Investment Banking NoteDocument6 pagesInvestment Banking NoteShwetank RaiNo ratings yet

- Introduction of TrustDocument19 pagesIntroduction of TrustNajmul HasanNo ratings yet

- CSR Articles & Reports - March 2018Document9 pagesCSR Articles & Reports - March 2018Celeste MonfortonNo ratings yet

- GoldFields Recruitment Scam DisclaimerDocument1 pageGoldFields Recruitment Scam DisclaimerNewsWire GHNo ratings yet

- White Flint Sector Plan Implementation Advisory CommitteeDocument3 pagesWhite Flint Sector Plan Implementation Advisory CommitteeM-NCPPCNo ratings yet

- Principle and Practice of TaxationDocument5 pagesPrinciple and Practice of TaxationAgyeiNo ratings yet

- Answer: D: Statement 2: The Share of A Co-Venturer Corporation in The Net Income of Tax Exempt Joint Venture orDocument3 pagesAnswer: D: Statement 2: The Share of A Co-Venturer Corporation in The Net Income of Tax Exempt Joint Venture orRosemarie CruzNo ratings yet

- AFAR Study Plan PDFDocument4 pagesAFAR Study Plan PDFMichelleOgatisNo ratings yet

- SriLankan Airlines Annual Report 2014-15 English PDFDocument84 pagesSriLankan Airlines Annual Report 2014-15 English PDFChandu De SilvaNo ratings yet

- CK2500-2F CKE2500-2F (Circuit Chart Collection)Document44 pagesCK2500-2F CKE2500-2F (Circuit Chart Collection)Nishant Sinha100% (1)

- Financial Analyst Accountant in Tallahassee FL Resume Andrew HornickDocument3 pagesFinancial Analyst Accountant in Tallahassee FL Resume Andrew HornickAndrewHornickNo ratings yet

- MFG Data MumbaiDocument34 pagesMFG Data MumbaiAnurag BhimrajkaNo ratings yet

- BankDocument47 pagesBankChaitali DegavkarNo ratings yet