Download as docx, pdf, or txt

You might also like

- Jonathan's Last Day: Reading Comprehension QuizDocument3 pagesJonathan's Last Day: Reading Comprehension QuizLoja Vtr43% (7)

- The Model Joint Venture AgreementDocument222 pagesThe Model Joint Venture AgreementWael LotfyNo ratings yet

- Newton Raphson MethodDocument29 pagesNewton Raphson Methodfaizankhan23100% (1)

- Threats To Compliance With The Fundamental PrinciplesDocument5 pagesThreats To Compliance With The Fundamental PrinciplesAbigail SubaNo ratings yet

- Threats To Auditors Independence PDFDocument7 pagesThreats To Auditors Independence PDFJay Mark ReponteNo ratings yet

- FJ EthicsDocument1 pageFJ EthicsFran GutierrezNo ratings yet

- Threats To IndependenceDocument5 pagesThreats To IndependencemadaaamNo ratings yet

- Audit Final ExamDocument9 pagesAudit Final ExamNurfairuz Diyanah RahzaliNo ratings yet

- TOPIC 3 - Threats & Safeguards To The Fundamental PrinciplesDocument30 pagesTOPIC 3 - Threats & Safeguards To The Fundamental PrinciplesVictor JonesNo ratings yet

- Part4A: Applying The Conceptual Framework Actual or Threatened LitigationDocument14 pagesPart4A: Applying The Conceptual Framework Actual or Threatened LitigationPhrexilyn PajarilloNo ratings yet

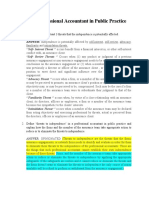

- Section 8 Professional Accountant in Public Practice: Essay QuestionsDocument2 pagesSection 8 Professional Accountant in Public Practice: Essay QuestionsKenneth Marcial Ege IINo ratings yet

- Auditing Theory Part 4Document4 pagesAuditing Theory Part 4DOthz DOrothyNo ratings yet

- Class Synopsis 10 & 11Document11 pagesClass Synopsis 10 & 11Shajib MondolNo ratings yet

- Pervezvikiyo - 3498 - 17836 - 2 - Ethics, Threats & Safeguards (Nov 1, 2021)Document11 pagesPervezvikiyo - 3498 - 17836 - 2 - Ethics, Threats & Safeguards (Nov 1, 2021)Sadia AbidNo ratings yet

- Code of Ethics For AccountantsDocument49 pagesCode of Ethics For AccountantsAlly CapacioNo ratings yet

- Final Audit AssignmentDocument11 pagesFinal Audit Assignmenttaohid khanNo ratings yet

- ACCY342 Tutorial Solutions (CHP 2) s1 2014Document5 pagesACCY342 Tutorial Solutions (CHP 2) s1 2014Bella SeahNo ratings yet

- The Code of Professional EthicsDocument50 pagesThe Code of Professional EthicsMicaela MarimlaNo ratings yet

- Fees - Relative SizeDocument47 pagesFees - Relative SizeJerauld BucolNo ratings yet

- Chapter 3Document56 pagesChapter 3Michael AnthonyNo ratings yet

- Auditing Ethics: Lecture # 2 Fundamental PrinciplesDocument3 pagesAuditing Ethics: Lecture # 2 Fundamental PrinciplessiddiqueicmaNo ratings yet

- Threats and Safeguards On Professional EthicsDocument10 pagesThreats and Safeguards On Professional EthicsAsumpta MunaNo ratings yet

- Germic NotesDocument24 pagesGermic NotesMojiNo ratings yet

- Past Employment With An Assurance ClientDocument3 pagesPast Employment With An Assurance ClientCatherine AcutimNo ratings yet

- SelfDocument2 pagesSelfNeriza PonceNo ratings yet

- Zaraz - Mia by Law 2Document7 pagesZaraz - Mia by Law 2Nur Izzah IlyanaNo ratings yet

- Ethical Issues in Accounting: Course Code: ACT 4102Document23 pagesEthical Issues in Accounting: Course Code: ACT 4102Tanvir AhmedNo ratings yet

- Introduction To Independence and GIP - Jan 2011Document16 pagesIntroduction To Independence and GIP - Jan 2011Praveen MalineniNo ratings yet

- General TheoryDocument5 pagesGeneral TheoryRahulNo ratings yet

- ISO 9001 Auditing Practices Group Guidance On:: Third Party Auditor Impartiality and Conflict of InterestDocument6 pagesISO 9001 Auditing Practices Group Guidance On:: Third Party Auditor Impartiality and Conflict of Interestnicoroman73_2No ratings yet

- COE UnfinishedDocument10 pagesCOE Unfinishedamanda masolutionNo ratings yet

- Impartiality: ISO 9001 Auditing Practices Group Guidance OnDocument6 pagesImpartiality: ISO 9001 Auditing Practices Group Guidance OnGa Ce J ManuelNo ratings yet

