Case Digest

Case Digest

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5834)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (903)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (350)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (824)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (405)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- MACK Truck Electrical Wiring and Connections Manual CHU, CXU, GU, TD, MRU, LR SeriesDocument94 pagesMACK Truck Electrical Wiring and Connections Manual CHU, CXU, GU, TD, MRU, LR SeriesAlex Renne Chambi100% (9)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Allstate/McKinsey Bates H000001010Document495 pagesAllstate/McKinsey Bates H0000010104207west59th100% (3)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- ACLS Study Guide NewDocument35 pagesACLS Study Guide NewNIRANJANA SHALINI100% (1)

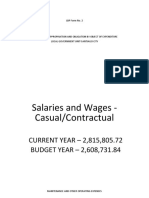

- LBP Form No. 4Document8 pagesLBP Form No. 4Shie La Ma RieNo ratings yet

- Case Digest in Corp - Law 2019 2020Document393 pagesCase Digest in Corp - Law 2019 2020Shie La Ma Rie100% (4)

- 4 - Hydro Jetting and Sludge RemovalDocument18 pages4 - Hydro Jetting and Sludge RemovalPerwez21100% (2)

- Affidavit of No EmbalmingDocument1 pageAffidavit of No EmbalmingShie La Ma RieNo ratings yet

- Affidavit of Loss JunkDocument1 pageAffidavit of Loss JunkShie La Ma RieNo ratings yet

- Election OffensesDocument6 pagesElection OffensesShie La Ma RieNo ratings yet

- Programmed Appropriation and Obligation by Object of Expenditure Local Government Unit-Santiago CityDocument2 pagesProgrammed Appropriation and Obligation by Object of Expenditure Local Government Unit-Santiago CityShie La Ma RieNo ratings yet

- "Bayanihan To Heal As One Act of 2020" and The Local Government Code of 1991: The Issues and Concerns Arising From Their InconsistenciesDocument18 pages"Bayanihan To Heal As One Act of 2020" and The Local Government Code of 1991: The Issues and Concerns Arising From Their InconsistenciesShie La Ma RieNo ratings yet

- (G.R. No. L-19808. September 29, 1966.) Carino V. AccfaDocument4 pages(G.R. No. L-19808. September 29, 1966.) Carino V. AccfaShie La Ma RieNo ratings yet

- Special Proceedings (Estate Settlement Preliminaries)Document31 pagesSpecial Proceedings (Estate Settlement Preliminaries)Shie La Ma RieNo ratings yet

- Affidavit of Loss (ELIZABETH T. MALIGSA)Document1 pageAffidavit of Loss (ELIZABETH T. MALIGSA)Shie La Ma RieNo ratings yet

- Acknowledgement ReceiptDocument2 pagesAcknowledgement ReceiptShie La Ma RieNo ratings yet

- Affidavit of Discrepancy - April Joy GayapDocument2 pagesAffidavit of Discrepancy - April Joy GayapShie La Ma RieNo ratings yet

- Affidavit of AcknowledgmentDocument1 pageAffidavit of AcknowledgmentShie La Ma RieNo ratings yet

- Pilipinas Loan Company Vs SECDocument1 pagePilipinas Loan Company Vs SECShie La Ma RieNo ratings yet

- Affidavit of Acknowledgement of Father Paternity - LABOGDocument1 pageAffidavit of Acknowledgement of Father Paternity - LABOGShie La Ma RieNo ratings yet

- Mid Pasig Land and Development Corporation Vs TablanteDocument2 pagesMid Pasig Land and Development Corporation Vs TablanteShie La Ma RieNo ratings yet

- LIGAYA ESGUERRA Vs HOLCIMDocument3 pagesLIGAYA ESGUERRA Vs HOLCIMShie La Ma Rie0% (1)

- Transpo Table of DoctrinesDocument7 pagesTranspo Table of DoctrinesShie La Ma RieNo ratings yet

- Transpo Table of DoctrinesDocument7 pagesTranspo Table of DoctrinesShie La Ma RieNo ratings yet

