Download as docx, pdf, or txt

You might also like

- Marginal - Absorption Costing - Practice Questions With SolutionsDocument11 pagesMarginal - Absorption Costing - Practice Questions With Solutionsaishabadar88% (17)

- Chapter 4Document8 pagesChapter 4Châu Ánh ViNo ratings yet

- Marginal & Absorption CostingDocument6 pagesMarginal & Absorption CostingEman Mirza100% (5)

- Marginal & Absorption Costing UpdatedDocument6 pagesMarginal & Absorption Costing UpdatedMUHAMMAD ZAID SIDDIQUI100% (2)

- Marginal & Absorption CostingDocument9 pagesMarginal & Absorption CostingRida JunejoNo ratings yet

- Math PracticeDocument3 pagesMath Practiceakmal_07No ratings yet

- Marginal CostingDocument4 pagesMarginal CostingFareha Riaz100% (3)

- Practice Set 2 (Cost Segregation and CVP)Document2 pagesPractice Set 2 (Cost Segregation and CVP)Jessica Aningat0% (1)

- Lecture 1-2 Marginal Vs Absoption CostingDocument23 pagesLecture 1-2 Marginal Vs Absoption CostingAfzal AhmedNo ratings yet

- Lecture 3-4 Marginal Vs Absoption CostingDocument16 pagesLecture 3-4 Marginal Vs Absoption CostingAfzal AhmedNo ratings yet

- Marginal CostingDocument2 pagesMarginal CostingOmkar DhamapurkarNo ratings yet

- TRIAL1Document2 pagesTRIAL1David DossouNo ratings yet

- Marginal CostingDocument2 pagesMarginal CostingpalaviyaNo ratings yet

- Cost & MGT II CH 1Document13 pagesCost & MGT II CH 1fikruhope533No ratings yet

- Absorption and Variable Costing ReviewDocument13 pagesAbsorption and Variable Costing ReviewRodelLabor100% (1)

- Variable and Absorption M 02Document6 pagesVariable and Absorption M 02sm munNo ratings yet

- Costing Techniques IllustrationDocument2 pagesCosting Techniques IllustrationbiggykhairNo ratings yet

- Budget .Document5 pagesBudget .rofoba6609No ratings yet

- Marginal Costing Chapter Satelite Centers PDFDocument17 pagesMarginal Costing Chapter Satelite Centers PDFSwasNo ratings yet

- BudgetDocument10 pagesBudgetKartikNo ratings yet

- Inter Cost 2Document27 pagesInter Cost 2Anirudha SatheNo ratings yet

- Variances MCQsDocument8 pagesVariances MCQsdanksaimNo ratings yet

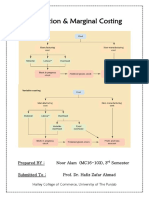

- Absorption & Marginal Costing - Noor Alam (MC16-103)Document24 pagesAbsorption & Marginal Costing - Noor Alam (MC16-103)Ahmed Ali Khan100% (2)

- Portfolio Problem 5 - P1Document7 pagesPortfolio Problem 5 - P1Dwight Gabriel C. GarciaNo ratings yet

- Revision5 Variance2Document4 pagesRevision5 Variance2adamNo ratings yet

- Cima Standard Costing Seesion 2 QuestionsDocument16 pagesCima Standard Costing Seesion 2 QuestionsKiri chrisNo ratings yet

- Practice Que 7 9 21 07092021 112106amDocument2 pagesPractice Que 7 9 21 07092021 112106amAsif KhanNo ratings yet

- Assignment # 1 Topic: Absorption and Marginal CostingDocument5 pagesAssignment # 1 Topic: Absorption and Marginal CostingAdnan HaiderNo ratings yet

- Examples FMA - 5Document10 pagesExamples FMA - 5DaddyNo ratings yet

- Budgetary ControlDocument3 pagesBudgetary Controlrohit sharmaNo ratings yet

- Management InformationDocument2 pagesManagement InformationMahediNo ratings yet

