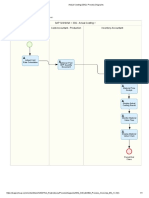

Example Sales Order Scenario

Example Sales Order Scenario

You might also like

- C Ts4co 2021 1673796089Document51 pagesC Ts4co 2021 1673796089bhaskarisbestNo ratings yet

- Implementing Integrated Business Planning: A Guide Exemplified With Process Context and SAP IBP Use CasesFrom EverandImplementing Integrated Business Planning: A Guide Exemplified With Process Context and SAP IBP Use CasesNo ratings yet

- Intercompany BillingDocument6 pagesIntercompany BillingkarthikbjNo ratings yet

- Left Outer JoinsDocument16 pagesLeft Outer JoinstopankajsharmaNo ratings yet

- Introducing Consolidation With SAP S/4HANA Finance For Group ReportingDocument7 pagesIntroducing Consolidation With SAP S/4HANA Finance For Group ReportingMichelle SYNo ratings yet

- Customer HierarchyDocument2 pagesCustomer HierarchyManishaNo ratings yet

- Release5 ReplicatingPricingDatafromtheSAPBackEnd 270116 1913 41114Document2 pagesRelease5 ReplicatingPricingDatafromtheSAPBackEnd 270116 1913 41114ahoilNo ratings yet

- About Error HandlingDocument6 pagesAbout Error HandlingGK SKNo ratings yet

- Product Cost by Sales Order: Scenario: PrerequisitesDocument5 pagesProduct Cost by Sales Order: Scenario: PrerequisitesGK SKNo ratings yet

- Valuated and Non-Valuated Sale Order Scenarios - Business Process FlowDocument3 pagesValuated and Non-Valuated Sale Order Scenarios - Business Process FlowvrkattulaNo ratings yet

- Valuated Project StockDocument9 pagesValuated Project StockjesurajajosephNo ratings yet

- Pre Reqisites To SD FI IntegrationDocument5 pagesPre Reqisites To SD FI IntegrationraghuNo ratings yet

- SAP Business Strategy & Product Portfolio and SAP HANA Cloud OfferingDocument17 pagesSAP Business Strategy & Product Portfolio and SAP HANA Cloud OfferingVEERANo ratings yet

- Intro ERP Using GBI Slides FI en v2.01Document25 pagesIntro ERP Using GBI Slides FI en v2.01shobhit1980inNo ratings yet

- EY Parthenon Pharma Industry Changes Survey Final Web 052017 PDFDocument16 pagesEY Parthenon Pharma Industry Changes Survey Final Web 052017 PDFMuhammad HassanNo ratings yet

- Competitor Analysis Framework - Definition, Types & ExamplesDocument23 pagesCompetitor Analysis Framework - Definition, Types & ExamplesRupesh SinghNo ratings yet

- Uneecops Technologies LTDDocument12 pagesUneecops Technologies LTDRajan KumarNo ratings yet

- Financial Accounting Course: 5101 Camden Lane, Pearland, TX 77584Document32 pagesFinancial Accounting Course: 5101 Camden Lane, Pearland, TX 77584Shaik ShafiNo ratings yet

- Enterprise StructureDocument13 pagesEnterprise StructuremadanvankaNo ratings yet

- SAP Procure To PayDocument13 pagesSAP Procure To PayAfifa Ahsan JannatNo ratings yet

- Maintaining The Deadline TypeDocument2 pagesMaintaining The Deadline TypereddysdNo ratings yet

- AP AR ConfigurationDocument36 pagesAP AR ConfigurationLeo O Junior100% (1)

- Assortment Planning: The Merchandise Category StructureDocument21 pagesAssortment Planning: The Merchandise Category StructureSabyasachi KonarNo ratings yet

- Basic Everyday Journal Entries PDFDocument2 pagesBasic Everyday Journal Entries PDFsivasivasapNo ratings yet

- SAP Query - User Group Creation: SQ03Document21 pagesSAP Query - User Group Creation: SQ03nagendraNo ratings yet

- MKT Potential and Sales ForecastingDocument15 pagesMKT Potential and Sales ForecastingPravah ShuklaNo ratings yet

- Edi Orders TemplateDocument19 pagesEdi Orders TemplatesimplepunjabiNo ratings yet

