Download as docx, pdf, or txt

You might also like

- Master Budget With SolutionsDocument12 pagesMaster Budget With SolutionsDea Andal100% (4)

- (NEW) Assessment II - FinanceDocument13 pages(NEW) Assessment II - FinanceCindy Huang50% (8)

- c5 Solutions BudgetingDocument13 pagesc5 Solutions BudgetingChinnam Lalitha100% (1)

- History of Nubia and Abyssinia PDFDocument344 pagesHistory of Nubia and Abyssinia PDFkiros80% (5)

- Accounting Reviewer PDFDocument19 pagesAccounting Reviewer PDFLawd God100% (1)

- Chapter Two: Master Budget and Responsibility AccountingDocument25 pagesChapter Two: Master Budget and Responsibility Accountingweyn deguNo ratings yet

- Cost II (Chapter-Two)Document48 pagesCost II (Chapter-Two)SemiraNo ratings yet

- Purposes of Budgeting Systems: BudgetDocument42 pagesPurposes of Budgeting Systems: BudgetJohn Joseph CambaNo ratings yet

- Master BudgetingDocument20 pagesMaster Budgetingjoinme2dayNo ratings yet

- Budgeting and Profit PlanningDocument78 pagesBudgeting and Profit Planningmohammad bilalNo ratings yet

- Budgeting - Planning: A325 Discussion - March 19, 2012Document8 pagesBudgeting - Planning: A325 Discussion - March 19, 2012alfaNo ratings yet

- Master BudgetDocument12 pagesMaster Budgetshi shiiisshhNo ratings yet

- Profit Planning, Activity-Based Budgeting and E-Budgeting: Mcgraw-Hill/IrwinDocument78 pagesProfit Planning, Activity-Based Budgeting and E-Budgeting: Mcgraw-Hill/IrwinSi HarisNo ratings yet

- Operational Budgeting ReviewerDocument5 pagesOperational Budgeting ReviewerMilcah Deloso Santos100% (1)

- Lecture 10Document41 pagesLecture 10Riaz Baloch NotezaiNo ratings yet

- Answers chapter 9Document6 pagesAnswers chapter 9hannyhosnyNo ratings yet

- Brewer8e GEs PPT Chapter 8 UpdDocument22 pagesBrewer8e GEs PPT Chapter 8 UpdNguyễn Ngọc Quỳnh TiênNo ratings yet

- Master Budget TemplateDocument19 pagesMaster Budget TemplateSanie Hizkia Hendrik MendeNo ratings yet

- CH 10 BudgetingDocument83 pagesCH 10 BudgetingShannon BánañasNo ratings yet

- Material BudgetDocument37 pagesMaterial BudgetRahul SardaNo ratings yet

- Case Analysis (1 30)Document3 pagesCase Analysis (1 30)manishadaaNo ratings yet

- Budgeting and Profit Planning CR PDFDocument27 pagesBudgeting and Profit Planning CR PDFafreenessaniNo ratings yet

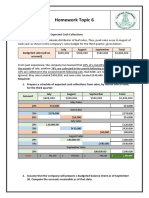

- Homework Topic 6: EXERCISE 8-1 Schedule of Expected Cash CollectionsDocument3 pagesHomework Topic 6: EXERCISE 8-1 Schedule of Expected Cash CollectionskhetamNo ratings yet

- CH 4 Profit PlanningDocument16 pagesCH 4 Profit PlanningMona ElzaherNo ratings yet

- Proj 2Document15 pagesProj 2Shahan AsifNo ratings yet

- Cost Accounting Assignment #2Document5 pagesCost Accounting Assignment #2BRIANNIE ASRI VIVASNo ratings yet

- Master BudgetDocument36 pagesMaster BudgetRafols AnnabelleNo ratings yet

- Operating Budget DiscussionDocument3 pagesOperating Budget DiscussionDavin DavinNo ratings yet

- Budgeting and Profit Planning CR PDFDocument24 pagesBudgeting and Profit Planning CR PDFLindcelle Jane DalopeNo ratings yet

- Drills - Comprehensive BudgetingDocument11 pagesDrills - Comprehensive BudgetingDan RyanNo ratings yet

- 6486 Chap008 PDFDocument17 pages6486 Chap008 PDFDheaNo ratings yet

- Handout 8 - CH8Document4 pagesHandout 8 - CH8MuhammadNo ratings yet

- Lecture 11Document26 pagesLecture 11Riaz Baloch Notezai100% (1)

