Download as pdf or txt

You might also like

- 2023 Calgary DT Report 3 Reduced FinalDocument78 pages2023 Calgary DT Report 3 Reduced FinalCTV Calgary DigitalNo ratings yet

- Ward 9 GreenLine Station Design FeedbackDocument17 pagesWard 9 GreenLine Station Design FeedbackDarren KrauseNo ratings yet

- CREST Final ReportDocument21 pagesCREST Final ReportDarren KrauseNo ratings yet

- BPR at Nike: Submitted By:-Krishan Pal B.E (Chem) Int MBA, 5 Year CM15216Document8 pagesBPR at Nike: Submitted By:-Krishan Pal B.E (Chem) Int MBA, 5 Year CM15216krishan pal100% (1)

- MBTA Orange and Red Line Cars RFPDocument13 pagesMBTA Orange and Red Line Cars RFPNate BoroyanNo ratings yet

- Environmental Assessment For Birmingham Regional Intermodal FacilityDocument520 pagesEnvironmental Assessment For Birmingham Regional Intermodal FacilityJoe OpenshawNo ratings yet

- World Bank Report On The Standard Gauge RailwayDocument5 pagesWorld Bank Report On The Standard Gauge RailwayMaskani Ya Taifa100% (2)

- Seven Secrets Boxing FootworkDocument25 pagesSeven Secrets Boxing Footworkehassan4288% (16)

- Rajashree 2Document5 pagesRajashree 2Vinay BansalNo ratings yet

- Estimation of Costs of Heavy Vehicle Use Per Vehicle-Kilometre in CanadaDocument71 pagesEstimation of Costs of Heavy Vehicle Use Per Vehicle-Kilometre in Canada07103091No ratings yet

- DoE RFI Response - ICCTDocument15 pagesDoE RFI Response - ICCTThe International Council on Clean TransportationNo ratings yet

- Rail Feasibility Study Appendix FDocument4 pagesRail Feasibility Study Appendix FKushal DagliNo ratings yet

- Graver Frey 2013 TRR Locomotive Dyno RYDocument24 pagesGraver Frey 2013 TRR Locomotive Dyno RYJavier Lopez DonosoNo ratings yet

- WIMpaper Anonymous Revised v2Document23 pagesWIMpaper Anonymous Revised v2Syria MostakNo ratings yet

- Commuter Rail Update 11-05-12Document3 pagesCommuter Rail Update 11-05-12Ann Arbor Government DocumentsNo ratings yet

- Quantifying Fuel Saving Benefit of Low Rolling - 2022 - Transportation ResearchDocument17 pagesQuantifying Fuel Saving Benefit of Low Rolling - 2022 - Transportation ResearchhanyNo ratings yet

- New Bus Purchase Staff ReportDocument12 pagesNew Bus Purchase Staff ReportMetro Los AngelesNo ratings yet

- VendorGuidelines CoreDocument40 pagesVendorGuidelines CoreAyush BansalNo ratings yet

- Benders-and-Price Approach For Electric Vehicle Charging Station Location Problem Under Probabilistic Travel RangeDocument35 pagesBenders-and-Price Approach For Electric Vehicle Charging Station Location Problem Under Probabilistic Travel RangeDîñ Êsh Chä ÛhâñNo ratings yet

- Calibration HDM 4 Fuel Consumption Model Using A Big Data Approach A UK Case StudyDocument30 pagesCalibration HDM 4 Fuel Consumption Model Using A Big Data Approach A UK Case StudyPiyush SharmaNo ratings yet

- Auckland Metro RCF Working Group 1june2021Document59 pagesAuckland Metro RCF Working Group 1june2021George WoodNo ratings yet

- Battery Electric Bus Initiative: Metro - Shuttlebus ZoomDocument19 pagesBattery Electric Bus Initiative: Metro - Shuttlebus ZoomhimagraNo ratings yet

- Tram Cost-Benefit DataDocument2 pagesTram Cost-Benefit Datarooseveltislander100% (2)