- Inbound Data Flow in SAP Retail EnvironmentDocument3 pagesInbound Data Flow in SAP Retail EnvironmentEklavya BansalNo ratings yet

- MM Inventory ManagementDocument43 pagesMM Inventory Managementjai dNo ratings yet

- EDI 810 Invoice Segment LayoutDocument31 pagesEDI 810 Invoice Segment LayoutuurNo ratings yet

- How To Configure Valuated Project Stock - SCNDocument4 pagesHow To Configure Valuated Project Stock - SCNsapdhanushNo ratings yet

- Whitepaper F R en 2018Document2 pagesWhitepaper F R en 2018Debi GhoshNo ratings yet

- Install SAP Best Practices Content 1SG S4H OnPremise - Docx 1909Document1 pageInstall SAP Best Practices Content 1SG S4H OnPremise - Docx 1909A V SrikanthNo ratings yet

- Sales and Marketing Alignment ToolDocument12 pagesSales and Marketing Alignment ToolTony Peterz KurewaNo ratings yet

- HubSpot Sales Forecasting TemplateDocument14 pagesHubSpot Sales Forecasting TemplateFAUZULNo ratings yet

- ERP - Enterprise Resource PlanningDocument38 pagesERP - Enterprise Resource Planningnehank17100% (3)

- Raymond FMCG - Org - Structure V8Document46 pagesRaymond FMCG - Org - Structure V8Vikram BhandeNo ratings yet

- Sap Is Retail Sample Resume 2Document4 pagesSap Is Retail Sample Resume 2Deepak Singh PatelNo ratings yet

- SAP FI-CO Technical Interview Questions 1Document26 pagesSAP FI-CO Technical Interview Questions 1Naveenkrishna MohanasundaramNo ratings yet

- Asset Under ConstructionDocument2 pagesAsset Under ConstructionmohammedraulmadridNo ratings yet

- Case Study: SAP Implementation in Poultry (Hatcheries) Industry PDFDocument9 pagesCase Study: SAP Implementation in Poultry (Hatcheries) Industry PDFSrinivas N GowdaNo ratings yet

- 2020 How To Configuration Content S4HGR V2Document261 pages2020 How To Configuration Content S4HGR V2Mamatha PendurthyNo ratings yet

- Sap MM PDFDocument31 pagesSap MM PDFGourav RaoNo ratings yet

- RRBDocument43 pagesRRBvenkat100% (1)

- Cost Object ControllingDocument6 pagesCost Object ControllingImran Mohammad0% (1)

- Condition Technique Sap MMDocument6 pagesCondition Technique Sap MMchituNo ratings yet

- Understanding Production Order VarianceDocument21 pagesUnderstanding Production Order VarianceveysiyigitNo ratings yet

- AP363 Data Definition ContractDocument7 pagesAP363 Data Definition ContractCathy DiazNo ratings yet

- Accounting Entries - SAP SD ForumDocument9 pagesAccounting Entries - SAP SD ForumRanjeet Ashokrao UlheNo ratings yet

- Exalca Company Profile V 0.2Document8 pagesExalca Company Profile V 0.2Rajkumar CNo ratings yet

- SAP Customer Master Structure: Account GroupsDocument2 pagesSAP Customer Master Structure: Account GroupsMihaiNo ratings yet

- SAP FI ALL-SAP Document Split Configuration and Manual-V1.1-Trigger LauDocument20 pagesSAP FI ALL-SAP Document Split Configuration and Manual-V1.1-Trigger LauSubramanian ChandrasekarNo ratings yet

- Sales Area: S / 4 HANA ContentDocument34 pagesSales Area: S / 4 HANA ContentEnrique Israel Flores ZúñigaNo ratings yet

- All Sap TablesDocument46 pagesAll Sap TablespriyankapotlaNo ratings yet

- The Agile Business AnalystDocument56 pagesThe Agile Business Analystsembalap29No ratings yet

- Inter Company Sales ProcessDocument2 pagesInter Company Sales ProcessVasanth KrishnaNo ratings yet

- FI-SD Integration: Quotation Sales Order Delivery Note Invoice (Billing) PaymentDocument6 pagesFI-SD Integration: Quotation Sales Order Delivery Note Invoice (Billing) PaymentfarrukhbaigNo ratings yet

- Fixed Assets Training ManualDocument56 pagesFixed Assets Training ManualManikantan Natarajan100% (1)