- BudgetingDocument3 pagesBudgetingWen Xin GanNo ratings yet

- VANDERBECKCh7 - Multiple Choice (Theory and Problem)Document8 pagesVANDERBECKCh7 - Multiple Choice (Theory and Problem)Saeym SegoviaNo ratings yet

- Schedule 1: Sales BudgetDocument9 pagesSchedule 1: Sales BudgetAndrea Lyn Salonga CacayNo ratings yet

- Final Exam - Sent StudentsDocument6 pagesFinal Exam - Sent StudentsYến Hoàng HảiNo ratings yet

- PA2 - Master Budget and Its ComponentsDocument10 pagesPA2 - Master Budget and Its ComponentsSunil N PunjabiNo ratings yet

- Cost II Chap3Document11 pagesCost II Chap3abelNo ratings yet

- Kế Toán Quản Trị Chương 3Document41 pagesKế Toán Quản Trị Chương 3Nhựt AnhNo ratings yet

- Seminar 11answer Group 11Document115 pagesSeminar 11answer Group 11Shweta SridharNo ratings yet

- Lecture 3 - Budgeting 1Document35 pagesLecture 3 - Budgeting 1Tgrh TgrhNo ratings yet

- Cost Accounting Profit Planning QuizDocument8 pagesCost Accounting Profit Planning QuizSittie Ainna A. UnteNo ratings yet

- Profit PlanningDocument86 pagesProfit PlanningSederiku KabaruzaNo ratings yet

- Cost II - Assignment & WorksheetDocument7 pagesCost II - Assignment & WorksheetBeamlak WegayehuNo ratings yet

- Profit Planning Discussion ProblemsDocument5 pagesProfit Planning Discussion ProblemsVatchdemonNo ratings yet

- Meiktila University of Economics MBA 112Document2 pagesMeiktila University of Economics MBA 112ApicalMitten 502No ratings yet

- Chap07 Rev. FI5 Ex PRDocument11 pagesChap07 Rev. FI5 Ex PRKhryzha Hanne Dela CruzNo ratings yet

- Manufacturing Company BudgetingDocument10 pagesManufacturing Company BudgetingSajakul SornNo ratings yet

- Topic 1 BudgetingDocument58 pagesTopic 1 BudgetingHanis RusnipaNo ratings yet

- Profit Planning and Activity-Based Budgeting: Mcgraw-Hill/IrwinDocument50 pagesProfit Planning and Activity-Based Budgeting: Mcgraw-Hill/IrwinFlorensia RestianNo ratings yet

- Ac102 ch7Document22 pagesAc102 ch7Mohammed OsmanNo ratings yet

- Chapter 9: The Master Budget: Purpose of Budgets Planning and ControlDocument6 pagesChapter 9: The Master Budget: Purpose of Budgets Planning and ControlVivienne Rozenn LaytoNo ratings yet

- Chap07 Rev. FI5 Ex PR 1Document10 pagesChap07 Rev. FI5 Ex PR 1Beyond ThatNo ratings yet

- Final Exam - Sent StudentsDocument5 pagesFinal Exam - Sent StudentsTrần Nguyễn Tuệ MinhNo ratings yet

- Exercises 7A1 and 7B1: Book: Administrative AccountingDocument9 pagesExercises 7A1 and 7B1: Book: Administrative AccountingScribdTranslationsNo ratings yet

- Review Problem: Budget Schedules: RequiredDocument8 pagesReview Problem: Budget Schedules: RequiredShafa AlyaNo ratings yet

- This Study Resource Was: Problem Set 7 Budgeting Problem 1 (Garrison Et Al. v15 8-1)Document8 pagesThis Study Resource Was: Problem Set 7 Budgeting Problem 1 (Garrison Et Al. v15 8-1)NCT100% (1)

- Problem 20Document4 pagesProblem 20Kath Chu100% (1)

- Basic Operating BudgetDocument6 pagesBasic Operating BudgetalyNo ratings yet

- CHƯƠNG 1 - 10đ - 4Document5 pagesCHƯƠNG 1 - 10đ - 4Trần Khánh VyNo ratings yet

- Economic and Business Forecasting: Analyzing and Interpreting Econometric ResultsFrom EverandEconomic and Business Forecasting: Analyzing and Interpreting Econometric ResultsNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Unit 1Document26 pagesUnit 1kirosNo ratings yet

- Process CostingDocument20 pagesProcess CostingkirosNo ratings yet

- Interview Questions For HDPDocument2 pagesInterview Questions For HDPkirosNo ratings yet

