Download as pdf or txt

You might also like

- Hydro Case Study MSTM 6032Document17 pagesHydro Case Study MSTM 6032butler_jonathancyahoNo ratings yet

- Civil Works Guidelines For Micro Hydropower in NepalDocument185 pagesCivil Works Guidelines For Micro Hydropower in Nepaljayusman100% (3)

- 4Q16 Earnings Eng FinalDocument18 pages4Q16 Earnings Eng FinalSabin LalNo ratings yet

- Investor Presentation February 2019 PDFDocument31 pagesInvestor Presentation February 2019 PDFkartik jangidNo ratings yet

- Quarterly Update Q1FY22: Century Plyboards (India) LTDDocument10 pagesQuarterly Update Q1FY22: Century Plyboards (India) LTDhackmaverickNo ratings yet

- CJ - Credit SuiseDocument24 pagesCJ - Credit Suisebackup tringuyenNo ratings yet

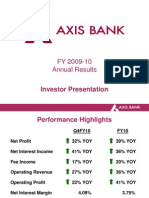

- FY 2009-10 Annual Results: Investor PresentationDocument34 pagesFY 2009-10 Annual Results: Investor PresentationDujesh KardamNo ratings yet

- Brief About The Co Brands Competitive Positioning of The Co / Advantages Tracking Points Financials Incl Shareholding Pattern Valuation Rational SwotDocument42 pagesBrief About The Co Brands Competitive Positioning of The Co / Advantages Tracking Points Financials Incl Shareholding Pattern Valuation Rational SwotMitesh PatilNo ratings yet

- Manappuram Finance Investor PresentationDocument43 pagesManappuram Finance Investor PresentationabmahendruNo ratings yet

- Result Update Presentation - Q1 FY18: AUGUST 10, 2017Document10 pagesResult Update Presentation - Q1 FY18: AUGUST 10, 2017Mohit PariharNo ratings yet

- Earnings Update: Presentation On Financial Results For The Period Ended March 31, 2017Document28 pagesEarnings Update: Presentation On Financial Results For The Period Ended March 31, 2017divya mNo ratings yet

- Mahindra & Mahindra: 3 August 2009Document8 pagesMahindra & Mahindra: 3 August 2009Chandni OzaNo ratings yet

- Maintain NEUTRAL: Acem in CMP Rs 219 Target Rs 191 ( 13%)Document7 pagesMaintain NEUTRAL: Acem in CMP Rs 219 Target Rs 191 ( 13%)9987303726No ratings yet

- 3Q17 Earning Eng FinalDocument18 pages3Q17 Earning Eng FinalarakeelNo ratings yet

- Balkrishna Ind - Ratio Analysis - Altman Z ScoreDocument4 pagesBalkrishna Ind - Ratio Analysis - Altman Z ScoredhruvNo ratings yet

- Cholamandalam Investment & Finance CompanyDocument2 pagesCholamandalam Investment & Finance CompanyAkshit SandoojaNo ratings yet

- Dixon InvestorPresentationJan2022Document12 pagesDixon InvestorPresentationJan2022raguramrNo ratings yet

- Krakatau Steel Case Financial Management Assignment - Syndicate 6Document10 pagesKrakatau Steel Case Financial Management Assignment - Syndicate 6Ayustina GiustiNo ratings yet

- Capa CiteDocument29 pagesCapa CiteParas ChhedaNo ratings yet

- Apollo Hospitals Enterprise Limited NSEI APOLLOHOSP FinancialsDocument40 pagesApollo Hospitals Enterprise Limited NSEI APOLLOHOSP Financialsakumar4uNo ratings yet

- 2018 Aug M&M ReportDocument12 pages2018 Aug M&M ReportVivek shindeNo ratings yet

- Analysts Meet - 2010Document17 pagesAnalysts Meet - 2010shabbir batterywalaNo ratings yet

- TVS Motor Company: CMP: INR549 TP: INR548Document12 pagesTVS Motor Company: CMP: INR549 TP: INR548anujonwebNo ratings yet

- Result Presentation (Result)Document14 pagesResult Presentation (Result)Shyam SunderNo ratings yet

- Reliance Industries: CMP: INR1,077 TP: INR1,057 (-2%)Document18 pagesReliance Industries: CMP: INR1,077 TP: INR1,057 (-2%)Abhiroop DasNo ratings yet

- Review On Financial Statements: Management Discussion & Analysis Quarter Ended 30 September, 2017Document10 pagesReview On Financial Statements: Management Discussion & Analysis Quarter Ended 30 September, 2017nanda rafsanjaniNo ratings yet

- Nokia Results 2022 q4Document33 pagesNokia Results 2022 q4Mukesh SomaniNo ratings yet

- q3 2016 PresentationDocument42 pagesq3 2016 Presentationvmekhasyuk2001No ratings yet