- Process Phases of Asset Under Construction in SAP: Asset Module Optimization & Accuracy in Costing / Depreciation RunDocument2 pagesProcess Phases of Asset Under Construction in SAP: Asset Module Optimization & Accuracy in Costing / Depreciation RunUppiliappan GopalanNo ratings yet

- Intercompany Sales ProcessDocument2 pagesIntercompany Sales ProcessKumarragamNo ratings yet

- Integrated Business Planning A Complete Guide - 2020 EditionFrom EverandIntegrated Business Planning A Complete Guide - 2020 EditionNo ratings yet

- Define COPA Mapping: RequirementsDocument4 pagesDefine COPA Mapping: RequirementsGK SKNo ratings yet

- Customizing Settings For Asset DocumentsDocument2 pagesCustomizing Settings For Asset DocumentsGK SKNo ratings yet

- Check Configuration Settings For Mapping Entities: How-ToDocument2 pagesCheck Configuration Settings For Mapping Entities: How-ToGK SKNo ratings yet

- Determination of Account Assignments in Central Finance SystemDocument1 pageDetermination of Account Assignments in Central Finance SystemGK SKNo ratings yet

- Define Scenarios For Cost Object MappingDocument4 pagesDefine Scenarios For Cost Object MappingGK SKNo ratings yet

- Configuration in Central Finance System: MappingDocument6 pagesConfiguration in Central Finance System: MappingGK SKNo ratings yet

- History of Key Mappings: How-ToDocument2 pagesHistory of Key Mappings: How-ToGK SKNo ratings yet

- Define Technical Settings For All Involved Systems: PrerequisitesDocument2 pagesDefine Technical Settings For All Involved Systems: PrerequisitesGK SKNo ratings yet

- 3Document4 pages3GK SKNo ratings yet

- Data Mapping: Previous NextDocument2 pagesData Mapping: Previous NextGK SKNo ratings yet

- Applied Overhead: Costing SheetDocument8 pagesApplied Overhead: Costing SheetGK SKNo ratings yet

- 4Document4 pages4GK SKNo ratings yet

- Defense Forces and Public Security: PurposeDocument10 pagesDefense Forces and Public Security: PurposeGK SKNo ratings yet

- 2Document2 pages2GK SKNo ratings yet

- Req Type DeterminationDocument3 pagesReq Type DeterminationGK SKNo ratings yet

- OverheadDocument5 pagesOverheadGK SKNo ratings yet

- Product Cost by Sales Order: Scenario: PrerequisitesDocument5 pagesProduct Cost by Sales Order: Scenario: PrerequisitesGK SKNo ratings yet

- Variance Valuated StockDocument5 pagesVariance Valuated StockGK SKNo ratings yet

- Checklist For Cost Object Controlling With Sales-Order-Related ProductionDocument4 pagesChecklist For Cost Object Controlling With Sales-Order-Related ProductionGK SKNo ratings yet

- Valuated Special StockDocument8 pagesValuated Special StockGK SKNo ratings yet

- Standard Price Valuated StickDocument7 pagesStandard Price Valuated StickGK SKNo ratings yet

- Could Lead To Messy BattlesDocument2 pagesCould Lead To Messy BattlesGK SKNo ratings yet

- Valuated Sales Order Stocks: Complex Make-To-Order ProductionDocument7 pagesValuated Sales Order Stocks: Complex Make-To-Order ProductionGK SKNo ratings yet

- Mcconnell To Trump: Health Care'S All YoursDocument7 pagesMcconnell To Trump: Health Care'S All YoursGK SKNo ratings yet

- Update of Valuated Sales Order StockDocument3 pagesUpdate of Valuated Sales Order StockGK SKNo ratings yet

- TRM, New Instruments, Accounting Enhancements, ReportingDocument8 pagesTRM, New Instruments, Accounting Enhancements, ReportingGK SKNo ratings yet

- Non Valuated StockDocument4 pagesNon Valuated StockGK SKNo ratings yet

- ScribdDocument2 pagesScribdGK SKNo ratings yet

- 10 U.S. Code 2808: Morning Defense NewsletterDocument2 pages10 U.S. Code 2808: Morning Defense NewsletterGK SKNo ratings yet