- Insurance Fraud: Atty. Dennis B. FunaDocument47 pagesInsurance Fraud: Atty. Dennis B. FunaShie La Ma RieNo ratings yet

- Case DigestsDocument11 pagesCase DigestsShie La Ma RieNo ratings yet

- Rem Law Case DigestsDocument28 pagesRem Law Case DigestsShie La Ma RieNo ratings yet

- Legal FormsDocument4 pagesLegal FormsShie La Ma RieNo ratings yet

- Group 8 Design Main Report + Appendix (1) 1 400Document400 pagesGroup 8 Design Main Report + Appendix (1) 1 400Manishaa Varatha RajuNo ratings yet

- SIM7000 Series - AT Command Manual - V1.01Document163 pagesSIM7000 Series - AT Command Manual - V1.01Bill CheimarasNo ratings yet

- DD175Document1 pageDD175James KelleyNo ratings yet

- Wbcviii PDFDocument1,192 pagesWbcviii PDFDaniel PinheiroNo ratings yet

- PRELIM Fire Technology and Arson InvestigationDocument6 pagesPRELIM Fire Technology and Arson InvestigationIgnacio Burog RazonaNo ratings yet

- PDFDocument1 pagePDFMiguel Ángel Gálvez FernándezNo ratings yet

- Adaptable Multi Nut Fastner With Manual Height Adjustment SystemDocument48 pagesAdaptable Multi Nut Fastner With Manual Height Adjustment SystemANAND KRISHNANNo ratings yet

- PNP ACG - Understanding Digital ForensicsDocument76 pagesPNP ACG - Understanding Digital ForensicsTin TinNo ratings yet

- July 2011 Jacksonville ReviewDocument36 pagesJuly 2011 Jacksonville ReviewThe Jacksonville ReviewNo ratings yet

- Norma ASTM B733Document14 pagesNorma ASTM B733diegohrey239100% (3)

- Regional Trial Court: Motion To Quash Search WarrantDocument3 pagesRegional Trial Court: Motion To Quash Search WarrantPaulo VillarinNo ratings yet

- Adaptive Multi RateDocument16 pagesAdaptive Multi RateRogelio HernandezNo ratings yet

- Hotel Administration and Management Network - AbstractDocument3 pagesHotel Administration and Management Network - AbstractMehadi Hasan RoxyNo ratings yet

- CursorDocument7 pagesCursorSachin KumarNo ratings yet

- New York City Subway: THE BronxDocument1 pageNew York City Subway: THE BronxPrincesa LizNo ratings yet

- 570 Academic Word ListDocument5 pages570 Academic Word ListTrà MyNo ratings yet

- Admin SummaryDocument116 pagesAdmin SummaryElliot PaulNo ratings yet

- Code of Practice For Power System ProtectionDocument3 pagesCode of Practice For Power System ProtectionVinit JhingronNo ratings yet

- Analytical Investigation of Entropy Production With Convective Heat Transfer in Pressure Driven Flow of A Generalised Newtonian FluidDocument30 pagesAnalytical Investigation of Entropy Production With Convective Heat Transfer in Pressure Driven Flow of A Generalised Newtonian FluidUğur DemirNo ratings yet

- Malinta PDFDocument8 pagesMalinta PDFAngelina CruzNo ratings yet

- CA ProjectDocument21 pagesCA Projectkalaswami100% (1)

- Environmental Liabilities in Colombia: A Critical Review of Current Status and Challenges For A Megadiverse CountryDocument16 pagesEnvironmental Liabilities in Colombia: A Critical Review of Current Status and Challenges For A Megadiverse CountryDgo PalaciosNo ratings yet

- Fusing Concurrent Orthogonal Wide-Aperture Sonar Images For Dense Underwater 3D ReconstructionDocument8 pagesFusing Concurrent Orthogonal Wide-Aperture Sonar Images For Dense Underwater 3D ReconstructionVincent WenNo ratings yet

- Module 3 Notes (1) - 1Document18 pagesModule 3 Notes (1) - 1PARZIVAL GAMINGNo ratings yet

