Download as docx, pdf, or txt

You might also like

- A Project Report On Kotak Life InsuranceDocument103 pagesA Project Report On Kotak Life Insurancevarun_bawa25191543% (7)

- A Project Report On Kotak InsuranceDocument82 pagesA Project Report On Kotak Insurancevarun_bawa251915No ratings yet

- Treasury Management Sample Questions Dec 18 ExamsDocument114 pagesTreasury Management Sample Questions Dec 18 ExamsajithaNo ratings yet

- Bajaj Cash Assure Renewal Receipt PDFDocument1 pageBajaj Cash Assure Renewal Receipt PDFPawan KumarNo ratings yet

- Insurance Servicesin IndiaDocument102 pagesInsurance Servicesin Indiabandi vijayarajuNo ratings yet

- Institute of Business Management & Research, IPS Academy: Major Research Project SynopsisDocument17 pagesInstitute of Business Management & Research, IPS Academy: Major Research Project SynopsisRachi JainNo ratings yet

- Training and Development in BHARTI AXA Life InsuranceDocument70 pagesTraining and Development in BHARTI AXA Life InsuranceAshutoshSharmaNo ratings yet

- Comprehensive Study On The Product of Kotak Mahindra Life InsuranceDocument73 pagesComprehensive Study On The Product of Kotak Mahindra Life InsuranceMadhuKar RaiNo ratings yet

- 09 - Chapter 2Document43 pages09 - Chapter 2touffiqNo ratings yet

- Insurance Karwalo ApnaDocument10 pagesInsurance Karwalo ApnaSandeep ChawdaNo ratings yet

- Project Report On LICDocument50 pagesProject Report On LICgaurav_boy001No ratings yet

- Insurance Black BookDocument61 pagesInsurance Black BookKunal Charaniya100% (1)

- HDFC LifeDocument66 pagesHDFC LifeChetan PahwaNo ratings yet

- Metlife Report 1Document77 pagesMetlife Report 1JaiHanumankiNo ratings yet

- Research On Impact of Covid On Life Insurance SectorDocument89 pagesResearch On Impact of Covid On Life Insurance SectorShivani KambliNo ratings yet

- Oriental InsuranceDocument24 pagesOriental InsuranceSumit BorichaNo ratings yet

- Overview of Indian Life Insurance IndustryDocument59 pagesOverview of Indian Life Insurance IndustryRajesh SadadekarNo ratings yet

- Innovations in InsuranceDocument47 pagesInnovations in InsuranceDouglas StoneNo ratings yet

- Insurance Services: Primary Functions Secondary Functions Other Functions Primary FunctionsDocument4 pagesInsurance Services: Primary Functions Secondary Functions Other Functions Primary FunctionsSunny SharmaNo ratings yet

- Insurancecompanies Icicilombard 150702155917 Lva1 App6891Document53 pagesInsurancecompanies Icicilombard 150702155917 Lva1 App6891Rutuja KulkarniNo ratings yet

- Insurance Law Module 1 1Document14 pagesInsurance Law Module 1 1xakij19914No ratings yet

- Praful ProjectDocument63 pagesPraful Projectvikas yadavNo ratings yet

- Practice of General Insurance NotesDocument74 pagesPractice of General Insurance NotesMohit Kumar100% (15)

- Icici Life InsuranceDocument40 pagesIcici Life Insurancekrittika03No ratings yet

- Raquib Chowdhury 1603410109197Document21 pagesRaquib Chowdhury 1603410109197mahfuzNo ratings yet

- Updated Insurance Awareness PDFDocument35 pagesUpdated Insurance Awareness PDFAnonymous iLTVZWPekTNo ratings yet

- Banking and Insurance - 061Document9 pagesBanking and Insurance - 061KANHA SHARMA MBA Kolkata 2022-24No ratings yet

- Chapter 1Document54 pagesChapter 1Siva NathNo ratings yet

- Life Insurance: Insurance Collective Bearing of RiskDocument49 pagesLife Insurance: Insurance Collective Bearing of RiskghagsonaNo ratings yet

- Training and Development in BHARTI AXA Life InsuranceDocument75 pagesTraining and Development in BHARTI AXA Life Insuranceankitasachaan89No ratings yet