- Practice Problems For Chapter 2 Part 1Document3 pagesPractice Problems For Chapter 2 Part 1Elisha MonteroNo ratings yet

- Group2 Managerial AccountinggDocument15 pagesGroup2 Managerial AccountinggVerano Michelle M.No ratings yet

- Acccob3 HW3Document6 pagesAcccob3 HW3neovaldezNo ratings yet

- AA025 Chapter AT7Document3 pagesAA025 Chapter AT7norismah isaNo ratings yet

- 46 Cost AccountingDocument23 pages46 Cost AccountingaprilNo ratings yet

- Rajapalayam MillDocument53 pagesRajapalayam MillVijaya LakshmiNo ratings yet

- 93 Production 51 Accounting AccountingDocument11 pages93 Production 51 Accounting AccountinganasirrrNo ratings yet

- 9410 - Job Order CostingDocument7 pages9410 - Job Order CostingMarshmallowNo ratings yet

- 08 Ias 2Document3 pages08 Ias 2Irtiza AbbasNo ratings yet

- Foundations of Operations Management Canadian 4th Edition Ritzman Solutions ManualDocument26 pagesFoundations of Operations Management Canadian 4th Edition Ritzman Solutions ManualMaryMurphyatqb98% (55)

- Estrella Company'S Mixing Department Fifo - Mixing Production: Step 1: Physical Flow AnalysisDocument15 pagesEstrella Company'S Mixing Department Fifo - Mixing Production: Step 1: Physical Flow AnalysisEarl Hyannis ElauriaNo ratings yet

- Mock Final Departmental Exam - Accounting 201 - NCABALUNA 1Document9 pagesMock Final Departmental Exam - Accounting 201 - NCABALUNA 1francis albaracinNo ratings yet

- Managerial Accounting Tools For Business Decision Making 7th Edition Weygandt Test BankDocument66 pagesManagerial Accounting Tools For Business Decision Making 7th Edition Weygandt Test BankKerriGonzalesgjtkz100% (13)

- C2 - Cost TerminologyDocument33 pagesC2 - Cost TerminologyNgọc Phương HoàngNo ratings yet

- Product Costing: Job and Process Operations: 1. Inventory Costs in Various OrganizationsDocument30 pagesProduct Costing: Job and Process Operations: 1. Inventory Costs in Various OrganizationsAnne Thea AtienzaNo ratings yet

- Actual Costing (33Q) - Process DiagramsDocument1 pageActual Costing (33Q) - Process DiagramsAhmed Al-SherbinyNo ratings yet

- Principles of Cost Accounting 15Th Edition Vanderbeck Test Bank Full Chapter PDFDocument48 pagesPrinciples of Cost Accounting 15Th Edition Vanderbeck Test Bank Full Chapter PDFmirabeltuyenwzp6f100% (10)

- Cost Accounting Cost AccumulationDocument57 pagesCost Accounting Cost AccumulationRoi Martin A. De VeyraNo ratings yet

- Process CostingDocument3 pagesProcess Costingjannatuldu03No ratings yet

- Tugas Managerial AccountinDocument3 pagesTugas Managerial Accountinlaurentinus fikaNo ratings yet

- Job Oder Costing CH 3Document62 pagesJob Oder Costing CH 3Abis BangashNo ratings yet

- CH 4 Working PapersDocument28 pagesCH 4 Working PapersYousef RawaniNo ratings yet

- Reviewer For Quiz 1Document9 pagesReviewer For Quiz 1skmasambongcouncilNo ratings yet

- Internship Report of Fahmida Nasrin KeyaDocument53 pagesInternship Report of Fahmida Nasrin KeyaNoman Khan TanvirNo ratings yet

- ACCT3203 Contemporary Managerial Accounting: Lecture Illustration Examples With SolutionsDocument10 pagesACCT3203 Contemporary Managerial Accounting: Lecture Illustration Examples With SolutionsJingwen YangNo ratings yet

- 3.0 Accounting For Materials, Labor, and OH 2023Document10 pages3.0 Accounting For Materials, Labor, and OH 2023Cristina NiebresNo ratings yet

- Cost of Manuf ScheduleDocument2 pagesCost of Manuf Scheduleebat11No ratings yet

- Inventory Question Bank 2013Document22 pagesInventory Question Bank 201344v8ct8cdyNo ratings yet

