1st Course

1st Course

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5820)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (898)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- F80B F100D: Service ManualDocument249 pagesF80B F100D: Service ManualIvan Alvarez OrtizNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- StatisticsDocument2 pagesStatisticsEhab hoba100% (1)

- Farmers First FormatDocument9 pagesFarmers First FormatAkhil ANo ratings yet

- CH 5 Audit-Planning MCQDocument3 pagesCH 5 Audit-Planning MCQEhab hoba0% (1)

- 3 - Lecture 3 Classified Balance SheetDocument11 pages3 - Lecture 3 Classified Balance SheetEhab hobaNo ratings yet

- CH 13Document40 pagesCH 13Ehab hobaNo ratings yet

- Insurance Is Defined As: E) All of The AboveDocument6 pagesInsurance Is Defined As: E) All of The AboveEhab hobaNo ratings yet

- قوانين محاسبه اداريهDocument4 pagesقوانين محاسبه اداريهEhab hobaNo ratings yet

- Choose The Best Answer::: Statistical TechniquesDocument3 pagesChoose The Best Answer::: Statistical TechniquesEhab hoba100% (1)

- 1 - Lecture 1 Introduction To AccountingDocument13 pages1 - Lecture 1 Introduction To AccountingEhab hobaNo ratings yet

- Ch2 4 ProblemsDocument5 pagesCh2 4 ProblemsEhab hobaNo ratings yet

- Mathematics of Finance: Chapter 3-C Compound InterestDocument1 pageMathematics of Finance: Chapter 3-C Compound InterestEhab hobaNo ratings yet

- Ch2 4 ProblemsDocument1 pageCh2 4 ProblemsEhab hobaNo ratings yet

- Cost Revision: Income Statement Using Contribution Margin Traditional Format of Income StatementDocument6 pagesCost Revision: Income Statement Using Contribution Margin Traditional Format of Income StatementEhab hobaNo ratings yet

- CH9Document3 pagesCH9Ehab hobaNo ratings yet

- Adjusted Trial Balances Home Office Branch Income StatementDocument3 pagesAdjusted Trial Balances Home Office Branch Income StatementEhab hobaNo ratings yet

- 20 نموذج امتحان نصف العام للصف الثالث الابتدائي لمنهج Time for EnglishDocument40 pages20 نموذج امتحان نصف العام للصف الثالث الابتدائي لمنهج Time for EnglishEhab hobaNo ratings yet

- Accrued RevenueDocument2 pagesAccrued RevenueEhab hobaNo ratings yet

- Regional Trial Courts BranchesDocument26 pagesRegional Trial Courts BranchesJacinto Jr Jamero50% (2)

- Services Quality Analysis in SBI and Axis Bank (Awadesh)Document58 pagesServices Quality Analysis in SBI and Axis Bank (Awadesh)jaganath121No ratings yet

- The Travel & Tourism Competitiveness ReportDocument19 pagesThe Travel & Tourism Competitiveness ReportFriti FritiNo ratings yet

- Industrial Visit Report of Dic KollamDocument10 pagesIndustrial Visit Report of Dic Kollamarjun lalNo ratings yet

- UI U12 Revision PDFDocument2 pagesUI U12 Revision PDFBenjamíns Eduardo SegoviaNo ratings yet

- 57th Campus Placement Brochure 2023 NewDocument12 pages57th Campus Placement Brochure 2023 NewGarima JainNo ratings yet

- CERI Idemitsu Astomos Meeting Midstream DonwstreamDocument31 pagesCERI Idemitsu Astomos Meeting Midstream DonwstreamesojzzucNo ratings yet

- Money, Output and Inflation in Classical Economics : Roy. GreenDocument27 pagesMoney, Output and Inflation in Classical Economics : Roy. GreenBruno DuarteNo ratings yet

- Linda and Steve Simmons Application Part 5Document9 pagesLinda and Steve Simmons Application Part 5mohamedamine.zemouriNo ratings yet

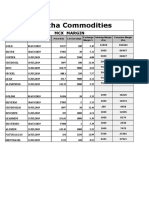

- Astha Commodities: MCX MarginDocument1 pageAstha Commodities: MCX MarginRenjithNo ratings yet

- Indonesia Stainless Steel MarketDocument4 pagesIndonesia Stainless Steel MarketAgustina EffendyNo ratings yet

- Export Promotion Front ProjectDocument13 pagesExport Promotion Front ProjectBikash Kumar NayakNo ratings yet

