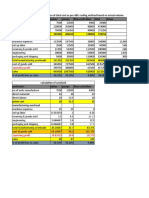

Accounts Case Study

Accounts Case Study

You might also like

- Case 26-2Document3 pagesCase 26-2NishaNo ratings yet

- Wilkerson Company ABCDocument4 pagesWilkerson Company ABCrajyalakshmiNo ratings yet

- Stuart Daw CoffeeDocument8 pagesStuart Daw CoffeeZarith Akhma100% (1)

- CFI FMVA Certification Program PDFDocument2 pagesCFI FMVA Certification Program PDFdhiraj agarwalNo ratings yet

- Chemalite - A - en - BDocument12 pagesChemalite - A - en - BAimane Beggar100% (1)

- Stuart DawDocument2 pagesStuart DawMike ChhabraNo ratings yet

- Destin Brass Case Study SolutionDocument5 pagesDestin Brass Case Study SolutionAmruta Turmé100% (2)

- Jackson Automotive Systems ExcelDocument5 pagesJackson Automotive Systems Excelonyechi2004No ratings yet

- Zenith - Marketing Research For HDTV Case AnalysisDocument7 pagesZenith - Marketing Research For HDTV Case Analysisdhiraj agarwalNo ratings yet

- AJAX OriginalDocument7 pagesAJAX Originalreva_radhakrish1834No ratings yet

- Case 18-1 Huron Automotive Company StudyDocument4 pagesCase 18-1 Huron Automotive Company StudyEmpress CarrotNo ratings yet

- Superior Manufacturing Company MpettesDocument8 pagesSuperior Manufacturing Company Mpettesapi-250891173100% (5)

- Hilton Manufacturing Company 1201326783827489 2Document6 pagesHilton Manufacturing Company 1201326783827489 2julijulijulioNo ratings yet

- BerkshireDocument12 pagesBerkshireShubhangi Satpute50% (2)

- Erie Steel Case Presentation: Decision Making With AnalyticsDocument4 pagesErie Steel Case Presentation: Decision Making With AnalyticsFiyinfoluwa OyewoNo ratings yet

- Health Development Corporation Spread Sheet (Sol)Document8 pagesHealth Development Corporation Spread Sheet (Sol)Surya Kant100% (2)

- Group 8Document20 pagesGroup 8nirajNo ratings yet

- Seligram 2Document4 pagesSeligram 2Yvette YuanNo ratings yet

- Polar SportsDocument7 pagesPolar SportsShah HussainNo ratings yet

- Delaney Motors Case SolutionDocument13 pagesDelaney Motors Case SolutionParambrahma Panda100% (2)

- Seligram Electronic Testing OperationsDocument34 pagesSeligram Electronic Testing OperationsKirtiKishanNo ratings yet

- Busines Plan-Juice StopDocument41 pagesBusines Plan-Juice StopShareef ChampNo ratings yet

- Superior ManufacturingDocument5 pagesSuperior ManufacturingCordel TwoKpsi TaildawgSnoop Cook100% (4)

- Selligram Case Answer KeyDocument3 pagesSelligram Case Answer Keysharkss521No ratings yet

- Superior Manufacturing CaseDocument4 pagesSuperior Manufacturing Casenand bhushan100% (1)

- Case-Bill FrenchDocument3 pagesCase-Bill FrenchthearpanNo ratings yet

- This Study Resource Was: Forner CarpetDocument4 pagesThis Study Resource Was: Forner CarpetLi CarinaNo ratings yet

- Compagnie Du Froid PDFDocument18 pagesCompagnie Du Froid PDFGunjanNo ratings yet

- Millichem Solution XDocument6 pagesMillichem Solution XMuhammad Junaid100% (1)

- SUBJECT: Analyses and Recommendations For The Different Cost AccountingDocument4 pagesSUBJECT: Analyses and Recommendations For The Different Cost AccountinglddNo ratings yet

- Bill French Google Docs Group 5Document7 pagesBill French Google Docs Group 5Jay Florence DalucanogNo ratings yet

- Case - SunAir Boat Builders Part - 2Document3 pagesCase - SunAir Boat Builders Part - 2dhakar_ravi1No ratings yet

- Bill French - Write Up1Document10 pagesBill French - Write Up1Nina EllyanaNo ratings yet

