EFM Chapter 10

EFM Chapter 10

You might also like

- 319 Question BankDocument142 pages319 Question BankElla67% (3)

- Supplementory Lease Deed!!!Document2 pagesSupplementory Lease Deed!!!Saddy Butt67% (3)

- Entrepreneurship Assignment 04: Critique Zipcar: M. Umar Ashraf REG # 2013-IM-23Document9 pagesEntrepreneurship Assignment 04: Critique Zipcar: M. Umar Ashraf REG # 2013-IM-23umar100% (3)

- Invst Reviewer Ver1Document3 pagesInvst Reviewer Ver1evenslzrNo ratings yet

- 03 DCF Valuation M&ADocument47 pages03 DCF Valuation M&AI DNo ratings yet

- PrelimsDocument6 pagesPrelimsJanna Grace Dela CruzNo ratings yet

- Clase III - Information For Investment and ValuationDocument208 pagesClase III - Information For Investment and ValuationMiguel Vega OtinianoNo ratings yet

- Chapter 4 Stock ValuationDocument68 pagesChapter 4 Stock ValuationHalisa HassanNo ratings yet

- Chapter 8Document12 pagesChapter 8Hannah Pauleen G. LabasaNo ratings yet

- F14 Fin PDFDocument13 pagesF14 Fin PDFNageshwar SinghNo ratings yet

- Absolute Vs Relative ValuationDocument3 pagesAbsolute Vs Relative ValuationLilliane EstrellaNo ratings yet

- Principles of Managerial Finance Brief 6th Edition Gitman Solutions ManualDocument38 pagesPrinciples of Managerial Finance Brief 6th Edition Gitman Solutions Manualjomaevelina2980100% (16)

- Bs Finance Chapter 6Document6 pagesBs Finance Chapter 6Erick KibeNo ratings yet

- Company Valuation Summary by Faldi Rev.1Document8 pagesCompany Valuation Summary by Faldi Rev.1Faldi HarisNo ratings yet

- Equity ValuationDocument20 pagesEquity ValuationDorah KahiseNo ratings yet

- Chapter 13 - PortfolioDocument25 pagesChapter 13 - Portfolioapi-308173825No ratings yet

- CORP Finance II Exam NotesDocument12 pagesCORP Finance II Exam NotesTeddie MowerNo ratings yet

- Business Valuation Part 1 Lorelei R. DanilaDocument27 pagesBusiness Valuation Part 1 Lorelei R. DanilaBoongaling, Jose Jr CondeNo ratings yet

- Fin Mar ReviewerDocument2 pagesFin Mar ReviewerPixie CanaveralNo ratings yet

- Market Multiple Valuation Models-Mod - 4Document20 pagesMarket Multiple Valuation Models-Mod - 4Ravichandran RamadassNo ratings yet

- This Study Resource Was: Ms-11: Long Term Equity FinancingDocument4 pagesThis Study Resource Was: Ms-11: Long Term Equity FinancingKathleen Lucas0% (1)

- Risk-Return Trade-Off in Financial Decision MakingDocument12 pagesRisk-Return Trade-Off in Financial Decision MakingAnmol Shrestha0% (1)

- Chapter 5 - NotesDocument2 pagesChapter 5 - NotesLovely CabardoNo ratings yet

- Val Indonesia 2014Document151 pagesVal Indonesia 2014Carlos Jesús Ponce AranedaNo ratings yet

- AFA - 4e - PPT - Chap12 (For Students)Document22 pagesAFA - 4e - PPT - Chap12 (For Students)Cẩm Tú NguyễnNo ratings yet

- Nism CH 10Document13 pagesNism CH 10Darshan JainNo ratings yet

- Referencer For Strategic Financial ManagementDocument24 pagesReferencer For Strategic Financial ManagementgauravNo ratings yet

- Stock Valuation: Legal Rights and Privileges of Common StockholdersDocument5 pagesStock Valuation: Legal Rights and Privileges of Common Stockholderssincere sincereNo ratings yet