- LPPF 4q18 - NomuraDocument6 pagesLPPF 4q18 - Nomurakrisyanto krisyantoNo ratings yet

- Sun Pharma: CMP: INR909 TP: INR1,000 BuyDocument8 pagesSun Pharma: CMP: INR909 TP: INR1,000 BuyKannan JainNo ratings yet

- Y-O-Y Sales Growth % 18% 19% 12% 10% 1% 9% 2% 11% 2% - 2%Document7 pagesY-O-Y Sales Growth % 18% 19% 12% 10% 1% 9% 2% 11% 2% - 2%muralyyNo ratings yet

- IHCL_Global_Conference_call_presentation_Q4_2022-23Document69 pagesIHCL_Global_Conference_call_presentation_Q4_2022-23prathamshukla0100No ratings yet

- Financial Results Briefing Material For FY2019: April 1, 2018 To March 31, 2019Document30 pagesFinancial Results Briefing Material For FY2019: April 1, 2018 To March 31, 2019choiand1No ratings yet

- Hero Motocorp: CMP: Inr3,707 TP: Inr3,818 (+3%)Document12 pagesHero Motocorp: CMP: Inr3,707 TP: Inr3,818 (+3%)SAHIL SHARMANo ratings yet

- Q3FY22 Result Update DLF LTD.: Strong Residential Performance ContinuesDocument10 pagesQ3FY22 Result Update DLF LTD.: Strong Residential Performance ContinuesVanshika BiyaniNo ratings yet

- Q4FY20 Earning UpdateDocument28 pagesQ4FY20 Earning UpdateSumit SharmaNo ratings yet

- Comparative Peer 4Q 2016Document7 pagesComparative Peer 4Q 2016BGA SustNo ratings yet

- Gabriel IndiaDocument137 pagesGabriel IndiaIshaan MakkerNo ratings yet

- P&L Assumption BS Assumptions P&L Output BS FCFF Wacc DCF ValueDocument66 pagesP&L Assumption BS Assumptions P&L Output BS FCFF Wacc DCF ValuePrabhdeep DadyalNo ratings yet

- Sanghi Industries: CMP: Inr56 TP: INR80 (+44%)Document10 pagesSanghi Industries: CMP: Inr56 TP: INR80 (+44%)Positive ThinkerNo ratings yet

- Mahindra & Mahindra: CMP: INR672 TP: INR810 (+20%)Document14 pagesMahindra & Mahindra: CMP: INR672 TP: INR810 (+20%)Yash DoshiNo ratings yet

- Max Healthcare Institute Limited BSE 543220 FinancialsDocument44 pagesMax Healthcare Institute Limited BSE 543220 Financialssubham kujmarNo ratings yet

- Q2FY24 Post Results Review - SMIFS Institutional ResearchDocument17 pagesQ2FY24 Post Results Review - SMIFS Institutional Researchkrishna_buntyNo ratings yet

- Tata MotorsDocument5 pagesTata Motorsinsurana73No ratings yet

- 4Q17 Earning Eng Final PDFDocument19 pages4Q17 Earning Eng Final PDFPandi IndraNo ratings yet

- Elecon Engineering Limited - in Line With Our EstimatesDocument4 pagesElecon Engineering Limited - in Line With Our EstimatesruchikdoshiNo ratings yet

- BOIPPTNew 06112020Document36 pagesBOIPPTNew 06112020Rohit AggarwalNo ratings yet

- Total Income - Annual: Sales Sales YoyDocument16 pagesTotal Income - Annual: Sales Sales YoyKshatrapati SinghNo ratings yet

- Investor Presentation Q316 FinalDocument23 pagesInvestor Presentation Q316 FinalClary DsilvaNo ratings yet

- Bajaj AnalysisDocument64 pagesBajaj AnalysisKetki PuranikNo ratings yet

- Financial Performance Trend: Sno. ParticularsDocument2 pagesFinancial Performance Trend: Sno. ParticularsASHOK JAINNo ratings yet

- H1 / Q2-Fy19 Earnings Presentation: Everest Industries LimitedDocument27 pagesH1 / Q2-Fy19 Earnings Presentation: Everest Industries LimitedMahamadali DesaiNo ratings yet

- Matrimony Fact Sheet Q2fy18 PDFDocument1 pageMatrimony Fact Sheet Q2fy18 PDFKanchanNo ratings yet

- Asiana Airlines ReportDocument16 pagesAsiana Airlines ReportShiamak FrancoNo ratings yet

- V F Corporation NYSE VFC FinancialsDocument9 pagesV F Corporation NYSE VFC FinancialsAmalia MegaNo ratings yet

- Ashok Leyland: Performance HighlightsDocument9 pagesAshok Leyland: Performance HighlightsSandeep ManglikNo ratings yet

- Presentacion 2019 PDFDocument9 pagesPresentacion 2019 PDFWilsonNo ratings yet

- Hero-MotoCorp - Annual ReportDocument40 pagesHero-MotoCorp - Annual ReportAdarsh DhakaNo ratings yet