- Code of Ethics Flashcards - QuizletDocument73 pagesCode of Ethics Flashcards - QuizletJomar Acar GuittoNo ratings yet

- Audit RiskDocument5 pagesAudit RiskFermie Shell100% (1)

- CAS 220 - IndependenceDocument2 pagesCAS 220 - IndependenceBeeboy CroSelNo ratings yet

- Role PlayDocument2 pagesRole PlayPraise Buenaflor100% (1)

- Suitability of PersonsDocument20 pagesSuitability of Personsjaphethmm01No ratings yet

- 4 Quality ControlDocument10 pages4 Quality ControlMoffat MakambaNo ratings yet

- Papiya (Topic 12,13)Document9 pagesPapiya (Topic 12,13)Taher Uz-zaman ImranNo ratings yet

- At.1304 - Code of EthicsDocument29 pagesAt.1304 - Code of EthicsSheila Mae PlanciaNo ratings yet

- MAS 4 TOPIC 1 Threats and Safeguards in The Practice of Accountancy (Reviewer)Document18 pagesMAS 4 TOPIC 1 Threats and Safeguards in The Practice of Accountancy (Reviewer)vintmyoNo ratings yet

- Working in A Lab Risk & AssessmentDocument4 pagesWorking in A Lab Risk & AssessmentMariam KhanNo ratings yet

- AT.1304 - Code of EthicsDocument28 pagesAT.1304 - Code of EthicsUzumaki NarutoNo ratings yet

- Review Questions: Click On The Questions To See AnswersDocument10 pagesReview Questions: Click On The Questions To See AnswersJinjer Ann LanticanNo ratings yet

- Chapter 3Document14 pagesChapter 3Donald HollistNo ratings yet

- Financial Interest in An Audit Client Creates Self Interest ThreatDocument2 pagesFinancial Interest in An Audit Client Creates Self Interest ThreatElai TrinidadNo ratings yet

- Internal ControlDocument14 pagesInternal ControlHemangNo ratings yet

- Ateneo de Davao University: 12:25 - 1:25 PM February 6, 2017Document5 pagesAteneo de Davao University: 12:25 - 1:25 PM February 6, 2017T WNo ratings yet

- 2022-Professional Accountant in BusinessDocument15 pages2022-Professional Accountant in Businessmae acuestaNo ratings yet

- CODE OF ETHICS For Professional Accountants in TheDocument61 pagesCODE OF ETHICS For Professional Accountants in TheDiana Rose BassigNo ratings yet

- Audit ExerciseDocument6 pagesAudit ExerciseAlodia Lulu SmileNo ratings yet

- 1.2. Rayner - Understanding Risk and Its ImportanceDocument6 pages1.2. Rayner - Understanding Risk and Its ImportanceagnesNo ratings yet

- Code of Professional EthicsDocument42 pagesCode of Professional EthicsMariella CatacutanNo ratings yet

- MAS 4 TOPIC 1 Threats and Safeguards in The Practice of AccountancyDocument20 pagesMAS 4 TOPIC 1 Threats and Safeguards in The Practice of AccountancyKezNo ratings yet

- Introduction To Audit and Assurance ServicesDocument61 pagesIntroduction To Audit and Assurance ServicesMAAN SHIN ANGNo ratings yet

- Code of EthicsDocument24 pagesCode of EthicsEman SaeedNo ratings yet

- What Is Auditor Independenc1Document6 pagesWhat Is Auditor Independenc1Neriza PonceNo ratings yet

- Professional Accountants in Public PracticeDocument40 pagesProfessional Accountants in Public PracticeUmmul Khair HasanNo ratings yet

- ACT 141-Module 5 Financial Statement AuditDocument125 pagesACT 141-Module 5 Financial Statement AuditJade Angelie FloresNo ratings yet

- Transfer Dock - Text - 20240201222540Document3 pagesTransfer Dock - Text - 20240201222540Christine Mae BetangcorNo ratings yet

- Hardening by Auditing: A Handbook for Measurably and Immediately Iimrpving the Security Management of Any OrganizationFrom EverandHardening by Auditing: A Handbook for Measurably and Immediately Iimrpving the Security Management of Any OrganizationNo ratings yet

- Chapter 20-Effective Interest Rate: PROBLEM 20-1 Requirement 1Document41 pagesChapter 20-Effective Interest Rate: PROBLEM 20-1 Requirement 1Jodie Ann PajacNo ratings yet

- Introduction To Balance SheetDocument10 pagesIntroduction To Balance SheetJodie Ann PajacNo ratings yet

- Accounting PrinciplesDocument9 pagesAccounting PrinciplesJodie Ann PajacNo ratings yet