- PrestigeDocument13 pagesPrestigeMona SahooNo ratings yet

- Stuart DawDocument3 pagesStuart DawHarsh SoniNo ratings yet

- Hilton Case1Document2 pagesHilton Case1Ana Fernanda Gonzales CaveroNo ratings yet

- Bill French Case DataDocument5 pagesBill French Case Datadamanfromiran100% (1)

- Bridgeton HWDocument3 pagesBridgeton HWravNo ratings yet

- Vaibhav Maheshwari Merrimack Tractors 2011pgp926Document3 pagesVaibhav Maheshwari Merrimack Tractors 2011pgp926studvabzNo ratings yet

- Various Types of Cost Classifications Basis Cost Concept ExampleDocument15 pagesVarious Types of Cost Classifications Basis Cost Concept ExampleUtkarsh SharmaNo ratings yet

- JHT Case ExcelDocument4 pagesJHT Case Excelanup akasheNo ratings yet

- Group 7 - Morrissey ForgingsDocument10 pagesGroup 7 - Morrissey ForgingsVishal AgarwalNo ratings yet

- Polar Sports: Where Does Polar Sports Fit in The Course?Document21 pagesPolar Sports: Where Does Polar Sports Fit in The Course?Hugo100% (1)

- AHM13e Chapter - 01 - Solution To Problems and Key To CasesDocument19 pagesAHM13e Chapter - 01 - Solution To Problems and Key To CasesGaurav ManiyarNo ratings yet

- Pinetree MotelMP 26 Case - N - Group 4Document5 pagesPinetree MotelMP 26 Case - N - Group 4harleeniitrNo ratings yet

- Baldwin Bicycle CompanyDocument5 pagesBaldwin Bicycle CompanyPremal Gangar0% (1)

- Prestige Telephone Company SlidesDocument13 pagesPrestige Telephone Company SlidesHarsh MaheshwariNo ratings yet

- Bill French Case Submitted By: Sourabh Phanase Section: ADocument2 pagesBill French Case Submitted By: Sourabh Phanase Section: AsourabhphanaseNo ratings yet

- Bill French SolutionDocument5 pagesBill French Solutionrics_alias087196No ratings yet

- Hilton Case1Document2 pagesHilton Case1Ken KandellNo ratings yet

- Air Thread Excel FileDocument7 pagesAir Thread Excel FileAlex Wilson0% (1)

- Sinclair Company Group Case StudyDocument20 pagesSinclair Company Group Case StudyNida Amri50% (4)

- Polar SportsDocument9 pagesPolar SportsAbhishek RawatNo ratings yet

- Danshui Plant 2Document13 pagesDanshui Plant 2Bernard EugineNo ratings yet

- Forner Carpet CompanyDocument7 pagesForner Carpet CompanySimranjeet KaurNo ratings yet

- Applichemcase Group 5 - PresentationDocument20 pagesApplichemcase Group 5 - Presentationnick najitoNo ratings yet

- Harley Davidson Case StudyDocument8 pagesHarley Davidson Case StudyfossacecaNo ratings yet

- Daktronics E Dividend Policy in 2010Document26 pagesDaktronics E Dividend Policy in 2010IBRAHIM KHANNo ratings yet

- PrestigeDocument10 pagesPrestigeSumit ChandraNo ratings yet

- Acc 205 Ca1Document11 pagesAcc 205 Ca1Nidhi SharmaNo ratings yet

- Sup Manuf Company Final DraftDocument20 pagesSup Manuf Company Final DraftkriteesinhaNo ratings yet

- Chapter 5 Solution To Problems and CasesDocument22 pagesChapter 5 Solution To Problems and Caseschandel08No ratings yet

- CH 26Document4 pagesCH 26Kurt Del RosarioNo ratings yet

- BMW - Case Analysis: Submitted To-Dr. K. Abdul WaheedDocument3 pagesBMW - Case Analysis: Submitted To-Dr. K. Abdul Waheeddhiraj agarwalNo ratings yet

- Harley-Davidson - CASE ANALYSISDocument4 pagesHarley-Davidson - CASE ANALYSISdhiraj agarwalNo ratings yet

- BMW - Case Analysis: Submitted To-Dr. K. Abdul WaheedDocument3 pagesBMW - Case Analysis: Submitted To-Dr. K. Abdul Waheeddhiraj agarwalNo ratings yet

