Download as docx, pdf, or txt

You might also like

- Fast FashionDocument23 pagesFast FashionRidhima Tripathi67% (3)

- Exercises: Job Order Costing: Q1: Lamonda Corp. Uses A Job Order Cost System. On April 1, The Accounts Had The FollowingDocument4 pagesExercises: Job Order Costing: Q1: Lamonda Corp. Uses A Job Order Cost System. On April 1, The Accounts Had The FollowingCynthia WongNo ratings yet

- Schaum's Outline of Principles of Accounting I, Fifth EditionFrom EverandSchaum's Outline of Principles of Accounting I, Fifth EditionRating: 5 out of 5 stars5/5 (3)

- Novice HedgeDocument130 pagesNovice HedgeAnujit Kumar100% (6)

- The McGraw-Hill 36-Hour Course: Finance for Non-Financial Managers 3/EFrom EverandThe McGraw-Hill 36-Hour Course: Finance for Non-Financial Managers 3/ERating: 4.5 out of 5 stars4.5/5 (6)

- Assignment 3 Accounting PDFDocument11 pagesAssignment 3 Accounting PDFjgfjhf arwtr100% (1)

- The Challenge of Going GreenDocument29 pagesThe Challenge of Going GreenAmitNo ratings yet

- Investments Test 4 Study Guide (11-14)Document23 pagesInvestments Test 4 Study Guide (11-14)Lauren100% (2)

- Confidential DataDocument12 pagesConfidential Datagayathri bangaramNo ratings yet

- Problem 9.10 SolutionDocument4 pagesProblem 9.10 SolutionPrincess Dhazerene M. ReyesNo ratings yet

- Acco 20073 Discussion Sy2122 (Bsma 2-4)Document81 pagesAcco 20073 Discussion Sy2122 (Bsma 2-4)Paul BandolaNo ratings yet

- Cost AccountingDocument3 pagesCost AccountingRajibNo ratings yet

- Cost Accounting. ActivityDocument6 pagesCost Accounting. ActivityReida DelmasNo ratings yet

- Unit CostingDocument9 pagesUnit Costinggmehul703No ratings yet

- Cost 1 and Cost 2 Compilation of Quizzes and Brain Teasers With Solutions in ProblemsDocument19 pagesCost 1 and Cost 2 Compilation of Quizzes and Brain Teasers With Solutions in ProblemsKieNo ratings yet

- Cost Sheet ProblemsDocument5 pagesCost Sheet ProblemsshamilaNo ratings yet

- Preparation of Individual Income Tax Return For Mixed Income EarnerDocument3 pagesPreparation of Individual Income Tax Return For Mixed Income Earnercarl patNo ratings yet

- Cost Accounting Adc Bcom Part 2 Solved Past Paper 2016Document8 pagesCost Accounting Adc Bcom Part 2 Solved Past Paper 2016Imran JuttNo ratings yet

- Assignment 3 Managerial Accounting: Submitted By-Ghayoor Zafar Submitted To - DR MohsinDocument11 pagesAssignment 3 Managerial Accounting: Submitted By-Ghayoor Zafar Submitted To - DR Mohsinjgfjhf arwtr100% (1)

- Solution of Advanced Cost SheetDocument2 pagesSolution of Advanced Cost SheetHebaNo ratings yet

- HorngrenIMA14eSM ch04Document75 pagesHorngrenIMA14eSM ch04Zarafshan Gul Gul MuhammadNo ratings yet

- 2 Manufacturing ProblemsDocument18 pages2 Manufacturing Problemsone dev onliNo ratings yet

- Costcon 1Document3 pagesCostcon 1Frances Clayne GonzalvoNo ratings yet

- Basic Cost Accounting DefinitionsDocument8 pagesBasic Cost Accounting Definitionsbritonkariuki97No ratings yet

- Lecture 3 Job Order CostingDocument20 pagesLecture 3 Job Order CostingTheresa RoqueNo ratings yet

- FS Financial StudyDocument6 pagesFS Financial StudyMarina AbanNo ratings yet

- Practical Problems and Solution of Cost SheetDocument7 pagesPractical Problems and Solution of Cost SheetAdityasai Gudimalla75% (4)

- Quiz Feb24Document5 pagesQuiz Feb24E RDNo ratings yet

- CA Inter Costing QFP Solutions Ebook - CA Ganesh BharadwajDocument103 pagesCA Inter Costing QFP Solutions Ebook - CA Ganesh Bharadwajsubasha1a1No ratings yet

