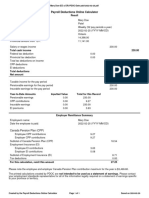

Model-Place 01012014

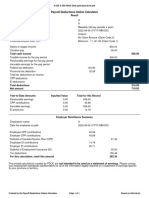

Model-Place 01012014

You might also like

- How To Pay Property TaxesDocument1 pageHow To Pay Property Taxesapi-1973110992% (60)

- ACCA F6 - Trading Profit AdjustmentDocument2 pagesACCA F6 - Trading Profit AdjustmentIftekhar Ifte100% (1)

- Amended Tax Credit Certificate 2020 7243210862511Document2 pagesAmended Tax Credit Certificate 2020 7243210862511Aurimas AurisNo ratings yet

- Minimum Salary in Romania (2023)Document1 pageMinimum Salary in Romania (2023)CALLISTAR GROUPNo ratings yet

- Model-Place 01012014Document3 pagesModel-Place 01012014senahidNo ratings yet

- Prudential Life Assurance Page 1 of 2 (Date Printed: 09-Oct-2019)Document2 pagesPrudential Life Assurance Page 1 of 2 (Date Printed: 09-Oct-2019)KomalaNo ratings yet

- UntitledDocument2 pagesUntitledMichael deMonetNo ratings yet

- Mary Doe - (EE & ER) - PDOC-Date Paid-2022-02-25Document1 pageMary Doe - (EE & ER) - PDOC-Date Paid-2022-02-25rahul_ransureNo ratings yet

- Prudential Life Assurance Page 1 of 2 (Date Printed: 09-Oct-2019)Document2 pagesPrudential Life Assurance Page 1 of 2 (Date Printed: 09-Oct-2019)KomalaNo ratings yet

- Month Net Taxable Income Tax Slabs Tax RateDocument2 pagesMonth Net Taxable Income Tax Slabs Tax RateBhargav ChintalapatiNo ratings yet

- Income Tax Projection202206Document1 pageIncome Tax Projection202206Rakhi JadavNo ratings yet

- Tax LawsDocument7 pagesTax Lawsbesong marlonNo ratings yet

- PayslipsDocument6 pagesPayslipsbskapoor68No ratings yet

- Prudential Life Assurance Page 1 of 2 (Date Printed: 16-Jul-2019)Document2 pagesPrudential Life Assurance Page 1 of 2 (Date Printed: 16-Jul-2019)KomalaNo ratings yet

- Tax PlanningDocument16 pagesTax PlanningNaresh ParmarNo ratings yet

- April 2023 - UnlockedDocument2 pagesApril 2023 - Unlockedajinkya jagtapNo ratings yet

- Employee Name - (EE & ER) - PDOC-Date Paid-2023-02-26Document1 pageEmployee Name - (EE & ER) - PDOC-Date Paid-2023-02-26William JoeNo ratings yet

- Ratio Model - Kannan DBADocument6 pagesRatio Model - Kannan DBAnabil.shaikhNo ratings yet

- JAN Payslip India-UnlockedDocument2 pagesJAN Payslip India-Unlockedbskapoor68No ratings yet

- Consolidated Statement of Profit and LossDocument9 pagesConsolidated Statement of Profit and LossHrushikesh DahaleNo ratings yet

- Declaration 3310586406613Document4 pagesDeclaration 3310586406613Muhammad WaqasNo ratings yet

- Graphical Model For Financial Simulation of Highway PPP ProjectsDocument5 pagesGraphical Model For Financial Simulation of Highway PPP ProjectsRisyda UmmamiNo ratings yet

- Faq'S & Guidlines On Income TaxDocument50 pagesFaq'S & Guidlines On Income TaxRavikarthik GurumurthyNo ratings yet

- Employee Informa On: 22856 Joseph Mathew Officer Kozhikode/ MalaparambaDocument1 pageEmployee Informa On: 22856 Joseph Mathew Officer Kozhikode/ Malaparambadilna dvdNo ratings yet

