Download as docx, pdf, or txt

You might also like

- Amazon Stock RSU Global Agreement PDFDocument27 pagesAmazon Stock RSU Global Agreement PDFlindytindylindtNo ratings yet

- Chapter 4 ExerciseDocument7 pagesChapter 4 ExerciseJoe DicksonNo ratings yet

- Practice Ques - Incremental Analysis PDFDocument8 pagesPractice Ques - Incremental Analysis PDFDaksh AnejaNo ratings yet

- Date: Monday 19/5/2015: Strategic Management Year 2015 Final ExamDocument6 pagesDate: Monday 19/5/2015: Strategic Management Year 2015 Final ExamNehal NabilNo ratings yet

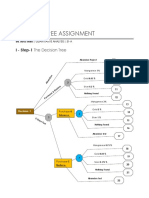

- Decision Tree Assignment QADocument5 pagesDecision Tree Assignment QANehal NabilNo ratings yet

- Chapter1-Carter Cleaning Centers PDFDocument4 pagesChapter1-Carter Cleaning Centers PDFNehal NabilNo ratings yet

- Earn Hart Corporation Has Outstanding 3 000 000 Shares of Common PDFDocument1 pageEarn Hart Corporation Has Outstanding 3 000 000 Shares of Common PDFAnbu jaromiaNo ratings yet

- AccountingDocument12 pagesAccountingpearl042008No ratings yet

- Quiz 3 Version BDocument2 pagesQuiz 3 Version BMishal KhalidNo ratings yet

- Question and Answer - 8Document30 pagesQuestion and Answer - 8acc-expertNo ratings yet

- Soal Asis Pert 2 - Jordy - PA1Document1 pageSoal Asis Pert 2 - Jordy - PA1Jordy TangNo ratings yet

- w9 - L2 - Review For Lecture Midterm 2Document14 pagesw9 - L2 - Review For Lecture Midterm 2Rashid AyubiNo ratings yet

- CH 4 Classpack With SolutionsDocument24 pagesCH 4 Classpack With SolutionsjimenaNo ratings yet

- 2011 Aug Tutorial 10 Working Capital ManagementDocument10 pages2011 Aug Tutorial 10 Working Capital ManagementHarmony TeeNo ratings yet

- Chapter 06 (Part II) - AssignmentDocument4 pagesChapter 06 (Part II) - AssignmentRawan YasserNo ratings yet

- Kelompok E-Akuntansi Manajemen-Module 7Document11 pagesKelompok E-Akuntansi Manajemen-Module 7vidiamyNo ratings yet

- Chapter 6 - Anchoring BiasDocument18 pagesChapter 6 - Anchoring BiasNehal NabilNo ratings yet

- 10 Cases Accounting - Answered-1 PDFDocument10 pages10 Cases Accounting - Answered-1 PDFNehal NabilNo ratings yet

- Real Estate Ventures I 2013 Course SyllabusDocument8 pagesReal Estate Ventures I 2013 Course SyllabusRajesh JadhavNo ratings yet

- Index of /training: The - C - Programming - Language - PDF Understandingthelinuxkernel3Rdedition PDFDocument2 pagesIndex of /training: The - C - Programming - Language - PDF Understandingthelinuxkernel3Rdedition PDFDavidXimenesNo ratings yet

- Accounting Chapter 10 Solutions GuideDocument56 pagesAccounting Chapter 10 Solutions GuidemeaningbehindclosedNo ratings yet

- Soal P 7.2, 7.3, 7.5Document3 pagesSoal P 7.2, 7.3, 7.5boba milkNo ratings yet

- Basic AccountingDocument4 pagesBasic Accountingkanding21No ratings yet

- Chapter 24 Homework SolutionsDocument18 pagesChapter 24 Homework Solutionslenovot61No ratings yet

- Solutions To ProblemsDocument33 pagesSolutions To ProblemsggjjyyNo ratings yet

- Quiz3 HolyeDocument35 pagesQuiz3 HolyegoamankNo ratings yet

- Depriciation AccountingDocument42 pagesDepriciation Accountingezek1elNo ratings yet