- Cost BBIT Lec-1Document11 pagesCost BBIT Lec-1Amna Seok-JinNo ratings yet

Download as docx, pdf, or txt

You might also like

- C Ts4co 2021 1673796089Document51 pagesC Ts4co 2021 1673796089bhaskarisbestNo ratings yet

- Implementing Integrated Business Planning: A Guide Exemplified With Process Context and SAP IBP Use CasesFrom EverandImplementing Integrated Business Planning: A Guide Exemplified With Process Context and SAP IBP Use CasesNo ratings yet

- Intercompany BillingDocument6 pagesIntercompany BillingkarthikbjNo ratings yet

- Left Outer JoinsDocument16 pagesLeft Outer JoinstopankajsharmaNo ratings yet

- Introducing Consolidation With SAP S/4HANA Finance For Group ReportingDocument7 pagesIntroducing Consolidation With SAP S/4HANA Finance For Group ReportingMichelle SYNo ratings yet

- Customer HierarchyDocument2 pagesCustomer HierarchyManishaNo ratings yet

- Release5 ReplicatingPricingDatafromtheSAPBackEnd 270116 1913 41114Document2 pagesRelease5 ReplicatingPricingDatafromtheSAPBackEnd 270116 1913 41114ahoilNo ratings yet

- About Error HandlingDocument6 pagesAbout Error HandlingGK SKNo ratings yet

- Product Cost by Sales Order: Scenario: PrerequisitesDocument5 pagesProduct Cost by Sales Order: Scenario: PrerequisitesGK SKNo ratings yet

- Valuated and Non-Valuated Sale Order Scenarios - Business Process FlowDocument3 pagesValuated and Non-Valuated Sale Order Scenarios - Business Process FlowvrkattulaNo ratings yet

- Valuated Project StockDocument9 pagesValuated Project StockjesurajajosephNo ratings yet

- Pre Reqisites To SD FI IntegrationDocument5 pagesPre Reqisites To SD FI IntegrationraghuNo ratings yet

- SAP Business Strategy & Product Portfolio and SAP HANA Cloud OfferingDocument17 pagesSAP Business Strategy & Product Portfolio and SAP HANA Cloud OfferingVEERANo ratings yet

- Intro ERP Using GBI Slides FI en v2.01Document25 pagesIntro ERP Using GBI Slides FI en v2.01shobhit1980inNo ratings yet

- EY Parthenon Pharma Industry Changes Survey Final Web 052017 PDFDocument16 pagesEY Parthenon Pharma Industry Changes Survey Final Web 052017 PDFMuhammad HassanNo ratings yet

- Competitor Analysis Framework - Definition, Types & ExamplesDocument23 pagesCompetitor Analysis Framework - Definition, Types & ExamplesRupesh SinghNo ratings yet

- Uneecops Technologies LTDDocument12 pagesUneecops Technologies LTDRajan KumarNo ratings yet

- Financial Accounting Course: 5101 Camden Lane, Pearland, TX 77584Document32 pagesFinancial Accounting Course: 5101 Camden Lane, Pearland, TX 77584Shaik ShafiNo ratings yet

- Enterprise StructureDocument13 pagesEnterprise StructuremadanvankaNo ratings yet

- SAP Procure To PayDocument13 pagesSAP Procure To PayAfifa Ahsan JannatNo ratings yet

- Maintaining The Deadline TypeDocument2 pagesMaintaining The Deadline TypereddysdNo ratings yet

- AP AR ConfigurationDocument36 pagesAP AR ConfigurationLeo O Junior100% (1)

- Assortment Planning: The Merchandise Category StructureDocument21 pagesAssortment Planning: The Merchandise Category StructureSabyasachi KonarNo ratings yet

- Basic Everyday Journal Entries PDFDocument2 pagesBasic Everyday Journal Entries PDFsivasivasapNo ratings yet

- SAP Query - User Group Creation: SQ03Document21 pagesSAP Query - User Group Creation: SQ03nagendraNo ratings yet

- MKT Potential and Sales ForecastingDocument15 pagesMKT Potential and Sales ForecastingPravah ShuklaNo ratings yet

- Edi Orders TemplateDocument19 pagesEdi Orders TemplatesimplepunjabiNo ratings yet

- Inbound Data Flow in SAP Retail EnvironmentDocument3 pagesInbound Data Flow in SAP Retail EnvironmentEklavya BansalNo ratings yet