- 2019 Declaration PDFDocument4 pages2019 Declaration PDFIkramNo ratings yet

- Tax Calculator 2018-19 (Farrukh Iqbal Khan)Document2 pagesTax Calculator 2018-19 (Farrukh Iqbal Khan)FarrukhNo ratings yet

- Employee Name - (EE & ER) - PDOC-Date Paid-2024-03-28Document2 pagesEmployee Name - (EE & ER) - PDOC-Date Paid-2024-03-28RileyNo ratings yet

- Tax System in BangladeshDocument6 pagesTax System in BangladeshNahid Hussain AdriNo ratings yet

- Draft Return For ReviewDocument4 pagesDraft Return For ReviewsajjadNo ratings yet

- Candy Simpson - (EE & ER) - PDOC-Date Paid-2020-12-12 (WEEK 2)Document1 pageCandy Simpson - (EE & ER) - PDOC-Date Paid-2020-12-12 (WEEK 2)mcocampo2No ratings yet

- YdryDocument2 pagesYdryVinodhkumar Shanmugam100% (2)

- PDF&Rendition 1Document2 pagesPDF&Rendition 1vijaybhaskar damireddyNo ratings yet

- Tax ReturnDocument3 pagesTax ReturnUsam UlhaqNo ratings yet

- Kahuta, District Kahuta, Pakistan Muhammad Mohsin Razzaq: Mon, 7 Dec 2020 21:17:28 +0500Document3 pagesKahuta, District Kahuta, Pakistan Muhammad Mohsin Razzaq: Mon, 7 Dec 2020 21:17:28 +0500Asif ShahzadNo ratings yet

- Sinothando PaylsipDocument1 pageSinothando PaylsipsinothandodekedaNo ratings yet

- It 2023 2024 7Document2 pagesIt 2023 2024 7luciferangellordNo ratings yet

- Payslip IndiaApproved On30 Nov 2023 - UnlockedDocument3 pagesPayslip IndiaApproved On30 Nov 2023 - UnlockedrithulblockchainNo ratings yet

- Kashana Hafiz Mir Colony Near Petrol PUMP LILYANI 0492450277 Khalil Ahmad ShakirDocument4 pagesKashana Hafiz Mir Colony Near Petrol PUMP LILYANI 0492450277 Khalil Ahmad ShakirKhalil ShakirNo ratings yet

- Form 16 - BLMPB2218K - 2019-20 - Part B PDFDocument6 pagesForm 16 - BLMPB2218K - 2019-20 - Part B PDFUmair BaigNo ratings yet

- Azreaal: Eqe WD Raipur Chhattisgarh 492007 IndiaDocument2 pagesAzreaal: Eqe WD Raipur Chhattisgarh 492007 IndiaAditya AgrawalNo ratings yet

- 22Document2 pages22TWCNo ratings yet

- Declaration 1610111025693Document3 pagesDeclaration 1610111025693Muhammad Aamir AbbasNo ratings yet

- Mahnia Wala Chak No 190 JB Post Office Khas Tehsil Chiniot Distt Muhammad Saleem Raza ShahDocument4 pagesMahnia Wala Chak No 190 JB Post Office Khas Tehsil Chiniot Distt Muhammad Saleem Raza ShahMUHAMMAD SALEEM RAZANo ratings yet

- Salary Slip EDIT-AUGDocument4 pagesSalary Slip EDIT-AUGpathyashisNo ratings yet

- Declaration4220102804067 PDFDocument5 pagesDeclaration4220102804067 PDFIkramNo ratings yet

- Acct312 07032020Document2 pagesAcct312 07032020KELLY DANGNo ratings yet

- Jul 2022Document2 pagesJul 2022Nikhil KumarNo ratings yet

- Sre Opol Q4 2022Document6 pagesSre Opol Q4 2022Mia ActubNo ratings yet

- HBT LiftDocument3 pagesHBT Liftakcabhay9No ratings yet

- Salary Slip EDIT-JULYDocument4 pagesSalary Slip EDIT-JULYpathyashisNo ratings yet

