Download as pdf or txt

You might also like

- Hull OFOD10 e Solutions CH 07Document12 pagesHull OFOD10 e Solutions CH 07Vishal GoyalNo ratings yet

- Interest Rate Swap-FinalDocument13 pagesInterest Rate Swap-FinalKaran DoshiNo ratings yet

- Sample Questions For SWAPDocument4 pagesSample Questions For SWAPKarthik Nandula100% (1)

- TAS BOOKS Introduction To Accounts 2006Document33 pagesTAS BOOKS Introduction To Accounts 2006mroovkoyadNo ratings yet

- Dual Currency (Abrevated Version)Document6 pagesDual Currency (Abrevated Version)SimonaltkornNo ratings yet

- Interest Rate ParityDocument3 pagesInterest Rate ParityPratik PatraNo ratings yet

- Swap Valuation Practice ProblemsDocument3 pagesSwap Valuation Practice ProblemsebbamorkNo ratings yet

- Covered Interest ArbitrageDocument3 pagesCovered Interest ArbitrageKamrul HasanNo ratings yet

- FCNR Swap Deal: What It Means For NrisDocument5 pagesFCNR Swap Deal: What It Means For NrisPrateek MohapatraNo ratings yet

- Currency SwapsDocument21 pagesCurrency Swapsdebaditya1985No ratings yet

- Currency SwapDocument19 pagesCurrency Swapneha sharma100% (1)

- Swap ContractsDocument11 pagesSwap ContractsSanya rajNo ratings yet

- Interest Rate Swap ValuationDocument7 pagesInterest Rate Swap Valuationamanmanji2011No ratings yet

- Sbi ReportDocument8 pagesSbi ReportKUMARAGURU PONRAJNo ratings yet

- Financial AccountingDocument11 pagesFinancial AccountingVipul ShahNo ratings yet

- Chapter 08 (International Short-Term Financing) NewDocument3 pagesChapter 08 (International Short-Term Financing) NewKobir HossainNo ratings yet

- RM PPT SwapDocument10 pagesRM PPT SwappankajkubadiyaNo ratings yet

- 05 Fixed Income SecuritiesDocument55 pages05 Fixed Income SecuritiessukeshNo ratings yet

- General Knowledge Today - 113Document2 pagesGeneral Knowledge Today - 113niranjan_meharNo ratings yet

- International Finance NoteDocument35 pagesInternational Finance Noteademoji00No ratings yet

- Time Value of MoneyDocument7 pagesTime Value of MoneyMarlon A. RodriguezNo ratings yet

- SwapDocument61 pagesSwapKajal ChaudharyNo ratings yet

- Instructor: Dr. LAU Sie Ting: Course Notes For Seminar 3 Chapter 5: Time Value of Money Part BDocument34 pagesInstructor: Dr. LAU Sie Ting: Course Notes For Seminar 3 Chapter 5: Time Value of Money Part B朱艺璇No ratings yet

- Nmims Sec A Test No 1Document6 pagesNmims Sec A Test No 1ROHAN DESAI100% (1)

- Lec 3Document16 pagesLec 3Dennis Noel de LaraNo ratings yet

- Banking TermiologyDocument4 pagesBanking TermiologyshivankNo ratings yet

- IRV Banikanta Mishra: Practice Assignment - 1Document9 pagesIRV Banikanta Mishra: Practice Assignment - 1SANCHITA PATINo ratings yet

- 02.time Value of Money IIDocument6 pages02.time Value of Money IIMaithri Vidana KariyakaranageNo ratings yet

- FIMA ReviewerDocument6 pagesFIMA ReviewerGoya TinderaNo ratings yet

- 02.time Value of Money III and Risk and Return IDocument4 pages02.time Value of Money III and Risk and Return IMaithri Vidana Kariyakaranage100% (1)

- Time Value of MoneyDocument44 pagesTime Value of MoneyerickavillongalvanNo ratings yet

- Week 6 - Types of Debt Securities Types of Debt Securities - Inflation Indexed Bond, ZCB, DDBDocument7 pagesWeek 6 - Types of Debt Securities Types of Debt Securities - Inflation Indexed Bond, ZCB, DDBKeigan ChatterjeeNo ratings yet

- CD Currency DerivativesDocument8 pagesCD Currency DerivativesSourabh MadanNo ratings yet

- UntitledDocument34 pagesUntitledXoan DươngNo ratings yet

- Term Loan: Presented byDocument24 pagesTerm Loan: Presented byShailesh ShettyNo ratings yet

- Example SwapDocument10 pagesExample SwapThanh Huyền TrầnNo ratings yet

- Bank RateDocument4 pagesBank RateAnonymous Ne9hTRNo ratings yet

- KUMARADocument8 pagesKUMARAKUMARAGURU PONRAJNo ratings yet

- Presentation Bond Analysis.Document16 pagesPresentation Bond Analysis.mij60No ratings yet

- Notes On Interest RatesDocument3 pagesNotes On Interest RatesKhawar Munir GorayaNo ratings yet

- Dual-Currency Private PlacementsDocument6 pagesDual-Currency Private PlacementsSimon AltkornNo ratings yet

- Asset Class RDDocument11 pagesAsset Class RDYuvi DudejaNo ratings yet

- International Fund Management in RINLDocument3 pagesInternational Fund Management in RINLvenkatadeepaksNo ratings yet

- AFM 2: Interest Rate Swaps: S Krishnamoorthy:, Cell:9821461488Document24 pagesAFM 2: Interest Rate Swaps: S Krishnamoorthy:, Cell:9821461488Johar MenezesNo ratings yet

