Download as pdf or txt

You might also like

- ch17 180206123815 PDFDocument75 pagesch17 180206123815 PDFYeni Amelia100% (1)

- Use The Following Information To Answer Items 3 and 4Document15 pagesUse The Following Information To Answer Items 3 and 4charlies parrenoNo ratings yet

- Statement of Transactions: Sundaram Finance LimitedDocument1 pageStatement of Transactions: Sundaram Finance LimitedBhavin SagarNo ratings yet

- Fab IndiaDocument10 pagesFab IndiaEruNo ratings yet

- Case Study 41 - Mogen IncDocument15 pagesCase Study 41 - Mogen IncPat Cunningham100% (4)

- Report On Sumeru Securities PVT LTDDocument48 pagesReport On Sumeru Securities PVT LTDsagar timilsina60% (5)

- Ayushman Merchants Private Limited: Summary of Rated InstrumentsDocument6 pagesAyushman Merchants Private Limited: Summary of Rated InstrumentsJeffNo ratings yet

- ABT Industries Limited: Summary of Rated Instruments Instrument Rated Amount (Rs. Crore) Rating ActionDocument6 pagesABT Industries Limited: Summary of Rated Instruments Instrument Rated Amount (Rs. Crore) Rating ActionWilliam Veloz DiazNo ratings yet

- Mechemco - R-30102017 PDFDocument7 pagesMechemco - R-30102017 PDFflytorahulNo ratings yet

- Aghara Knitwear Pvt. LTD.: Summary of Rated InstrumentsDocument6 pagesAghara Knitwear Pvt. LTD.: Summary of Rated Instrumentssatvik ahujaNo ratings yet

- Vikas Spool Private Limited: Summary of Rated Instruments Instrument Rated Amount (Rs. Crore) Rating ActionDocument6 pagesVikas Spool Private Limited: Summary of Rated Instruments Instrument Rated Amount (Rs. Crore) Rating Actionvinay durgapalNo ratings yet

- Aegis Agro Chemicals India Private Limited: Summary of Rated InstrumentsDocument6 pagesAegis Agro Chemicals India Private Limited: Summary of Rated InstrumentsBhavin SagarNo ratings yet

- Gujarat Guardian Limited-R-30032018Document6 pagesGujarat Guardian Limited-R-30032018SuhasNo ratings yet

- AOV Exports Private Limited: Summary of Rated Instruments Instrument Rated Amount (In Rs. Crore) Rating ActionDocument7 pagesAOV Exports Private Limited: Summary of Rated Instruments Instrument Rated Amount (In Rs. Crore) Rating ActionDevansh ThaparNo ratings yet

- Eurotex Industries and Exports Limited: Summary of Rated InstrumentsDocument7 pagesEurotex Industries and Exports Limited: Summary of Rated InstrumentsHari KrishnanNo ratings yet

- Jainam Cables (India) Private Limited: Summary of Rated InstrumentsDocument6 pagesJainam Cables (India) Private Limited: Summary of Rated InstrumentspunamNo ratings yet

- R.S. Brothers Retail - R-06122017Document7 pagesR.S. Brothers Retail - R-06122017srv 99No ratings yet

- Sara International Private Limited May 19, 2020: RatingsDocument6 pagesSara International Private Limited May 19, 2020: RatingsRavi BabuNo ratings yet

- Ankit Pulps and Boards - R-25102018Document6 pagesAnkit Pulps and Boards - R-25102018HEMANT GURJARNo ratings yet

- Triveni TurbineDocument6 pagesTriveni TurbinevikasNo ratings yet

- LGB Forge Limited: Summary of Rating ActionDocument7 pagesLGB Forge Limited: Summary of Rating ActionPuneet367No ratings yet

- The DataDocument7 pagesThe DatashettyNo ratings yet

- BFG International Private Limited: Summary of Rated InstrumentsDocument6 pagesBFG International Private Limited: Summary of Rated InstrumentsB Vignesh BabuNo ratings yet

- J.G. Hosiery - R-03102017Document7 pagesJ.G. Hosiery - R-03102017Mohit GirdherNo ratings yet

- Prof. Ishwar SinghDocument7 pagesProf. Ishwar SinghDeepak RanaNo ratings yet

- VNS Finance & Capital Services Limited: Summary of Rated InstrumentsDocument6 pagesVNS Finance & Capital Services Limited: Summary of Rated InstrumentsRakesh JainNo ratings yet