- MM Inventory ManagementDocument43 pagesMM Inventory Managementjai dNo ratings yet

- EDI 810 Invoice Segment LayoutDocument31 pagesEDI 810 Invoice Segment LayoutuurNo ratings yet

- How To Configure Valuated Project Stock - SCNDocument4 pagesHow To Configure Valuated Project Stock - SCNsapdhanushNo ratings yet

- Whitepaper F R en 2018Document2 pagesWhitepaper F R en 2018Debi GhoshNo ratings yet

- Install SAP Best Practices Content 1SG S4H OnPremise - Docx 1909Document1 pageInstall SAP Best Practices Content 1SG S4H OnPremise - Docx 1909A V SrikanthNo ratings yet

- Sales and Marketing Alignment ToolDocument12 pagesSales and Marketing Alignment ToolTony Peterz KurewaNo ratings yet

- HubSpot Sales Forecasting TemplateDocument14 pagesHubSpot Sales Forecasting TemplateFAUZULNo ratings yet

- ERP - Enterprise Resource PlanningDocument38 pagesERP - Enterprise Resource Planningnehank17100% (3)

- Raymond FMCG - Org - Structure V8Document46 pagesRaymond FMCG - Org - Structure V8Vikram BhandeNo ratings yet

- Sap Is Retail Sample Resume 2Document4 pagesSap Is Retail Sample Resume 2Deepak Singh PatelNo ratings yet

- SAP FI-CO Technical Interview Questions 1Document26 pagesSAP FI-CO Technical Interview Questions 1Naveenkrishna MohanasundaramNo ratings yet

- Asset Under ConstructionDocument2 pagesAsset Under ConstructionmohammedraulmadridNo ratings yet

- Case Study: SAP Implementation in Poultry (Hatcheries) Industry PDFDocument9 pagesCase Study: SAP Implementation in Poultry (Hatcheries) Industry PDFSrinivas N GowdaNo ratings yet

- 2020 How To Configuration Content S4HGR V2Document261 pages2020 How To Configuration Content S4HGR V2Mamatha PendurthyNo ratings yet

- Sap MM PDFDocument31 pagesSap MM PDFGourav RaoNo ratings yet

- RRBDocument43 pagesRRBvenkat100% (1)

- Cost Object ControllingDocument6 pagesCost Object ControllingImran Mohammad0% (1)

- Condition Technique Sap MMDocument6 pagesCondition Technique Sap MMchituNo ratings yet

- Understanding Production Order VarianceDocument21 pagesUnderstanding Production Order VarianceveysiyigitNo ratings yet

- AP363 Data Definition ContractDocument7 pagesAP363 Data Definition ContractCathy DiazNo ratings yet

- Accounting Entries - SAP SD ForumDocument9 pagesAccounting Entries - SAP SD ForumRanjeet Ashokrao UlheNo ratings yet

- Exalca Company Profile V 0.2Document8 pagesExalca Company Profile V 0.2Rajkumar CNo ratings yet

- SAP Customer Master Structure: Account GroupsDocument2 pagesSAP Customer Master Structure: Account GroupsMihaiNo ratings yet

- SAP FI ALL-SAP Document Split Configuration and Manual-V1.1-Trigger LauDocument20 pagesSAP FI ALL-SAP Document Split Configuration and Manual-V1.1-Trigger LauSubramanian ChandrasekarNo ratings yet

- Sales Area: S / 4 HANA ContentDocument34 pagesSales Area: S / 4 HANA ContentEnrique Israel Flores ZúñigaNo ratings yet

- All Sap TablesDocument46 pagesAll Sap TablespriyankapotlaNo ratings yet

- The Agile Business AnalystDocument56 pagesThe Agile Business Analystsembalap29No ratings yet

- Inter Company Sales ProcessDocument2 pagesInter Company Sales ProcessVasanth KrishnaNo ratings yet

- FI-SD Integration: Quotation Sales Order Delivery Note Invoice (Billing) PaymentDocument6 pagesFI-SD Integration: Quotation Sales Order Delivery Note Invoice (Billing) PaymentfarrukhbaigNo ratings yet

- Fixed Assets Training ManualDocument56 pagesFixed Assets Training ManualManikantan Natarajan100% (1)