- Loan and AdvancesDocument9 pagesLoan and AdvancesSumit NaugraiyaNo ratings yet

- Bond ValuationDocument1 pageBond Valuationairish21081501No ratings yet

- Fixed DepositsDocument16 pagesFixed DepositsAlok SinghNo ratings yet

- Types of Bank Accounts in IndiaDocument3 pagesTypes of Bank Accounts in IndiaVasudev GovindanNo ratings yet

- Currency SwapDocument5 pagesCurrency SwapSachin RanadeNo ratings yet

- BFIN Week 11-20Document14 pagesBFIN Week 11-20KingDyther Velasco92% (13)

- Financial Risk Management - SWAPDocument23 pagesFinancial Risk Management - SWAPChau NguyenNo ratings yet

- Eco 531 - Chapter 4Document46 pagesEco 531 - Chapter 4Nurul Aina IzzatiNo ratings yet

- Flat Interest Rate Vs Reducing Balance Interest Rate Calculator CashkumarDocument1 pageFlat Interest Rate Vs Reducing Balance Interest Rate Calculator CashkumarSatvant Singh SarwaraNo ratings yet

- Assignment 2Document2 pagesAssignment 2Anil RaiNo ratings yet

- M. SC and M. Phil Diaries: 1. Financial EconomicsDocument14 pagesM. SC and M. Phil Diaries: 1. Financial EconomicsSumra KhanNo ratings yet

- AdmasDocument11 pagesAdmasAbdellah TeshomeNo ratings yet

- Chapter+4 +time+value+of+moneyDocument109 pagesChapter+4 +time+value+of+moneyThảo Nhi LêNo ratings yet

- The Risk-Return Tradeoff Is The Principle That Potential Return Rises With An Increase in RiskDocument15 pagesThe Risk-Return Tradeoff Is The Principle That Potential Return Rises With An Increase in RiskJofanie MeridaNo ratings yet

- AIG TA Claim Procedure 2013 Mar PDFDocument2 pagesAIG TA Claim Procedure 2013 Mar PDFRyan LamNo ratings yet

- HSBC Weekly 2013 - 1 PDFDocument3 pagesHSBC Weekly 2013 - 1 PDFsuperhappysurferNo ratings yet

- Next Generation BankingDocument20 pagesNext Generation BankingyosephNo ratings yet

- Nitin Proect ReportDocument106 pagesNitin Proect ReportNageshwar SinghNo ratings yet

- Ty Warner Filing Ahead of Sentencing On Tax Evasion ConvictionDocument41 pagesTy Warner Filing Ahead of Sentencing On Tax Evasion ConvictionChicago Tribune100% (1)

- MGT (404) Banker-Customer RelationshipDocument33 pagesMGT (404) Banker-Customer RelationshipFerdous AlaminNo ratings yet

- Cosajay V MERS (RI 2013)Document11 pagesCosajay V MERS (RI 2013)Thom Lee ChapmanNo ratings yet

- Derivatives Case StudyDocument4 pagesDerivatives Case StudyPavnesh KumarNo ratings yet

- ISNT Course Calendar For 2023-2024Document5 pagesISNT Course Calendar For 2023-2024Murugesh pNo ratings yet

- Cash Concentration StrategiesDocument11 pagesCash Concentration StrategiesAditya100% (1)

- Instruments of Wealth ManagementDocument3 pagesInstruments of Wealth ManagementHeena JeevaniNo ratings yet

- NWO + MexicoDocument13 pagesNWO + Mexicoharrythehorse3093100% (1)

- DFI and Evolution of ICICI From A DFIDocument50 pagesDFI and Evolution of ICICI From A DFIManoj BharadwajNo ratings yet

- Which Equity Release ReportDocument4 pagesWhich Equity Release ReportStepChangeNo ratings yet

- Malaysia Company Profile (Sample) : Type of No ofDocument1 pageMalaysia Company Profile (Sample) : Type of No ofAditya SharmaNo ratings yet

- PunjabPolice DS PDFDocument1 pagePunjabPolice DS PDFHamza SheikhNo ratings yet

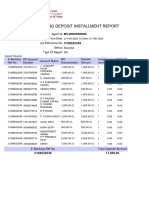

- Recurring Deposit Installment Report: Agent Id: From DateDocument2 pagesRecurring Deposit Installment Report: Agent Id: From DateGirish SapraNo ratings yet

- NABARDDocument46 pagesNABARDMahesh Gaddamedi100% (1)

- G SecDocument14 pagesG SecDhairya VinayakNo ratings yet

- HAMP TIER 2 Supplimental DirectiveDocument22 pagesHAMP TIER 2 Supplimental DirectiveMartin AndelmanNo ratings yet

- Multitech Business School: Department of Professional StudiesDocument5 pagesMultitech Business School: Department of Professional StudiestubenaweambroseNo ratings yet

- United States v. Hoffler-Riddick, 4th Cir. (2007)Document10 pagesUnited States v. Hoffler-Riddick, 4th Cir. (2007)Scribd Government DocsNo ratings yet

- Repaso1, PRIMER AÑODocument8 pagesRepaso1, PRIMER AÑOtowersalar1117No ratings yet

- To Financial Markets: in This Unit We Will Learn As What Is A Financial Market and How Does It WorkDocument6 pagesTo Financial Markets: in This Unit We Will Learn As What Is A Financial Market and How Does It WorksuryamlacwNo ratings yet

- First Investment Bank - BulgariaDocument10 pagesFirst Investment Bank - Bulgariag_sarcevich5427No ratings yet

- IB Tutorial 7 Q1Document2 pagesIB Tutorial 7 Q1Kahseng WooNo ratings yet

- Cityam 2012-10-15Document31 pagesCityam 2012-10-15City A.M.No ratings yet

- Bcash SuitDocument57 pagesBcash SuitAnonymous BLkOv8hKNo ratings yet