- FIN533 Chapter 9Document1 pageFIN533 Chapter 9zurelyanajwaNo ratings yet

- Mas Notes Rev - FinmanDocument4 pagesMas Notes Rev - FinmanPineda, Paula MarieNo ratings yet

- Lesson 12Document6 pagesLesson 12Jamaica bunielNo ratings yet

- UntitledDocument37 pagesUntitledRadNo ratings yet

- Cost of CapitalDocument14 pagesCost of CapitalShardulNo ratings yet

- Topic 4 - Valuation of SharesDocument26 pagesTopic 4 - Valuation of SharesMiera FrnhNo ratings yet

- Financial Filings and Annual Reports: Separating The Wheat From The ChaffDocument10 pagesFinancial Filings and Annual Reports: Separating The Wheat From The ChaffsuksesNo ratings yet

- Week 5 - Chapter 4Document45 pagesWeek 5 - Chapter 4AJNo ratings yet

- CHAPTER 22 Theory Financial Assets at Fair ValueDocument3 pagesCHAPTER 22 Theory Financial Assets at Fair ValueRomel BucaloyNo ratings yet

- 07 Cafmst14 - CH - 05Document52 pages07 Cafmst14 - CH - 05Mahabub AlamNo ratings yet

- Types of Securities Equity DebtDocument21 pagesTypes of Securities Equity DebtTeja MullapudiNo ratings yet

- Lesson 1 - Intro To FMDocument2 pagesLesson 1 - Intro To FMStanley AquinoNo ratings yet

- Synergies and ValuationDocument16 pagesSynergies and ValuationPaul GhanimehNo ratings yet

- Chapter 4Document2 pagesChapter 4Azi LheyNo ratings yet

- Mutual Fund in Pakistan, Types and Performance EvaluationDocument7 pagesMutual Fund in Pakistan, Types and Performance Evaluationbonfument100% (2)

- (FMDFINA) Bridging Blaze FMDFINA ReviewerDocument24 pages(FMDFINA) Bridging Blaze FMDFINA Reviewerseokyung2021No ratings yet

- Divided by The Number of Shares OutstandingDocument5 pagesDivided by The Number of Shares OutstandingRia GabsNo ratings yet

- Chapter 2: Securities: Types, Features and ConceptsDocument22 pagesChapter 2: Securities: Types, Features and ConceptsTeja MullapudiNo ratings yet

- Primer On Trading CompsDocument6 pagesPrimer On Trading CompsfaiyazadamNo ratings yet

- Cost+of+Capital +Ajay+Kulkarni+Document38 pagesCost+of+Capital +Ajay+Kulkarni+jangitisindhu2002No ratings yet

- Mutual FundsDocument36 pagesMutual FundsShodasakshari VidyaNo ratings yet

- Discounted Cash Flow (DCF) ModellingDocument43 pagesDiscounted Cash Flow (DCF) Modellingjasonccheng25No ratings yet

- Controllership REVIEWERDocument10 pagesControllership REVIEWERDanielle AndreiNo ratings yet

- The Principle of Financial Accounting MeasurementDocument12 pagesThe Principle of Financial Accounting Measurementjiaozitang100% (1)

- Finman ReviewerDocument24 pagesFinman ReviewerXeleen Elizabeth ArcaNo ratings yet

- Finance PDFDocument6 pagesFinance PDFBritney valladaresNo ratings yet

- Strategic Financial Management: A Capsule For Quick RevisionDocument22 pagesStrategic Financial Management: A Capsule For Quick RevisionدهانوجﻛﻮﻣﺎﺭNo ratings yet

- Valuation - Discounted Cash Flow Method With Case Studies: Bengaluru Branch of SIRC of ICAIDocument33 pagesValuation - Discounted Cash Flow Method With Case Studies: Bengaluru Branch of SIRC of ICAIpre.meh21No ratings yet

- FRA DossierDocument94 pagesFRA DossierRNo ratings yet

- Session 2 - Capital Structure - Classroom - UpdatedDocument65 pagesSession 2 - Capital Structure - Classroom - UpdatedmarcchamiehNo ratings yet

- Introduction To InvestmentsDocument16 pagesIntroduction To InvestmentsWilyn Grace AljasNo ratings yet

