Download as docx, pdf, or txt

You might also like

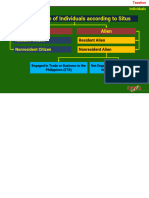

- Income Tax On Individuals - Ust PDFDocument15 pagesIncome Tax On Individuals - Ust PDFKana Lou Cassandra Besana100% (1)

- Samsona-Case-Act 122 5 - 3GDocument4 pagesSamsona-Case-Act 122 5 - 3GMelanie Samsona100% (2)

- Respondent PDFDocument30 pagesRespondent PDFUNIVERSITY LAW COLLEGE BHUBANESWAR60% (5)

- Reviewer Chapter 2Document6 pagesReviewer Chapter 2Ken NavarroNo ratings yet

- Handout 3Document51 pagesHandout 3Jilian Kate Alpapara Bustamante100% (1)

- Taxation 1 NotesDocument15 pagesTaxation 1 NotesTricia SandovalNo ratings yet

- Financial Statement Analysis ExerciseDocument5 pagesFinancial Statement Analysis ExerciseMelanie SamsonaNo ratings yet

- Case Analysis - Hockey Camp-CvpDocument2 pagesCase Analysis - Hockey Camp-CvpMelanie SamsonaNo ratings yet

- CASE ANALYSIS - Don Masters and Assoicates Law OfficeDocument1 pageCASE ANALYSIS - Don Masters and Assoicates Law OfficeMelanie Samsona0% (1)

- Case Analysis - Hockey Camp-CvpDocument2 pagesCase Analysis - Hockey Camp-CvpMelanie Samsona100% (1)

- Tax Reviewer PDFDocument6 pagesTax Reviewer PDFdave excelleNo ratings yet

- TAX-601: Income TAX - Individuals, Estates AND Trusts: - T R S ADocument12 pagesTAX-601: Income TAX - Individuals, Estates AND Trusts: - T R S AVaughn TheoNo ratings yet

- HO 1 INDIVIDUAL ESTATE AND TRUST TAXATION AND SOURCES OF INCOME Version 2.0Document5 pagesHO 1 INDIVIDUAL ESTATE AND TRUST TAXATION AND SOURCES OF INCOME Version 2.0Erine ContranoNo ratings yet

- Individual TaxpayersDocument3 pagesIndividual TaxpayersJoy Orena100% (2)

- Module TX003 Types On Income TaxpayersDocument3 pagesModule TX003 Types On Income TaxpayersErvin Ray FernandezNo ratings yet

- Module TX003 Types On Income TaxpayersDocument3 pagesModule TX003 Types On Income TaxpayersErwin TorresNo ratings yet

- TAX Outline 2 1Document18 pagesTAX Outline 2 1Master GTNo ratings yet

- TAX Outline 2 1Document18 pagesTAX Outline 2 1Master GTNo ratings yet

- Classification of Individual Income TaxpayersDocument3 pagesClassification of Individual Income TaxpayersOdessa De JesusNo ratings yet

- Tax601 Individual Itx Lecture Notes 122Document12 pagesTax601 Individual Itx Lecture Notes 122Justine JaymaNo ratings yet

- PreFi Tax PDFDocument21 pagesPreFi Tax PDFJoesil Dianne SempronNo ratings yet

- Quickie PreFi Tax PDFDocument12 pagesQuickie PreFi Tax PDFJoesil Dianne Sempron100% (1)

- Module 2 - Individuals Estates and Trusts Without Answer-2Document12 pagesModule 2 - Individuals Estates and Trusts Without Answer-2KarenFayeBadillesNo ratings yet

- Income Taxation ReviewerDocument8 pagesIncome Taxation ReviewerMichael SanchezNo ratings yet

- Introduction To Individual Income Taxation Chapter Overview and ObjectivesDocument25 pagesIntroduction To Individual Income Taxation Chapter Overview and ObjectivesMatta, Jherrie MaeNo ratings yet

- Tax 601Document11 pagesTax 601C.J. Clarisse FranciscoNo ratings yet

- Tax 1 MidtermsDocument18 pagesTax 1 MidtermsElaine Yap100% (1)

- Handout TaxationDocument2 pagesHandout TaxationJohn Oicemen RocaNo ratings yet

- Introduction To Income TaxationDocument4 pagesIntroduction To Income TaxationJean Diane JoveloNo ratings yet

