Download as pdf or txt

You might also like

- Quiz 9 FinacrDocument9 pagesQuiz 9 FinacrJen Ner100% (5)

- Assignment Help Journal Ledger and MyodDocument9 pagesAssignment Help Journal Ledger and MyodrajeshNo ratings yet

- Ic s01 Survey and Loss AssessmentDocument55 pagesIc s01 Survey and Loss AssessmentRanjith50% (4)

- Tugas Variable Costing and The Measurement of ESG and Quality CostsDocument5 pagesTugas Variable Costing and The Measurement of ESG and Quality Costsirga ayudiasNo ratings yet

- 01 - FINC 0200 IP - Assignment Units 1 - 6 Questions - Winter 2022Document6 pages01 - FINC 0200 IP - Assignment Units 1 - 6 Questions - Winter 2022hermitpassiNo ratings yet

- Structure of The Examination PaperDocument12 pagesStructure of The Examination PaperRaffa MukoonNo ratings yet

- Far Quiz 2 Final W AnswersDocument6 pagesFar Quiz 2 Final W AnswersGia HipolitoNo ratings yet

- CH 4Document12 pagesCH 4Miftahudin Miftahudin0% (1)

- Activity #6Document20 pagesActivity #6JEWELL ANN PENARANDANo ratings yet

- Chapter 4: Adjusting The Accounts and Preparing The Financial StatementsDocument5 pagesChapter 4: Adjusting The Accounts and Preparing The Financial Statementschi_nguyen_100No ratings yet

- Accountancy I 2016 PDFDocument4 pagesAccountancy I 2016 PDFShahid RazwanNo ratings yet

- Accountancy and Auditing-2016 PDFDocument6 pagesAccountancy and Auditing-2016 PDFMian Abdullah YaseenNo ratings yet

- Solution - B124 - FTHE - V2 Summer 2020-2021 2 - V1Document13 pagesSolution - B124 - FTHE - V2 Summer 2020-2021 2 - V1AhmEd GhayasNo ratings yet

- Accountancy Auditing 2016Document7 pagesAccountancy Auditing 2016Abdul basitNo ratings yet

- ACC705 Corporate Accounting AssignmentDocument9 pagesACC705 Corporate Accounting AssignmentMuhammad AhsanNo ratings yet

- HI5020 Tutorial Question Assignment T3 2020 FinalDocument7 pagesHI5020 Tutorial Question Assignment T3 2020 FinalAamirNo ratings yet

- Unit 2 WorksheetDocument13 pagesUnit 2 WorksheetHhvvgg BbbbNo ratings yet

- 12 Accounts Imp ch10 PDFDocument14 pages12 Accounts Imp ch10 PDFmukesh kumarNo ratings yet

- Accounts HomeworkDocument9 pagesAccounts HomeworkSasha KingNo ratings yet

- QUIZ 9 fINACRDocument9 pagesQUIZ 9 fINACRJen NerNo ratings yet

- P3 Set 1-1Document5 pagesP3 Set 1-1Shingirayi MazingaizoNo ratings yet

- Book 2Document8 pagesBook 2May ManseNo ratings yet

- Name Roll No Program: Hamza Iqbal 2021-25-0001 Financial ManagementDocument9 pagesName Roll No Program: Hamza Iqbal 2021-25-0001 Financial ManagementHamza IqbalNo ratings yet

- Book 1Document14 pagesBook 1by ScribdNo ratings yet

- Soal Mojakoe-UTS Akuntansi Keuangan 1 Ganjil 2020-2021Document9 pagesSoal Mojakoe-UTS Akuntansi Keuangan 1 Ganjil 2020-2021Vincenttio le CloudNo ratings yet

- Group Assignment Account SEM1Document7 pagesGroup Assignment Account SEM1NUR LIEYANA BINTI MOHD SHUKOR MoeNo ratings yet

- 4 Completing The Accounting Cycle PartDocument1 page4 Completing The Accounting Cycle PartTalionNo ratings yet

- Dissolution of Partnership - Question 1Document16 pagesDissolution of Partnership - Question 1anthony hoNo ratings yet

- Past Exam QuestionDocument3 pagesPast Exam QuestionYến Hoàng HảiNo ratings yet

- Intermediate Accounting 3 Second Grading Quiz: Name: Date: Professor: Section: ScoreDocument2 pagesIntermediate Accounting 3 Second Grading Quiz: Name: Date: Professor: Section: ScoreGrezel NiceNo ratings yet