- Process Phases of Asset Under Construction in SAP: Asset Module Optimization & Accuracy in Costing / Depreciation RunDocument2 pagesProcess Phases of Asset Under Construction in SAP: Asset Module Optimization & Accuracy in Costing / Depreciation RunUppiliappan GopalanNo ratings yet

- Intercompany Sales ProcessDocument2 pagesIntercompany Sales ProcessKumarragamNo ratings yet

- Integrated Business Planning A Complete Guide - 2020 EditionFrom EverandIntegrated Business Planning A Complete Guide - 2020 EditionNo ratings yet

- Define COPA Mapping: RequirementsDocument4 pagesDefine COPA Mapping: RequirementsGK SKNo ratings yet

- Customizing Settings For Asset DocumentsDocument2 pagesCustomizing Settings For Asset DocumentsGK SKNo ratings yet

- Check Configuration Settings For Mapping Entities: How-ToDocument2 pagesCheck Configuration Settings For Mapping Entities: How-ToGK SKNo ratings yet

- Determination of Account Assignments in Central Finance SystemDocument1 pageDetermination of Account Assignments in Central Finance SystemGK SKNo ratings yet

- Define Scenarios For Cost Object MappingDocument4 pagesDefine Scenarios For Cost Object MappingGK SKNo ratings yet

- Configuration in Central Finance System: MappingDocument6 pagesConfiguration in Central Finance System: MappingGK SKNo ratings yet

- History of Key Mappings: How-ToDocument2 pagesHistory of Key Mappings: How-ToGK SKNo ratings yet

- Define Technical Settings For All Involved Systems: PrerequisitesDocument2 pagesDefine Technical Settings For All Involved Systems: PrerequisitesGK SKNo ratings yet

- 3Document4 pages3GK SKNo ratings yet

- Data Mapping: Previous NextDocument2 pagesData Mapping: Previous NextGK SKNo ratings yet

- Applied Overhead: Costing SheetDocument8 pagesApplied Overhead: Costing SheetGK SKNo ratings yet

- 4Document4 pages4GK SKNo ratings yet

- Defense Forces and Public Security: PurposeDocument10 pagesDefense Forces and Public Security: PurposeGK SKNo ratings yet

- 2Document2 pages2GK SKNo ratings yet

- Req Type DeterminationDocument3 pagesReq Type DeterminationGK SKNo ratings yet

- OverheadDocument5 pagesOverheadGK SKNo ratings yet

- Product Cost by Sales Order: Scenario: PrerequisitesDocument5 pagesProduct Cost by Sales Order: Scenario: PrerequisitesGK SKNo ratings yet

- Variance Valuated StockDocument5 pagesVariance Valuated StockGK SKNo ratings yet

- Checklist For Cost Object Controlling With Sales-Order-Related ProductionDocument4 pagesChecklist For Cost Object Controlling With Sales-Order-Related ProductionGK SKNo ratings yet

- Valuated Special StockDocument8 pagesValuated Special StockGK SKNo ratings yet

- Standard Price Valuated StickDocument7 pagesStandard Price Valuated StickGK SKNo ratings yet

- Could Lead To Messy BattlesDocument2 pagesCould Lead To Messy BattlesGK SKNo ratings yet

- Valuated Sales Order Stocks: Complex Make-To-Order ProductionDocument7 pagesValuated Sales Order Stocks: Complex Make-To-Order ProductionGK SKNo ratings yet

- Mcconnell To Trump: Health Care'S All YoursDocument7 pagesMcconnell To Trump: Health Care'S All YoursGK SKNo ratings yet

- Update of Valuated Sales Order StockDocument3 pagesUpdate of Valuated Sales Order StockGK SKNo ratings yet

- TRM, New Instruments, Accounting Enhancements, ReportingDocument8 pagesTRM, New Instruments, Accounting Enhancements, ReportingGK SKNo ratings yet

- Non Valuated StockDocument4 pagesNon Valuated StockGK SKNo ratings yet

- ScribdDocument2 pagesScribdGK SKNo ratings yet

- 10 U.S. Code 2808: Morning Defense NewsletterDocument2 pages10 U.S. Code 2808: Morning Defense NewsletterGK SKNo ratings yet

- Practice Problems For Chapter 2 Part 1Document3 pagesPractice Problems For Chapter 2 Part 1Elisha MonteroNo ratings yet