- 03 Individuals. Study Notes. LectureDocument54 pages03 Individuals. Study Notes. Lecturemarvin.cpa.cmaNo ratings yet

- Taxation of IndividualsDocument22 pagesTaxation of IndividualsTurksNo ratings yet

- (TAX) Income Taxation Updated Jan 9 2022Document133 pages(TAX) Income Taxation Updated Jan 9 2022Reginald ValenciaNo ratings yet

- Income Tax ReviewerDocument18 pagesIncome Tax ReviewerRicci FrijillanoNo ratings yet

- Tax 1 Unit 1. Chapter 3Document5 pagesTax 1 Unit 1. Chapter 3angelika dijamcoNo ratings yet

- Summary Lesson 4Document6 pagesSummary Lesson 4Janien MedestomasNo ratings yet

- InTax Unit 2Document3 pagesInTax Unit 2ElleNo ratings yet

- M2u Classification Individual Taxation P1Document30 pagesM2u Classification Individual Taxation P1Xehdrickke FernandezNo ratings yet

- TAX LAW BALA SA BAR SERIES ExportDocument10 pagesTAX LAW BALA SA BAR SERIES Exportmetrexz17.03No ratings yet

- BAC103A-02a Income Tax For IndividualsDocument8 pagesBAC103A-02a Income Tax For IndividualsNovelyn Duyogan100% (1)

- Template Taxation Unit IIDocument29 pagesTemplate Taxation Unit IINacion, Jaime G.No ratings yet

- Income Tax On Individuals PDFDocument20 pagesIncome Tax On Individuals PDFKaren Joy MagsayoNo ratings yet

- Person - Orporation: Income TaxDocument223 pagesPerson - Orporation: Income TaxMich FelloneNo ratings yet

- Types of Individual Taxpayers Citizens Revenue Regulations No. 1-79Document8 pagesTypes of Individual Taxpayers Citizens Revenue Regulations No. 1-79James Evan I. ObnamiaNo ratings yet

- Person - Orporation: Income TaxDocument138 pagesPerson - Orporation: Income TaxMich FelloneNo ratings yet

- Income Tax On IndividualsDocument7 pagesIncome Tax On IndividualsThe man with a Square stacheNo ratings yet

- Written Output - Intro To Income Tax & Tax Schemes, Periods, and Methods and ReportingDocument10 pagesWritten Output - Intro To Income Tax & Tax Schemes, Periods, and Methods and ReportingDiana BellenNo ratings yet

- Income Taxation Midterm ReviewerDocument16 pagesIncome Taxation Midterm ReviewerRAMIREZ, MARVIN L.No ratings yet

- Types of TaxpayerDocument23 pagesTypes of TaxpayerReina Rose LebrillaNo ratings yet

- Income Tax On Individuals - REVISED 2022Document141 pagesIncome Tax On Individuals - REVISED 2022rav dano100% (2)

- Income On IndividualsDocument6 pagesIncome On IndividualsDarwish masturaNo ratings yet

- Lesson 5 Inclusions Exclusions From Gi Final TaxDocument17 pagesLesson 5 Inclusions Exclusions From Gi Final TaxOrduna Mae AnnNo ratings yet

- Classification of Individual TaxpayerDocument31 pagesClassification of Individual TaxpayerPatrick BituinNo ratings yet

- Citizenship and Residency Inside RP Outside RPDocument2 pagesCitizenship and Residency Inside RP Outside RPRhea Royce CabuhatNo ratings yet

- Bar TaxDocument29 pagesBar TaxMaisie ZabalaNo ratings yet

- What Are The Kinds of TaxpayersDocument4 pagesWhat Are The Kinds of TaxpayersALee Bud100% (1)

- Inroduction To Income TaxationDocument20 pagesInroduction To Income TaxationW-304-Bautista,PreciousNo ratings yet

- 3 - Income Tax On IndividualsDocument22 pages3 - Income Tax On IndividualsRylleMatthanCorderoNo ratings yet

- Types of Income Tax PayersDocument3 pagesTypes of Income Tax PayersAce Fati-igNo ratings yet

- G.Income Tax-Kinds of TaxpayerDocument1 pageG.Income Tax-Kinds of TaxpayerVinteNo ratings yet

- Income Taxation - Part 2Document12 pagesIncome Taxation - Part 2Prie DitucalanNo ratings yet