- Laser Fibers Private Limited: Summary of Rated Instruments Instrument Rated Amount (In Rs. Crore) Rating ActionDocument6 pagesLaser Fibers Private Limited: Summary of Rated Instruments Instrument Rated Amount (In Rs. Crore) Rating ActionBhavin SagarNo ratings yet

- D&H Secheron Electrodes Private Limited: Summary of Rated InstrumentsDocument6 pagesD&H Secheron Electrodes Private Limited: Summary of Rated InstrumentsMahee MahemaaNo ratings yet

- Bata India Limited: Summary of Rating ActionDocument6 pagesBata India Limited: Summary of Rating ActionDhrubajyoti DattaNo ratings yet

- Export-Import Bank of India: Summary of Rated InstrumentsDocument12 pagesExport-Import Bank of India: Summary of Rated InstrumentsSakthi GaneshNo ratings yet

- Vibracoustic India Private LimitedDocument6 pagesVibracoustic India Private LimitedBithal PrasadNo ratings yet

- Wipro Limited - Update On Material Event: Summary of Rating(s) OutstandingDocument7 pagesWipro Limited - Update On Material Event: Summary of Rating(s) OutstandingMegha PrakashNo ratings yet

- Della Adventure R 17112017Document7 pagesDella Adventure R 17112017Anil KanojiaNo ratings yet

- Acknit Industries Limited: Summary of Rating ActionDocument7 pagesAcknit Industries Limited: Summary of Rating ActionprasanthNo ratings yet

- Gokak Textiles Limited: Ratings Reaffirmed Long-Term Rating Withdrawn Summary of Rating ActionDocument6 pagesGokak Textiles Limited: Ratings Reaffirmed Long-Term Rating Withdrawn Summary of Rating Actionabhi MestriNo ratings yet

- Super Screws Private Limited: Summary of Rated InstrumentsDocument7 pagesSuper Screws Private Limited: Summary of Rated InstrumentsAnonymous bdUhUNm7JNo ratings yet

- T V Sundram Iyengar-R-16022018Document7 pagesT V Sundram Iyengar-R-16022018AGN YaNo ratings yet

- Ajax Fiori-R-07092017Document7 pagesAjax Fiori-R-07092017parimal.rodeNo ratings yet

- TM International Logistics Limited: Summary of Rated InstrumentsDocument7 pagesTM International Logistics Limited: Summary of Rated InstrumentsSunny SkNo ratings yet

- Thanjavur Spinning R 11082017Document8 pagesThanjavur Spinning R 11082017TitanNo ratings yet

- Dharmesh Textiles Limited: Summary of Rated Instruments Instrument Rated Amount (In Rs. Crore) Rating ActionDocument7 pagesDharmesh Textiles Limited: Summary of Rated Instruments Instrument Rated Amount (In Rs. Crore) Rating ActionJeffNo ratings yet

- JBM Ogihara Automotive India LimitedDocument8 pagesJBM Ogihara Automotive India Limitedankityad129No ratings yet

- Ganga Rasayanie Private Limited-R-10102019Document7 pagesGanga Rasayanie Private Limited-R-10102019DarshanNo ratings yet

- Titan Company Limited: Migration of The Rating Outstanding On The Medium-Term Rating Scale To The Long-Term Rating ScaleDocument5 pagesTitan Company Limited: Migration of The Rating Outstanding On The Medium-Term Rating Scale To The Long-Term Rating ScaleMalavShahNo ratings yet

- Press Release 3B Fibreglass SPRL: Facilities Amount (Rs. Crore) Rating Rating ActionDocument4 pagesPress Release 3B Fibreglass SPRL: Facilities Amount (Rs. Crore) Rating Rating ActionData CentrumNo ratings yet

- Kellton Tech Solutions R 28092018Document7 pagesKellton Tech Solutions R 28092018Suresh Kumar RaiNo ratings yet

- Zinka Logistics Solutions - R - 07062018 PDFDocument6 pagesZinka Logistics Solutions - R - 07062018 PDFSANIL BADHANINo ratings yet

- Singer India Limited: Summary of Rated Instruments Instrument Rated Amount (Rs. Crore) Rating ActionDocument6 pagesSinger India Limited: Summary of Rated Instruments Instrument Rated Amount (Rs. Crore) Rating ActionSaravanan BalakrishnanNo ratings yet

- BPR Infrastructure Limited: Summary of Rated Instruments Instruments Amount Rated (Rs. Crore) Rating ActionDocument7 pagesBPR Infrastructure Limited: Summary of Rated Instruments Instruments Amount Rated (Rs. Crore) Rating ActionNithinNo ratings yet

- Nezone Pipes & Structures-R-05042018Document7 pagesNezone Pipes & Structures-R-05042018rahul badgujarNo ratings yet