- Schedule of FinishesDocument7 pagesSchedule of FinishesĐức ToànNo ratings yet

- Bushing High VoltageDocument3 pagesBushing High VoltageRavi K NNo ratings yet

Download as docx, pdf, or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5834)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (903)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (350)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (824)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (405)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- MACK Truck Electrical Wiring and Connections Manual CHU, CXU, GU, TD, MRU, LR SeriesDocument94 pagesMACK Truck Electrical Wiring and Connections Manual CHU, CXU, GU, TD, MRU, LR SeriesAlex Renne Chambi100% (9)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Allstate/McKinsey Bates H000001010Document495 pagesAllstate/McKinsey Bates H0000010104207west59th100% (3)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- ACLS Study Guide NewDocument35 pagesACLS Study Guide NewNIRANJANA SHALINI100% (1)

- LBP Form No. 4Document8 pagesLBP Form No. 4Shie La Ma RieNo ratings yet

- Case Digest in Corp - Law 2019 2020Document393 pagesCase Digest in Corp - Law 2019 2020Shie La Ma Rie100% (4)

- 4 - Hydro Jetting and Sludge RemovalDocument18 pages4 - Hydro Jetting and Sludge RemovalPerwez21100% (2)

- Affidavit of No EmbalmingDocument1 pageAffidavit of No EmbalmingShie La Ma RieNo ratings yet

- Affidavit of Loss JunkDocument1 pageAffidavit of Loss JunkShie La Ma RieNo ratings yet

- Election OffensesDocument6 pagesElection OffensesShie La Ma RieNo ratings yet

- Programmed Appropriation and Obligation by Object of Expenditure Local Government Unit-Santiago CityDocument2 pagesProgrammed Appropriation and Obligation by Object of Expenditure Local Government Unit-Santiago CityShie La Ma RieNo ratings yet

- "Bayanihan To Heal As One Act of 2020" and The Local Government Code of 1991: The Issues and Concerns Arising From Their InconsistenciesDocument18 pages"Bayanihan To Heal As One Act of 2020" and The Local Government Code of 1991: The Issues and Concerns Arising From Their InconsistenciesShie La Ma RieNo ratings yet

- (G.R. No. L-19808. September 29, 1966.) Carino V. AccfaDocument4 pages(G.R. No. L-19808. September 29, 1966.) Carino V. AccfaShie La Ma RieNo ratings yet

- Special Proceedings (Estate Settlement Preliminaries)Document31 pagesSpecial Proceedings (Estate Settlement Preliminaries)Shie La Ma RieNo ratings yet

- Affidavit of Loss (ELIZABETH T. MALIGSA)Document1 pageAffidavit of Loss (ELIZABETH T. MALIGSA)Shie La Ma RieNo ratings yet

- Acknowledgement ReceiptDocument2 pagesAcknowledgement ReceiptShie La Ma RieNo ratings yet

- Affidavit of Discrepancy - April Joy GayapDocument2 pagesAffidavit of Discrepancy - April Joy GayapShie La Ma RieNo ratings yet

- Affidavit of AcknowledgmentDocument1 pageAffidavit of AcknowledgmentShie La Ma RieNo ratings yet

- Pilipinas Loan Company Vs SECDocument1 pagePilipinas Loan Company Vs SECShie La Ma RieNo ratings yet

- Affidavit of Acknowledgement of Father Paternity - LABOGDocument1 pageAffidavit of Acknowledgement of Father Paternity - LABOGShie La Ma RieNo ratings yet

- Mid Pasig Land and Development Corporation Vs TablanteDocument2 pagesMid Pasig Land and Development Corporation Vs TablanteShie La Ma RieNo ratings yet

- LIGAYA ESGUERRA Vs HOLCIMDocument3 pagesLIGAYA ESGUERRA Vs HOLCIMShie La Ma Rie0% (1)

- Transpo Table of DoctrinesDocument7 pagesTranspo Table of DoctrinesShie La Ma RieNo ratings yet

- Transpo Table of DoctrinesDocument7 pagesTranspo Table of DoctrinesShie La Ma RieNo ratings yet

- Insurance Fraud: Atty. Dennis B. FunaDocument47 pagesInsurance Fraud: Atty. Dennis B. FunaShie La Ma RieNo ratings yet