- Street Sheikh Gulab Din Wali, Muhalla Islamabad Mohsin Razi: Wed, 5 May 2021 13:55:14 +0500Document4 pagesStreet Sheikh Gulab Din Wali, Muhalla Islamabad Mohsin Razi: Wed, 5 May 2021 13:55:14 +0500Sadiq SonsNo ratings yet

- A - (EE & ER) - PDOC-Date Paid-2022-08-05Document1 pageA - (EE & ER) - PDOC-Date Paid-2022-08-05armanf2020zNo ratings yet

- NON MEDICLAIM AY2024-25 SARBANI BORA-BDPPB0721G-ComputationDocument2 pagesNON MEDICLAIM AY2024-25 SARBANI BORA-BDPPB0721G-ComputationlaskarmohinNo ratings yet

- NL Ec LS 400 6Document1 pageNL Ec LS 400 6Gladys CasarrubiasNo ratings yet

- Sre Opol Q4 2022Document6 pagesSre Opol Q4 2022Mia ActubNo ratings yet

- Formal Letter of Demand: Republic of The Philippines Department of Finance Bureau of Internal RevenueDocument3 pagesFormal Letter of Demand: Republic of The Philippines Department of Finance Bureau of Internal RevenueDominic Dela VegaNo ratings yet

- Declaration 3130333240279Document6 pagesDeclaration 3130333240279haunted houseNo ratings yet

- Payslip Jul2023 EDU - 01098Document1 pagePayslip Jul2023 EDU - 01098PrabhuNo ratings yet

- Lucrul-Individual-Finante - MIDGARD TERRA S.A. MoldovaDocument16 pagesLucrul-Individual-Finante - MIDGARD TERRA S.A. MoldovaTrifan_DumitruNo ratings yet

- Vat Summary-30-09-2010Document2 pagesVat Summary-30-09-2010anon_978060No ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- GST Registration Procedure and FAQsDocument21 pagesGST Registration Procedure and FAQsSahil KumarNo ratings yet

- Old - AOP - Complete Study PDFDocument8 pagesOld - AOP - Complete Study PDFSwathi JainNo ratings yet

- How The Super Rich Avoid Paying TaxesDocument8 pagesHow The Super Rich Avoid Paying TaxeshortelNo ratings yet

- ReportDocument2 pagesReportnag85No ratings yet

- Islamabad Electric Supply Company - Electricity Consumer Bill (Mdi)Document1 pageIslamabad Electric Supply Company - Electricity Consumer Bill (Mdi)sufyan khursheedNo ratings yet

- SMBR - Offering Letter (Rizal Yon Aulia)Document3 pagesSMBR - Offering Letter (Rizal Yon Aulia)RaffaIlhamNo ratings yet

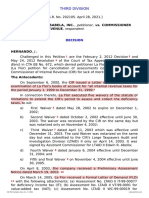

- La Flor Dela Isabela, Inc. v. CIR (2021)Document17 pagesLa Flor Dela Isabela, Inc. v. CIR (2021)Lyn Jeen BinuaNo ratings yet

- Suggested Answer To Q1Document6 pagesSuggested Answer To Q1KY LawNo ratings yet

- Multiplier Effect ExplanationDocument5 pagesMultiplier Effect Explanationfreaky mintyNo ratings yet

- NPS Calculator Free Download ExcelDocument7 pagesNPS Calculator Free Download Excelsambhavjoshi100% (1)

- Essay On The Financial Relationship Between Centre and State - OdtDocument5 pagesEssay On The Financial Relationship Between Centre and State - OdtchanshrNo ratings yet

