Download as pdf or txt

You might also like

- Anne Sliwka - Alternative EducationDocument14 pagesAnne Sliwka - Alternative EducationTheKidLocoNo ratings yet

- On The Path To Innovation AnaDocument26 pagesOn The Path To Innovation Anathe kusumasNo ratings yet

- Advantages and Disadvantages of Digitalisation in AccountingDocument6 pagesAdvantages and Disadvantages of Digitalisation in AccountingHannoun NouhailaNo ratings yet

- Technology Changes and The Impact On AccDocument331 pagesTechnology Changes and The Impact On AccsahilNo ratings yet

- The Acceptance of Information Technology by The Accounting AreaDocument10 pagesThe Acceptance of Information Technology by The Accounting AreaerwinNo ratings yet

- Montecalvolopez Final PaperDocument30 pagesMontecalvolopez Final PaperMa. Trina AnotnioNo ratings yet

- Informatics 09 00019Document17 pagesInformatics 09 00019nqa1994No ratings yet

- Leno Oliveira - 51688042 - UpdatedDocument10 pagesLeno Oliveira - 51688042 - UpdatedLeno OliveiraNo ratings yet

- Accounting 2020Document10 pagesAccounting 2020Leno OliveiraNo ratings yet

- Research - Edited2 - FINALDocument67 pagesResearch - Edited2 - FINALDonna AbogadoNo ratings yet

- How Digital Technologies Are Transforming Financial Sector?: Organizational AgilityDocument2 pagesHow Digital Technologies Are Transforming Financial Sector?: Organizational AgilityBibinsNo ratings yet

- Accounting Automation and The Future of The AccounDocument17 pagesAccounting Automation and The Future of The Accounareveral.dvconsultingNo ratings yet

- Claves para La Transformación Digital de Las PymesDocument14 pagesClaves para La Transformación Digital de Las PymesCamila ContrerasNo ratings yet

- Journal of Business Research: João J.M. Ferreira, Cristina I. Fernandes, Fernando A.F. FerreiraDocument8 pagesJournal of Business Research: João J.M. Ferreira, Cristina I. Fernandes, Fernando A.F. FerreiraayuNo ratings yet

- UntitledDocument7 pagesUntitledMark William AbnerNo ratings yet

- APJARBA 2015 1 006 Computerized vs. Non Computerized Accounting System PDFDocument8 pagesAPJARBA 2015 1 006 Computerized vs. Non Computerized Accounting System PDFsijinyooNo ratings yet

- Digital Accounting Implementation and Audit Performance - An Empirical Research of Tax Auditors in ThailandDocument11 pagesDigital Accounting Implementation and Audit Performance - An Empirical Research of Tax Auditors in ThailandChaima LejriNo ratings yet

- Do Lower Taxes Reduce Informality Evidence From Brazil 2018Document55 pagesDo Lower Taxes Reduce Informality Evidence From Brazil 2018Bruno SalesNo ratings yet

- Digital Transformation in Accounting and Auditing: Navigating Technological Advances For The FutureDocument422 pagesDigital Transformation in Accounting and Auditing: Navigating Technological Advances For The FutureAtangana Martin AimeNo ratings yet

- 10.2478 - Picbe 2022 0079Document10 pages10.2478 - Picbe 2022 0079ENUNGNo ratings yet

- Accounting Information Systems: The Challenge of The Real-Time ReportingDocument10 pagesAccounting Information Systems: The Challenge of The Real-Time ReportingAtalya Fidela SambengaNo ratings yet

- Accounting Information Systems: The Challenge of The Real-Time ReportingDocument10 pagesAccounting Information Systems: The Challenge of The Real-Time Reportingace hoodNo ratings yet

- Final Research 1Document6 pagesFinal Research 1Rinkashitamodo AbarcarNo ratings yet

- 2.what Challenges Does The Digital Economy Bring To AccountingDocument5 pages2.what Challenges Does The Digital Economy Bring To AccountingCarolNo ratings yet

- Chapter 1Document13 pagesChapter 1Marwin Ace100% (1)

- New Era of Accounting ProjectDocument11 pagesNew Era of Accounting ProjectMihai GrecuNo ratings yet

- THE USE OF ACCOUNTING SOFTWARE AND ITS IMPACT ON PROFITABILITY OF SME IN BOCAUE Research 1Document15 pagesTHE USE OF ACCOUNTING SOFTWARE AND ITS IMPACT ON PROFITABILITY OF SME IN BOCAUE Research 1Normito DomingoNo ratings yet

- The Impact of Accounting Information Systems AIS oDocument20 pagesThe Impact of Accounting Information Systems AIS oSaleha QuadsiaNo ratings yet