- Dupont (A) - Case AnalysisDocument5 pagesDupont (A) - Case Analysisdhiraj agarwalNo ratings yet

- Dominion Motors and Controls Ltd. - Case AnalysisDocument7 pagesDominion Motors and Controls Ltd. - Case Analysisdhiraj agarwalNo ratings yet

- Exim Policy of IndiaDocument10 pagesExim Policy of IndiaYash BhatiaNo ratings yet

- G3 1 Index and ChecklistDocument123 pagesG3 1 Index and ChecklistWendy Al SyabanaNo ratings yet

- Calculus 2 - Tutorial 4Document4 pagesCalculus 2 - Tutorial 4Albert CofieNo ratings yet

- Arun Kumar Shukla: Notable Attainments at HDB Financial Services LimitedDocument2 pagesArun Kumar Shukla: Notable Attainments at HDB Financial Services Limitedsaurabh kumar1No ratings yet

- Bus Trans Taxes Key Solution PTVAT 2013 2014Document17 pagesBus Trans Taxes Key Solution PTVAT 2013 2014Jandave ApinoNo ratings yet

- Patni Ar2009Document174 pagesPatni Ar2009chip_blueNo ratings yet

- Policy WriteupDocument3 pagesPolicy Writeupdey.joybrotoNo ratings yet

- Profitability Ratio 2Document18 pagesProfitability Ratio 2Wynphap podiotanNo ratings yet

- Measuring Customer Experience in Service: A Systematic ReviewDocument22 pagesMeasuring Customer Experience in Service: A Systematic ReviewTheatre GareNo ratings yet

- MTN OFS Application Form EditableDocument1 pageMTN OFS Application Form Editablepeter sundayNo ratings yet

- Joshua Greenberg 9 1 12Document3 pagesJoshua Greenberg 9 1 12api-239860330No ratings yet

- Product Distribution The BasicsDocument8 pagesProduct Distribution The BasicsNicol Katherine Sierra RodríguezNo ratings yet

- Kajal Rai 24Document23 pagesKajal Rai 24KAJAL RAINo ratings yet

- Introduction To Accounting Mock Exam: Certificate in Accounting and Finance Stage ExaminationDocument9 pagesIntroduction To Accounting Mock Exam: Certificate in Accounting and Finance Stage ExaminationUsman WaheedNo ratings yet

- Marketing Debate Ch17Document3 pagesMarketing Debate Ch17Mariska Putri Adelia67% (3)

- Web Design RFP SampleDocument9 pagesWeb Design RFP Samplebarneygurl0% (1)

- Kaizen Costing: A Catalyst For Change and Continuous Cost ImprovementDocument16 pagesKaizen Costing: A Catalyst For Change and Continuous Cost ImprovementnoorNo ratings yet

- 2.2.5 Using The Marketing MixDocument6 pages2.2.5 Using The Marketing MixryanNo ratings yet

- InventoryDocument3 pagesInventoryrhandy oyaoNo ratings yet

- The Road To Regtech: The (Astonishing) Example of The European UnionDocument12 pagesThe Road To Regtech: The (Astonishing) Example of The European UnionDamero PalominoNo ratings yet

- Tupelo Medical:: Managing Price ErosionDocument5 pagesTupelo Medical:: Managing Price ErosionxyzNo ratings yet

- SURVEY QUESTIONNAIRE FinalDocument6 pagesSURVEY QUESTIONNAIRE FinalFai MeileNo ratings yet

- Punjab Fabricators: About OwnersDocument4 pagesPunjab Fabricators: About OwnersDinesh ChahalNo ratings yet

- Model Canevas 3Document10 pagesModel Canevas 3Hind Nia BenbrahimNo ratings yet

- Chapter 14Document4 pagesChapter 14jorgeNo ratings yet

- 2 Power System Economics 1-58Document87 pages2 Power System Economics 1-58Rudraraju Chaitanya100% (1)

- KOUDIA WF Contract - Morocco - ANAS - Electrical Engineer (Telework)Document23 pagesKOUDIA WF Contract - Morocco - ANAS - Electrical Engineer (Telework)Anass EL OUARDINo ratings yet

- Intellectual CapitalDocument2 pagesIntellectual CapitalraprapNo ratings yet

- Secretary Day - Secretaries, PAs, and EAsDocument4 pagesSecretary Day - Secretaries, PAs, and EAsMr MathipsNo ratings yet