- Stove Kraft Limited-3Document5 pagesStove Kraft Limited-3venkyniyerNo ratings yet

- Investigation On The Flow Behaviour of ADocument6 pagesInvestigation On The Flow Behaviour of ANikhil GuptaNo ratings yet

- Press Release MaharajaDocument5 pagesPress Release MaharajaMS SAMIRANNo ratings yet

- Muthoot Finance LimitedDocument11 pagesMuthoot Finance LimitedKhasimvali ShaikNo ratings yet

- SMFG India Credit Company LimitedDocument11 pagesSMFG India Credit Company Limitedvatsal sinhaNo ratings yet

- Happy ForgingsDocument7 pagesHappy ForgingsArshChandraNo ratings yet

- Sun Home Appliances Private - R - 25082020Document7 pagesSun Home Appliances Private - R - 25082020DarshanNo ratings yet

- Vinayak Steels Limited Financial ReportDocument7 pagesVinayak Steels Limited Financial Reportsaikiran reddyNo ratings yet

- Vaighai Agro Products Limited: Instruments Amount Rated (Rs. Crore) Rating ActionDocument7 pagesVaighai Agro Products Limited: Instruments Amount Rated (Rs. Crore) Rating ActionSuresh NmsNo ratings yet

- Iscon Balaji Foods - R-24052017Document7 pagesIscon Balaji Foods - R-24052017Kunal DamaniNo ratings yet

- Suprajit Engineering LimitedDocument6 pagesSuprajit Engineering LimitedHarinath ReddyNo ratings yet

- Modern Construction Company R 18062020Document7 pagesModern Construction Company R 18062020Ali KayaNo ratings yet

- MRF Limited - R - 30112020Document7 pagesMRF Limited - R - 30112020deepal patilNo ratings yet

- Sree Akkamamba Textiles - R - 13032020Document7 pagesSree Akkamamba Textiles - R - 13032020saikiran reddyNo ratings yet

- Saya Homes ProjectDocument5 pagesSaya Homes ProjectSatish RAjNo ratings yet

- Credit Union Revenues World Summary: Market Values & Financials by CountryFrom EverandCredit Union Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Bse Sme Ipo IndexDocument4 pagesBse Sme Ipo IndexBhavin SagarNo ratings yet

- Qtrly - Reportq1 FY 2008 2009Document2 pagesQtrly - Reportq1 FY 2008 2009Bhavin SagarNo ratings yet

- Nebbia Mutual NDADocument3 pagesNebbia Mutual NDABhavin SagarNo ratings yet

- Yap 31 1 19Document345 pagesYap 31 1 19Bhavin SagarNo ratings yet

- Revised Underwriting Agreement 31.03Document14 pagesRevised Underwriting Agreement 31.03Bhavin SagarNo ratings yet

- Amalgmation - August 2020 - Arihant Capital Shree Renuka Sugars LTDDocument10 pagesAmalgmation - August 2020 - Arihant Capital Shree Renuka Sugars LTDBhavin SagarNo ratings yet

- Corporate Deck - InternationalDocument16 pagesCorporate Deck - InternationalBhavin SagarNo ratings yet

- Revised Market Making Agreement 31.03Document13 pagesRevised Market Making Agreement 31.03Bhavin SagarNo ratings yet

- Revised RV - Draft Valuation Report - Hakuna MatataDocument11 pagesRevised RV - Draft Valuation Report - Hakuna MatataBhavin SagarNo ratings yet

- 01 Business Partnership Powerpoint TemplateDocument12 pages01 Business Partnership Powerpoint TemplateBhavin SagarNo ratings yet

- August 2021 - Shipping Corporation of India LTD by Corporate ProfessionalsDocument10 pagesAugust 2021 - Shipping Corporation of India LTD by Corporate ProfessionalsBhavin SagarNo ratings yet

- Capital Reduction - Escorts LTD - GalacticoDocument10 pagesCapital Reduction - Escorts LTD - GalacticoBhavin SagarNo ratings yet

- 01 Business Partnership Powerpoint TemplateDocument12 pages01 Business Partnership Powerpoint TemplateBhavin SagarNo ratings yet

- List of Valuation ReportsDocument18 pagesList of Valuation ReportsBhavin SagarNo ratings yet

- 02 Corporate Orange Powerpoint Presentations 16x9 1Document13 pages02 Corporate Orange Powerpoint Presentations 16x9 1Bhavin SagarNo ratings yet

- EKI Energy Services Limited: Payments MadeDocument2 pagesEKI Energy Services Limited: Payments MadeBhavin SagarNo ratings yet