- List of Bir FormsDocument26 pagesList of Bir FormsAviaNo ratings yet

- InvoiceDocument1 pageInvoice10-XII-Sci-A Saima ChoudharyNo ratings yet

- 3) Howden Vs CIRDocument2 pages3) Howden Vs CIRjoyceNo ratings yet

- 23072600198046KVBL ChallanReceiptDocument2 pages23072600198046KVBL ChallanReceiptNaveen SNo ratings yet

- Assessment 1 - Written or Oral QuestionsDocument7 pagesAssessment 1 - Written or Oral Questionswilson garzonNo ratings yet

- IntxDocument6 pagesIntxSophia KeratinNo ratings yet

- Dead Person Mass of Property Left by Dead Person: NO Estate Is Not A Tax On Person or Personal TaxDocument3 pagesDead Person Mass of Property Left by Dead Person: NO Estate Is Not A Tax On Person or Personal TaxAbraham ChinNo ratings yet

- TCS On Sale of Goods: Padmanathan K V, Chartered AccountantDocument20 pagesTCS On Sale of Goods: Padmanathan K V, Chartered AccountantSainaath RNo ratings yet

- The Employees' Pension Scheme, 1995: (For Exempted Establishments Only)Document1 pageThe Employees' Pension Scheme, 1995: (For Exempted Establishments Only)Avengers endgameNo ratings yet

- Glacier Tax User GuideDocument5 pagesGlacier Tax User Guideinter4ever77No ratings yet

- Taxation PresentationDocument10 pagesTaxation Presentationmhilet_chiNo ratings yet

- Salary Slip July'09Document1 pageSalary Slip July'09Erin HamiltonNo ratings yet

- VAT Vs NonVATDocument3 pagesVAT Vs NonVATMary Dale Joie BocalaNo ratings yet

- Revenue Memorandum Circular No. 07-94Document2 pagesRevenue Memorandum Circular No. 07-94Lance MorilloNo ratings yet

- Income Tax MCQ With Answers PDFDocument19 pagesIncome Tax MCQ With Answers PDFAman Pandit100% (1)

- Gcin901337274co2020000000006266 PDFDocument1 pageGcin901337274co2020000000006266 PDFjccb1980No ratings yet

- Authority To Sell - DraftDocument2 pagesAuthority To Sell - DraftJed Daet100% (3)

Download as xls, pdf, or txt

You might also like

- How To Pay Property TaxesDocument1 pageHow To Pay Property Taxesapi-1973110992% (60)

- ACCA F6 - Trading Profit AdjustmentDocument2 pagesACCA F6 - Trading Profit AdjustmentIftekhar Ifte100% (1)

- Amended Tax Credit Certificate 2020 7243210862511Document2 pagesAmended Tax Credit Certificate 2020 7243210862511Aurimas AurisNo ratings yet

- Minimum Salary in Romania (2023)Document1 pageMinimum Salary in Romania (2023)CALLISTAR GROUPNo ratings yet

- Model-Place 01012014Document3 pagesModel-Place 01012014senahidNo ratings yet

- Prudential Life Assurance Page 1 of 2 (Date Printed: 09-Oct-2019)Document2 pagesPrudential Life Assurance Page 1 of 2 (Date Printed: 09-Oct-2019)KomalaNo ratings yet

- UntitledDocument2 pagesUntitledMichael deMonetNo ratings yet

- Mary Doe - (EE & ER) - PDOC-Date Paid-2022-02-25Document1 pageMary Doe - (EE & ER) - PDOC-Date Paid-2022-02-25rahul_ransureNo ratings yet

- Prudential Life Assurance Page 1 of 2 (Date Printed: 09-Oct-2019)Document2 pagesPrudential Life Assurance Page 1 of 2 (Date Printed: 09-Oct-2019)KomalaNo ratings yet

- Month Net Taxable Income Tax Slabs Tax RateDocument2 pagesMonth Net Taxable Income Tax Slabs Tax RateBhargav ChintalapatiNo ratings yet

- Income Tax Projection202206Document1 pageIncome Tax Projection202206Rakhi JadavNo ratings yet