Download as docx, pdf, or txt

You might also like

- Case 26-2Document3 pagesCase 26-2NishaNo ratings yet

- Wilkerson Company ABCDocument4 pagesWilkerson Company ABCrajyalakshmiNo ratings yet

- Stuart Daw CoffeeDocument8 pagesStuart Daw CoffeeZarith Akhma100% (1)

- CFI FMVA Certification Program PDFDocument2 pagesCFI FMVA Certification Program PDFdhiraj agarwalNo ratings yet

- Chemalite - A - en - BDocument12 pagesChemalite - A - en - BAimane Beggar100% (1)

- Stuart DawDocument2 pagesStuart DawMike ChhabraNo ratings yet

- Destin Brass Case Study SolutionDocument5 pagesDestin Brass Case Study SolutionAmruta Turmé100% (2)

- Jackson Automotive Systems ExcelDocument5 pagesJackson Automotive Systems Excelonyechi2004No ratings yet

- Zenith - Marketing Research For HDTV Case AnalysisDocument7 pagesZenith - Marketing Research For HDTV Case Analysisdhiraj agarwalNo ratings yet

- AJAX OriginalDocument7 pagesAJAX Originalreva_radhakrish1834No ratings yet

- Case 18-1 Huron Automotive Company StudyDocument4 pagesCase 18-1 Huron Automotive Company StudyEmpress CarrotNo ratings yet

- Superior Manufacturing Company MpettesDocument8 pagesSuperior Manufacturing Company Mpettesapi-250891173100% (5)

- Hilton Manufacturing Company 1201326783827489 2Document6 pagesHilton Manufacturing Company 1201326783827489 2julijulijulioNo ratings yet

- BerkshireDocument12 pagesBerkshireShubhangi Satpute50% (2)

- Erie Steel Case Presentation: Decision Making With AnalyticsDocument4 pagesErie Steel Case Presentation: Decision Making With AnalyticsFiyinfoluwa OyewoNo ratings yet

- Health Development Corporation Spread Sheet (Sol)Document8 pagesHealth Development Corporation Spread Sheet (Sol)Surya Kant100% (2)

- Group 8Document20 pagesGroup 8nirajNo ratings yet

- Seligram 2Document4 pagesSeligram 2Yvette YuanNo ratings yet

- Polar SportsDocument7 pagesPolar SportsShah HussainNo ratings yet

- Delaney Motors Case SolutionDocument13 pagesDelaney Motors Case SolutionParambrahma Panda100% (2)

- Seligram Electronic Testing OperationsDocument34 pagesSeligram Electronic Testing OperationsKirtiKishanNo ratings yet

- Busines Plan-Juice StopDocument41 pagesBusines Plan-Juice StopShareef ChampNo ratings yet

- Superior ManufacturingDocument5 pagesSuperior ManufacturingCordel TwoKpsi TaildawgSnoop Cook100% (4)

- Selligram Case Answer KeyDocument3 pagesSelligram Case Answer Keysharkss521No ratings yet

- Superior Manufacturing CaseDocument4 pagesSuperior Manufacturing Casenand bhushan100% (1)

- Case-Bill FrenchDocument3 pagesCase-Bill FrenchthearpanNo ratings yet

- This Study Resource Was: Forner CarpetDocument4 pagesThis Study Resource Was: Forner CarpetLi CarinaNo ratings yet

- Compagnie Du Froid PDFDocument18 pagesCompagnie Du Froid PDFGunjanNo ratings yet

- Millichem Solution XDocument6 pagesMillichem Solution XMuhammad Junaid100% (1)

- SUBJECT: Analyses and Recommendations For The Different Cost AccountingDocument4 pagesSUBJECT: Analyses and Recommendations For The Different Cost AccountinglddNo ratings yet

- Bill French Google Docs Group 5Document7 pagesBill French Google Docs Group 5Jay Florence DalucanogNo ratings yet

- Case - SunAir Boat Builders Part - 2Document3 pagesCase - SunAir Boat Builders Part - 2dhakar_ravi1No ratings yet

- Bill French - Write Up1Document10 pagesBill French - Write Up1Nina EllyanaNo ratings yet

