Download as docx, pdf, or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5825)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (903)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (823)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- 11882646 (1)Document1 page11882646 (1)Sacred Heart Academy of La LomaNo ratings yet

- Accounting For Labor - ExercisesDocument3 pagesAccounting For Labor - ExercisesAmy SpencerNo ratings yet

- North Delhi Municipal Corporation Internal Audit Department Zonal Audit Party, City ZoneDocument3 pagesNorth Delhi Municipal Corporation Internal Audit Department Zonal Audit Party, City ZoneSubhas MishraNo ratings yet

- Crude Next Day Buy Sell LevelDocument2 pagesCrude Next Day Buy Sell LevelSubhas MishraNo ratings yet

- SI (Store) C-87 Nabi Kareem 2012-14Document9 pagesSI (Store) C-87 Nabi Kareem 2012-14Subhas MishraNo ratings yet

- DELI07766D Internal Audit Officer Internal Audit Department 14 TH Floor Civic Centre Minto Road Delhi 110002 9818581720Document9 pagesDELI07766D Internal Audit Officer Internal Audit Department 14 TH Floor Civic Centre Minto Road Delhi 110002 9818581720Subhas MishraNo ratings yet

- Untitled Page PDFDocument1 pageUntitled Page PDFSubhas MishraNo ratings yet

- The Trend Following Trading StrategyDocument5 pagesThe Trend Following Trading StrategySubhas MishraNo ratings yet

- Para No.-30: Other Audit ObservationsDocument19 pagesPara No.-30: Other Audit ObservationsSubhas MishraNo ratings yet

- North Delhi Municipal Corporation Internal Audit Department Zonal Audit Party, City ZoneDocument1 pageNorth Delhi Municipal Corporation Internal Audit Department Zonal Audit Party, City ZoneSubhas MishraNo ratings yet

- North Delhi Municipal Corporation Internal Audit Department Zonal Audit Party, City Zone To Check The Accounts & Tender FilesDocument1 pageNorth Delhi Municipal Corporation Internal Audit Department Zonal Audit Party, City Zone To Check The Accounts & Tender FilesSubhas MishraNo ratings yet

- Pension ReportDocument17 pagesPension ReportSubhas MishraNo ratings yet

- MCP School MuftiwalanDocument4 pagesMCP School MuftiwalanSubhas MishraNo ratings yet

- NO - IAD/ZAP/CZ/2015/ Dated: North Delhi Municipal Corportion Internal Audit Department City ZoneDocument3 pagesNO - IAD/ZAP/CZ/2015/ Dated: North Delhi Municipal Corportion Internal Audit Department City ZoneSubhas MishraNo ratings yet

- SI Store C-84-I Turkman GateDocument9 pagesSI Store C-84-I Turkman GateSubhas MishraNo ratings yet

- Accounts Upto 2013 KBZDocument16 pagesAccounts Upto 2013 KBZSubhas MishraNo ratings yet

- Drop ParasDocument20 pagesDrop ParasSubhas MishraNo ratings yet

- A & C Report of CLZDocument86 pagesA & C Report of CLZSubhas MishraNo ratings yet

- North Delhimunicipal Corporation Internal Audit Department City ZoneDocument5 pagesNorth Delhimunicipal Corporation Internal Audit Department City ZoneSubhas MishraNo ratings yet

- Annual Progress ReportDocument3 pagesAnnual Progress ReportSubhas MishraNo ratings yet

- CSB 2016Document3,030 pagesCSB 2016Subhas MishraNo ratings yet

- Form IAD-4 C-90BDocument1 pageForm IAD-4 C-90BSubhas MishraNo ratings yet

- A&c Report of SPZDocument15 pagesA&c Report of SPZSubhas MishraNo ratings yet

- Cateogry BDocument124 pagesCateogry BSubhas MishraNo ratings yet

- SUBJECT: Request For Extension of Special Audit Programe W.E.F. 01.10.2016 To 31.12.2016Document2 pagesSUBJECT: Request For Extension of Special Audit Programe W.E.F. 01.10.2016 To 31.12.2016Subhas MishraNo ratings yet

- North Delhi Municipal Corporation Internal Audit Department City ZoneDocument6 pagesNorth Delhi Municipal Corporation Internal Audit Department City ZoneSubhas MishraNo ratings yet

- Sub: - Extension of Special Audit of CSB/CZDocument1 pageSub: - Extension of Special Audit of CSB/CZSubhas MishraNo ratings yet

- M&CW Centre HauzkhaziDocument5 pagesM&CW Centre HauzkhaziSubhas MishraNo ratings yet