- Hydrogen and Fuel Cells Training - 9 - A Elgowainy - H2 and FCV in The USADocument28 pagesHydrogen and Fuel Cells Training - 9 - A Elgowainy - H2 and FCV in The USAAsian Development Bank - TransportNo ratings yet

- Direct Hydrogen Fuel Cell Electric Vehicle Cost AnalysisDocument10 pagesDirect Hydrogen Fuel Cell Electric Vehicle Cost AnalysisANo ratings yet

- Methodology Development To Locate Hydrogen Stations For The Initial Deployment StageDocument18 pagesMethodology Development To Locate Hydrogen Stations For The Initial Deployment Stage김형진No ratings yet

- Verification of The HDM-4 Fuel Consumption Model Using A Big Data Approach: A UK Case StudyDocument30 pagesVerification of The HDM-4 Fuel Consumption Model Using A Big Data Approach: A UK Case Studyjaafar abdullahNo ratings yet

- Smart Grids: & Electric Drive Transportation's ImpactDocument25 pagesSmart Grids: & Electric Drive Transportation's Impactsetiamohit007No ratings yet

- CORE GuidelinesDocument40 pagesCORE Guidelinesa_sengar1100% (1)

- Transportation Research Part DDocument10 pagesTransportation Research Part DFardzanela SuwartoNo ratings yet

- Hydrogen Distribution InfrastructureDocument12 pagesHydrogen Distribution InfrastructureChirack Singhtony SNo ratings yet

- NEPRA Mechanism For TariffDocument10 pagesNEPRA Mechanism For TariffMuhammad ShahzebNo ratings yet

- Turn RoundDocument50 pagesTurn RoundHanuma ReddyNo ratings yet

- NH Sor 6TH Revision 2018 Combine PDFDocument170 pagesNH Sor 6TH Revision 2018 Combine PDFM/s Gogoi AssociatesNo ratings yet

- Sound Transit - Capital Cost Estimate Update For Projects in Development - Sound TransitDocument54 pagesSound Transit - Capital Cost Estimate Update For Projects in Development - Sound TransitThe UrbanistNo ratings yet

- Oakland Airport Connector Project OverviewDocument9 pagesOakland Airport Connector Project OverviewTransFormCANo ratings yet

- Simulation and Optimization of The Power Station Coal-Fired Logistics System Based On Witness Simulation SoftwareDocument5 pagesSimulation and Optimization of The Power Station Coal-Fired Logistics System Based On Witness Simulation SoftwareSaddam HussainNo ratings yet

- Preface To Rate AnalysisDocument3 pagesPreface To Rate AnalysisRavi ValakrishnanNo ratings yet

- Indian Railways Increasing The Axle Loading: Atul Sonkhla Naveen Tondan Rahul GautamDocument8 pagesIndian Railways Increasing The Axle Loading: Atul Sonkhla Naveen Tondan Rahul Gautam01202No ratings yet

- Haul Truck Fuel Consumption - PublishedDocument6 pagesHaul Truck Fuel Consumption - PublishedSudhaakar MNNo ratings yet

- KRRI To Deploy Hydrogen Fuel Cell Train, Powered by HorizonDocument2 pagesKRRI To Deploy Hydrogen Fuel Cell Train, Powered by HorizonPR.comNo ratings yet

- Vizag Roads Price Steel Cement Rhythm and Blues Asphalt: Price Adjustment Gos & Circulars R&B Department..Document6 pagesVizag Roads Price Steel Cement Rhythm and Blues Asphalt: Price Adjustment Gos & Circulars R&B Department..Anonymous oVmxT9KzrbNo ratings yet

- Land Value Uplift From Light Rail: Cameron K. Murray September 5, 2016Document13 pagesLand Value Uplift From Light Rail: Cameron K. Murray September 5, 2016rupert_j_boothNo ratings yet

- Estimating The Voc Used For Economic Feasibility Analysis of HW Construction Projects (Ranawaka, 2017)Document4 pagesEstimating The Voc Used For Economic Feasibility Analysis of HW Construction Projects (Ranawaka, 2017)Mario SolanoNo ratings yet

- Price Adjustment GOs & Circulars R&B Department...Document37 pagesPrice Adjustment GOs & Circulars R&B Department...Vizag Roads88% (24)