- Management Accounting 9mrQc9m4HBDocument3 pagesManagement Accounting 9mrQc9m4HBMadhuram SharmaNo ratings yet

- Absorption and Marginal CostingDocument19 pagesAbsorption and Marginal CostingsadikzeenatNo ratings yet

- Paper - 4: Cost Accounting and Financial Management Section A: Cost Accounting QuestionsDocument47 pagesPaper - 4: Cost Accounting and Financial Management Section A: Cost Accounting QuestionspranllNo ratings yet

- Grande Finale Solving May 2023 - A4 & T6 - Set 2Document5 pagesGrande Finale Solving May 2023 - A4 & T6 - Set 2henry misangoNo ratings yet

- Fill in The Blanks by Using The Words or Phrases Given BelowDocument8 pagesFill in The Blanks by Using The Words or Phrases Given BelowhokageNo ratings yet

- Absorption and Variable CostingDocument2 pagesAbsorption and Variable CostingFelimar CalaNo ratings yet

- 6.standard CostingDocument11 pages6.standard CostingInnocent escoNo ratings yet

- Assignment ProblemsDocument5 pagesAssignment ProblemsRamesh SigdelNo ratings yet

- Marginal Costing SumsDocument3 pagesMarginal Costing SumsMedhaNo ratings yet

- Variance QuestionsDocument3 pagesVariance QuestionsHadeed HafeezNo ratings yet

- Chapter 9 - Marginal - Absorption CostingDocument37 pagesChapter 9 - Marginal - Absorption CostingMaha IqrarNo ratings yet

- Management Information June-2012Document2 pagesManagement Information June-2012Laskar REAZNo ratings yet

- Week 11 Budgeting SystemsDocument12 pagesWeek 11 Budgeting SystemsDamien HewNo ratings yet

- Review Questions-Ac, MC &CVPDocument4 pagesReview Questions-Ac, MC &CVPOctavius MuyungiNo ratings yet

- ACCTG 42 Module 3Document5 pagesACCTG 42 Module 3Hazel Grace PaguiaNo ratings yet

- Meiktila University of Economics MBA 112Document2 pagesMeiktila University of Economics MBA 112ApicalMitten 502No ratings yet

- Marginal Costing NumericalDocument6 pagesMarginal Costing Numericalswarnim chauhanNo ratings yet

- Required: Prepare A Variable-Costing Income Statement For The Same PeriodDocument2 pagesRequired: Prepare A Variable-Costing Income Statement For The Same PeriodFarjana AkterNo ratings yet

- Total Variance: Required: Compute The Direct Materials, Direct Labor, and Variable Manufacturing Overhead VariancesDocument20 pagesTotal Variance: Required: Compute The Direct Materials, Direct Labor, and Variable Manufacturing Overhead VariancesEyuel SintayehuNo ratings yet

- Assignment 2024Document5 pagesAssignment 2024edwardphirijoshua656No ratings yet

- Practical Question For ManagementDocument10 pagesPractical Question For ManagementAbrantie JoeNo ratings yet

- Cost and Management Accounting II.Document19 pagesCost and Management Accounting II.Bahar aliyiNo ratings yet

- Marginal & Absorption Feb 20-19 PDFDocument12 pagesMarginal & Absorption Feb 20-19 PDFhamza khanNo ratings yet

- Learning Activity 1 Variable Vs Absorption Costing3Document1 pageLearning Activity 1 Variable Vs Absorption Costing3summerginger27No ratings yet

- Variable CostingDocument7 pagesVariable CostingRainie LopezNo ratings yet

- 2017 International Comparison Program in Asia and the Pacific: Purchasing Power Parities and Real Expenditures—A Summary ReportFrom Everand2017 International Comparison Program in Asia and the Pacific: Purchasing Power Parities and Real Expenditures—A Summary ReportNo ratings yet

- Economic and Business Forecasting: Analyzing and Interpreting Econometric ResultsFrom EverandEconomic and Business Forecasting: Analyzing and Interpreting Econometric ResultsNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet