Download as docx, pdf, or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5834)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (903)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (350)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (824)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (405)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- An Post Mar-24Document3 pagesAn Post Mar-24liskonohanastasiiaNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- LBP Form No. 4Document8 pagesLBP Form No. 4Shie La Ma RieNo ratings yet

- Case Digest in Corp - Law 2019 2020Document393 pagesCase Digest in Corp - Law 2019 2020Shie La Ma Rie100% (4)

- Internship - Report - On - E - Banking - For Merge05Document63 pagesInternship - Report - On - E - Banking - For Merge05ঘুম বাবুNo ratings yet

- 2011 01 09 Implementing High Value Fund Transfer Pricing Systems PDFDocument19 pages2011 01 09 Implementing High Value Fund Transfer Pricing Systems PDFHoàng Trần HữuNo ratings yet

- BUAd 801Document47 pagesBUAd 801Adetunji Taiwo100% (1)

- Treasury Management ModuleDocument9 pagesTreasury Management ModuleCraig SvotwaNo ratings yet

- Affidavit of No EmbalmingDocument1 pageAffidavit of No EmbalmingShie La Ma RieNo ratings yet

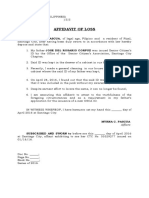

- Affidavit of Loss JunkDocument1 pageAffidavit of Loss JunkShie La Ma RieNo ratings yet

- Election OffensesDocument6 pagesElection OffensesShie La Ma RieNo ratings yet

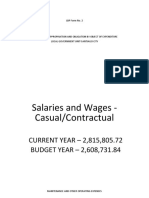

- Programmed Appropriation and Obligation by Object of Expenditure Local Government Unit-Santiago CityDocument2 pagesProgrammed Appropriation and Obligation by Object of Expenditure Local Government Unit-Santiago CityShie La Ma RieNo ratings yet

- "Bayanihan To Heal As One Act of 2020" and The Local Government Code of 1991: The Issues and Concerns Arising From Their InconsistenciesDocument18 pages"Bayanihan To Heal As One Act of 2020" and The Local Government Code of 1991: The Issues and Concerns Arising From Their InconsistenciesShie La Ma RieNo ratings yet

- (G.R. No. L-19808. September 29, 1966.) Carino V. AccfaDocument4 pages(G.R. No. L-19808. September 29, 1966.) Carino V. AccfaShie La Ma RieNo ratings yet

- Special Proceedings (Estate Settlement Preliminaries)Document31 pagesSpecial Proceedings (Estate Settlement Preliminaries)Shie La Ma RieNo ratings yet

- Affidavit of Loss (ELIZABETH T. MALIGSA)Document1 pageAffidavit of Loss (ELIZABETH T. MALIGSA)Shie La Ma RieNo ratings yet

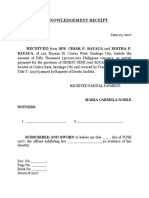

- Acknowledgement ReceiptDocument2 pagesAcknowledgement ReceiptShie La Ma RieNo ratings yet

- Affidavit of Discrepancy - April Joy GayapDocument2 pagesAffidavit of Discrepancy - April Joy GayapShie La Ma RieNo ratings yet

- Affidavit of AcknowledgmentDocument1 pageAffidavit of AcknowledgmentShie La Ma RieNo ratings yet

- Pilipinas Loan Company Vs SECDocument1 pagePilipinas Loan Company Vs SECShie La Ma RieNo ratings yet

- Affidavit of Acknowledgement of Father Paternity - LABOGDocument1 pageAffidavit of Acknowledgement of Father Paternity - LABOGShie La Ma RieNo ratings yet

- Mid Pasig Land and Development Corporation Vs TablanteDocument2 pagesMid Pasig Land and Development Corporation Vs TablanteShie La Ma RieNo ratings yet

- LIGAYA ESGUERRA Vs HOLCIMDocument3 pagesLIGAYA ESGUERRA Vs HOLCIMShie La Ma Rie0% (1)

- Transpo Table of DoctrinesDocument7 pagesTranspo Table of DoctrinesShie La Ma RieNo ratings yet

- Transpo Table of DoctrinesDocument7 pagesTranspo Table of DoctrinesShie La Ma RieNo ratings yet

- Insurance Fraud: Atty. Dennis B. FunaDocument47 pagesInsurance Fraud: Atty. Dennis B. FunaShie La Ma RieNo ratings yet

- Case DigestsDocument11 pagesCase DigestsShie La Ma RieNo ratings yet

- Rem Law Case DigestsDocument28 pagesRem Law Case DigestsShie La Ma RieNo ratings yet

- Legal FormsDocument4 pagesLegal FormsShie La Ma RieNo ratings yet

- Salik Ahmed, BBA, Project Report 2021, FullBrand Equity and Advertising Iin CBLDocument73 pagesSalik Ahmed, BBA, Project Report 2021, FullBrand Equity and Advertising Iin CBLTasmia KawsarNo ratings yet

- 14c CashManagementDocument76 pages14c CashManagementali iqbalNo ratings yet

- Share RegistarDocument4 pagesShare RegistarBishwa ShikharNo ratings yet

- Securities Market (Advanced) Module PDFDocument196 pagesSecurities Market (Advanced) Module PDFbipinjaiswal1230% (1)

- Kotak Mahindra Bank Limited FY 2020 21Document148 pagesKotak Mahindra Bank Limited FY 2020 21Harshvardhan PatilNo ratings yet

- IIBF Flyer 202010v2Document1 pageIIBF Flyer 202010v2vijayjhingaNo ratings yet

- Jurnal Cash Flow Ke 2Document24 pagesJurnal Cash Flow Ke 2sarahNo ratings yet

- Accounting Grade 11 Revision Term 1 - 2023Document15 pagesAccounting Grade 11 Revision Term 1 - 2023sihlemooi3No ratings yet

- Customer Service in Banking: By: Doris ReinsDocument35 pagesCustomer Service in Banking: By: Doris ReinsmadhurendrahraNo ratings yet

- SOP BESCOM Manual - 231008 - 124602Document37 pagesSOP BESCOM Manual - 231008 - 124602Geogy GeorgeNo ratings yet

- Technical Support and Resistance - 050719Document6 pagesTechnical Support and Resistance - 050719Prasanna ManaviNo ratings yet

- Dear Parents / GuardianDocument1 pageDear Parents / GuardianSatya DubeyNo ratings yet

- Proof of Cash - Sample ProblemsDocument1 pageProof of Cash - Sample ProblemsFucio, Mark JeroldNo ratings yet

- 1 Af 101 FfaDocument4 pages1 Af 101 FfaHakim JanNo ratings yet

- Education Loans For Higher StudiesDocument7 pagesEducation Loans For Higher StudiesSREYANo ratings yet

- The Assessment of Management Information SystemDocument35 pagesThe Assessment of Management Information Systemabdirisak mahamed80% (5)

- Bank FormDocument1 pageBank FormMark Leo CasidsidNo ratings yet

- Islamic Capital MarketDocument42 pagesIslamic Capital MarketTee Soon HuatNo ratings yet

- Barangay Proposal-1Document4 pagesBarangay Proposal-1Rosevie ZantuaNo ratings yet

- BPI v. Court of Appeals 255 SCRA 571 G.R. No. 116792 March 29 1996Document2 pagesBPI v. Court of Appeals 255 SCRA 571 G.R. No. 116792 March 29 1996Hurjae Soriano Lubag100% (4)

- A Project On "A Study On Working Capital Management": An INTERNSHIP REPORT Submitted by Bimalkanta DasDocument88 pagesA Project On "A Study On Working Capital Management": An INTERNSHIP REPORT Submitted by Bimalkanta DasBimal DasNo ratings yet

- Customer Perception Towards HDFC Standard LifeDocument78 pagesCustomer Perception Towards HDFC Standard LiferahulmalladiNo ratings yet

- Susan Strange - Finance, Power, InstitutionDocument17 pagesSusan Strange - Finance, Power, InstitutionHalida RizkinaNo ratings yet

- New Regular Contractor's License (SOLE - PROP) - 11192018Document27 pagesNew Regular Contractor's License (SOLE - PROP) - 11192018Francisco TaquioNo ratings yet

- Managerial EconomicsDocument15 pagesManagerial EconomicsDaniel KerandiNo ratings yet