- Us Army..of Hybrid CarsDocument18 pagesUs Army..of Hybrid CarsKiran Moy MandalNo ratings yet

- Wsf2 855 OriginalDocument16 pagesWsf2 855 OriginalCrystal HarrisNo ratings yet

- Hybrid Engine Research PaperDocument8 pagesHybrid Engine Research Paperzijkchbkf100% (1)

- Future Aircraft Fuel EfficiencyDocument92 pagesFuture Aircraft Fuel Efficiencya1rm4n1100% (1)

- Transportation Research B: Okan Arslan, Oya Ekin Kara S AnDocument26 pagesTransportation Research B: Okan Arslan, Oya Ekin Kara S AnDîñ Êsh Chä ÛhâñNo ratings yet

- 2018 Annual Evaluation of Fuel Cell Electric Vehicle Deployment & Hydrogen Fuel Station Network ... (PDFDrive)Document128 pages2018 Annual Evaluation of Fuel Cell Electric Vehicle Deployment & Hydrogen Fuel Station Network ... (PDFDrive)Sachin ZagadeNo ratings yet

- North American Railcar Manufacturing Industry: Strong Backlog, New Orders Losing SteamDocument24 pagesNorth American Railcar Manufacturing Industry: Strong Backlog, New Orders Losing Steambillroberts981No ratings yet

- WHITE PAPER - Cost of New Generating Capacity in PerspectiveDocument12 pagesWHITE PAPER - Cost of New Generating Capacity in Perspectivealiscribd46No ratings yet

- Trends in Railways SectorDocument20 pagesTrends in Railways SectorShaji VkNo ratings yet

- Efh Ausimm PaperDocument7 pagesEfh Ausimm PaperSunny SouravNo ratings yet

- Benchmark Capital Cost For TPSDocument27 pagesBenchmark Capital Cost For TPSdipenkhandhediyaNo ratings yet

- Epri ReportDocument198 pagesEpri ReportsurajbvNo ratings yet

- ICCT Public Comments in Support of The Approval of California's In-Use Locomotive RegulationDocument2 pagesICCT Public Comments in Support of The Approval of California's In-Use Locomotive RegulationThe International Council on Clean TransportationNo ratings yet

- Haul Truck Fuel Consumption and CO2 EmissionDocument5 pagesHaul Truck Fuel Consumption and CO2 EmissionBruna RahdNo ratings yet

- National Roads Authority: Project Appraisal GuidelinesDocument63 pagesNational Roads Authority: Project Appraisal GuidelinesPratish BalaNo ratings yet

- Optimization of Hydrogen Stations in Florida Using The Flow-Refueling Location ModelDocument20 pagesOptimization of Hydrogen Stations in Florida Using The Flow-Refueling Location Model김형진No ratings yet

- Motor Truck Logging Methods Engineering Experiment Station Series, Bulletin No. 12From EverandMotor Truck Logging Methods Engineering Experiment Station Series, Bulletin No. 12No ratings yet

- Train Doctor: Trouble Shooting with Diesel and Electric TractionFrom EverandTrain Doctor: Trouble Shooting with Diesel and Electric TractionNo ratings yet

- Guide to Performance-Based Road Maintenance ContractsFrom EverandGuide to Performance-Based Road Maintenance ContractsNo ratings yet

- Richmond CA Slide Deck Nov 14 2023 Updated Nov 13 2023 OPT 1Document14 pagesRichmond CA Slide Deck Nov 14 2023 Updated Nov 13 2023 OPT 1Darren KrauseNo ratings yet

- Coyote Conflict Response Guide - City of CalgaryDocument33 pagesCoyote Conflict Response Guide - City of CalgaryDarren KrauseNo ratings yet

- New Investment Recommendations - 2024 Calgary BudgetDocument65 pagesNew Investment Recommendations - 2024 Calgary BudgetDarren KrauseNo ratings yet

- Roadside Naturalization Project CalgaryDocument4 pagesRoadside Naturalization Project CalgaryDarren KrauseNo ratings yet