- Short-Term ExamDocument6 pagesShort-Term Examymkuzangwe16No ratings yet

- AfB1 Tutorial Questions For Week 3Document3 pagesAfB1 Tutorial Questions For Week 3zhaok0610No ratings yet

- Bacc210 Assig 1Document6 pagesBacc210 Assig 1TarusengaNo ratings yet

- FABM 2 HANDOUTS 1st QRTRDocument17 pagesFABM 2 HANDOUTS 1st QRTRDanise PorrasNo ratings yet

- ACCT1200 (20) Additional P&L Account and Balance Sheet QuestionDocument2 pagesACCT1200 (20) Additional P&L Account and Balance Sheet QuestionTaleh HasanzadaNo ratings yet

- Final ReviewDocument53 pagesFinal ReviewLalalaNo ratings yet

- CA IPCCAccounting314081 PDFDocument17 pagesCA IPCCAccounting314081 PDFJanhvi AroraNo ratings yet

- Adjusting Entries: Q1: Pass The Necessary Adjusting Entries For The FollowingDocument9 pagesAdjusting Entries: Q1: Pass The Necessary Adjusting Entries For The FollowingHassan AliNo ratings yet

- Homework 2Document2 pagesHomework 2Sudeep0% (1)

- Tutorial 23 Financial Statement 1 2 Management SkillsDocument4 pagesTutorial 23 Financial Statement 1 2 Management SkillsOkgar Myint SoeNo ratings yet

- Homework 4題目Document2 pagesHomework 4題目劉百祥No ratings yet

- Financial PositionDocument4 pagesFinancial PositionBeth Diaz Laurente100% (2)

- M.B.A (2019 Pattern)Document157 pagesM.B.A (2019 Pattern)girishpawarudgirkarNo ratings yet

- SdsasacsacsacsacsacDocument4 pagesSdsasacsacsacsacsacIden PratamaNo ratings yet

- Company Final Accounts: Debit Rs. Credit RsDocument5 pagesCompany Final Accounts: Debit Rs. Credit RsDebaditya SenguptaNo ratings yet

- PGDM (2021-23) Exercise On Final AccountsDocument9 pagesPGDM (2021-23) Exercise On Final Accountspriyanshu guptaNo ratings yet

- 2019-06 ICMAB FL 001 PAC Year Question JUNE 2019Document3 pages2019-06 ICMAB FL 001 PAC Year Question JUNE 2019Mohammad ShahidNo ratings yet

- Accounting For Finance: Eric Cauvin Exercises 2Document6 pagesAccounting For Finance: Eric Cauvin Exercises 2ddd huangNo ratings yet

- Class Test Accountancy 11 JanDocument2 pagesClass Test Accountancy 11 Jansara VermaNo ratings yet

- Model Paper AnswersDocument12 pagesModel Paper AnswersShenali NupehewaNo ratings yet

- Corporate Final Accounts With AdjustmentsDocument6 pagesCorporate Final Accounts With AdjustmentsNeelu AggrawalNo ratings yet

- MOJAKOE AK1 UTS 2012 GasalDocument15 pagesMOJAKOE AK1 UTS 2012 GasalVincenttio le CloudNo ratings yet

- Tutorial QuestionsDocument2 pagesTutorial QuestionsNishika KaranNo ratings yet

- Project Corporate AccountingDocument2 pagesProject Corporate AccountingARATFTAFTNo ratings yet

- FA1 Financial StatementsDocument5 pagesFA1 Financial StatementsamirNo ratings yet

- Mid Sem 1sem Exam Paper Oct2015Document26 pagesMid Sem 1sem Exam Paper Oct2015angel100% (1)

- Arab Final 90% Fall2021 (YS)Document8 pagesArab Final 90% Fall2021 (YS)ahmed abuzedNo ratings yet

- Mock ExamDocument4 pagesMock ExamAna-Maria GhNo ratings yet

- Fundamentals of Corporate Finance 6th Edition Christensen Solutions ManualDocument6 pagesFundamentals of Corporate Finance 6th Edition Christensen Solutions ManualJamesOrtegapfcs100% (66)

- W4 - SW1 - Statement of Financial PositionDocument2 pagesW4 - SW1 - Statement of Financial PositionJere Mae MarananNo ratings yet

- Finalterm Examination: Unfair Means in Completing ItDocument4 pagesFinalterm Examination: Unfair Means in Completing ItMuhammad Abdullah SaniNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- SS 2 Store MGT Third Term E-Learning NoteDocument38 pagesSS 2 Store MGT Third Term E-Learning Notepalmer okiemuteNo ratings yet

