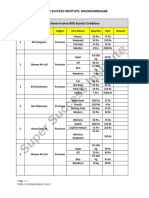

FAA Ist Assignemnt

FAA Ist Assignemnt

You might also like

- BasicAcctng AsgnmtSpreadsheets Unit 02Document9 pagesBasicAcctng AsgnmtSpreadsheets Unit 02Syeda Muneebaali67% (3)

- InvoiceDocument1 pageInvoiceAnirban DindaNo ratings yet

- Pas 7 Cash Flow StatementsDocument7 pagesPas 7 Cash Flow StatementsRechelleNo ratings yet

- T4Document1 pageT4mehulpbNo ratings yet

- B Com - VI Sem - (Specialization - Computer Applications) - Computerised Accounting With Tally PDFDocument19 pagesB Com - VI Sem - (Specialization - Computer Applications) - Computerised Accounting With Tally PDFDoIT Churu0% (1)

- Tally ProblemsDocument9 pagesTally ProblemsM ZNo ratings yet

- Konica Minolta Bizhub 367 BrochureDocument4 pagesKonica Minolta Bizhub 367 BrochureAsad Irfan100% (1)

- Tally - ERP 9Document1 pageTally - ERP 9mandeepNo ratings yet

- XyzDocument8 pagesXyzRaghav KanoongoNo ratings yet

- Tally - Erp 9 - Interest Calculation of Accounting & Inventory Vouchers Creation, Modification, DeletionsDocument5 pagesTally - Erp 9 - Interest Calculation of Accounting & Inventory Vouchers Creation, Modification, DeletionsHeemanshu ShahNo ratings yet

- Tally Syllabus: 1. Basics of AccountingDocument4 pagesTally Syllabus: 1. Basics of AccountingijrailNo ratings yet

- TallyDocument27 pagesTallyvinothkumararaja8249No ratings yet

- Ch-13 Cash Book Entry in Tally PrimeDocument3 pagesCh-13 Cash Book Entry in Tally PrimeSanchita ChauhanNo ratings yet

- Tally Question PaperDocument5 pagesTally Question PaperSubham Kumar SahooNo ratings yet

- Tally Accouting GST PDFDocument35 pagesTally Accouting GST PDFkannnamreddyeswar50% (2)

- GST in Tally Erp.9Document4 pagesGST in Tally Erp.9Jancy SunishNo ratings yet

- TallyDocument172 pagesTallyEzhil Kumar100% (1)

- Tally Assignment: Question Create A Company Using Tally SoftwareDocument11 pagesTally Assignment: Question Create A Company Using Tally SoftwaregsaNo ratings yet

- Villamor FinalDocument25 pagesVillamor FinalRinconada Benori ReynalynNo ratings yet

- Tally Assignment With GSTDocument28 pagesTally Assignment With GSTCoindcx SrkNo ratings yet

- Tally QuestionsDocument73 pagesTally QuestionsVishal Shah100% (1)

- Set 1 & 3 PDFDocument6 pagesSet 1 & 3 PDFCorona VirusNo ratings yet

- Tally TestDocument2 pagesTally TestHK DuggalNo ratings yet

- Working Problem For Tally With GSTDocument8 pagesWorking Problem For Tally With GSTPalani Sun InforNo ratings yet

- Fundamentals of TallyDocument81 pagesFundamentals of TallyRishabh chaudhary100% (1)

- Calculation of GSTDocument13 pagesCalculation of GSTSukanta PalNo ratings yet

- Final AssignmentDocument42 pagesFinal AssignmentRoopesh PandeNo ratings yet

- Itt Training Programme Project On "Tally - Erp9 Features Including Tally Audit "Document37 pagesItt Training Programme Project On "Tally - Erp9 Features Including Tally Audit "Yash shajNo ratings yet

- Project On T 9Document37 pagesProject On T 9Kartik JhakalNo ratings yet

- Comcomputerised Acct Invited LectureDocument7 pagesComcomputerised Acct Invited LectureBenstarkNo ratings yet