- Calgary Police Employee Survey ResultsDocument118 pagesCalgary Police Employee Survey ResultsDarren KrauseNo ratings yet

- Private Career College Experiences in Alberta (23.04.10)Document21 pagesPrivate Career College Experiences in Alberta (23.04.10)Darren Krause100% (1)

- Home Is Here City of Calgary Housing Strategy 2024 2030Document38 pagesHome Is Here City of Calgary Housing Strategy 2024 2030Darren Krause100% (1)

- Calgary, Edmonton Housing Letter To Federal GovernmentDocument2 pagesCalgary, Edmonton Housing Letter To Federal GovernmentDarren KrauseNo ratings yet

- Additional City of Calgary InvestmentsDocument36 pagesAdditional City of Calgary InvestmentsDarren KrauseNo ratings yet

- Public Transit Safety Strategy - CalgaryDocument49 pagesPublic Transit Safety Strategy - CalgaryDarren KrauseNo ratings yet

- Updated Transit Capital Project Prioritization List 2022 - Route AheadDocument8 pagesUpdated Transit Capital Project Prioritization List 2022 - Route AheadDarren KrauseNo ratings yet

- Attach 3 - Harvie Passage Facility Enhancement Plan - CD2023-0522Document70 pagesAttach 3 - Harvie Passage Facility Enhancement Plan - CD2023-0522Darren KrauseNo ratings yet

- Housing and Affordability Taskforce RecommendationsDocument10 pagesHousing and Affordability Taskforce RecommendationsDarren Krause100% (1)

- Assessing A Closed System As Part of The City of Calgary Transit Safety Strategy - IP2023-0368Document14 pagesAssessing A Closed System As Part of The City of Calgary Transit Safety Strategy - IP2023-0368Darren KrauseNo ratings yet

- Alberta Medical Emergency Services Dispatch ReviewDocument186 pagesAlberta Medical Emergency Services Dispatch ReviewDarren KrauseNo ratings yet

- City of Calgary Anti-Racism Program Strategic PlanDocument36 pagesCity of Calgary Anti-Racism Program Strategic PlanDarren KrauseNo ratings yet

- CED 2023 Highlights2022Document34 pagesCED 2023 Highlights2022Darren KrauseNo ratings yet

- 2022 Quality of Life Report - Calgary FoundationDocument24 pages2022 Quality of Life Report - Calgary FoundationDarren KrauseNo ratings yet

- 2022 FINAL Quality of Life ReportDocument24 pages2022 FINAL Quality of Life ReportDarren KrauseNo ratings yet

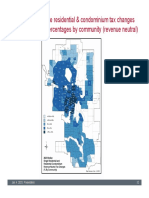

- Revenue Neutral Tax Impact 2023Document1 pageRevenue Neutral Tax Impact 2023Darren KrauseNo ratings yet

- 18th ST SE Adaptive Bike Lane (ABL) Pilot Result Summary Feb 2023Document3 pages18th ST SE Adaptive Bike Lane (ABL) Pilot Result Summary Feb 2023Darren KrauseNo ratings yet

- 18 ST SE StudyDocument4 pages18 ST SE StudyDarren KrauseNo ratings yet

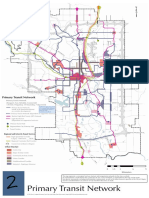

- Primary Transit NetworkDocument1 pagePrimary Transit NetworkDarren KrauseNo ratings yet

- Primary Transit NetworkDocument1 pagePrimary Transit NetworkDarren KrauseNo ratings yet

- Dan McLean - Elections Alberta ReviewDocument6 pagesDan McLean - Elections Alberta ReviewDarren KrauseNo ratings yet

- 2023 2026 Calgary Police Budget 1Document5 pages2023 2026 Calgary Police Budget 1Darren KrauseNo ratings yet

- Executive Summary Airport Transit LineDocument17 pagesExecutive Summary Airport Transit LineDarren KrauseNo ratings yet

- Inglês 11 Classe (Textos Editores) PDFDocument180 pagesInglês 11 Classe (Textos Editores) PDFNota Joao Tembo50% (2)