- Chapter 8 PDFDocument62 pagesChapter 8 PDFgetasewNo ratings yet

- Chapter 009 Test BankDocument13 pagesChapter 009 Test Banknadecho1No ratings yet

- AccountingDocument7 pagesAccountingGifford NaleNo ratings yet

- Problem Solving 16Document11 pagesProblem Solving 16Ehab M. Abdel HadyNo ratings yet

- Homework 4: Computing Deferred Income Tax (Supplement B)Document5 pagesHomework 4: Computing Deferred Income Tax (Supplement B)Dev SharmaNo ratings yet

- Intermediate Accounting IFRS 3rd Edition-574-576Document3 pagesIntermediate Accounting IFRS 3rd Edition-574-576dindaNo ratings yet

- Accounting Ratios Tell The Story of Financial HealthDocument2 pagesAccounting Ratios Tell The Story of Financial Healthku_nabilaNo ratings yet

- CH 3Document19 pagesCH 3hey100% (1)

- Accounting Textbook Solutions - 43Document19 pagesAccounting Textbook Solutions - 43acc-expertNo ratings yet

- Chap005-Consolidation of Less-Than-Wholly Owned SubsidiariesDocument71 pagesChap005-Consolidation of Less-Than-Wholly Owned Subsidiaries_casals100% (3)

- Financial AccountingDocument4 pagesFinancial Accountingbub12345678No ratings yet

- Udah Bener'Document4 pagesUdah Bener'Shafa AzahraNo ratings yet

- ACC-423 Learning Team B Week 2 Textbook ProblemsDocument10 pagesACC-423 Learning Team B Week 2 Textbook ProblemsdanielsvcNo ratings yet

- Chapter 3Document30 pagesChapter 3Varun ChauhanNo ratings yet

- 5.1 Questions: Chapter 5 Relevant Information For Decision Making With A Focus On Pricing DecisionsDocument37 pages5.1 Questions: Chapter 5 Relevant Information For Decision Making With A Focus On Pricing DecisionsLiyana ChuaNo ratings yet

- Chapter 4Document16 pagesChapter 4Girma NegashNo ratings yet

- Public AccountingDocument3 pagesPublic Accountingjoliejolie28No ratings yet

- CVP AnalysisDocument7 pagesCVP AnalysisKat Lontok0% (1)

- CH 11Document51 pagesCH 11Nguyen Ngoc Minh Chau (K15 HL)No ratings yet

- Ch01 SMDocument33 pagesCh01 SMcalz_ccccssssdddd_550% (1)

- DocxDocument6 pagesDocxVịt HoàngNo ratings yet

- ch06 SolDocument10 pagesch06 SolJohn Nigz PayeeNo ratings yet

- Chapter 2Document17 pagesChapter 2jinny6061100% (1)

- Fair ValueDocument8 pagesFair Valueiceman2167No ratings yet

- Early in The Year Bill Barnes and Several Friends OrganizedDocument1 pageEarly in The Year Bill Barnes and Several Friends OrganizedM Bilal Saleem0% (1)

- S03 - Chapter 5 Job Order Costing Without AnswersDocument2 pagesS03 - Chapter 5 Job Order Costing Without AnswersRigel Kent MansuetoNo ratings yet

- Managerial Accounting: Job Order CostingDocument75 pagesManagerial Accounting: Job Order Costingsouayeh wejdenNo ratings yet

- Delta Oil Company Uses The Successful Efforts Method To Account ForDocument1 pageDelta Oil Company Uses The Successful Efforts Method To Account ForFreelance WorkerNo ratings yet

- Prepare A Cash Budget - by Quarter and in Total ... - GlobalExperts4UDocument31 pagesPrepare A Cash Budget - by Quarter and in Total ... - GlobalExperts4USaiful IslamNo ratings yet

- Advanced AccountingDocument304 pagesAdvanced AccountingDeep100% (2)

- Rubica - Acc123 Final ExamDocument30 pagesRubica - Acc123 Final ExammarietorianoNo ratings yet

- ACG 2071, Test 2-Sample QuestionsDocument11 pagesACG 2071, Test 2-Sample QuestionsCresenciano MalabuyocNo ratings yet