- Icici Prudential: An Analysis of Indian Insurance Industry With Special Reference ToDocument69 pagesIcici Prudential: An Analysis of Indian Insurance Industry With Special Reference ToRachit SachdevaNo ratings yet

- Research Project Report: in Partial Fulfillment of The Degree ofDocument84 pagesResearch Project Report: in Partial Fulfillment of The Degree ofanon_548912339No ratings yet

- Chapter 1: Insurance IntroductionDocument72 pagesChapter 1: Insurance IntroductionNeha SinghNo ratings yet

- Dissertation On ULIPDocument30 pagesDissertation On ULIPRakesh RajputNo ratings yet

- General Insurance Corporation of IndiaDocument44 pagesGeneral Insurance Corporation of IndiaDIVYA DUBEYNo ratings yet

- Customer Satisfaction & Recruitment of Financial Advisors ForDocument47 pagesCustomer Satisfaction & Recruitment of Financial Advisors Forabhishekkothari100% (4)

- Report On Recruitment of Life Advisors Bharti AXADocument84 pagesReport On Recruitment of Life Advisors Bharti AXAmegha140190No ratings yet

- Insurance Law ProjectDocument15 pagesInsurance Law ProjectShalini Dwivedi100% (1)

- 506080ACORD Certificates of Insurance Coverage - What Certification Owners As Well As Suppliers Required To KnowDocument2 pages506080ACORD Certificates of Insurance Coverage - What Certification Owners As Well As Suppliers Required To Knowhealthplan79No ratings yet

- Ankur SaxenaDocument85 pagesAnkur SaxenaMudit Dang AroraNo ratings yet

- 1st-2nd Unit Insurance Law 10th SemDocument47 pages1st-2nd Unit Insurance Law 10th Semsainipreeti20001No ratings yet

- Life InsuranceDocument55 pagesLife InsuranceNehaNo ratings yet

- Black BookDocument10 pagesBlack Bookharesh kukrejaNo ratings yet

- MODULE-2-sip ReportDocument32 pagesMODULE-2-sip ReportJoy OfficialNo ratings yet

- DefinitionDocument25 pagesDefinitionRahul SinghNo ratings yet

- General Insurance: General Insurance Is A General Term Used For All The Insurance Plans ThatDocument6 pagesGeneral Insurance: General Insurance Is A General Term Used For All The Insurance Plans ThatSarthak Khurana 2027803No ratings yet

- Sip PDFDocument81 pagesSip PDF41APayoshni ChaudhariNo ratings yet

- A Project Report On: An Analysis of Indian Insurance Industry With Special Reference TO Icici PrudentialDocument68 pagesA Project Report On: An Analysis of Indian Insurance Industry With Special Reference TO Icici PrudentialNiharika MathurNo ratings yet

- Tata AIG Life InsuranceDocument62 pagesTata AIG Life InsuranceMitul Modi100% (1)

- Insurance Law QuestionsDocument44 pagesInsurance Law QuestionsNithi SpsNo ratings yet

- Icici 1Document118 pagesIcici 1sknagarNo ratings yet

- Akshay ProjectDocument37 pagesAkshay ProjectAkšhâý AkýNo ratings yet

- Insurance Law ProjectDocument14 pagesInsurance Law Projectlokesh4nigamNo ratings yet

- Chapter 11 Audit of Insurance CompaniesDocument62 pagesChapter 11 Audit of Insurance CompaniesDiyanaBankovaNo ratings yet

- What Is Insurance?: PremiumDocument51 pagesWhat Is Insurance?: PremiumsangeethaNo ratings yet

- Project ON Life Insurance Corporati ONDocument34 pagesProject ON Life Insurance Corporati ONVirendra JhaNo ratings yet

- Market Share of Insurannce CompanyDocument29 pagesMarket Share of Insurannce Companysaurabh dixitNo ratings yet

- Insurance As A Investment Tool at Icici Bank Project Report Mba FinanceDocument73 pagesInsurance As A Investment Tool at Icici Bank Project Report Mba FinanceBabasab Patil (Karrisatte)No ratings yet