- Pr. Legalitatii Incriminarii in Dreptul UEDocument9 pagesPr. Legalitatii Incriminarii in Dreptul UEION STEFANETNo ratings yet

- United States v. Hite, 204 U.S. 343 (1907)Document5 pagesUnited States v. Hite, 204 U.S. 343 (1907)Scribd Government DocsNo ratings yet

- Onlinevotingsystem 141129054401 Conversion Gate01Document15 pagesOnlinevotingsystem 141129054401 Conversion Gate01Kamal Yeshodhar Shastry GattuNo ratings yet

- Why We Need The Individual MandateDocument3 pagesWhy We Need The Individual MandateCenter for American ProgressNo ratings yet

- GPHC Standards For Pharmacy ProfessionalsDocument18 pagesGPHC Standards For Pharmacy Professionalsjbpark7255No ratings yet

- 3.32 Max Resources Assignment Brief 2Document3 pages3.32 Max Resources Assignment Brief 2Syed Imam BakharNo ratings yet

- Agreement Copy From Parties - Azzurra Pharmaconutrition PVT - Ltd...............Document4 pagesAgreement Copy From Parties - Azzurra Pharmaconutrition PVT - Ltd...............PUSHKAR PHARMANo ratings yet

- 2020 HSC PhysicsDocument40 pages2020 HSC PhysicsT LinNo ratings yet

- 2007 ConsumercatalogDocument68 pages2007 ConsumercatalogVladimirNo ratings yet

- Kumar Sabnani Org CultureDocument2 pagesKumar Sabnani Org CultureAayushi SinghNo ratings yet

- EOT Crane Maintenance ManualDocument99 pagesEOT Crane Maintenance ManualAvishek DasNo ratings yet

- 37 Associated Communications & Wireless Services v. NTCDocument2 pages37 Associated Communications & Wireless Services v. NTCRuby SantillanaNo ratings yet

- Savage Worlds - The Thin Blue Line - Sample CharactersDocument6 pagesSavage Worlds - The Thin Blue Line - Sample CharactersDanDan_XPNo ratings yet

- Welspun Corp SR2016Document40 pagesWelspun Corp SR2016Gautam LamaNo ratings yet

- Milestone Academy: Class IX - Progress Report - 2020-21Document1 pageMilestone Academy: Class IX - Progress Report - 2020-21Priyansh AnandNo ratings yet

- ASEAN ATM Master Planning Activity 4.2: AgendaDocument6 pagesASEAN ATM Master Planning Activity 4.2: AgendaXA Pakse Pakz ApprNo ratings yet

- Cambridge International AS & A Level: Biology 9700/01Document18 pagesCambridge International AS & A Level: Biology 9700/01Raphael JosephNo ratings yet

- East Delta University Assignment Assessment GuidelineDocument10 pagesEast Delta University Assignment Assessment GuidelineFahim MahmudNo ratings yet

- UNITAS 91 1 Bayani Santos Translating Banaag at Sikat PDFDocument24 pagesUNITAS 91 1 Bayani Santos Translating Banaag at Sikat PDFCharles DoradoNo ratings yet

- ProphetessDocument134 pagesProphetessMarvin Naeto CMNo ratings yet

- 500 Oncology QuestionsDocument52 pages500 Oncology QuestionsCha ChaNo ratings yet

- The Greatest Hoax Serge Monast - Project Blue Beam TranscriptDocument17 pagesThe Greatest Hoax Serge Monast - Project Blue Beam TranscriptMillenium100% (1)

- 0500 FigurativeLanguage TPDocument30 pages0500 FigurativeLanguage TPsabinNo ratings yet

- Steering SOLAS RegulationsDocument2 pagesSteering SOLAS Regulationsmy print100% (1)

- GNLD Carotenoid Complex BrochureDocument2 pagesGNLD Carotenoid Complex BrochureNishit KotakNo ratings yet

- Brl-004 Customerservice Management: Content Digitized by Egyankosh, IgnouDocument13 pagesBrl-004 Customerservice Management: Content Digitized by Egyankosh, IgnouShivatiNo ratings yet

- FansDocument5 pagesFansJoydev Ganguly100% (1)