- Tax LawsDocument7 pagesTax Lawsbesong marlonNo ratings yet

- PayslipsDocument6 pagesPayslipsbskapoor68No ratings yet

- Prudential Life Assurance Page 1 of 2 (Date Printed: 16-Jul-2019)Document2 pagesPrudential Life Assurance Page 1 of 2 (Date Printed: 16-Jul-2019)KomalaNo ratings yet

- Tax PlanningDocument16 pagesTax PlanningNaresh ParmarNo ratings yet

- April 2023 - UnlockedDocument2 pagesApril 2023 - Unlockedajinkya jagtapNo ratings yet

- Employee Name - (EE & ER) - PDOC-Date Paid-2023-02-26Document1 pageEmployee Name - (EE & ER) - PDOC-Date Paid-2023-02-26William JoeNo ratings yet

- Ratio Model - Kannan DBADocument6 pagesRatio Model - Kannan DBAnabil.shaikhNo ratings yet

- JAN Payslip India-UnlockedDocument2 pagesJAN Payslip India-Unlockedbskapoor68No ratings yet

- Consolidated Statement of Profit and LossDocument9 pagesConsolidated Statement of Profit and LossHrushikesh DahaleNo ratings yet

- Declaration 3310586406613Document4 pagesDeclaration 3310586406613Muhammad WaqasNo ratings yet

- Graphical Model For Financial Simulation of Highway PPP ProjectsDocument5 pagesGraphical Model For Financial Simulation of Highway PPP ProjectsRisyda UmmamiNo ratings yet

- Faq'S & Guidlines On Income TaxDocument50 pagesFaq'S & Guidlines On Income TaxRavikarthik GurumurthyNo ratings yet

- Employee Informa On: 22856 Joseph Mathew Officer Kozhikode/ MalaparambaDocument1 pageEmployee Informa On: 22856 Joseph Mathew Officer Kozhikode/ Malaparambadilna dvdNo ratings yet

- 2019 Declaration PDFDocument4 pages2019 Declaration PDFIkramNo ratings yet

- Tax Calculator 2018-19 (Farrukh Iqbal Khan)Document2 pagesTax Calculator 2018-19 (Farrukh Iqbal Khan)FarrukhNo ratings yet

- Employee Name - (EE & ER) - PDOC-Date Paid-2024-03-28Document2 pagesEmployee Name - (EE & ER) - PDOC-Date Paid-2024-03-28RileyNo ratings yet

- Tax System in BangladeshDocument6 pagesTax System in BangladeshNahid Hussain AdriNo ratings yet

- Draft Return For ReviewDocument4 pagesDraft Return For ReviewsajjadNo ratings yet

- Candy Simpson - (EE & ER) - PDOC-Date Paid-2020-12-12 (WEEK 2)Document1 pageCandy Simpson - (EE & ER) - PDOC-Date Paid-2020-12-12 (WEEK 2)mcocampo2No ratings yet

- YdryDocument2 pagesYdryVinodhkumar Shanmugam100% (2)

- PDF&Rendition 1Document2 pagesPDF&Rendition 1vijaybhaskar damireddyNo ratings yet

- Tax ReturnDocument3 pagesTax ReturnUsam UlhaqNo ratings yet

- Kahuta, District Kahuta, Pakistan Muhammad Mohsin Razzaq: Mon, 7 Dec 2020 21:17:28 +0500Document3 pagesKahuta, District Kahuta, Pakistan Muhammad Mohsin Razzaq: Mon, 7 Dec 2020 21:17:28 +0500Asif ShahzadNo ratings yet

- Sinothando PaylsipDocument1 pageSinothando PaylsipsinothandodekedaNo ratings yet

- It 2023 2024 7Document2 pagesIt 2023 2024 7luciferangellordNo ratings yet

- Payslip IndiaApproved On30 Nov 2023 - UnlockedDocument3 pagesPayslip IndiaApproved On30 Nov 2023 - UnlockedrithulblockchainNo ratings yet