- T4-Common Stock BasicsDocument50 pagesT4-Common Stock BasicsszaNo ratings yet

- FMar Financial Markets Formulas Rob NotesDocument8 pagesFMar Financial Markets Formulas Rob NotesEvelyn LabhananNo ratings yet

- SFM PDFDocument22 pagesSFM PDFZafar IqbalNo ratings yet

- Summary of Michael J. Mauboussin & Alfred Rappaport's Expectations InvestingFrom EverandSummary of Michael J. Mauboussin & Alfred Rappaport's Expectations InvestingNo ratings yet

- Patent ValuationDocument11 pagesPatent ValuationAkhil JainNo ratings yet

- Iso 22000 Checklist Fsms f6.4-22 (FSMS)Document14 pagesIso 22000 Checklist Fsms f6.4-22 (FSMS)BRIGHT DZAH100% (1)

- Branch Banking SystemDocument16 pagesBranch Banking SystemPrathyusha ReddyNo ratings yet

- PBRXDocument29 pagesPBRXMoe EcchiNo ratings yet

- PWC Food Fraud Vulnerability AssessmentDocument8 pagesPWC Food Fraud Vulnerability AssessmentAnous AlamiNo ratings yet

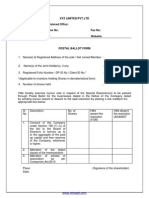

- Postal Ballot Form FormatDocument4 pagesPostal Ballot Form FormatGaurav Kumar SharmaNo ratings yet

- Six Sigma Green Belt Examination - Six Sigma - Normal DistributionDocument15 pagesSix Sigma Green Belt Examination - Six Sigma - Normal DistributionVighnesh VikkiNo ratings yet

- Direct and Indirect CostsDocument18 pagesDirect and Indirect Costsengrwaqas_11No ratings yet

- Commercial RecDocument12 pagesCommercial Recapi-280054911No ratings yet

- PLANNING AND WORKING CAPITAL MANAGEMENT (Chapter 3)Document3 pagesPLANNING AND WORKING CAPITAL MANAGEMENT (Chapter 3)Marie Nica J. GarciaNo ratings yet

- Learning Spring Application Development - Sample ChapterDocument35 pagesLearning Spring Application Development - Sample ChapterPackt Publishing100% (1)

- Case Digests TaxDocument10 pagesCase Digests TaxAron PanturillaNo ratings yet

- Business Plan Vegetable Lumpia DRAFTDocument9 pagesBusiness Plan Vegetable Lumpia DRAFTCristel CadayongNo ratings yet

- SD Questions About Pricing ConditionDocument9 pagesSD Questions About Pricing ConditionAniruddha Chakraborty100% (1)

- Mvela GroupDocument97 pagesMvela GroupsizwehNo ratings yet

- Sugar Plugin For Excel 6.1.0Document6 pagesSugar Plugin For Excel 6.1.0chicagogroovesNo ratings yet

- Haykal 838Document1 pageHaykal 838Dinesh KhatiNo ratings yet

- ACCOUNTSDocument7 pagesACCOUNTSChan Chan75% (4)

- Data Analytics For AuditingDocument70 pagesData Analytics For AuditingBintanKamilaNo ratings yet

- Purchasing and Inventory ControlDocument7 pagesPurchasing and Inventory Controlalemtsehaysima49No ratings yet

- Response Essay: Customer Data Means Nothing Without An Action PlanDocument3 pagesResponse Essay: Customer Data Means Nothing Without An Action PlanGhulamNo ratings yet

- 200702Document40 pages200702manilamedia100% (1)

- Suguna Project Pons Last ReloadedDocument51 pagesSuguna Project Pons Last ReloadedPerumal Kumar100% (1)

- Chap 011Document35 pagesChap 011tb7976skNo ratings yet

- SOW IT - Management.Services - IT.Security PDFDocument36 pagesSOW IT - Management.Services - IT.Security PDFRichard RamirezNo ratings yet