- Kinds of WarrantyDocument10 pagesKinds of WarrantyJodie Ann PajacNo ratings yet

- A Seminar Report On: An International Study On A Risk of Cyber TerrorismDocument7 pagesA Seminar Report On: An International Study On A Risk of Cyber TerrorismManish SakalkarNo ratings yet

- Carte Fantome PDFDocument390 pagesCarte Fantome PDFbinzegger100% (1)

- Acid Rain: Kingdom of Saudi Arabia Ministry of Higher Education King Faisal University Dept. of ScienceDocument7 pagesAcid Rain: Kingdom of Saudi Arabia Ministry of Higher Education King Faisal University Dept. of ScienceAl HasaNo ratings yet

- Certificate: Internal External PrincipalDocument36 pagesCertificate: Internal External PrincipalNitesh kuraheNo ratings yet

- Responsibility AccountingDocument14 pagesResponsibility AccountingJignesh TogadiyaNo ratings yet

- Me 04-601Document15 pagesMe 04-601Vishnu DasNo ratings yet

- Wordsearch Fruits Fun Activities Games Games Icebreakers Oneonone Ac - 109759Document2 pagesWordsearch Fruits Fun Activities Games Games Icebreakers Oneonone Ac - 109759raquel lujanNo ratings yet

- Chang 2013Document20 pagesChang 2013Nguyễn HàNo ratings yet

- Umbilical Catheterization in ServiceDocument11 pagesUmbilical Catheterization in ServiceLucian CaelumNo ratings yet

- Application of Negative Stiffness Devices For Seismic Protection of Bridge StructuresDocument10 pagesApplication of Negative Stiffness Devices For Seismic Protection of Bridge StructuresganeshNo ratings yet

- Textiles Mills Waste: Cotton Textile Mill Waste Woolen Textile Mills Waste Synthetic Textile Mill WasteDocument3 pagesTextiles Mills Waste: Cotton Textile Mill Waste Woolen Textile Mills Waste Synthetic Textile Mill WasteAbhishek AryaNo ratings yet

- Notes Receivable and Loan ReceivableDocument21 pagesNotes Receivable and Loan ReceivableLady BelleNo ratings yet

- MCQ Test of PolymerDocument4 pagesMCQ Test of PolymerDrAman Khan Pathan100% (2)

- PPT5-S5 - Problem & Change ManagementDocument29 pagesPPT5-S5 - Problem & Change ManagementDinne RatjNo ratings yet

- Facility Preventive Maintenance ChecklistDocument5 pagesFacility Preventive Maintenance ChecklistFaisalNo ratings yet

- AOS Injury Classification Systems Poster 20200327 THORACOLUMBARDocument1 pageAOS Injury Classification Systems Poster 20200327 THORACOLUMBARRakhmat RamadhaniNo ratings yet

- AWS Command SyntaxDocument2 pagesAWS Command SyntaxOMRoutNo ratings yet

- AnalogyDocument11 pagesAnalogydamuNo ratings yet

- Introduction SlidesDocument23 pagesIntroduction SlidesMathiselvan GopalNo ratings yet

- Koch I. Analysis of Multivariate and High-Dimensional Data 2013Document532 pagesKoch I. Analysis of Multivariate and High-Dimensional Data 2013rciani100% (15)

- IGTM-CT Gas Turbine Meter: Documentation and Technical SpecificationsDocument12 pagesIGTM-CT Gas Turbine Meter: Documentation and Technical Specificationsajitp123No ratings yet

- Investment Analysis and Portfolio Management: Lecture Presentation SoftwareDocument43 pagesInvestment Analysis and Portfolio Management: Lecture Presentation SoftwareNoman KhalidNo ratings yet

- Unit 2 - Basic Instrumentation and Measurement Techniques PPT Notes Material For Sem II Uploaded by Navdeep RaghavDocument72 pagesUnit 2 - Basic Instrumentation and Measurement Techniques PPT Notes Material For Sem II Uploaded by Navdeep Raghavavikool1708No ratings yet

- PRACTICA 3 - Holguino ErnestoDocument6 pagesPRACTICA 3 - Holguino ErnestoErnesto HolguinoNo ratings yet

- Radiation Heat Transfer ExperimentDocument6 pagesRadiation Heat Transfer ExperimentDaniel IsmailNo ratings yet

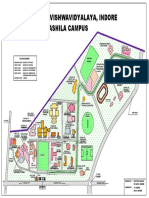

- Devi Ahilya Vishwavidyalaya, Indore Takshashila Campus: Vigyan BhawanDocument1 pageDevi Ahilya Vishwavidyalaya, Indore Takshashila Campus: Vigyan BhawankapasNo ratings yet

- Introduction To Computational Finance and Financial EconometricsDocument54 pagesIntroduction To Computational Finance and Financial EconometricsMR 2No ratings yet