- Kashana Hafiz Mir Colony Near Petrol PUMP LILYANI 0492450277 Khalil Ahmad ShakirDocument4 pagesKashana Hafiz Mir Colony Near Petrol PUMP LILYANI 0492450277 Khalil Ahmad ShakirKhalil ShakirNo ratings yet

- Form 16 - BLMPB2218K - 2019-20 - Part B PDFDocument6 pagesForm 16 - BLMPB2218K - 2019-20 - Part B PDFUmair BaigNo ratings yet

- Azreaal: Eqe WD Raipur Chhattisgarh 492007 IndiaDocument2 pagesAzreaal: Eqe WD Raipur Chhattisgarh 492007 IndiaAditya AgrawalNo ratings yet

- 22Document2 pages22TWCNo ratings yet

- Declaration 1610111025693Document3 pagesDeclaration 1610111025693Muhammad Aamir AbbasNo ratings yet

- Mahnia Wala Chak No 190 JB Post Office Khas Tehsil Chiniot Distt Muhammad Saleem Raza ShahDocument4 pagesMahnia Wala Chak No 190 JB Post Office Khas Tehsil Chiniot Distt Muhammad Saleem Raza ShahMUHAMMAD SALEEM RAZANo ratings yet

- Salary Slip EDIT-AUGDocument4 pagesSalary Slip EDIT-AUGpathyashisNo ratings yet

- Declaration4220102804067 PDFDocument5 pagesDeclaration4220102804067 PDFIkramNo ratings yet

- Acct312 07032020Document2 pagesAcct312 07032020KELLY DANGNo ratings yet

- Jul 2022Document2 pagesJul 2022Nikhil KumarNo ratings yet

- Sre Opol Q4 2022Document6 pagesSre Opol Q4 2022Mia ActubNo ratings yet

- HBT LiftDocument3 pagesHBT Liftakcabhay9No ratings yet

- Salary Slip EDIT-JULYDocument4 pagesSalary Slip EDIT-JULYpathyashisNo ratings yet

- Street Sheikh Gulab Din Wali, Muhalla Islamabad Mohsin Razi: Wed, 5 May 2021 13:55:14 +0500Document4 pagesStreet Sheikh Gulab Din Wali, Muhalla Islamabad Mohsin Razi: Wed, 5 May 2021 13:55:14 +0500Sadiq SonsNo ratings yet

- A - (EE & ER) - PDOC-Date Paid-2022-08-05Document1 pageA - (EE & ER) - PDOC-Date Paid-2022-08-05armanf2020zNo ratings yet

- NON MEDICLAIM AY2024-25 SARBANI BORA-BDPPB0721G-ComputationDocument2 pagesNON MEDICLAIM AY2024-25 SARBANI BORA-BDPPB0721G-ComputationlaskarmohinNo ratings yet

- NL Ec LS 400 6Document1 pageNL Ec LS 400 6Gladys CasarrubiasNo ratings yet

- Sre Opol Q4 2022Document6 pagesSre Opol Q4 2022Mia ActubNo ratings yet

- Formal Letter of Demand: Republic of The Philippines Department of Finance Bureau of Internal RevenueDocument3 pagesFormal Letter of Demand: Republic of The Philippines Department of Finance Bureau of Internal RevenueDominic Dela VegaNo ratings yet

- Declaration 3130333240279Document6 pagesDeclaration 3130333240279haunted houseNo ratings yet

- Payslip Jul2023 EDU - 01098Document1 pagePayslip Jul2023 EDU - 01098PrabhuNo ratings yet

- Lucrul-Individual-Finante - MIDGARD TERRA S.A. MoldovaDocument16 pagesLucrul-Individual-Finante - MIDGARD TERRA S.A. MoldovaTrifan_DumitruNo ratings yet