- Forecasting SKDocument20 pagesForecasting SKNirmay Mufc ShahNo ratings yet

- Ilovepdf MergedDocument3 pagesIlovepdf MergedKirill KalininNo ratings yet

Download as pdf or txt

You might also like

- 319 Question BankDocument142 pages319 Question BankElla67% (3)

- Supplementory Lease Deed!!!Document2 pagesSupplementory Lease Deed!!!Saddy Butt67% (3)

- Entrepreneurship Assignment 04: Critique Zipcar: M. Umar Ashraf REG # 2013-IM-23Document9 pagesEntrepreneurship Assignment 04: Critique Zipcar: M. Umar Ashraf REG # 2013-IM-23umar100% (3)

- Invst Reviewer Ver1Document3 pagesInvst Reviewer Ver1evenslzrNo ratings yet

- 03 DCF Valuation M&ADocument47 pages03 DCF Valuation M&AI DNo ratings yet

- PrelimsDocument6 pagesPrelimsJanna Grace Dela CruzNo ratings yet

- Clase III - Information For Investment and ValuationDocument208 pagesClase III - Information For Investment and ValuationMiguel Vega OtinianoNo ratings yet

- Chapter 4 Stock ValuationDocument68 pagesChapter 4 Stock ValuationHalisa HassanNo ratings yet

- Chapter 8Document12 pagesChapter 8Hannah Pauleen G. LabasaNo ratings yet

- F14 Fin PDFDocument13 pagesF14 Fin PDFNageshwar SinghNo ratings yet

- Absolute Vs Relative ValuationDocument3 pagesAbsolute Vs Relative ValuationLilliane EstrellaNo ratings yet

- Principles of Managerial Finance Brief 6th Edition Gitman Solutions ManualDocument38 pagesPrinciples of Managerial Finance Brief 6th Edition Gitman Solutions Manualjomaevelina2980100% (16)

- Bs Finance Chapter 6Document6 pagesBs Finance Chapter 6Erick KibeNo ratings yet

- Company Valuation Summary by Faldi Rev.1Document8 pagesCompany Valuation Summary by Faldi Rev.1Faldi HarisNo ratings yet

- Equity ValuationDocument20 pagesEquity ValuationDorah KahiseNo ratings yet

- Chapter 13 - PortfolioDocument25 pagesChapter 13 - Portfolioapi-308173825No ratings yet

- CORP Finance II Exam NotesDocument12 pagesCORP Finance II Exam NotesTeddie MowerNo ratings yet

- Business Valuation Part 1 Lorelei R. DanilaDocument27 pagesBusiness Valuation Part 1 Lorelei R. DanilaBoongaling, Jose Jr CondeNo ratings yet

- Fin Mar ReviewerDocument2 pagesFin Mar ReviewerPixie CanaveralNo ratings yet

- Market Multiple Valuation Models-Mod - 4Document20 pagesMarket Multiple Valuation Models-Mod - 4Ravichandran RamadassNo ratings yet

- This Study Resource Was: Ms-11: Long Term Equity FinancingDocument4 pagesThis Study Resource Was: Ms-11: Long Term Equity FinancingKathleen Lucas0% (1)

- Risk-Return Trade-Off in Financial Decision MakingDocument12 pagesRisk-Return Trade-Off in Financial Decision MakingAnmol Shrestha0% (1)

- Chapter 5 - NotesDocument2 pagesChapter 5 - NotesLovely CabardoNo ratings yet

- Val Indonesia 2014Document151 pagesVal Indonesia 2014Carlos Jesús Ponce AranedaNo ratings yet

- AFA - 4e - PPT - Chap12 (For Students)Document22 pagesAFA - 4e - PPT - Chap12 (For Students)Cẩm Tú NguyễnNo ratings yet

- Nism CH 10Document13 pagesNism CH 10Darshan JainNo ratings yet

- Referencer For Strategic Financial ManagementDocument24 pagesReferencer For Strategic Financial ManagementgauravNo ratings yet

- Stock Valuation: Legal Rights and Privileges of Common StockholdersDocument5 pagesStock Valuation: Legal Rights and Privileges of Common Stockholderssincere sincereNo ratings yet

- FIN533 Chapter 9Document1 pageFIN533 Chapter 9zurelyanajwaNo ratings yet

- Mas Notes Rev - FinmanDocument4 pagesMas Notes Rev - FinmanPineda, Paula MarieNo ratings yet

- Lesson 12Document6 pagesLesson 12Jamaica bunielNo ratings yet

- UntitledDocument37 pagesUntitledRadNo ratings yet

- Cost of CapitalDocument14 pagesCost of CapitalShardulNo ratings yet

- Topic 4 - Valuation of SharesDocument26 pagesTopic 4 - Valuation of SharesMiera FrnhNo ratings yet

- Financial Filings and Annual Reports: Separating The Wheat From The ChaffDocument10 pagesFinancial Filings and Annual Reports: Separating The Wheat From The ChaffsuksesNo ratings yet

- Week 5 - Chapter 4Document45 pagesWeek 5 - Chapter 4AJNo ratings yet

- CHAPTER 22 Theory Financial Assets at Fair ValueDocument3 pagesCHAPTER 22 Theory Financial Assets at Fair ValueRomel BucaloyNo ratings yet

- 07 Cafmst14 - CH - 05Document52 pages07 Cafmst14 - CH - 05Mahabub AlamNo ratings yet

- Types of Securities Equity DebtDocument21 pagesTypes of Securities Equity DebtTeja MullapudiNo ratings yet

- Lesson 1 - Intro To FMDocument2 pagesLesson 1 - Intro To FMStanley AquinoNo ratings yet

- Synergies and ValuationDocument16 pagesSynergies and ValuationPaul GhanimehNo ratings yet

- Chapter 4Document2 pagesChapter 4Azi LheyNo ratings yet

- Mutual Fund in Pakistan, Types and Performance EvaluationDocument7 pagesMutual Fund in Pakistan, Types and Performance Evaluationbonfument100% (2)

- (FMDFINA) Bridging Blaze FMDFINA ReviewerDocument24 pages(FMDFINA) Bridging Blaze FMDFINA Reviewerseokyung2021No ratings yet

- Divided by The Number of Shares OutstandingDocument5 pagesDivided by The Number of Shares OutstandingRia GabsNo ratings yet

- Chapter 2: Securities: Types, Features and ConceptsDocument22 pagesChapter 2: Securities: Types, Features and ConceptsTeja MullapudiNo ratings yet

- Primer On Trading CompsDocument6 pagesPrimer On Trading CompsfaiyazadamNo ratings yet

- Cost+of+Capital +Ajay+Kulkarni+Document38 pagesCost+of+Capital +Ajay+Kulkarni+jangitisindhu2002No ratings yet

- Mutual FundsDocument36 pagesMutual FundsShodasakshari VidyaNo ratings yet

- Discounted Cash Flow (DCF) ModellingDocument43 pagesDiscounted Cash Flow (DCF) Modellingjasonccheng25No ratings yet

- Controllership REVIEWERDocument10 pagesControllership REVIEWERDanielle AndreiNo ratings yet

- The Principle of Financial Accounting MeasurementDocument12 pagesThe Principle of Financial Accounting Measurementjiaozitang100% (1)

- Finman ReviewerDocument24 pagesFinman ReviewerXeleen Elizabeth ArcaNo ratings yet

- Finance PDFDocument6 pagesFinance PDFBritney valladaresNo ratings yet

- Strategic Financial Management: A Capsule For Quick RevisionDocument22 pagesStrategic Financial Management: A Capsule For Quick RevisionدهانوجﻛﻮﻣﺎﺭNo ratings yet

- Valuation - Discounted Cash Flow Method With Case Studies: Bengaluru Branch of SIRC of ICAIDocument33 pagesValuation - Discounted Cash Flow Method With Case Studies: Bengaluru Branch of SIRC of ICAIpre.meh21No ratings yet

- FRA DossierDocument94 pagesFRA DossierRNo ratings yet

- Session 2 - Capital Structure - Classroom - UpdatedDocument65 pagesSession 2 - Capital Structure - Classroom - UpdatedmarcchamiehNo ratings yet