- Tally RefDocument352 pagesTally RefsandeepfatehpuriaNo ratings yet

- Tally Test: Kishan Lal SharmaDocument4 pagesTally Test: Kishan Lal Sharmakhan patelNo ratings yet

- Fill The Details As Fallow: DirectoryDocument3 pagesFill The Details As Fallow: DirectoryKrishan PatelNo ratings yet

- Questions On Trial Balance To StudentsDocument6 pagesQuestions On Trial Balance To Studentsveraji3735No ratings yet

- Step by Step Tally Question Practice SBSCDocument2 pagesStep by Step Tally Question Practice SBSCBalkrishan AgarwalNo ratings yet

- Tally Introduction-: +Document12 pagesTally Introduction-: +Harsh KhandelwalNo ratings yet

- GST With Tally (PDFDrive)Document63 pagesGST With Tally (PDFDrive)sakthi raoNo ratings yet

- Tally Test No. 2Document2 pagesTally Test No. 2AMIN BUHARI ABDUL KHADER83% (6)

- Question 7Document2 pagesQuestion 7abhishek georgeNo ratings yet

- Kitgum Business Institute: 4.0 Accounting VouchersDocument23 pagesKitgum Business Institute: 4.0 Accounting Vouchersoloka George100% (2)

- Tally Prime Question Paper TP001Document1 pageTally Prime Question Paper TP001AnuragNo ratings yet

- List of PublicationsDocument1 pageList of PublicationsbagsouravNo ratings yet

- Tally AssignmentDocument9 pagesTally AssignmentDebjit Naskar100% (1)

- A1 - Assignment Stock Practice in Tally PrimeDocument4 pagesA1 - Assignment Stock Practice in Tally Primeram dhukeNo ratings yet

- Tally and GSTDocument12 pagesTally and GSTKannan SNo ratings yet

- Accounting and Tally BookDocument10 pagesAccounting and Tally BookCA PASSNo ratings yet

- Syllabus Deg CeDocument78 pagesSyllabus Deg CebagsouravNo ratings yet

- Test 3Document7 pagesTest 3info view0% (1)

- Learning Tally - Erp 9 With GST in TamilDocument2 pagesLearning Tally - Erp 9 With GST in TamilSiva LingamNo ratings yet

- Accounts - Journal EntriesDocument3 pagesAccounts - Journal Entriessjjjsjs0% (1)

- Tally 5Document128 pagesTally 5Rahul MakwanaNo ratings yet

- Tally Exercise 6Document1 pageTally Exercise 6Arun100% (1)

- TALLY Suraj 1 1 1 (1) 1Document31 pagesTALLY Suraj 1 1 1 (1) 1Roopesh PandeNo ratings yet

- GST Accounting Entries in TallyDocument16 pagesGST Accounting Entries in TallyRevathi naidu100% (1)

- Tally Erp 9 Coplete TheoryDocument94 pagesTally Erp 9 Coplete Theorytuntun yadavNo ratings yet

- Tally Question PaperDocument4 pagesTally Question PaperJitender Rajpoot0% (1)

- Tally ERP9 Course Syllabus GSTDocument37 pagesTally ERP9 Course Syllabus GSTPeter joseph SinhaNo ratings yet

- Discount Tally PDFDocument6 pagesDiscount Tally PDFTHABIRA BAGNo ratings yet

- GST Tally ERP9 English: A Handbook for Understanding GST Implementation in TallyFrom EverandGST Tally ERP9 English: A Handbook for Understanding GST Implementation in TallyRating: 5 out of 5 stars5/5 (1)

- Financial Accounting Unit 1Document7 pagesFinancial Accounting Unit 1MOAAZ AHMEDNo ratings yet

- Accounting For Mgt.Document3 pagesAccounting For Mgt.RNo ratings yet

- A Study On Working Capital Management in Textile IndustryDocument7 pagesA Study On Working Capital Management in Textile IndustryAmaan KhanNo ratings yet

- 2018 Management Accounting Ibm2 PrepDocument9 pages2018 Management Accounting Ibm2 PrepВероника КулякNo ratings yet