- 2018 Management Accounting Ibm2 PrepDocument9 pages2018 Management Accounting Ibm2 PrepВероника КулякNo ratings yet

- CVP Analysis QA AllDocument63 pagesCVP Analysis QA Allg8kd6r8np2No ratings yet

- Managerial Accounting PDFDocument8 pagesManagerial Accounting PDFMeryana DjapNo ratings yet

- Full Book Test 5Document12 pagesFull Book Test 5alihanaveed9No ratings yet

- Tutorial 7Document16 pagesTutorial 7JMSB09No ratings yet

- Soultions - Chapter 3Document8 pagesSoultions - Chapter 3Naudia L. TurnbullNo ratings yet

- Charles AKMENDocument11 pagesCharles AKMENCharles GohNo ratings yet

- Chapter 7 Facility LayoutDocument6 pagesChapter 7 Facility LayoutAndrew Miranda100% (1)

- Decision Tree Assignment: Supervised By: Dr. Adel Sakr Introduced By: Nehal Nabil Abd AlzaherDocument3 pagesDecision Tree Assignment: Supervised By: Dr. Adel Sakr Introduced By: Nehal Nabil Abd AlzaherNehal NabilNo ratings yet

- Change Management and ResistanceDocument5 pagesChange Management and ResistanceNehal NabilNo ratings yet

- Specialized Training Program in Big Data AnalyticsDocument3 pagesSpecialized Training Program in Big Data AnalyticsNehal NabilNo ratings yet

- Mid Term Problem 1 & 2-1-54877Document2 pagesMid Term Problem 1 & 2-1-54877Nehal NabilNo ratings yet

- Addressing CompetitiveDocument17 pagesAddressing CompetitiveNehal Nabil100% (1)

- What Are The Main Steps of Quantitative Analysis?Document9 pagesWhat Are The Main Steps of Quantitative Analysis?Nehal NabilNo ratings yet

- Project: E-Guard Professor Dr. Ahmed FouadDocument23 pagesProject: E-Guard Professor Dr. Ahmed FouadNehal NabilNo ratings yet

- Chapter 1Document8 pagesChapter 1Nehal NabilNo ratings yet

- The Case For Enterprise-Ready Virtual Private CloudsDocument5 pagesThe Case For Enterprise-Ready Virtual Private CloudsNehal NabilNo ratings yet

- Academic Writing - Assessment SchemeDocument2 pagesAcademic Writing - Assessment SchemeNehal NabilNo ratings yet

- Session 2 Kotler - Mm15eDocument12 pagesSession 2 Kotler - Mm15eNehal NabilNo ratings yet

- Session 3 Kotler - Mm15e PDFDocument15 pagesSession 3 Kotler - Mm15e PDFNehal NabilNo ratings yet

- Network Exercise: Consider The PERT/CPM Network Shown Below. D E F G H I JDocument5 pagesNetwork Exercise: Consider The PERT/CPM Network Shown Below. D E F G H I JNehal NabilNo ratings yet

- Consider The Following Network: (P6) (Times Are in Weeks)Document1 pageConsider The Following Network: (P6) (Times Are in Weeks)Nehal NabilNo ratings yet

- Session 5 Kotler - Mm15e PDFDocument15 pagesSession 5 Kotler - Mm15e PDFNehal NabilNo ratings yet

- TH He Rise & & Fall O of New CokeDocument1 pageTH He Rise & & Fall O of New CokeNehal NabilNo ratings yet

- Training (Problem Solving - Decision Making)Document88 pagesTraining (Problem Solving - Decision Making)Nehal NabilNo ratings yet

- PowerPoint Slides Business EtiquetteDocument81 pagesPowerPoint Slides Business EtiquetteNehal Nabil100% (1)

- Training (Problem Solving - Decision Making)Document88 pagesTraining (Problem Solving - Decision Making)Nehal NabilNo ratings yet

- Review Questions On Standard-1Document4 pagesReview Questions On Standard-1George Adjei100% (1)

- Options - Capturing The Volatility Premium Through Call OverwritingDocument12 pagesOptions - Capturing The Volatility Premium Through Call OverwritingXerach GHNo ratings yet