- Accounting Information SystemDocument10 pagesAccounting Information SystemJRNo ratings yet

- The Effects of ICTs As Innovation Facilitators For A Greater Business Performance. Evidence From MexicoDocument10 pagesThe Effects of ICTs As Innovation Facilitators For A Greater Business Performance. Evidence From MexicoMien MienNo ratings yet

- Stage 1 Recognize The CourseDocument10 pagesStage 1 Recognize The CourseMariangelica VargasNo ratings yet

- Accounting Information Systems: The Challenge of The Real-Time ReportingDocument11 pagesAccounting Information Systems: The Challenge of The Real-Time ReportingGashinet AsfyeNo ratings yet

- Sustaining The Digital Transformation: An Exploratory Approach To Prioritize Competencies For The Future of WorkDocument6 pagesSustaining The Digital Transformation: An Exploratory Approach To Prioritize Competencies For The Future of Workraquel.cmadureiraNo ratings yet

- Blog On ITDocument14 pagesBlog On ITHalima KhatunNo ratings yet

- The Impact of Ict in Today's Accounting Seminar (Olawale)Document22 pagesThe Impact of Ict in Today's Accounting Seminar (Olawale)Seye KareemNo ratings yet

- Continuous Auditing: Strategi Pengauditan Berbasis Teknologi InformasiDocument17 pagesContinuous Auditing: Strategi Pengauditan Berbasis Teknologi InformasiESTERNo ratings yet

- The Importance of Information System in Accounting As Innovation Towards Future (Balaba, Jhon Paul J) CutieDocument13 pagesThe Importance of Information System in Accounting As Innovation Towards Future (Balaba, Jhon Paul J) CutieJhon Paul BalabaNo ratings yet

- Project On HRMDocument12 pagesProject On HRMtanuj jainNo ratings yet

- FULLTEXT01Document43 pagesFULLTEXT01Yurie MarcoNo ratings yet

- Antecedents, Consequences, and Challenges of Small and Medium-SizedDocument9 pagesAntecedents, Consequences, and Challenges of Small and Medium-SizedObinna UMgbemenaNo ratings yet

- ProjectDocument7 pagesProjectJunior EngaNo ratings yet

- Digital Trends in An Organizatio NDocument3 pagesDigital Trends in An Organizatio Nbhavisha narwaniNo ratings yet

- ResearzhDocument34 pagesResearzhxylynn myka cabanatanNo ratings yet

- Computerized Accounting Systems Usage by Small and Medium Scale Enterprises in Kumasi Metropolis, GhanaDocument14 pagesComputerized Accounting Systems Usage by Small and Medium Scale Enterprises in Kumasi Metropolis, GhanaLady Diane LuceroNo ratings yet

- Small and Medium Enterprises (Smes) Are The Enterprises Which Are Decided by The Number of Employees and or Revenues They HaveDocument21 pagesSmall and Medium Enterprises (Smes) Are The Enterprises Which Are Decided by The Number of Employees and or Revenues They HaveGeethaNo ratings yet

- Exploratory ResearchDocument13 pagesExploratory ResearchWinfree DimaalaNo ratings yet

- Comm 226 Assignment 1 ICT ReportDocument4 pagesComm 226 Assignment 1 ICT Reporttits6969No ratings yet

- Artikel Audit 4 PDFDocument10 pagesArtikel Audit 4 PDFMarchelyn PongsapanNo ratings yet

- Final Chapter 1 To 3 Bsais 3B Sure YaaDocument45 pagesFinal Chapter 1 To 3 Bsais 3B Sure YaaNikki Jean HonaNo ratings yet

- Ijias 13 167 02Document14 pagesIjias 13 167 02Younes El HachmiNo ratings yet

- Santos Bennert Figueiredo Beuren 2018 Uso-dos-Instrumentos-De-Contab 49485Document15 pagesSantos Bennert Figueiredo Beuren 2018 Uso-dos-Instrumentos-De-Contab 49485TCCONM22 - Grupo 11No ratings yet

- The Digital Transformation of External Audit and Its Impact On Corporate GovernanceDocument10 pagesThe Digital Transformation of External Audit and Its Impact On Corporate GovernanceNURUL CHOIRIYAHNo ratings yet

- E Commerce Issues Opportunities Challenges and TrendsDocument22 pagesE Commerce Issues Opportunities Challenges and TrendsLabib ShahNo ratings yet

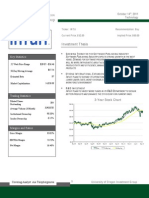

- Investment Thesis: Key StatisticsDocument19 pagesInvestment Thesis: Key Statisticsboka987No ratings yet