- TVM NetDocument24 pagesTVM Netkareem3456No ratings yet

- Birla Sunlife InsuranceDocument64 pagesBirla Sunlife InsuranceNithin ThinaNo ratings yet

- Hong Kong Monthly Digest of Statistics (February 2014)Document334 pagesHong Kong Monthly Digest of Statistics (February 2014)Eduardo PetazzeNo ratings yet

- Assignment-Competitive Advantage % PrinciplesDocument13 pagesAssignment-Competitive Advantage % PrinciplesSky Mambo100% (4)

- Employee Stock Purchase PlanDocument13 pagesEmployee Stock Purchase Planvikrant911No ratings yet

- Auditing Problem (Modules 7-10)Document6 pagesAuditing Problem (Modules 7-10)Serena Van der WoodsenNo ratings yet

- Computation of Deductions (Sanderson Employee's)Document6 pagesComputation of Deductions (Sanderson Employee's)CHRISTOPHER DIAZNo ratings yet

- Ashutosh Sohil Salary 2020-03 PDFDocument1 pageAshutosh Sohil Salary 2020-03 PDFMohit Sharma100% (1)

- Sustainability-Rse Financial Performance Mineral IndustryDocument25 pagesSustainability-Rse Financial Performance Mineral IndustryConi Fuenzalida VarelaNo ratings yet

- ACC 4041 Tutorial - Business Income and ExpensesDocument5 pagesACC 4041 Tutorial - Business Income and ExpensesAyekurik0% (1)

- Financial Statements: Viet Nam - Aeg Joint Stock CompanyDocument3 pagesFinancial Statements: Viet Nam - Aeg Joint Stock CompanyHung NguyenNo ratings yet

- Assessing A New Venture's Financial Strength and Viability: Bruce R. Barringer R. Duane IrelandDocument36 pagesAssessing A New Venture's Financial Strength and Viability: Bruce R. Barringer R. Duane IrelandGhulam MustafaNo ratings yet

- CFAB - Accounting - QB - Chapter 13Document14 pagesCFAB - Accounting - QB - Chapter 13Huy NguyenNo ratings yet

- Financial Accounting: Theory & Practice Intangible AssetsDocument81 pagesFinancial Accounting: Theory & Practice Intangible AssetsXNo ratings yet

- Chap002 Cost TermsDocument41 pagesChap002 Cost TermsNgái Ngủ100% (1)

- Chap 001Document80 pagesChap 001matthewsNo ratings yet

- C39CA 1617 Sample PaperDocument6 pagesC39CA 1617 Sample Paperdoba1000No ratings yet

- Group 7 Vinamilk Financial AnalysisDocument17 pagesGroup 7 Vinamilk Financial AnalysisLại Ngọc Cẩm NhungNo ratings yet

- Standalone Balance Sheet: As at March 31, 2019Document40 pagesStandalone Balance Sheet: As at March 31, 2019Ashutosh BiswalNo ratings yet

- Why It's So Difficult For Most People To Make Money in The Markets - Van K. TharpDocument3 pagesWhy It's So Difficult For Most People To Make Money in The Markets - Van K. Tharptraderdust4502100% (4)

- Output Vat - Zero-Rated SalesDocument36 pagesOutput Vat - Zero-Rated SalesCoreen Samaniego0% (2)

- Tax2 Donalvo 2018 TSN First ExamDocument33 pagesTax2 Donalvo 2018 TSN First ExamsonyaNo ratings yet

- Project Report ReadymadeDocument13 pagesProject Report Readymademayank malikNo ratings yet

- Percentage Taxes UstDocument5 pagesPercentage Taxes UstGabriel PonceNo ratings yet

- Infosys Financial Analysis ReportDocument5 pagesInfosys Financial Analysis Reportbhavin rathodNo ratings yet

- Gopal G. Trivedi - (108-108) - (2011 - 2012) - Form24Document2 pagesGopal G. Trivedi - (108-108) - (2011 - 2012) - Form24Gopal TrivediNo ratings yet

- Arita Prima Indonesia Annual Report 2016 Company Profile Indonesia Investments PDFDocument103 pagesArita Prima Indonesia Annual Report 2016 Company Profile Indonesia Investments PDFNurul karimahNo ratings yet

Download as pdf or txt

You might also like

- BasicAcctng AsgnmtSpreadsheets Unit 02Document9 pagesBasicAcctng AsgnmtSpreadsheets Unit 02Syeda Muneebaali67% (3)

- InvoiceDocument1 pageInvoiceAnirban DindaNo ratings yet

- Pas 7 Cash Flow StatementsDocument7 pagesPas 7 Cash Flow StatementsRechelleNo ratings yet

- T4Document1 pageT4mehulpbNo ratings yet

- B Com - VI Sem - (Specialization - Computer Applications) - Computerised Accounting With Tally PDFDocument19 pagesB Com - VI Sem - (Specialization - Computer Applications) - Computerised Accounting With Tally PDFDoIT Churu0% (1)

- Tally ProblemsDocument9 pagesTally ProblemsM ZNo ratings yet

- Konica Minolta Bizhub 367 BrochureDocument4 pagesKonica Minolta Bizhub 367 BrochureAsad Irfan100% (1)

- Tally - ERP 9Document1 pageTally - ERP 9mandeepNo ratings yet

- XyzDocument8 pagesXyzRaghav KanoongoNo ratings yet

- Tally - Erp 9 - Interest Calculation of Accounting & Inventory Vouchers Creation, Modification, DeletionsDocument5 pagesTally - Erp 9 - Interest Calculation of Accounting & Inventory Vouchers Creation, Modification, DeletionsHeemanshu ShahNo ratings yet

- Tally Syllabus: 1. Basics of AccountingDocument4 pagesTally Syllabus: 1. Basics of AccountingijrailNo ratings yet

- TallyDocument27 pagesTallyvinothkumararaja8249No ratings yet

- Ch-13 Cash Book Entry in Tally PrimeDocument3 pagesCh-13 Cash Book Entry in Tally PrimeSanchita ChauhanNo ratings yet

- Tally Question PaperDocument5 pagesTally Question PaperSubham Kumar SahooNo ratings yet

- Tally Accouting GST PDFDocument35 pagesTally Accouting GST PDFkannnamreddyeswar50% (2)

- GST in Tally Erp.9Document4 pagesGST in Tally Erp.9Jancy SunishNo ratings yet

- TallyDocument172 pagesTallyEzhil Kumar100% (1)

- Tally Assignment: Question Create A Company Using Tally SoftwareDocument11 pagesTally Assignment: Question Create A Company Using Tally SoftwaregsaNo ratings yet

- Villamor FinalDocument25 pagesVillamor FinalRinconada Benori ReynalynNo ratings yet

- Tally Assignment With GSTDocument28 pagesTally Assignment With GSTCoindcx SrkNo ratings yet

- Tally QuestionsDocument73 pagesTally QuestionsVishal Shah100% (1)

- Set 1 & 3 PDFDocument6 pagesSet 1 & 3 PDFCorona VirusNo ratings yet

- Tally TestDocument2 pagesTally TestHK DuggalNo ratings yet

- Working Problem For Tally With GSTDocument8 pagesWorking Problem For Tally With GSTPalani Sun InforNo ratings yet

- Fundamentals of TallyDocument81 pagesFundamentals of TallyRishabh chaudhary100% (1)

- Calculation of GSTDocument13 pagesCalculation of GSTSukanta PalNo ratings yet

- Final AssignmentDocument42 pagesFinal AssignmentRoopesh PandeNo ratings yet

- Itt Training Programme Project On "Tally - Erp9 Features Including Tally Audit "Document37 pagesItt Training Programme Project On "Tally - Erp9 Features Including Tally Audit "Yash shajNo ratings yet

- Project On T 9Document37 pagesProject On T 9Kartik JhakalNo ratings yet

- Comcomputerised Acct Invited LectureDocument7 pagesComcomputerised Acct Invited LectureBenstarkNo ratings yet

- Tally RefDocument352 pagesTally RefsandeepfatehpuriaNo ratings yet

- Tally Test: Kishan Lal SharmaDocument4 pagesTally Test: Kishan Lal Sharmakhan patelNo ratings yet