- MCA FinanicialsDocument50 pagesMCA FinanicialsBhavin SagarNo ratings yet

- EKI Energy Services Limited: Payments MadeDocument2 pagesEKI Energy Services Limited: Payments MadeBhavin SagarNo ratings yet

- Bulk DealsDocument63 pagesBulk DealsBhavin SagarNo ratings yet

- Bhavin Valuation Cases For FY21Document17 pagesBhavin Valuation Cases For FY21Bhavin SagarNo ratings yet

- Valuation Assignement - WIPDocument2 pagesValuation Assignement - WIPBhavin SagarNo ratings yet

- Bhavin - Valuation Cases - May 2021Document3 pagesBhavin - Valuation Cases - May 2021Bhavin SagarNo ratings yet

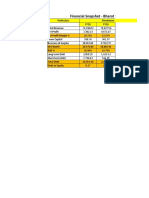

- Bharat Serums & Vaccines LTD - Financial SnapshotDocument2 pagesBharat Serums & Vaccines LTD - Financial SnapshotBhavin SagarNo ratings yet

- Taxation Laws2Document156 pagesTaxation Laws2KIran100% (1)

- CRG660 - Full SS 2022 To 2019Document51 pagesCRG660 - Full SS 2022 To 2019Wibi Ali HazaratNo ratings yet

- FINAL B. Riley FBR PresentationDocument17 pagesFINAL B. Riley FBR Presentationsl7789No ratings yet

- Internal Assessment Based On Summer Internship Company (Praedico Global Research Private Limited)Document3 pagesInternal Assessment Based On Summer Internship Company (Praedico Global Research Private Limited)Nishant BhartiNo ratings yet

- BIR Ruling (DA-152-07) (Restricted Stock Unit Plan)Document4 pagesBIR Ruling (DA-152-07) (Restricted Stock Unit Plan)Archie GuevarraNo ratings yet

- Axia Futures Price Ladder Course NotesDocument26 pagesAxia Futures Price Ladder Course NotesDio diocapital100% (1)

- Japanese International Marketing StrategyDocument11 pagesJapanese International Marketing StrategyspriyanthagNo ratings yet

- Financial MarketDocument8 pagesFinancial MarketDileep Kumar SinghNo ratings yet

- LEAPOfferings Combined PWADocument42 pagesLEAPOfferings Combined PWAsanaa.kanjianiNo ratings yet

- SECP PresDocument29 pagesSECP PresZoha MirNo ratings yet

- 708-Article Text-2727-1-10-20210325Document11 pages708-Article Text-2727-1-10-20210325Joicelyne HuangNo ratings yet

- BUS20269 Financial Management Final ExamDocument7 pagesBUS20269 Financial Management Final Examshiyingyang98No ratings yet

- Global Equities - A Canadian Investors PerspectiveDocument12 pagesGlobal Equities - A Canadian Investors PerspectivejennaNo ratings yet

- Review of LiteratureDocument12 pagesReview of LiteratureRanjit Superanjit100% (1)

- Managerial Economics Sees1Document19 pagesManagerial Economics Sees1doraline0911100% (2)

- Influential Factors of Country Accounting System DeveDocument12 pagesInfluential Factors of Country Accounting System DeveJoEst KaraNgNo ratings yet

- Financial Statement For Quiz 3 PDFDocument4 pagesFinancial Statement For Quiz 3 PDFJiaXinLimNo ratings yet

- Fundamentals of PE Deal Structuring - DeloitteDocument8 pagesFundamentals of PE Deal Structuring - DeloitteEkansh AroraNo ratings yet

- B.O.M. AssignmentDocument23 pagesB.O.M. AssignmentMoh'ed A. KhalafNo ratings yet

- CircularDocument46 pagesCircularGodknows MudzingwaNo ratings yet

- Jurisdiction CasesDocument25 pagesJurisdiction CasesAerwin AbesamisNo ratings yet

- Cheat Sheet Financial Statement ModellingDocument8 pagesCheat Sheet Financial Statement ModellingAsmitaNo ratings yet

- Secretarial Practice: Std. Xii LMRDocument45 pagesSecretarial Practice: Std. Xii LMRaliffya rangwalaNo ratings yet

- A Study of Equity Research of Company of ITC LTD"Document31 pagesA Study of Equity Research of Company of ITC LTD"Dibyaranjan SahooNo ratings yet

- The Little Book of Valuation: Cash FlowsDocument5 pagesThe Little Book of Valuation: Cash FlowsSangram PandaNo ratings yet