- PADERES V. CA (2005) Summary: MICC Executed A REM Over 21 Lands Including Improvements in Favor of BancoDocument3 pagesPADERES V. CA (2005) Summary: MICC Executed A REM Over 21 Lands Including Improvements in Favor of BancoRachel LeachonNo ratings yet

- Franchise Accounting - DoneDocument3 pagesFranchise Accounting - DoneJymldy EnclnNo ratings yet

- Varanasi - Sugam Darshan - 1121232Document1 pageVaranasi - Sugam Darshan - 1121232raj1602No ratings yet

- Synopsis RaghvendraDocument34 pagesSynopsis RaghvendraNadar AkshaNo ratings yet

- 6807-1295 - Mr. Rambabu Prasad GuptaDocument2 pages6807-1295 - Mr. Rambabu Prasad GuptaMahesh SapkotaNo ratings yet

- Call Paper Wieke Dewi SuryandariDocument25 pagesCall Paper Wieke Dewi Suryandariargo victoriaNo ratings yet

- United States Court of Appeals For The Second Circuit: Docket Nos. 98-9269, 98-9270 August Term, 1998Document6 pagesUnited States Court of Appeals For The Second Circuit: Docket Nos. 98-9269, 98-9270 August Term, 1998Scribd Government DocsNo ratings yet

- Bricks Bussines PlanDocument23 pagesBricks Bussines Plansirajt300No ratings yet

- Personal Loan Application Form: Applicant DetailDocument8 pagesPersonal Loan Application Form: Applicant DetailAkanksha GuptaNo ratings yet

- Upstocx Demat-Account-Closure-Form PDFDocument1 pageUpstocx Demat-Account-Closure-Form PDFGautam DixitNo ratings yet

- Current Affairs 2017Document17 pagesCurrent Affairs 2017hinaNo ratings yet

- IIM Sambalpur ExampleDocument2 pagesIIM Sambalpur ExampledebojyotiNo ratings yet

- Build Financial Confidence: One of A Series of Papers On The Confident Retirement ApproachDocument9 pagesBuild Financial Confidence: One of A Series of Papers On The Confident Retirement ApproachBiki sahaNo ratings yet

- Problem Session-2 - 15.03.2012Document44 pagesProblem Session-2 - 15.03.2012markydee_20No ratings yet

- Koons Buick Pontiac GMC, Inc. v. Nigh, 543 U.S. 50 (2004)Document22 pagesKoons Buick Pontiac GMC, Inc. v. Nigh, 543 U.S. 50 (2004)Scribd Government DocsNo ratings yet

- Letter Submission MR 71 2018Document3 pagesLetter Submission MR 71 2018Ronish ChandraNo ratings yet

- Service Delivery Process - An Analysis Through Service Blueprinting at IL&FS Invest SmartDocument37 pagesService Delivery Process - An Analysis Through Service Blueprinting at IL&FS Invest Smartsam_max_bladerunner100% (2)

- FIN 645 - Chapter 6 - Interest Rate FuturesDocument45 pagesFIN 645 - Chapter 6 - Interest Rate FuturesAllieya AlawiNo ratings yet

- Nursery Care Corp Vs City of ManilaDocument2 pagesNursery Care Corp Vs City of ManilaCarlu YooNo ratings yet

- Leslie Ha Contract Quote PDFDocument1 pageLeslie Ha Contract Quote PDFfllamas1973No ratings yet

- 財務習題Document2 pages財務習題李映諭No ratings yet

- MBA Questions I Year & II Year Safety ManagementDocument44 pagesMBA Questions I Year & II Year Safety Managementbabu1434100% (3)

- Metrobank vs. Riverside MillsDocument18 pagesMetrobank vs. Riverside MillsStrawberryNo ratings yet

- Revoobit - Extended Trial Balance 2022Document3 pagesRevoobit - Extended Trial Balance 2022NURUL AIN EDIANNo ratings yet

- Business Accounting Quiz 2 (Answers) Updated.Document7 pagesBusiness Accounting Quiz 2 (Answers) Updated.Hareen JuniorNo ratings yet