- Fill The Details As Fallow: DirectoryDocument3 pagesFill The Details As Fallow: DirectoryKrishan PatelNo ratings yet

- Questions On Trial Balance To StudentsDocument6 pagesQuestions On Trial Balance To Studentsveraji3735No ratings yet

- Step by Step Tally Question Practice SBSCDocument2 pagesStep by Step Tally Question Practice SBSCBalkrishan AgarwalNo ratings yet

- Tally Introduction-: +Document12 pagesTally Introduction-: +Harsh KhandelwalNo ratings yet

- GST With Tally (PDFDrive)Document63 pagesGST With Tally (PDFDrive)sakthi raoNo ratings yet

- Tally Test No. 2Document2 pagesTally Test No. 2AMIN BUHARI ABDUL KHADER83% (6)

- Question 7Document2 pagesQuestion 7abhishek georgeNo ratings yet

- Kitgum Business Institute: 4.0 Accounting VouchersDocument23 pagesKitgum Business Institute: 4.0 Accounting Vouchersoloka George100% (2)

- Tally Prime Question Paper TP001Document1 pageTally Prime Question Paper TP001AnuragNo ratings yet

- List of PublicationsDocument1 pageList of PublicationsbagsouravNo ratings yet

- Tally AssignmentDocument9 pagesTally AssignmentDebjit Naskar100% (1)

- A1 - Assignment Stock Practice in Tally PrimeDocument4 pagesA1 - Assignment Stock Practice in Tally Primeram dhukeNo ratings yet

- Tally and GSTDocument12 pagesTally and GSTKannan SNo ratings yet

- Accounting and Tally BookDocument10 pagesAccounting and Tally BookCA PASSNo ratings yet

- Syllabus Deg CeDocument78 pagesSyllabus Deg CebagsouravNo ratings yet

- Test 3Document7 pagesTest 3info view0% (1)

- Learning Tally - Erp 9 With GST in TamilDocument2 pagesLearning Tally - Erp 9 With GST in TamilSiva LingamNo ratings yet

- Accounts - Journal EntriesDocument3 pagesAccounts - Journal Entriessjjjsjs0% (1)

- Tally 5Document128 pagesTally 5Rahul MakwanaNo ratings yet

- Tally Exercise 6Document1 pageTally Exercise 6Arun100% (1)

- TALLY Suraj 1 1 1 (1) 1Document31 pagesTALLY Suraj 1 1 1 (1) 1Roopesh PandeNo ratings yet

- GST Accounting Entries in TallyDocument16 pagesGST Accounting Entries in TallyRevathi naidu100% (1)

- Tally Erp 9 Coplete TheoryDocument94 pagesTally Erp 9 Coplete Theorytuntun yadavNo ratings yet

- Tally Question PaperDocument4 pagesTally Question PaperJitender Rajpoot0% (1)

- Tally ERP9 Course Syllabus GSTDocument37 pagesTally ERP9 Course Syllabus GSTPeter joseph SinhaNo ratings yet

- Discount Tally PDFDocument6 pagesDiscount Tally PDFTHABIRA BAGNo ratings yet

- GST Tally ERP9 English: A Handbook for Understanding GST Implementation in TallyFrom EverandGST Tally ERP9 English: A Handbook for Understanding GST Implementation in TallyRating: 5 out of 5 stars5/5 (1)

- Financial Accounting Unit 1Document7 pagesFinancial Accounting Unit 1MOAAZ AHMEDNo ratings yet

- Accounting For Mgt.Document3 pagesAccounting For Mgt.RNo ratings yet

- A Study On Working Capital Management in Textile IndustryDocument7 pagesA Study On Working Capital Management in Textile IndustryAmaan KhanNo ratings yet

- 2018 Management Accounting Ibm2 PrepDocument9 pages2018 Management Accounting Ibm2 PrepВероника КулякNo ratings yet

- TVM NetDocument24 pagesTVM Netkareem3456No ratings yet

- Birla Sunlife InsuranceDocument64 pagesBirla Sunlife InsuranceNithin ThinaNo ratings yet