- Insurance, Regulations and Loss Prevention : Basic Rules for the Industry Insurance: Business strategy books, #5From EverandInsurance, Regulations and Loss Prevention : Basic Rules for the Industry Insurance: Business strategy books, #5No ratings yet

- Black Book 102Document71 pagesBlack Book 102Rishika BafnaNo ratings yet

- 25 Premium Calculation For Life-InsuranceDocument2 pages25 Premium Calculation For Life-Insuranceanujsharma0001No ratings yet

- Option Chain Part1Document3 pagesOption Chain Part1ramyatan SinghNo ratings yet

- International Financial Management 11 Edition: by Jeff MaduraDocument33 pagesInternational Financial Management 11 Edition: by Jeff MaduraCorolla SedanNo ratings yet

- Louise Bedford Trading InsightsDocument80 pagesLouise Bedford Trading Insightsartendu100% (3)

- Type of Policy:-YS Premium TableDocument11 pagesType of Policy:-YS Premium TableKuruAnandNo ratings yet

- Valerio Scacco PresentationDocument33 pagesValerio Scacco PresentationValerio ScaccoNo ratings yet

- Smart Income Protect - FlierDocument1 pageSmart Income Protect - Flierc.niharika1986No ratings yet

- CommodityDocument14 pagesCommodityChamp DsouzaNo ratings yet

- CFTC Commitments of Traders Report - CME (Futures Only) 06082013Document10 pagesCFTC Commitments of Traders Report - CME (Futures Only) 06082013Md YusofNo ratings yet

- BB050523125230716Document1 pageBB050523125230716chidambari SahooNo ratings yet

- 11 Valuation of Entrepreneurial VenturesDocument15 pages11 Valuation of Entrepreneurial VenturesSatendra JaiswalNo ratings yet

- Understanding Life InsuranceDocument3 pagesUnderstanding Life InsuranceSasiNo ratings yet

- Aviation InsuranceDocument11 pagesAviation InsuranceHaniaSadiaNo ratings yet

- Professional ExaminationDocument35 pagesProfessional ExaminationKarthic KeyanNo ratings yet

- Final Internship ReportDocument46 pagesFinal Internship Reportezaz ahmedNo ratings yet

- Chapter 4: Option Pricing Models: The Binomial Model: The Journal of DerivativesDocument59 pagesChapter 4: Option Pricing Models: The Binomial Model: The Journal of DerivativesTrúc NguyễnNo ratings yet

- Chapter 27Document20 pagesChapter 27Daisy Ann Cariaga SaccuanNo ratings yet

- Question 1: Explain Black Whastcholes Model and Show That It Satisfies Put Call Parity ?Document8 pagesQuestion 1: Explain Black Whastcholes Model and Show That It Satisfies Put Call Parity ?arpitNo ratings yet

- Bajaj Allianz Term PlanDocument4 pagesBajaj Allianz Term PlanTanuja KoshyNo ratings yet

- First Name: ChimwemweDocument7 pagesFirst Name: ChimwemweChimwemwe Thandiwe MtongaNo ratings yet

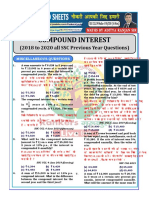

- Compound Interest: (2018 To 2020 All SSC Previous Year Questions)Document17 pagesCompound Interest: (2018 To 2020 All SSC Previous Year Questions)HakjsNo ratings yet

- CH 4 Hedging and DerivativesDocument31 pagesCH 4 Hedging and DerivativesAbdii DhufeeraNo ratings yet

- General Insurance Actuarial Interview QuestionsDocument20 pagesGeneral Insurance Actuarial Interview QuestionsJatin shahNo ratings yet

- Cp. 8: Financial Options and Applications in Corporate FinanceDocument12 pagesCp. 8: Financial Options and Applications in Corporate FinanceesthdNo ratings yet

- IC Trad Exam Reviewer 1Document5 pagesIC Trad Exam Reviewer 1scribd KokoNo ratings yet

- Zerodha Options Theory For Professional Trading Part 2Document141 pagesZerodha Options Theory For Professional Trading Part 2KS SiddhantNo ratings yet

- Basic Reinsurance Guide PDFDocument80 pagesBasic Reinsurance Guide PDFKandeel AfzalNo ratings yet