- CBSE 2015 Syllabus 12 Accountancy NewDocument5 pagesCBSE 2015 Syllabus 12 Accountancy NewAdil AliNo ratings yet

- A Project On Funds Flow Ststements 2016 in HeritageDocument61 pagesA Project On Funds Flow Ststements 2016 in Heritagevishnupriya100% (1)

- ch04Document76 pagesch04Margareta Jessica NathaniaNo ratings yet

- Intermediate Accounting Stice Stice SkousenDocument58 pagesIntermediate Accounting Stice Stice SkousenTornike Jashi100% (1)

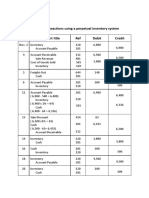

- Group 1: A) Journalize The Transactions Using A Perpetual Inventory System Date Account Title Ref Debit CreditDocument6 pagesGroup 1: A) Journalize The Transactions Using A Perpetual Inventory System Date Account Title Ref Debit CreditQuỳnh'ss Đắc'ssNo ratings yet

- G.O. (MS) No.112 Dated: 22.06.2017 Naés à Tul, Må 08Document76 pagesG.O. (MS) No.112 Dated: 22.06.2017 Naés à Tul, Må 08Natchimuthu KannanNo ratings yet

- 17 Financial Statements (With Adjustments)Document16 pages17 Financial Statements (With Adjustments)Dayaan ANo ratings yet

- Finance and Accounting Lecture 4Document47 pagesFinance and Accounting Lecture 4Mustafa MoatamedNo ratings yet

- Presentation1 ReshmaDocument26 pagesPresentation1 ReshmaJOE NOBLE 2020519No ratings yet

- ACCT1002 - Introduction To Financial Accounting Assignment # 2 Page - 1Document21 pagesACCT1002 - Introduction To Financial Accounting Assignment # 2 Page - 1MingxNo ratings yet

- Financial Ratio Analysis Case StudyDocument10 pagesFinancial Ratio Analysis Case StudyGracel Joy VicenteNo ratings yet

- Shalini Chaurasia, Voyage Accounting, M. Com. Sem.-Iii, Advance AccountingDocument5 pagesShalini Chaurasia, Voyage Accounting, M. Com. Sem.-Iii, Advance AccountingRitik SankarNo ratings yet

- Exercises of Accounting N PDocument34 pagesExercises of Accounting N PVan caothaiNo ratings yet

- Acc 223a CH 5 AnswersDocument13 pagesAcc 223a CH 5 Answersjr centenoNo ratings yet

- 11 Chapter 3 (Working Capital Aspects)Document30 pages11 Chapter 3 (Working Capital Aspects)Abin VargheseNo ratings yet

- Test Bank Advanced Accounting 3e by Jeter 07 ChapterDocument18 pagesTest Bank Advanced Accounting 3e by Jeter 07 ChapterNicolas ErnestoNo ratings yet

- Prepare An Income Statements and A Balance Sheet: Senior High School DepartmentDocument10 pagesPrepare An Income Statements and A Balance Sheet: Senior High School DepartmentAira Mae PazNo ratings yet

- Final Accounts With Case Solution & Dindorf SolutionDocument39 pagesFinal Accounts With Case Solution & Dindorf SolutionAnkit kumarNo ratings yet

- Solution Performa - Mamta FashionsDocument3 pagesSolution Performa - Mamta FashionsGarimaBhandariNo ratings yet

- Ia3 - Chapter 1Document8 pagesIa3 - Chapter 1chesca marie penarandaNo ratings yet

- Cash Flow Statement New For YoutubeDocument48 pagesCash Flow Statement New For YoutubeTapan BarikNo ratings yet

- Annexure II CP 14-13-14 PDFDocument381 pagesAnnexure II CP 14-13-14 PDFவேணிNo ratings yet

- Singapore GamingDocument12 pagesSingapore GamingJunyuanNo ratings yet

- AUVZSFDocument7 pagesAUVZSFnareeshkumar_koppalaNo ratings yet

- Income Statement and Related Information: Chapter Learning ObjectivesDocument52 pagesIncome Statement and Related Information: Chapter Learning ObjectivesIvern BautistaNo ratings yet

- SITXFIN004 Prepare and Monitorassessment 1 - Short Answer Questions v2.2Document7 pagesSITXFIN004 Prepare and Monitorassessment 1 - Short Answer Questions v2.2Tongshuo Liu0% (1)