- Unit 2Document22 pagesUnit 2kirosNo ratings yet

- Chapter 3 & 4 Flexible Vs Standards FullDocument17 pagesChapter 3 & 4 Flexible Vs Standards FullkirosNo ratings yet

- Course Breakdown For Extension Program PGDocument2 pagesCourse Breakdown For Extension Program PGkirosNo ratings yet

- CH4 - CH 6 Edited - 2013Document6 pagesCH4 - CH 6 Edited - 2013kirosNo ratings yet

- Chapter Five Decision Making and Relevant Information Information and The Decision ProcessDocument10 pagesChapter Five Decision Making and Relevant Information Information and The Decision ProcesskirosNo ratings yet

- Cost AccountingDocument14 pagesCost Accountingkiros100% (1)

- Stat ExamDocument5 pagesStat ExamkirosNo ratings yet

- RSB FinalDocument103 pagesRSB FinalKomal KorishettiNo ratings yet

- ZDC Act 2014 - FinalDocument17 pagesZDC Act 2014 - FinalBILAL KHANNo ratings yet

- 3.4 Final AccountsDocument114 pages3.4 Final AccountsMinh Thu NguyenNo ratings yet

- Istilah Istilah Ekonomi TeknikDocument6 pagesIstilah Istilah Ekonomi Teknikreza cakralNo ratings yet

- Financial AccountingDocument217 pagesFinancial AccountingGhalib HussainNo ratings yet

- Lecture 02Document42 pagesLecture 02CaraboNo ratings yet

- Entrepreneur Chapter 18Document6 pagesEntrepreneur Chapter 18CaladhielNo ratings yet

- Understanding Financial Statements, Taxes, and Cash Flows:, Prentice Hall, IncDocument50 pagesUnderstanding Financial Statements, Taxes, and Cash Flows:, Prentice Hall, IncYuslia Nandha Anasta SariNo ratings yet

- Chapter 3 Job Order CostingDocument26 pagesChapter 3 Job Order CostingwubeNo ratings yet

- The Following Figures Have Been Extracted From The Accounting RecordsDocument1 pageThe Following Figures Have Been Extracted From The Accounting RecordsHassan JanNo ratings yet

- Financial Statements PLDT and GLobeDocument18 pagesFinancial Statements PLDT and GLobeArnelli GregorioNo ratings yet

- Unit 1: Developing A Business PlanDocument50 pagesUnit 1: Developing A Business PlanLoren Cruz100% (1)

- Tax Lec 2Document14 pagesTax Lec 2Yousef Waleed100% (1)

- Chapter 5 The Business PlanDocument27 pagesChapter 5 The Business PlanLawrence MosizaNo ratings yet

- Chapter 15 - Solution ManualDocument55 pagesChapter 15 - Solution ManualMade Gita AnggrainiNo ratings yet

- Unit 4Document46 pagesUnit 4K.l.No ratings yet

- Its Earning That Count SummaryDocument115 pagesIts Earning That Count SummaryTheda VeldaNo ratings yet

- FAR MerchandisingDocument68 pagesFAR MerchandisingAira DavidNo ratings yet

- INGInsurance AnnualReport 2002Document61 pagesINGInsurance AnnualReport 2002Saurav HanswalNo ratings yet

- Exercise Books EthiopiaDocument23 pagesExercise Books EthiopiaDilip Kumar Ladwa100% (3)

- Project (IBM Nitu)Document85 pagesProject (IBM Nitu)Nandan JhaNo ratings yet

- DuPont Analysis Operating MethodDocument31 pagesDuPont Analysis Operating MethodAi Lin ChenNo ratings yet

- HSBC Annual Report 2010Document97 pagesHSBC Annual Report 2010Suchismita BhattacharjeeNo ratings yet

- Corporate Tax Planning & ManagemenDocument94 pagesCorporate Tax Planning & ManagemenArshit PatelNo ratings yet

- Chapter 2Document90 pagesChapter 2Sky walkingNo ratings yet

- Financial Analysis of Information and Technology Industry of India 2017Document17 pagesFinancial Analysis of Information and Technology Industry of India 2017Priyanka KumariNo ratings yet

- Job & Contract Costing NEPDocument8 pagesJob & Contract Costing NEPUnknown 1No ratings yet

- Suggested Answer CAP III June 2017 GIIDocument59 pagesSuggested Answer CAP III June 2017 GIIKimil TimilsinaNo ratings yet