- Cost Activity 1Document12 pagesCost Activity 1Dark Ninja100% (1)

- 07 Reconciliation FTDocument7 pages07 Reconciliation FTnsm2zmvnbbNo ratings yet

- Statement of COGSDocument3 pagesStatement of COGSIan CalinawanNo ratings yet

- Drill12 Drill13 Manufacturing BusinesDocument6 pagesDrill12 Drill13 Manufacturing BusinesAngelo FelizardoNo ratings yet

- Addisu Tadesse Adj FSDocument6 pagesAddisu Tadesse Adj FSGali AbamededNo ratings yet

- (New Account Titles and Financial Statements) : Module 8: Introduction To Manufacturing OperationDocument4 pages(New Account Titles and Financial Statements) : Module 8: Introduction To Manufacturing OperationAshitero YoNo ratings yet

- DAIBB MA Math Solutions 290315Document11 pagesDAIBB MA Math Solutions 290315joyNo ratings yet

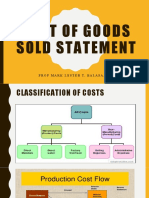

- Cost of Goods Sold StatementDocument18 pagesCost of Goods Sold StatementCherrylane EdicaNo ratings yet

- BSMA 1A Quiz 3 Cost Accounting CycleDocument5 pagesBSMA 1A Quiz 3 Cost Accounting CycleMaeca Angela SerranoNo ratings yet

- Cost Accounting MidDocument7 pagesCost Accounting MidHuma NadeemNo ratings yet

- Unit - Ii Cost and Management AccountingDocument17 pagesUnit - Ii Cost and Management AccountingRamakrishna RoshanNo ratings yet

- Cost Sheet Prepation-NotesDocument12 pagesCost Sheet Prepation-NotesSunita BasakNo ratings yet

- Manufacturing OperationsDocument14 pagesManufacturing OperationsGet BurnNo ratings yet

- Answer To Exercises To AnswerDocument9 pagesAnswer To Exercises To AnswerLEONNA BEATRIZ LOPEZNo ratings yet

- Accounting For Managers Canadian 1st Edition Collier Solutions ManualDocument17 pagesAccounting For Managers Canadian 1st Edition Collier Solutions Manualnicholassmithyrmkajxiet100% (28)

- F.Y.B.B.A Sem 1 Financial Accounting Unit CostingDocument3 pagesF.Y.B.B.A Sem 1 Financial Accounting Unit CostingSamir ParekhNo ratings yet

- Activity 2.2 Answer Key Pre Test Normal Costing Answer KeyDocument14 pagesActivity 2.2 Answer Key Pre Test Normal Costing Answer KeyJamesNo ratings yet

- Abellano - Activity 1 & 2Document4 pagesAbellano - Activity 1 & 2Nelia AbellanoNo ratings yet

- Cost Accounting AssignmentDocument6 pagesCost Accounting AssignmentCharles BarcelaNo ratings yet

- Villanueva, JaneDocument14 pagesVillanueva, JaneVillanueva, Jane G.No ratings yet

- Problem Lecture - MANUFACTURING 2 With ANSWERSDocument4 pagesProblem Lecture - MANUFACTURING 2 With ANSWERSNia BranzuelaNo ratings yet

- Sdathn Ripsryd@r@ea@pis - Unit) : - SolutionDocument16 pagesSdathn Ripsryd@r@ea@pis - Unit) : - SolutionAnimesh VoraNo ratings yet

- P4 Costing Solutions To QFPDocument96 pagesP4 Costing Solutions To QFPparithinilavan07No ratings yet

- Cost AccountingDocument2 pagesCost AccountingMaricar RoqueNo ratings yet

- CMA Vol 1-1Document211 pagesCMA Vol 1-1Shahaer MumtazNo ratings yet

- Midterm Review QuestionsDocument6 pagesMidterm Review QuestionsnamiyuartsNo ratings yet

- Takehome - Quiz - Manac - Docx Filename - UTF-8''Takehome Quiz Manac-1Document3 pagesTakehome - Quiz - Manac - Docx Filename - UTF-8''Takehome Quiz Manac-1Sharmaine SurNo ratings yet

- Chapter 3 Cost Accounting Cycle Multiple Choice - TheoriesDocument36 pagesChapter 3 Cost Accounting Cycle Multiple Choice - TheoriesAyra Pelenio100% (2)

- Jawaban Perhitungan Dan Akumulasi BiayaDocument7 pagesJawaban Perhitungan Dan Akumulasi BiayaEka OematanNo ratings yet