- Chandler Vargo 2011 MTDocument25 pagesChandler Vargo 2011 MTTariq Waheed QureshiNo ratings yet

- Contemp Quiz 3 Score 9 10Document9 pagesContemp Quiz 3 Score 9 10Charlz Joshua CruzNo ratings yet

- Reff No.0001/LOI/CKW/V/2017: Letter of Intent (Loi)Document3 pagesReff No.0001/LOI/CKW/V/2017: Letter of Intent (Loi)M Hadi MulyantoNo ratings yet

- Political & Legal Environment: MKTG7506: International Marketing Management (S1-2010) 22 March 2010Document11 pagesPolitical & Legal Environment: MKTG7506: International Marketing Management (S1-2010) 22 March 2010Princess KhanNo ratings yet

- Humanizing GlobalizationDocument3 pagesHumanizing GlobalizationEmad Adel Abu SafiahNo ratings yet

- Curtis TurbineDocument18 pagesCurtis TurbineDivya Prakash SrivastavaNo ratings yet

- Rich Dad ScamsDocument26 pagesRich Dad ScamsIustina Haroianu100% (13)

- Bank Receipt VoucherDocument20 pagesBank Receipt VoucherDevi Ayu100% (1)

- Law On Taxation Review.-Chapter 1Document17 pagesLaw On Taxation Review.-Chapter 1GeeanNo ratings yet

- Land Acquisition ActDocument5 pagesLand Acquisition ActDees_24No ratings yet

- Ancient China WebquestDocument2 pagesAncient China Webquestapi-234908816100% (1)

- RCDC SWOT Analysis - Tech Manufacturing FirmsDocument6 pagesRCDC SWOT Analysis - Tech Manufacturing FirmsPaul Michael AngeloNo ratings yet

- Most Visited Countries by International Tourist Arrivals: US$ Euro Real TermsDocument6 pagesMost Visited Countries by International Tourist Arrivals: US$ Euro Real TermsCrazyguy VikzNo ratings yet

- PriceDocument8 pagesPriceWEBTREE TECHNOLOGYNo ratings yet

- Lecture Note 2 Thinking Like An EconomistDocument29 pagesLecture Note 2 Thinking Like An EconomistShourav Roy 1530951030No ratings yet

Download as doc, pdf, or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5820)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (898)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- F80B F100D: Service ManualDocument249 pagesF80B F100D: Service ManualIvan Alvarez OrtizNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- StatisticsDocument2 pagesStatisticsEhab hoba100% (1)

- Farmers First FormatDocument9 pagesFarmers First FormatAkhil ANo ratings yet

- CH 5 Audit-Planning MCQDocument3 pagesCH 5 Audit-Planning MCQEhab hoba0% (1)

- 3 - Lecture 3 Classified Balance SheetDocument11 pages3 - Lecture 3 Classified Balance SheetEhab hobaNo ratings yet

- CH 13Document40 pagesCH 13Ehab hobaNo ratings yet

- Insurance Is Defined As: E) All of The AboveDocument6 pagesInsurance Is Defined As: E) All of The AboveEhab hobaNo ratings yet

- قوانين محاسبه اداريهDocument4 pagesقوانين محاسبه اداريهEhab hobaNo ratings yet

- Choose The Best Answer::: Statistical TechniquesDocument3 pagesChoose The Best Answer::: Statistical TechniquesEhab hoba100% (1)

- 1 - Lecture 1 Introduction To AccountingDocument13 pages1 - Lecture 1 Introduction To AccountingEhab hobaNo ratings yet

- Ch2 4 ProblemsDocument5 pagesCh2 4 ProblemsEhab hobaNo ratings yet

- Mathematics of Finance: Chapter 3-C Compound InterestDocument1 pageMathematics of Finance: Chapter 3-C Compound InterestEhab hobaNo ratings yet

- Ch2 4 ProblemsDocument1 pageCh2 4 ProblemsEhab hobaNo ratings yet

- Cost Revision: Income Statement Using Contribution Margin Traditional Format of Income StatementDocument6 pagesCost Revision: Income Statement Using Contribution Margin Traditional Format of Income StatementEhab hobaNo ratings yet

- CH9Document3 pagesCH9Ehab hobaNo ratings yet

- Adjusted Trial Balances Home Office Branch Income StatementDocument3 pagesAdjusted Trial Balances Home Office Branch Income StatementEhab hobaNo ratings yet