- Vat Summary-30-09-2010Document2 pagesVat Summary-30-09-2010anon_978060No ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- GST Registration Procedure and FAQsDocument21 pagesGST Registration Procedure and FAQsSahil KumarNo ratings yet

- Old - AOP - Complete Study PDFDocument8 pagesOld - AOP - Complete Study PDFSwathi JainNo ratings yet

- How The Super Rich Avoid Paying TaxesDocument8 pagesHow The Super Rich Avoid Paying TaxeshortelNo ratings yet

- ReportDocument2 pagesReportnag85No ratings yet

- Islamabad Electric Supply Company - Electricity Consumer Bill (Mdi)Document1 pageIslamabad Electric Supply Company - Electricity Consumer Bill (Mdi)sufyan khursheedNo ratings yet

- SMBR - Offering Letter (Rizal Yon Aulia)Document3 pagesSMBR - Offering Letter (Rizal Yon Aulia)RaffaIlhamNo ratings yet

- La Flor Dela Isabela, Inc. v. CIR (2021)Document17 pagesLa Flor Dela Isabela, Inc. v. CIR (2021)Lyn Jeen BinuaNo ratings yet

- Suggested Answer To Q1Document6 pagesSuggested Answer To Q1KY LawNo ratings yet

- Multiplier Effect ExplanationDocument5 pagesMultiplier Effect Explanationfreaky mintyNo ratings yet

- NPS Calculator Free Download ExcelDocument7 pagesNPS Calculator Free Download Excelsambhavjoshi100% (1)

- Essay On The Financial Relationship Between Centre and State - OdtDocument5 pagesEssay On The Financial Relationship Between Centre and State - OdtchanshrNo ratings yet

- List of Bir FormsDocument26 pagesList of Bir FormsAviaNo ratings yet

- InvoiceDocument1 pageInvoice10-XII-Sci-A Saima ChoudharyNo ratings yet

- 3) Howden Vs CIRDocument2 pages3) Howden Vs CIRjoyceNo ratings yet

- 23072600198046KVBL ChallanReceiptDocument2 pages23072600198046KVBL ChallanReceiptNaveen SNo ratings yet

- Assessment 1 - Written or Oral QuestionsDocument7 pagesAssessment 1 - Written or Oral Questionswilson garzonNo ratings yet

- IntxDocument6 pagesIntxSophia KeratinNo ratings yet

- Dead Person Mass of Property Left by Dead Person: NO Estate Is Not A Tax On Person or Personal TaxDocument3 pagesDead Person Mass of Property Left by Dead Person: NO Estate Is Not A Tax On Person or Personal TaxAbraham ChinNo ratings yet

- TCS On Sale of Goods: Padmanathan K V, Chartered AccountantDocument20 pagesTCS On Sale of Goods: Padmanathan K V, Chartered AccountantSainaath RNo ratings yet

- The Employees' Pension Scheme, 1995: (For Exempted Establishments Only)Document1 pageThe Employees' Pension Scheme, 1995: (For Exempted Establishments Only)Avengers endgameNo ratings yet

- Glacier Tax User GuideDocument5 pagesGlacier Tax User Guideinter4ever77No ratings yet

- Taxation PresentationDocument10 pagesTaxation Presentationmhilet_chiNo ratings yet

- Salary Slip July'09Document1 pageSalary Slip July'09Erin HamiltonNo ratings yet

- VAT Vs NonVATDocument3 pagesVAT Vs NonVATMary Dale Joie BocalaNo ratings yet

- Revenue Memorandum Circular No. 07-94Document2 pagesRevenue Memorandum Circular No. 07-94Lance MorilloNo ratings yet

- Income Tax MCQ With Answers PDFDocument19 pagesIncome Tax MCQ With Answers PDFAman Pandit100% (1)

- Gcin901337274co2020000000006266 PDFDocument1 pageGcin901337274co2020000000006266 PDFjccb1980No ratings yet

- Authority To Sell - DraftDocument2 pagesAuthority To Sell - DraftJed Daet100% (3)