- Hong Kong Monthly Digest of Statistics (February 2014)Document334 pagesHong Kong Monthly Digest of Statistics (February 2014)Eduardo PetazzeNo ratings yet

- Assignment-Competitive Advantage % PrinciplesDocument13 pagesAssignment-Competitive Advantage % PrinciplesSky Mambo100% (4)

- Employee Stock Purchase PlanDocument13 pagesEmployee Stock Purchase Planvikrant911No ratings yet

- Auditing Problem (Modules 7-10)Document6 pagesAuditing Problem (Modules 7-10)Serena Van der WoodsenNo ratings yet

- Computation of Deductions (Sanderson Employee's)Document6 pagesComputation of Deductions (Sanderson Employee's)CHRISTOPHER DIAZNo ratings yet

- Ashutosh Sohil Salary 2020-03 PDFDocument1 pageAshutosh Sohil Salary 2020-03 PDFMohit Sharma100% (1)

- Sustainability-Rse Financial Performance Mineral IndustryDocument25 pagesSustainability-Rse Financial Performance Mineral IndustryConi Fuenzalida VarelaNo ratings yet

- ACC 4041 Tutorial - Business Income and ExpensesDocument5 pagesACC 4041 Tutorial - Business Income and ExpensesAyekurik0% (1)

- Financial Statements: Viet Nam - Aeg Joint Stock CompanyDocument3 pagesFinancial Statements: Viet Nam - Aeg Joint Stock CompanyHung NguyenNo ratings yet

- Assessing A New Venture's Financial Strength and Viability: Bruce R. Barringer R. Duane IrelandDocument36 pagesAssessing A New Venture's Financial Strength and Viability: Bruce R. Barringer R. Duane IrelandGhulam MustafaNo ratings yet

- CFAB - Accounting - QB - Chapter 13Document14 pagesCFAB - Accounting - QB - Chapter 13Huy NguyenNo ratings yet

- Financial Accounting: Theory & Practice Intangible AssetsDocument81 pagesFinancial Accounting: Theory & Practice Intangible AssetsXNo ratings yet

- Chap002 Cost TermsDocument41 pagesChap002 Cost TermsNgái Ngủ100% (1)

- Chap 001Document80 pagesChap 001matthewsNo ratings yet

- C39CA 1617 Sample PaperDocument6 pagesC39CA 1617 Sample Paperdoba1000No ratings yet

- Group 7 Vinamilk Financial AnalysisDocument17 pagesGroup 7 Vinamilk Financial AnalysisLại Ngọc Cẩm NhungNo ratings yet

- Standalone Balance Sheet: As at March 31, 2019Document40 pagesStandalone Balance Sheet: As at March 31, 2019Ashutosh BiswalNo ratings yet

- Why It's So Difficult For Most People To Make Money in The Markets - Van K. TharpDocument3 pagesWhy It's So Difficult For Most People To Make Money in The Markets - Van K. Tharptraderdust4502100% (4)

- Output Vat - Zero-Rated SalesDocument36 pagesOutput Vat - Zero-Rated SalesCoreen Samaniego0% (2)

- Tax2 Donalvo 2018 TSN First ExamDocument33 pagesTax2 Donalvo 2018 TSN First ExamsonyaNo ratings yet

- Project Report ReadymadeDocument13 pagesProject Report Readymademayank malikNo ratings yet

- Percentage Taxes UstDocument5 pagesPercentage Taxes UstGabriel PonceNo ratings yet

- Infosys Financial Analysis ReportDocument5 pagesInfosys Financial Analysis Reportbhavin rathodNo ratings yet

- Gopal G. Trivedi - (108-108) - (2011 - 2012) - Form24Document2 pagesGopal G. Trivedi - (108-108) - (2011 - 2012) - Form24Gopal TrivediNo ratings yet

- Arita Prima Indonesia Annual Report 2016 Company Profile Indonesia Investments PDFDocument103 pagesArita Prima Indonesia Annual Report 2016 Company Profile Indonesia Investments PDFNurul karimahNo ratings yet