- 20 نموذج امتحان نصف العام للصف الثالث الابتدائي لمنهج Time for EnglishDocument40 pages20 نموذج امتحان نصف العام للصف الثالث الابتدائي لمنهج Time for EnglishEhab hobaNo ratings yet

- Accrued RevenueDocument2 pagesAccrued RevenueEhab hobaNo ratings yet

- Regional Trial Courts BranchesDocument26 pagesRegional Trial Courts BranchesJacinto Jr Jamero50% (2)

- Services Quality Analysis in SBI and Axis Bank (Awadesh)Document58 pagesServices Quality Analysis in SBI and Axis Bank (Awadesh)jaganath121No ratings yet

- The Travel & Tourism Competitiveness ReportDocument19 pagesThe Travel & Tourism Competitiveness ReportFriti FritiNo ratings yet

- Industrial Visit Report of Dic KollamDocument10 pagesIndustrial Visit Report of Dic Kollamarjun lalNo ratings yet

- UI U12 Revision PDFDocument2 pagesUI U12 Revision PDFBenjamíns Eduardo SegoviaNo ratings yet

- 57th Campus Placement Brochure 2023 NewDocument12 pages57th Campus Placement Brochure 2023 NewGarima JainNo ratings yet

- CERI Idemitsu Astomos Meeting Midstream DonwstreamDocument31 pagesCERI Idemitsu Astomos Meeting Midstream DonwstreamesojzzucNo ratings yet

- Money, Output and Inflation in Classical Economics : Roy. GreenDocument27 pagesMoney, Output and Inflation in Classical Economics : Roy. GreenBruno DuarteNo ratings yet

- Linda and Steve Simmons Application Part 5Document9 pagesLinda and Steve Simmons Application Part 5mohamedamine.zemouriNo ratings yet

- Astha Commodities: MCX MarginDocument1 pageAstha Commodities: MCX MarginRenjithNo ratings yet

- Indonesia Stainless Steel MarketDocument4 pagesIndonesia Stainless Steel MarketAgustina EffendyNo ratings yet

- Export Promotion Front ProjectDocument13 pagesExport Promotion Front ProjectBikash Kumar NayakNo ratings yet

- Chandler Vargo 2011 MTDocument25 pagesChandler Vargo 2011 MTTariq Waheed QureshiNo ratings yet

- Contemp Quiz 3 Score 9 10Document9 pagesContemp Quiz 3 Score 9 10Charlz Joshua CruzNo ratings yet

- Reff No.0001/LOI/CKW/V/2017: Letter of Intent (Loi)Document3 pagesReff No.0001/LOI/CKW/V/2017: Letter of Intent (Loi)M Hadi MulyantoNo ratings yet

- Political & Legal Environment: MKTG7506: International Marketing Management (S1-2010) 22 March 2010Document11 pagesPolitical & Legal Environment: MKTG7506: International Marketing Management (S1-2010) 22 March 2010Princess KhanNo ratings yet

- Humanizing GlobalizationDocument3 pagesHumanizing GlobalizationEmad Adel Abu SafiahNo ratings yet

- Curtis TurbineDocument18 pagesCurtis TurbineDivya Prakash SrivastavaNo ratings yet

- Rich Dad ScamsDocument26 pagesRich Dad ScamsIustina Haroianu100% (13)

- Bank Receipt VoucherDocument20 pagesBank Receipt VoucherDevi Ayu100% (1)

- Law On Taxation Review.-Chapter 1Document17 pagesLaw On Taxation Review.-Chapter 1GeeanNo ratings yet

- Land Acquisition ActDocument5 pagesLand Acquisition ActDees_24No ratings yet

- Ancient China WebquestDocument2 pagesAncient China Webquestapi-234908816100% (1)

- RCDC SWOT Analysis - Tech Manufacturing FirmsDocument6 pagesRCDC SWOT Analysis - Tech Manufacturing FirmsPaul Michael AngeloNo ratings yet

- Most Visited Countries by International Tourist Arrivals: US$ Euro Real TermsDocument6 pagesMost Visited Countries by International Tourist Arrivals: US$ Euro Real TermsCrazyguy VikzNo ratings yet

- PriceDocument8 pagesPriceWEBTREE TECHNOLOGYNo ratings yet

- Lecture Note 2 Thinking Like An EconomistDocument29 pagesLecture Note 2 Thinking Like An EconomistShourav Roy 1530951030No ratings yet