- WS 6Document11 pagesWS 6Luis DiasNo ratings yet

- Peluang Dan Tantangan Profesi Akuntan Di Era Big Data: Afrida PutritamaDocument11 pagesPeluang Dan Tantangan Profesi Akuntan Di Era Big Data: Afrida PutritamaRiskaNo ratings yet

- Providing Leadership Digital Full ReportDocument20 pagesProviding Leadership Digital Full ReportEditorial BuxiNo ratings yet

- 202 JLS S1 222 0Document6 pages202 JLS S1 222 0عزالدين الحسينيNo ratings yet

- Digitalization Cases: How Organizations Rethink Their Business for the Digital AgeFrom EverandDigitalization Cases: How Organizations Rethink Their Business for the Digital AgeNo ratings yet

- Lesson 3: Emergent LiteracyDocument11 pagesLesson 3: Emergent LiteracyMs. aZiaNo ratings yet

- Story of An Hour Student Charts ALLDocument42 pagesStory of An Hour Student Charts ALLRoshio Tsuyu TejidoNo ratings yet

- Assignment On Mind-Body ProblemDocument5 pagesAssignment On Mind-Body ProblemFerdous MostofaNo ratings yet

- The Great WorkDocument5 pagesThe Great WorkCristian CiobanuNo ratings yet

- 235 Performance Appraisal FormDocument3 pages235 Performance Appraisal FormCheri Ho100% (1)

- Cross Cultural Management: ChinaDocument18 pagesCross Cultural Management: Chinacarlito348150% (2)

- Understanding The Self: Name: Charlene Aurora Garjas BSCOOP1ADocument1 pageUnderstanding The Self: Name: Charlene Aurora Garjas BSCOOP1AMike AntonioNo ratings yet

- Introduction To Personal DevelopmentDocument2 pagesIntroduction To Personal DevelopmentRoselynLaurelNo ratings yet

- Narcissistic Personality DisorderDocument39 pagesNarcissistic Personality DisorderRisha Vee Argete Tutor100% (2)

- American Philological AssociationDocument11 pagesAmerican Philological AssociationNeli KoutsandreaNo ratings yet

- Positive Psychology Assignment 2Document12 pagesPositive Psychology Assignment 2Awais. anwarNo ratings yet

- Retno Fajar Satiti Thesis Proposal 0203514018Document40 pagesRetno Fajar Satiti Thesis Proposal 0203514018Utami Rosalina FirmansyahNo ratings yet

- Fundamentals of Production Logistics - Theory, Tools and Applications - 3540342109Document320 pagesFundamentals of Production Logistics - Theory, Tools and Applications - 3540342109mikloska100% (1)

- Anatoll IDocument356 pagesAnatoll IRay MoscarellaNo ratings yet

- QUantum Tunneling PDFDocument25 pagesQUantum Tunneling PDFIrun IrunNo ratings yet

- Voice in Kathy Acker's FictionDocument32 pagesVoice in Kathy Acker's FictionanaloguesNo ratings yet

- Montaigne-Of CannibalsDocument19 pagesMontaigne-Of CannibalsKasra SeifiNo ratings yet

- The Symbolism of GaneshaDocument2 pagesThe Symbolism of GaneshaSathasivam GovindasamyNo ratings yet

- Process Action and Experience 1St Edition Rowland Stout All ChapterDocument67 pagesProcess Action and Experience 1St Edition Rowland Stout All Chapterangeline.pendergrass490100% (6)

- 001complete Synonym Antonym PDF by @tglokii - 240108 - 183900Document267 pages001complete Synonym Antonym PDF by @tglokii - 240108 - 183900satul0616No ratings yet

- Vxej5 Multilevel Modeling Using RDocument226 pagesVxej5 Multilevel Modeling Using RlinoNo ratings yet

- Pathfinder - Aventuras Ocultas-131Document1 pagePathfinder - Aventuras Ocultas-131Alejandro Moriña de MoraNo ratings yet

- Peter Roe Human Designina NutshellDocument3 pagesPeter Roe Human Designina NutshellАнна БлохинаNo ratings yet

- EDST5806 - Assessment Task 1Document10 pagesEDST5806 - Assessment Task 1vu_minh1995_60171068No ratings yet

- Ethics Natural LawDocument20 pagesEthics Natural LawChristyNo ratings yet

- Sister FriendsDocument9 pagesSister FriendsPristael C MtzNo ratings yet

- NEO PI 3 BRC Sample ReportDocument8 pagesNEO PI 3 BRC Sample Reportafzallodhi736No ratings yet

- Eyers - Lacan Bachelard and FormalizationDocument19 pagesEyers - Lacan Bachelard and FormalizationHugo Tannous Jorge100% (1)