- Financial and Management and Accouting MBA0041 Assingment FALL 2014 LC-02009 Name: Nandeshwar Singh ROLL NO.1408001255Document7 pagesFinancial and Management and Accouting MBA0041 Assingment FALL 2014 LC-02009 Name: Nandeshwar Singh ROLL NO.1408001255Nageshwar singhNo ratings yet

- BSA 2B Roco, Xyriene Von Briel MDocument8 pagesBSA 2B Roco, Xyriene Von Briel MXyriene RocoNo ratings yet

- Course Name: Cost and Management: Question No 1 Schedule For Purchases of Raw MaterialDocument4 pagesCourse Name: Cost and Management: Question No 1 Schedule For Purchases of Raw Materialyasir shahNo ratings yet

- Cost Sheet 1Document6 pagesCost Sheet 1Tamilselvi ANo ratings yet

- 625009eef26fe Cost Accounting and Cost Management 1 Quiz No. 2Document2 pages625009eef26fe Cost Accounting and Cost Management 1 Quiz No. 2El Jehn Grace Babor - Ledesma100% (1)

- Bacolod, Queenie Rose C. BSA2-B Summary of Answers Problem 5-Chapter 3 Requirement 1-Journal EntriesDocument7 pagesBacolod, Queenie Rose C. BSA2-B Summary of Answers Problem 5-Chapter 3 Requirement 1-Journal EntriesQueenie Rose BacolodNo ratings yet

- Chapter 1 5Document52 pagesChapter 1 5chen NituradaNo ratings yet

- Project Cost Control in The Nigerian Construction IndustryDocument7 pagesProject Cost Control in The Nigerian Construction IndustryChun LimNo ratings yet

- National Book Store Success StoryDocument3 pagesNational Book Store Success StoryMj Gutierrez0% (1)

- Vitara Brezza MMC BrochureDocument12 pagesVitara Brezza MMC BrochureRajnesh RkNo ratings yet

- Amazon Financial Statement Analysis PT 2 PaperDocument5 pagesAmazon Financial Statement Analysis PT 2 Paperapi-242679288No ratings yet

- Warranty Claim Procedure ManualDocument28 pagesWarranty Claim Procedure ManualjorgegachaNo ratings yet

- Competition Act 2002Document37 pagesCompetition Act 2002Anonymous jnuQN8No ratings yet

- Pampers 7 PDFDocument10 pagesPampers 7 PDFAdeelNo ratings yet

- MathDocument10 pagesMathJustine TabanaoNo ratings yet

- 2006 FaridaDocument22 pages2006 FaridaGió Vi VuNo ratings yet

- Fomc Statements - Side-By-sideDocument2 pagesFomc Statements - Side-By-sideurbanovNo ratings yet

- Quotation Form PDFDocument4 pagesQuotation Form PDFRhandee GarlítosNo ratings yet

- ECON 425 AssignmentDocument2 pagesECON 425 AssignmentGeorge CheungNo ratings yet

- 0455 Economics ChecklistDocument10 pages0455 Economics ChecklistsallyohhNo ratings yet

- Powerpoint Lectures For Principles of Economics, 9E by Karl E. Case, Ray C. Fair & Sharon M. OsterDocument50 pagesPowerpoint Lectures For Principles of Economics, 9E by Karl E. Case, Ray C. Fair & Sharon M. OsterPrisca Wahyu HNo ratings yet

- How To Read Stock ChartsDocument36 pagesHow To Read Stock Chartsnayan kumar duttaNo ratings yet

- FM Quiz #3 SET 1Document2 pagesFM Quiz #3 SET 1Cjhay MarcosNo ratings yet

- Request Repo FormDocument30 pagesRequest Repo Formana bagolorNo ratings yet

- MOP-Capital Theory Assignment-020310Document4 pagesMOP-Capital Theory Assignment-020310charnu1988No ratings yet

- Parkin12e Economics Ch09Document39 pagesParkin12e Economics Ch09Lamia SiddiquiNo ratings yet

- KahootDocument4 pagesKahootDNo ratings yet

- Direct Material CostDocument29 pagesDirect Material CostRaj DharodNo ratings yet

- CT8 - P XS - 13: Series X SolutionsDocument82 pagesCT8 - P XS - 13: Series X SolutionsTuff BubaNo ratings yet

- Tax - ProjectDocument14 pagesTax - ProjectFatima BrionesNo ratings yet

- MCQ On National Income PptsDocument82 pagesMCQ On National Income Pptsdheeraj0650% (4)