- Parag Milk Foods: CMP: INR207 TP: INR255 (+23%) BuyDocument10 pagesParag Milk Foods: CMP: INR207 TP: INR255 (+23%) BuyNiravAcharyaNo ratings yet

- Q307data SumDocument1 pageQ307data SumdiazromeriNo ratings yet

- Ashok Leyland Kotak 050218Document4 pagesAshok Leyland Kotak 050218suprabhattNo ratings yet

- To the Moon Investing: Visually Mapping Your Winning Stock Market PortfolioFrom EverandTo the Moon Investing: Visually Mapping Your Winning Stock Market PortfolioNo ratings yet

- Environment in Serbia FullDocument174 pagesEnvironment in Serbia FullvanjadamjanovicNo ratings yet

- 1 Unit 1 Full Notes of Och752Document13 pages1 Unit 1 Full Notes of Och752G Chandrasekaran100% (1)

- Hy Andritz Hydro enDocument20 pagesHy Andritz Hydro enlufimanNo ratings yet

- DUDBC Hydro GuidelineDocument306 pagesDUDBC Hydro GuidelineDiwakar DiwashNo ratings yet

- IELTS Writing Task 1 LessonsDocument88 pagesIELTS Writing Task 1 LessonsHassan A. Shoukr100% (2)

- Engr. Marjun B. Macasilhig: I. Multiple ChoiceDocument35 pagesEngr. Marjun B. Macasilhig: I. Multiple Choicemaryeonee12No ratings yet

- CE Specializations in The Phils.Document23 pagesCE Specializations in The Phils.DETECTIVE DUCKNo ratings yet

- Hydropower Intake Design and CriteriaDocument6 pagesHydropower Intake Design and CriteriaManikandanNo ratings yet

- 15 - Other Generator Protection - r4Document52 pages15 - Other Generator Protection - r4tajudeen100% (1)

- Pws-Small System Design CalcDocument5 pagesPws-Small System Design CalcAnand TatteNo ratings yet

- Tajikistan 2022: Energy Sector ReviewDocument131 pagesTajikistan 2022: Energy Sector ReviewThea KhitarishviliNo ratings yet

- Diversion Head WorkDocument71 pagesDiversion Head WorkHarish Dutt100% (6)

- Hydro Power Plant Site Selection ParametersDocument25 pagesHydro Power Plant Site Selection ParametersAbdul RafayNo ratings yet

- Hydraulic TransientsDocument58 pagesHydraulic TransientsjulianvillajosNo ratings yet

- Chapter 5 Hydropower - Arun KumarDocument60 pagesChapter 5 Hydropower - Arun KumarSu Crez No AtmajaNo ratings yet

- Activity 2: Hydroelectric Power Plants: Ee133L Power Plant Engineering Laboratory Learning OutcomesDocument8 pagesActivity 2: Hydroelectric Power Plants: Ee133L Power Plant Engineering Laboratory Learning OutcomesErica Villas100% (1)

- CBSE Class 10 Science Chapter 14 Sources of Energy Important Questions 2022-23Document21 pagesCBSE Class 10 Science Chapter 14 Sources of Energy Important Questions 2022-23S MNo ratings yet

- Study On Grid Connected Electricity Baselines in Malaysia PDFDocument35 pagesStudy On Grid Connected Electricity Baselines in Malaysia PDFYusmadi J MohamadNo ratings yet

- MTech EnergyDocument28 pagesMTech EnergyPrashant100% (1)

- Non-Conventional Energy Sources (Semester - 8) : CS/B.TECH (ME) /SEM-8/ME-806/09Document6 pagesNon-Conventional Energy Sources (Semester - 8) : CS/B.TECH (ME) /SEM-8/ME-806/09Krishna Prakash KPNo ratings yet

- Chapter One Classification of Hydroelectric Power PlantsDocument27 pagesChapter One Classification of Hydroelectric Power PlantsKorsa KorsaNo ratings yet

- Annual Progress Report of NRREP 2012.13Document55 pagesAnnual Progress Report of NRREP 2012.13raghurmiNo ratings yet

- Ielts Writing Task 1 - Pie ChartDocument53 pagesIelts Writing Task 1 - Pie ChartAmy HicksNo ratings yet

- Importance of Energy in Society: Module - 8BDocument13 pagesImportance of Energy in Society: Module - 8BJoao LinoNo ratings yet

- Exercise ProblemsDocument1 pageExercise Problemsian heniel100% (1)

- Solar Energy Quality Infrastructure in IndiaDocument82 pagesSolar Energy Quality Infrastructure in IndiaAryyaas ANo ratings yet

- EE TherajaDocument54 pagesEE TherajaJun RyNo ratings yet

- FulltextDocument113 pagesFulltextColleen MurphyNo ratings yet