- Introduction To InvestmentsDocument16 pagesIntroduction To InvestmentsWilyn Grace AljasNo ratings yet

- T4-Common Stock BasicsDocument50 pagesT4-Common Stock BasicsszaNo ratings yet

- FMar Financial Markets Formulas Rob NotesDocument8 pagesFMar Financial Markets Formulas Rob NotesEvelyn LabhananNo ratings yet

- SFM PDFDocument22 pagesSFM PDFZafar IqbalNo ratings yet

- Summary of Michael J. Mauboussin & Alfred Rappaport's Expectations InvestingFrom EverandSummary of Michael J. Mauboussin & Alfred Rappaport's Expectations InvestingNo ratings yet

- Patent ValuationDocument11 pagesPatent ValuationAkhil JainNo ratings yet

- Iso 22000 Checklist Fsms f6.4-22 (FSMS)Document14 pagesIso 22000 Checklist Fsms f6.4-22 (FSMS)BRIGHT DZAH100% (1)

- Branch Banking SystemDocument16 pagesBranch Banking SystemPrathyusha ReddyNo ratings yet

- PBRXDocument29 pagesPBRXMoe EcchiNo ratings yet

- PWC Food Fraud Vulnerability AssessmentDocument8 pagesPWC Food Fraud Vulnerability AssessmentAnous AlamiNo ratings yet

- Postal Ballot Form FormatDocument4 pagesPostal Ballot Form FormatGaurav Kumar SharmaNo ratings yet

- Six Sigma Green Belt Examination - Six Sigma - Normal DistributionDocument15 pagesSix Sigma Green Belt Examination - Six Sigma - Normal DistributionVighnesh VikkiNo ratings yet

- Direct and Indirect CostsDocument18 pagesDirect and Indirect Costsengrwaqas_11No ratings yet

- Commercial RecDocument12 pagesCommercial Recapi-280054911No ratings yet

- PLANNING AND WORKING CAPITAL MANAGEMENT (Chapter 3)Document3 pagesPLANNING AND WORKING CAPITAL MANAGEMENT (Chapter 3)Marie Nica J. GarciaNo ratings yet

- Learning Spring Application Development - Sample ChapterDocument35 pagesLearning Spring Application Development - Sample ChapterPackt Publishing100% (1)

- Case Digests TaxDocument10 pagesCase Digests TaxAron PanturillaNo ratings yet

- Business Plan Vegetable Lumpia DRAFTDocument9 pagesBusiness Plan Vegetable Lumpia DRAFTCristel CadayongNo ratings yet

- SD Questions About Pricing ConditionDocument9 pagesSD Questions About Pricing ConditionAniruddha Chakraborty100% (1)

- Mvela GroupDocument97 pagesMvela GroupsizwehNo ratings yet

- Sugar Plugin For Excel 6.1.0Document6 pagesSugar Plugin For Excel 6.1.0chicagogroovesNo ratings yet

- Haykal 838Document1 pageHaykal 838Dinesh KhatiNo ratings yet

- ACCOUNTSDocument7 pagesACCOUNTSChan Chan75% (4)

- Data Analytics For AuditingDocument70 pagesData Analytics For AuditingBintanKamilaNo ratings yet

- Purchasing and Inventory ControlDocument7 pagesPurchasing and Inventory Controlalemtsehaysima49No ratings yet

- Response Essay: Customer Data Means Nothing Without An Action PlanDocument3 pagesResponse Essay: Customer Data Means Nothing Without An Action PlanGhulamNo ratings yet

- 200702Document40 pages200702manilamedia100% (1)

- Suguna Project Pons Last ReloadedDocument51 pagesSuguna Project Pons Last ReloadedPerumal Kumar100% (1)

- Chap 011Document35 pagesChap 011tb7976skNo ratings yet

- SOW IT - Management.Services - IT.Security PDFDocument36 pagesSOW IT - Management.Services - IT.Security PDFRichard RamirezNo ratings yet

- Forecasting SKDocument20 pagesForecasting SKNirmay Mufc ShahNo ratings yet

- Ilovepdf MergedDocument3 pagesIlovepdf MergedKirill KalininNo ratings yet