- Introduction To Income TaxDocument28 pagesIntroduction To Income TaxGeena Chavez GabrielNo ratings yet

- Mary Joy P. Junio, Cpa Notre Dame of Midsayap College Midsayap, CotabatoDocument8 pagesMary Joy P. Junio, Cpa Notre Dame of Midsayap College Midsayap, CotabatoJonathan JunioNo ratings yet

- (Tax1) - Income Tax On Individuals - Discussion and ActivitiesDocument12 pages(Tax1) - Income Tax On Individuals - Discussion and ActivitiesKim EllaNo ratings yet

- CH09B Income and Business TaxationDocument20 pagesCH09B Income and Business TaxationArt MelancholiaNo ratings yet

- Canadian International Taxation: Income Tax Rules for ResidentsFrom EverandCanadian International Taxation: Income Tax Rules for ResidentsNo ratings yet

- Impact of Time On Students' Academic PerformanceDocument14 pagesImpact of Time On Students' Academic PerformanceMelanie SamsonaNo ratings yet

- Assignment #2Document18 pagesAssignment #2Melanie Samsona100% (1)

- 5TH ActivityDocument15 pages5TH ActivityMelanie SamsonaNo ratings yet

- CombinepdfDocument3 pagesCombinepdfMelanie SamsonaNo ratings yet

- Specialized Industry HospitalDocument44 pagesSpecialized Industry HospitalMelanie SamsonaNo ratings yet

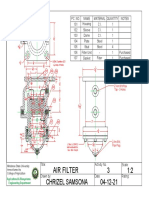

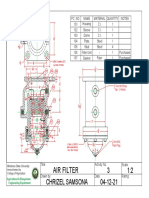

- Air FilterDocument1 pageAir FilterMelanie SamsonaNo ratings yet

- Corliss EngineDocument1 pageCorliss EngineMelanie SamsonaNo ratings yet

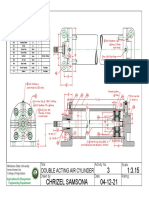

- Double Acting Air CylinderDocument1 pageDouble Acting Air CylinderMelanie SamsonaNo ratings yet

- Senior High School Electronic Class Record: InstructionsDocument39 pagesSenior High School Electronic Class Record: InstructionsMelanie SamsonaNo ratings yet

- FilmmakingDocument10 pagesFilmmakingMelanie Samsona100% (1)

- Koronadal National Comprehensive High School-Senior High SchoolDocument60 pagesKoronadal National Comprehensive High School-Senior High SchoolMelanie SamsonaNo ratings yet

- Impact of Time On StudentsDocument10 pagesImpact of Time On StudentsMelanie SamsonaNo ratings yet

- ENS 164 SyllabusDocument1 pageENS 164 SyllabusMelanie SamsonaNo ratings yet

- Stress: Normal Stress Shearing Stress Bearing StressDocument79 pagesStress: Normal Stress Shearing Stress Bearing StressMelanie Samsona100% (1)

- Happy MeDocument1 pageHappy MeMelanie SamsonaNo ratings yet

- ABE051 - 2nd MAjor ExamDocument1 pageABE051 - 2nd MAjor ExamMelanie SamsonaNo ratings yet

- Stress: Normal Stress Shearing Stress Bearing StressDocument23 pagesStress: Normal Stress Shearing Stress Bearing StressMelanie SamsonaNo ratings yet

- ENS 181 - Seatwork No. 1 - Samsona - A1Document1 pageENS 181 - Seatwork No. 1 - Samsona - A1Melanie SamsonaNo ratings yet

- TORSIONDocument25 pagesTORSIONMelanie SamsonaNo ratings yet

- STRAINDocument30 pagesSTRAINMelanie SamsonaNo ratings yet

- Grade 11-TVL 3 Aviso 2018-2019Document42 pagesGrade 11-TVL 3 Aviso 2018-2019Melanie SamsonaNo ratings yet

- Grade 11-Abm 3 HamiltonDocument45 pagesGrade 11-Abm 3 HamiltonMelanie SamsonaNo ratings yet

- ENS181 Seatwork 10 - Samsona - A1Document12 pagesENS181 Seatwork 10 - Samsona - A1Melanie SamsonaNo ratings yet

- Agricultural and Biosystems Engineering Department: College of AgricultureDocument1 pageAgricultural and Biosystems Engineering Department: College of AgricultureMelanie SamsonaNo ratings yet