- Case DigestsDocument11 pagesCase DigestsShie La Ma RieNo ratings yet

- Rem Law Case DigestsDocument28 pagesRem Law Case DigestsShie La Ma RieNo ratings yet

- Legal FormsDocument4 pagesLegal FormsShie La Ma RieNo ratings yet

- Group 8 Design Main Report + Appendix (1) 1 400Document400 pagesGroup 8 Design Main Report + Appendix (1) 1 400Manishaa Varatha RajuNo ratings yet

- SIM7000 Series - AT Command Manual - V1.01Document163 pagesSIM7000 Series - AT Command Manual - V1.01Bill CheimarasNo ratings yet

- DD175Document1 pageDD175James KelleyNo ratings yet

- Wbcviii PDFDocument1,192 pagesWbcviii PDFDaniel PinheiroNo ratings yet

- PRELIM Fire Technology and Arson InvestigationDocument6 pagesPRELIM Fire Technology and Arson InvestigationIgnacio Burog RazonaNo ratings yet

- PDFDocument1 pagePDFMiguel Ángel Gálvez FernándezNo ratings yet

- Adaptable Multi Nut Fastner With Manual Height Adjustment SystemDocument48 pagesAdaptable Multi Nut Fastner With Manual Height Adjustment SystemANAND KRISHNANNo ratings yet

- PNP ACG - Understanding Digital ForensicsDocument76 pagesPNP ACG - Understanding Digital ForensicsTin TinNo ratings yet

- July 2011 Jacksonville ReviewDocument36 pagesJuly 2011 Jacksonville ReviewThe Jacksonville ReviewNo ratings yet

- Norma ASTM B733Document14 pagesNorma ASTM B733diegohrey239100% (3)

- Regional Trial Court: Motion To Quash Search WarrantDocument3 pagesRegional Trial Court: Motion To Quash Search WarrantPaulo VillarinNo ratings yet

- Adaptive Multi RateDocument16 pagesAdaptive Multi RateRogelio HernandezNo ratings yet

- Hotel Administration and Management Network - AbstractDocument3 pagesHotel Administration and Management Network - AbstractMehadi Hasan RoxyNo ratings yet

- CursorDocument7 pagesCursorSachin KumarNo ratings yet

- New York City Subway: THE BronxDocument1 pageNew York City Subway: THE BronxPrincesa LizNo ratings yet

- 570 Academic Word ListDocument5 pages570 Academic Word ListTrà MyNo ratings yet

- Admin SummaryDocument116 pagesAdmin SummaryElliot PaulNo ratings yet

- Code of Practice For Power System ProtectionDocument3 pagesCode of Practice For Power System ProtectionVinit JhingronNo ratings yet

- Analytical Investigation of Entropy Production With Convective Heat Transfer in Pressure Driven Flow of A Generalised Newtonian FluidDocument30 pagesAnalytical Investigation of Entropy Production With Convective Heat Transfer in Pressure Driven Flow of A Generalised Newtonian FluidUğur DemirNo ratings yet

- Malinta PDFDocument8 pagesMalinta PDFAngelina CruzNo ratings yet

- CA ProjectDocument21 pagesCA Projectkalaswami100% (1)

- Environmental Liabilities in Colombia: A Critical Review of Current Status and Challenges For A Megadiverse CountryDocument16 pagesEnvironmental Liabilities in Colombia: A Critical Review of Current Status and Challenges For A Megadiverse CountryDgo PalaciosNo ratings yet

- Fusing Concurrent Orthogonal Wide-Aperture Sonar Images For Dense Underwater 3D ReconstructionDocument8 pagesFusing Concurrent Orthogonal Wide-Aperture Sonar Images For Dense Underwater 3D ReconstructionVincent WenNo ratings yet

- Module 3 Notes (1) - 1Document18 pagesModule 3 Notes (1) - 1PARZIVAL GAMINGNo ratings yet

- Schedule of FinishesDocument7 pagesSchedule of FinishesĐức ToànNo ratings yet

- Bushing High VoltageDocument3 pagesBushing High VoltageRavi K NNo ratings yet