- Group2 Managerial AccountinggDocument15 pagesGroup2 Managerial AccountinggVerano Michelle M.No ratings yet

- Acccob3 HW3Document6 pagesAcccob3 HW3neovaldezNo ratings yet

- AA025 Chapter AT7Document3 pagesAA025 Chapter AT7norismah isaNo ratings yet

- 46 Cost AccountingDocument23 pages46 Cost AccountingaprilNo ratings yet

- Rajapalayam MillDocument53 pagesRajapalayam MillVijaya LakshmiNo ratings yet

- 93 Production 51 Accounting AccountingDocument11 pages93 Production 51 Accounting AccountinganasirrrNo ratings yet

- 9410 - Job Order CostingDocument7 pages9410 - Job Order CostingMarshmallowNo ratings yet

- 08 Ias 2Document3 pages08 Ias 2Irtiza AbbasNo ratings yet

- Foundations of Operations Management Canadian 4th Edition Ritzman Solutions ManualDocument26 pagesFoundations of Operations Management Canadian 4th Edition Ritzman Solutions ManualMaryMurphyatqb98% (55)

- Estrella Company'S Mixing Department Fifo - Mixing Production: Step 1: Physical Flow AnalysisDocument15 pagesEstrella Company'S Mixing Department Fifo - Mixing Production: Step 1: Physical Flow AnalysisEarl Hyannis ElauriaNo ratings yet

- Mock Final Departmental Exam - Accounting 201 - NCABALUNA 1Document9 pagesMock Final Departmental Exam - Accounting 201 - NCABALUNA 1francis albaracinNo ratings yet

- Managerial Accounting Tools For Business Decision Making 7th Edition Weygandt Test BankDocument66 pagesManagerial Accounting Tools For Business Decision Making 7th Edition Weygandt Test BankKerriGonzalesgjtkz100% (13)

- C2 - Cost TerminologyDocument33 pagesC2 - Cost TerminologyNgọc Phương HoàngNo ratings yet

- Product Costing: Job and Process Operations: 1. Inventory Costs in Various OrganizationsDocument30 pagesProduct Costing: Job and Process Operations: 1. Inventory Costs in Various OrganizationsAnne Thea AtienzaNo ratings yet

- Actual Costing (33Q) - Process DiagramsDocument1 pageActual Costing (33Q) - Process DiagramsAhmed Al-SherbinyNo ratings yet

- Principles of Cost Accounting 15Th Edition Vanderbeck Test Bank Full Chapter PDFDocument48 pagesPrinciples of Cost Accounting 15Th Edition Vanderbeck Test Bank Full Chapter PDFmirabeltuyenwzp6f100% (10)

- Cost Accounting Cost AccumulationDocument57 pagesCost Accounting Cost AccumulationRoi Martin A. De VeyraNo ratings yet

- Process CostingDocument3 pagesProcess Costingjannatuldu03No ratings yet

- Tugas Managerial AccountinDocument3 pagesTugas Managerial Accountinlaurentinus fikaNo ratings yet

- Job Oder Costing CH 3Document62 pagesJob Oder Costing CH 3Abis BangashNo ratings yet

- CH 4 Working PapersDocument28 pagesCH 4 Working PapersYousef RawaniNo ratings yet

- Reviewer For Quiz 1Document9 pagesReviewer For Quiz 1skmasambongcouncilNo ratings yet

- Internship Report of Fahmida Nasrin KeyaDocument53 pagesInternship Report of Fahmida Nasrin KeyaNoman Khan TanvirNo ratings yet

- ACCT3203 Contemporary Managerial Accounting: Lecture Illustration Examples With SolutionsDocument10 pagesACCT3203 Contemporary Managerial Accounting: Lecture Illustration Examples With SolutionsJingwen YangNo ratings yet

- 3.0 Accounting For Materials, Labor, and OH 2023Document10 pages3.0 Accounting For Materials, Labor, and OH 2023Cristina NiebresNo ratings yet

- Cost of Manuf ScheduleDocument2 pagesCost of Manuf Scheduleebat11No ratings yet

- Inventory Question Bank 2013Document22 pagesInventory Question Bank 201344v8ct8cdyNo ratings yet

- Cost BBIT Lec-1Document11 pagesCost BBIT Lec-1Amna Seok-JinNo ratings yet