- Module 4 Estate Taxation 3Document4 pagesModule 4 Estate Taxation 3Melanie SamsonaNo ratings yet

- Tax Planning, Avoidance, Tax EvasionDocument40 pagesTax Planning, Avoidance, Tax Evasionsimm170226No ratings yet

- Act 489 Majlis Amanah Rakyat Act 1966Document34 pagesAct 489 Majlis Amanah Rakyat Act 1966Adam Haida & CoNo ratings yet

- AssignmentDocument16 pagesAssignmentRiya SinghNo ratings yet

- CLJ5 Module2Document11 pagesCLJ5 Module2Smith BlakeNo ratings yet

- 13 G.R. No. 1051Document5 pages13 G.R. No. 1051Jessel MaglinteNo ratings yet

- Molefe V Mahaeng 1999 PDFDocument7 pagesMolefe V Mahaeng 1999 PDFModiti Moeti100% (1)

- IRVM 2006 CH 5Document8 pagesIRVM 2006 CH 5prasad19No ratings yet

- Forcible Entry ComplaintDocument2 pagesForcible Entry ComplaintPJeffayerNo ratings yet

- Reforming The NYPD and Its Enablers Who Thwart ReformDocument44 pagesReforming The NYPD and Its Enablers Who Thwart ReformNew England Law ReviewNo ratings yet

- Sexual Harassment and Child Abuse DigestsDocument15 pagesSexual Harassment and Child Abuse DigestsCarla January OngNo ratings yet

- Mathay Vs Consolidated Bank Case DigestDocument2 pagesMathay Vs Consolidated Bank Case DigestjovifactorNo ratings yet

- Rule 58 Preliminary InjunctionDocument250 pagesRule 58 Preliminary InjunctionDaniel Besina Jr.No ratings yet

- Case LawsDocument7 pagesCase LawsGoharz2No ratings yet

- Subject: Constitution Law Course: LLB Sl. No. TopicDocument3 pagesSubject: Constitution Law Course: LLB Sl. No. TopicJm VenkiNo ratings yet

- CredTrans 2017Document2 pagesCredTrans 2017Sinetch EteyNo ratings yet

- 23CAssessmentCert-IRM11 3 13 9 4Document35 pages23CAssessmentCert-IRM11 3 13 9 4MARK HOLMESNo ratings yet

- Bartlett v. Kansas Parole Board Et Al - Document No. 4Document3 pagesBartlett v. Kansas Parole Board Et Al - Document No. 4Justia.comNo ratings yet

- Vietnamese Legal GlossaryDocument124 pagesVietnamese Legal GlossaryTamber HiltonNo ratings yet

- Legal Ethics No. 2Document165 pagesLegal Ethics No. 2vj hernandezNo ratings yet

- Visayan SawmillDocument2 pagesVisayan SawmillPhie CuetoNo ratings yet

- Market Basket Age Discrimnination-Demoulas Response 4-1-24Document10 pagesMarket Basket Age Discrimnination-Demoulas Response 4-1-24Boston 25 DeskNo ratings yet

- List of Bribery DefendantsDocument9 pagesList of Bribery DefendantsStaten Island Advance/SILive.comNo ratings yet

- PC & FBC Workshop Agenda 09-28-16Document2 pagesPC & FBC Workshop Agenda 09-28-16L. A. PatersonNo ratings yet

- Barandon V FerrerDocument3 pagesBarandon V Ferrermangopie00000No ratings yet

- Bangalore Water Supply CaseDocument11 pagesBangalore Water Supply CaseSurya SriramNo ratings yet

- Case Digests Remedial LawDocument53 pagesCase Digests Remedial LawJulienne A ArgosinoNo ratings yet

- Crim 2 Elements (Index Card Size)Document117 pagesCrim 2 Elements (Index Card Size)Karla BeeNo ratings yet

- K.P.rm. Kuppan Chettiar Alias ... Vs Sp.R.M.rm. Ramaswami Chettiar ... On 15 January, 1946Document9 pagesK.P.rm. Kuppan Chettiar Alias ... Vs Sp.R.M.rm. Ramaswami Chettiar ... On 15 January, 1946Karthik KannappanNo ratings yet

- Pbs IosDocument48 pagesPbs Iospradeep punuruNo ratings yet