Download as pdf or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5834)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (903)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (824)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (405)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Final Fund Accounting Study ManualDocument295 pagesFinal Fund Accounting Study ManualAnonymous pQsvSk100% (10)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Application Problem - Gfia101Document45 pagesApplication Problem - Gfia101Dan Lachica NarcisoNo ratings yet

- CGTMSE Application (Revised) FormatDocument4 pagesCGTMSE Application (Revised) FormatdimpleNo ratings yet

- Solution Overview Presentation SAP Treasury and Risk ManagementDocument59 pagesSolution Overview Presentation SAP Treasury and Risk Managementsameer0% (1)

- Practice Questions - Eqty2Document20 pagesPractice Questions - Eqty2gauravroongta67% (3)

- SchwabDocument9 pagesSchwabsanchitaNo ratings yet

- Top 50 Wealth Management Family OfficesDocument1 pageTop 50 Wealth Management Family Officesabelardbonaventura100% (1)

- Merrill LynchDocument18 pagesMerrill LynchVikas Singhal0% (2)

- Financial Statement AnalysisDocument3 pagesFinancial Statement AnalysisMichelle GoNo ratings yet

- Result Presentation For December 31, 2015 (Result)Document27 pagesResult Presentation For December 31, 2015 (Result)Shyam SunderNo ratings yet

- What Is Portfolio ManagementDocument4 pagesWhat Is Portfolio Managementsakpal_smitaNo ratings yet

- Financial Awareness Top 500 QuestionsDocument104 pagesFinancial Awareness Top 500 QuestionsRanjeeth KNo ratings yet

- Thesis Table of ContentsDocument25 pagesThesis Table of ContentsNaina BakshiNo ratings yet

- WorldCom SummaryDocument4 pagesWorldCom Summaryburka123100% (1)

- Principles of FinanceDocument5 pagesPrinciples of FinanceELgün F. QurbanovNo ratings yet

- Equity Swaps 3Document12 pagesEquity Swaps 3gileperNo ratings yet

- List of European Stock ExchangesDocument6 pagesList of European Stock ExchangessaradhahariniNo ratings yet

- Span Margin SystemDocument69 pagesSpan Margin SystemAbhinav KumarNo ratings yet

- On January 1 2012 Parkway Inc Issued Securities With ADocument1 pageOn January 1 2012 Parkway Inc Issued Securities With AMiroslav GegoskiNo ratings yet

- Financial Market & Institution WorksheetDocument5 pagesFinancial Market & Institution WorksheetBobasa S Ahmed100% (1)

- History and Development of Banking in NepalDocument5 pagesHistory and Development of Banking in NepalPRiNCEMagNus100% (2)

- Capital BudgetingDocument37 pagesCapital BudgetingJErome DeGuzman100% (3)

- Banking Regulation Act, 1949Document50 pagesBanking Regulation Act, 1949DrRitesh PatelNo ratings yet

- The Financial Sector Reforms in IndiaDocument6 pagesThe Financial Sector Reforms in IndiahamidfarahiNo ratings yet

- Patient CallingDocument2 pagesPatient CallingKarna Palanivelu100% (2)

- TWSGuide 1 600Document600 pagesTWSGuide 1 600Dimitar DachkinovNo ratings yet

- 4 4 Conversion of A Partnership Firm Into A Company Under Part Ix of The Companies ActDocument8 pages4 4 Conversion of A Partnership Firm Into A Company Under Part Ix of The Companies ActSantosh SinghNo ratings yet

- FS Presentation PPSASDocument12 pagesFS Presentation PPSASMarlyn Cayetano MercadoNo ratings yet

- Credit Risk ModelingDocument3 pagesCredit Risk ModelingsinghhcmNo ratings yet

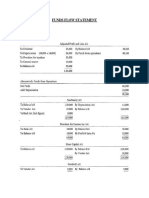

- Funds Flow Statement: Numerical 1Document4 pagesFunds Flow Statement: Numerical 1Neelu AhluwaliaNo ratings yet