- PrestigeDocument13 pagesPrestigeMona SahooNo ratings yet

- Stuart DawDocument3 pagesStuart DawHarsh SoniNo ratings yet

- Hilton Case1Document2 pagesHilton Case1Ana Fernanda Gonzales CaveroNo ratings yet

- Bill French Case DataDocument5 pagesBill French Case Datadamanfromiran100% (1)

- Bridgeton HWDocument3 pagesBridgeton HWravNo ratings yet

- Vaibhav Maheshwari Merrimack Tractors 2011pgp926Document3 pagesVaibhav Maheshwari Merrimack Tractors 2011pgp926studvabzNo ratings yet

- Various Types of Cost Classifications Basis Cost Concept ExampleDocument15 pagesVarious Types of Cost Classifications Basis Cost Concept ExampleUtkarsh SharmaNo ratings yet

- JHT Case ExcelDocument4 pagesJHT Case Excelanup akasheNo ratings yet

- Group 7 - Morrissey ForgingsDocument10 pagesGroup 7 - Morrissey ForgingsVishal AgarwalNo ratings yet

- Polar Sports: Where Does Polar Sports Fit in The Course?Document21 pagesPolar Sports: Where Does Polar Sports Fit in The Course?Hugo100% (1)

- AHM13e Chapter - 01 - Solution To Problems and Key To CasesDocument19 pagesAHM13e Chapter - 01 - Solution To Problems and Key To CasesGaurav ManiyarNo ratings yet

- Pinetree MotelMP 26 Case - N - Group 4Document5 pagesPinetree MotelMP 26 Case - N - Group 4harleeniitrNo ratings yet

- Baldwin Bicycle CompanyDocument5 pagesBaldwin Bicycle CompanyPremal Gangar0% (1)

- Prestige Telephone Company SlidesDocument13 pagesPrestige Telephone Company SlidesHarsh MaheshwariNo ratings yet

- Bill French Case Submitted By: Sourabh Phanase Section: ADocument2 pagesBill French Case Submitted By: Sourabh Phanase Section: AsourabhphanaseNo ratings yet

- Bill French SolutionDocument5 pagesBill French Solutionrics_alias087196No ratings yet

- Hilton Case1Document2 pagesHilton Case1Ken KandellNo ratings yet

- Air Thread Excel FileDocument7 pagesAir Thread Excel FileAlex Wilson0% (1)

- Sinclair Company Group Case StudyDocument20 pagesSinclair Company Group Case StudyNida Amri50% (4)

- Polar SportsDocument9 pagesPolar SportsAbhishek RawatNo ratings yet

- Danshui Plant 2Document13 pagesDanshui Plant 2Bernard EugineNo ratings yet

- Forner Carpet CompanyDocument7 pagesForner Carpet CompanySimranjeet KaurNo ratings yet

- Applichemcase Group 5 - PresentationDocument20 pagesApplichemcase Group 5 - Presentationnick najitoNo ratings yet

- Harley Davidson Case StudyDocument8 pagesHarley Davidson Case StudyfossacecaNo ratings yet

- Daktronics E Dividend Policy in 2010Document26 pagesDaktronics E Dividend Policy in 2010IBRAHIM KHANNo ratings yet

- PrestigeDocument10 pagesPrestigeSumit ChandraNo ratings yet

- Acc 205 Ca1Document11 pagesAcc 205 Ca1Nidhi SharmaNo ratings yet

- Sup Manuf Company Final DraftDocument20 pagesSup Manuf Company Final DraftkriteesinhaNo ratings yet

- Chapter 5 Solution To Problems and CasesDocument22 pagesChapter 5 Solution To Problems and Caseschandel08No ratings yet

- CH 26Document4 pagesCH 26Kurt Del RosarioNo ratings yet

- BMW - Case Analysis: Submitted To-Dr. K. Abdul WaheedDocument3 pagesBMW - Case Analysis: Submitted To-Dr. K. Abdul Waheeddhiraj agarwalNo ratings yet

- Harley-Davidson - CASE ANALYSISDocument4 pagesHarley-Davidson - CASE ANALYSISdhiraj agarwalNo ratings yet

- BMW - Case Analysis: Submitted To-Dr. K. Abdul WaheedDocument3 pagesBMW - Case Analysis: Submitted To-Dr. K. Abdul Waheeddhiraj agarwalNo ratings yet

- Dupont (A) - Case AnalysisDocument5 pagesDupont (A) - Case Analysisdhiraj agarwalNo ratings yet

