Download as docx, pdf, or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5834)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Stern Strategy EssentialsDocument121 pagesStern Strategy Essentialssatya324100% (3)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (903)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (824)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (405)

- Comprehensive Reviewer On Appraiser ExamjenDocument110 pagesComprehensive Reviewer On Appraiser ExamjenHarold Pelias87% (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- A Project On Cost AnalysisDocument80 pagesA Project On Cost Analysisnet635194% (16)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- (Andrew Davidson & Co) An Implied Prepayment Model For MBSDocument13 pages(Andrew Davidson & Co) An Implied Prepayment Model For MBSgatzarNo ratings yet

- Group 1Document15 pagesGroup 1Rolly BaniquedNo ratings yet

- GG NaDocument10 pagesGG NaRolly BaniquedNo ratings yet

- MAS Reviewer Roque Chapter 1 PDFDocument18 pagesMAS Reviewer Roque Chapter 1 PDFRolly BaniquedNo ratings yet

- Case Study Written ReportDocument39 pagesCase Study Written ReportRolly BaniquedNo ratings yet

- LP - Acctg - 19 - 1stsem - 2019-2020Document16 pagesLP - Acctg - 19 - 1stsem - 2019-2020Rolly BaniquedNo ratings yet

- Net Operating Income Sales Sales Average Operating Assets Net Operating Income Average Operating AssetsDocument4 pagesNet Operating Income Sales Sales Average Operating Assets Net Operating Income Average Operating AssetsRolly BaniquedNo ratings yet

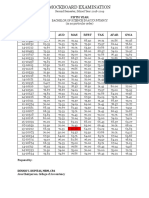

- Mockboard Examination: Id. NoDocument1 pageMockboard Examination: Id. NoRolly BaniquedNo ratings yet

- University of La Salette Inc. College of Accountancy College of Accountancy Student Council Dubinan East, Santiago City, PhilippinesDocument3 pagesUniversity of La Salette Inc. College of Accountancy College of Accountancy Student Council Dubinan East, Santiago City, PhilippinesRolly BaniquedNo ratings yet

- Gov SEC MeetingDocument1 pageGov SEC MeetingRolly BaniquedNo ratings yet

- Customer Privacy Policy 2019 V1Document2 pagesCustomer Privacy Policy 2019 V1Rolly BaniquedNo ratings yet

- Hamza Akbar: Investment/M&A Analyst InternDocument1 pageHamza Akbar: Investment/M&A Analyst Internapi-417045412No ratings yet

- Test Bank Chapter 3Document13 pagesTest Bank Chapter 3Caselyn Clyde UyNo ratings yet

- Milestone 2 Prompt 1Document9 pagesMilestone 2 Prompt 1NeelabhNo ratings yet

- Submissions: Score: 1 Out of 1Document77 pagesSubmissions: Score: 1 Out of 1Geli AceNo ratings yet

- Project On Ambuja CementDocument66 pagesProject On Ambuja CementMOHITKOLLINo ratings yet

- AFM Cash Budgeting Andria Ma'AmDocument9 pagesAFM Cash Budgeting Andria Ma'AmNavya KNo ratings yet

- NIBL Sahabhagita FundDocument5 pagesNIBL Sahabhagita FundyogendrasthaNo ratings yet

- Exim Bank MalaysiaDocument93 pagesExim Bank MalaysiaJohan Arief SoohaimiNo ratings yet

- DocxDocument26 pagesDocxMary DenizeNo ratings yet

- Aa1 3 2024Document39 pagesAa1 3 2024esratbithikaNo ratings yet

- Bayesian Methods For Measuring Operational Risks: ICBI Technical Risk Management ReportsDocument15 pagesBayesian Methods For Measuring Operational Risks: ICBI Technical Risk Management ReportsHejoolju Grubs100% (1)

- L & T Glass Installation QuoteDocument4 pagesL & T Glass Installation QuoteJessica Spears100% (1)

- Quizzer 5Document6 pagesQuizzer 5RarajNo ratings yet

- T4 - Past Paper CombinedDocument53 pagesT4 - Past Paper CombinedU Abdul Rehman100% (1)

- Set-Off and Counterclaim CJS HFRDocument4 pagesSet-Off and Counterclaim CJS HFRTitle IV-D Man with a plan100% (5)

- Investment Appraisal Taxation, InflationDocument8 pagesInvestment Appraisal Taxation, InflationJiya RajputNo ratings yet

- The Rationale of New Economic Policy 1991Document3 pagesThe Rationale of New Economic Policy 1991Neeraj Agarwal50% (2)

- ) Under The Correct Heading To Show Whether The Item: For Examiner's UseDocument13 pages) Under The Correct Heading To Show Whether The Item: For Examiner's UseAung Zaw HtweNo ratings yet

- Bir Revenue Regulations No. 4-2007Document22 pagesBir Revenue Regulations No. 4-2007hirohonmaNo ratings yet

- 10000027146Document47 pages10000027146Chapter 11 DocketsNo ratings yet

- MC AnswerDocument24 pagesMC AnswerMiss MegzzNo ratings yet

- CA Inter Tax Q MTP 2 May 2024 Castudynotes ComDocument13 pagesCA Inter Tax Q MTP 2 May 2024 Castudynotes ComineffableadityisticNo ratings yet

- Solomon WorkuDocument101 pagesSolomon WorkuchuchuNo ratings yet

- Finalising Basel III: in BriefDocument9 pagesFinalising Basel III: in BriefScribddNo ratings yet

- Complaint Management Policy-ISO Standards: Grievance Redressal IntroductionDocument9 pagesComplaint Management Policy-ISO Standards: Grievance Redressal IntroductionHitechSoft HitsoftNo ratings yet

- Banking and Finance Project-1Document37 pagesBanking and Finance Project-1ADITYA DHONENo ratings yet