- 510046214-Gas-Bill InvoiceDocument1 page510046214-Gas-Bill InvoiceviphainhumNo ratings yet

- Project One: Hana PLC. Is Unable To Reconcile The Bank Balance at September 30, 2018 Bank Reconciliation As FollowDocument6 pagesProject One: Hana PLC. Is Unable To Reconcile The Bank Balance at September 30, 2018 Bank Reconciliation As FollowYesakNo ratings yet

- Nowadays Plastic Money Replacements Such As Credit and Debit Cards Are Extremely Popular, Even More Than Banknotes and CoinsDocument3 pagesNowadays Plastic Money Replacements Such As Credit and Debit Cards Are Extremely Popular, Even More Than Banknotes and CoinsGurpal VehniwalNo ratings yet

- May Card StatementDocument4 pagesMay Card Statementlmcknight93.lmNo ratings yet

- Tally ERP9 MarathiEditionDocument19 pagesTally ERP9 MarathiEditionBharath Raj100% (1)

- Form WDocument8 pagesForm Wcvd8107No ratings yet

- Mohinder Singh DuaDocument1 pageMohinder Singh DuaHimanshu GoyalNo ratings yet

- StatementOfAccount 7157238650 22092022 182727Document4 pagesStatementOfAccount 7157238650 22092022 182727JANE 20COHE016No ratings yet

- 2GO Travel MS DELA TORRE AND CO ODI MPHDocument5 pages2GO Travel MS DELA TORRE AND CO ODI MPHCristine BuñalesNo ratings yet

- SettlementReportDocument1 pageSettlementReportBhanuranjan S BNo ratings yet

- F6 VAT QuestionsDocument9 pagesF6 VAT QuestionsHuỳnh TrungNo ratings yet

- Towncall Rural Bank, Inc.: To Adjust Retirement Fund Based On Retirement Benefit Obligation BalanceDocument1 pageTowncall Rural Bank, Inc.: To Adjust Retirement Fund Based On Retirement Benefit Obligation BalanceJudith CastroNo ratings yet

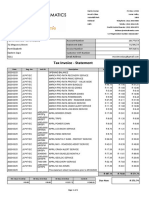

- MiX Telematics Tax Invoice - StatementDocument2 pagesMiX Telematics Tax Invoice - StatementMuvimwa IsraelNo ratings yet

- DE0319-5946 Front Support TableDocument1 pageDE0319-5946 Front Support TableAroelNo ratings yet

- Scan 18-Sep-2020 PDFDocument1 pageScan 18-Sep-2020 PDFdebasish dasNo ratings yet

- Customs Duty Revision QuestionsDocument3 pagesCustoms Duty Revision QuestionsGODBARNo ratings yet

- P45 - Regan LaingDocument3 pagesP45 - Regan LaingbangtantaekNo ratings yet

- Odm AcDocument2 pagesOdm AcRahavanNo ratings yet

- State Tax Return NC-F14Document2 pagesState Tax Return NC-F14aklank_218105No ratings yet

- Cashflow FormatDocument4 pagesCashflow FormatRaja kumarNo ratings yet

- High Level Setup For Accounts Payable (AP) On R12Document3 pagesHigh Level Setup For Accounts Payable (AP) On R12gopii_mNo ratings yet

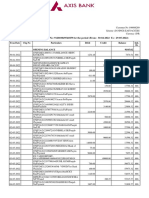

- Statement of Axis Account No:912010049541859 For The Period (From: 30-04-2022 To: 29-05-2022)Document5 pagesStatement of Axis Account No:912010049541859 For The Period (From: 30-04-2022 To: 29-05-2022)Rahul BansalNo ratings yet

- Translated - OBAŞ 2018 KURUMLAR BYNMDocument11 pagesTranslated - OBAŞ 2018 KURUMLAR BYNMIndranil MandalNo ratings yet

- InvoiceDocument1 pageInvoiceAmit PrajapatiNo ratings yet

- IT-11GA (New Form) For Private Service Tax Year 2020-21 19 Oct 20 - PDFDocument16 pagesIT-11GA (New Form) For Private Service Tax Year 2020-21 19 Oct 20 - PDFMASUD RANANo ratings yet

- Yes Bank Mitc Byoc PDFDocument13 pagesYes Bank Mitc Byoc PDFHarinder SinghNo ratings yet

- Liabilities Deferred TaxDocument3 pagesLiabilities Deferred TaxHikari0% (1)

- Solved International Paint Company Wants To Sell A Large Tract ofDocument1 pageSolved International Paint Company Wants To Sell A Large Tract ofAnbu jaromiaNo ratings yet