- Dominion Motors and Controls Ltd. - Case AnalysisDocument7 pagesDominion Motors and Controls Ltd. - Case Analysisdhiraj agarwalNo ratings yet

- Exim Policy of IndiaDocument10 pagesExim Policy of IndiaYash BhatiaNo ratings yet

- G3 1 Index and ChecklistDocument123 pagesG3 1 Index and ChecklistWendy Al SyabanaNo ratings yet

- Calculus 2 - Tutorial 4Document4 pagesCalculus 2 - Tutorial 4Albert CofieNo ratings yet

- Arun Kumar Shukla: Notable Attainments at HDB Financial Services LimitedDocument2 pagesArun Kumar Shukla: Notable Attainments at HDB Financial Services Limitedsaurabh kumar1No ratings yet

- Bus Trans Taxes Key Solution PTVAT 2013 2014Document17 pagesBus Trans Taxes Key Solution PTVAT 2013 2014Jandave ApinoNo ratings yet

- Patni Ar2009Document174 pagesPatni Ar2009chip_blueNo ratings yet

- Policy WriteupDocument3 pagesPolicy Writeupdey.joybrotoNo ratings yet

- Profitability Ratio 2Document18 pagesProfitability Ratio 2Wynphap podiotanNo ratings yet

- Measuring Customer Experience in Service: A Systematic ReviewDocument22 pagesMeasuring Customer Experience in Service: A Systematic ReviewTheatre GareNo ratings yet

- MTN OFS Application Form EditableDocument1 pageMTN OFS Application Form Editablepeter sundayNo ratings yet

- Joshua Greenberg 9 1 12Document3 pagesJoshua Greenberg 9 1 12api-239860330No ratings yet

- Product Distribution The BasicsDocument8 pagesProduct Distribution The BasicsNicol Katherine Sierra RodríguezNo ratings yet

- Kajal Rai 24Document23 pagesKajal Rai 24KAJAL RAINo ratings yet

- Introduction To Accounting Mock Exam: Certificate in Accounting and Finance Stage ExaminationDocument9 pagesIntroduction To Accounting Mock Exam: Certificate in Accounting and Finance Stage ExaminationUsman WaheedNo ratings yet

- Marketing Debate Ch17Document3 pagesMarketing Debate Ch17Mariska Putri Adelia67% (3)

- Web Design RFP SampleDocument9 pagesWeb Design RFP Samplebarneygurl0% (1)

- Kaizen Costing: A Catalyst For Change and Continuous Cost ImprovementDocument16 pagesKaizen Costing: A Catalyst For Change and Continuous Cost ImprovementnoorNo ratings yet

- 2.2.5 Using The Marketing MixDocument6 pages2.2.5 Using The Marketing MixryanNo ratings yet

- InventoryDocument3 pagesInventoryrhandy oyaoNo ratings yet

- The Road To Regtech: The (Astonishing) Example of The European UnionDocument12 pagesThe Road To Regtech: The (Astonishing) Example of The European UnionDamero PalominoNo ratings yet

- Tupelo Medical:: Managing Price ErosionDocument5 pagesTupelo Medical:: Managing Price ErosionxyzNo ratings yet

- SURVEY QUESTIONNAIRE FinalDocument6 pagesSURVEY QUESTIONNAIRE FinalFai MeileNo ratings yet

- Punjab Fabricators: About OwnersDocument4 pagesPunjab Fabricators: About OwnersDinesh ChahalNo ratings yet

- Model Canevas 3Document10 pagesModel Canevas 3Hind Nia BenbrahimNo ratings yet

- Chapter 14Document4 pagesChapter 14jorgeNo ratings yet

- 2 Power System Economics 1-58Document87 pages2 Power System Economics 1-58Rudraraju Chaitanya100% (1)

- KOUDIA WF Contract - Morocco - ANAS - Electrical Engineer (Telework)Document23 pagesKOUDIA WF Contract - Morocco - ANAS - Electrical Engineer (Telework)Anass EL OUARDINo ratings yet

- Intellectual CapitalDocument2 pagesIntellectual CapitalraprapNo ratings yet

- Secretary Day - Secretaries, PAs, and EAsDocument4 pagesSecretary Day - Secretaries, PAs, and EAsMr MathipsNo ratings yet