Download as pdf or txt

You might also like

- Forge LTD ReportDocument10 pagesForge LTD Reportzahrahassan78No ratings yet

- CBMEC - Skilled Care PharmacyDocument3 pagesCBMEC - Skilled Care PharmacyNors Pataytay67% (3)

- Absorption and Variable CostingDocument22 pagesAbsorption and Variable CostingJamaica David100% (4)

- Chapter 9 Standard Costing - SynopsisDocument8 pagesChapter 9 Standard Costing - SynopsissajedulNo ratings yet

- AC 2203 Economic Development SyllabusDocument2 pagesAC 2203 Economic Development SyllabusNors PataytayNo ratings yet

- El FiliDocument125 pagesEl FiliNors Pataytay0% (1)

- Personal Financial ManagementDocument39 pagesPersonal Financial ManagementNors PataytayNo ratings yet

- Promise To PayDocument1 pagePromise To PayYehezkiel Romartogi0% (1)

- Strategy Analysis of TTK PrestigeDocument57 pagesStrategy Analysis of TTK PrestigeManak OberoiNo ratings yet

- 06 Standard Costing PDFDocument5 pages06 Standard Costing PDFMarielle CastañedaNo ratings yet

- Module 005 Standard CostingDocument12 pagesModule 005 Standard CostinggagahejuniorNo ratings yet

- MS 06-06 Process CostingDocument6 pagesMS 06-06 Process CostingxernathanNo ratings yet

- Standard Costing 2024 - 1397583526Document20 pagesStandard Costing 2024 - 1397583526k.makwetu0No ratings yet

- Overhead and Other Variances PDFDocument26 pagesOverhead and Other Variances PDFAnuruddha RajasuriyaNo ratings yet

- MAS Lecture Variable CostingDocument8 pagesMAS Lecture Variable CostingLhoel Delremedios100% (1)

- P 15 5. Standard Costing ChartDocument1 pageP 15 5. Standard Costing ChartHari MNo ratings yet

- CH 10 NotesDocument13 pagesCH 10 NotesmohamedNo ratings yet

- MAS 2 - Standard CostingDocument13 pagesMAS 2 - Standard CostingLovely Mae Lariosa100% (1)

- Chapter 7Document12 pagesChapter 7Camille GarciaNo ratings yet

- 2 - Variable Costing V Absorption CostingDocument16 pages2 - Variable Costing V Absorption CostingAbigail PadillaNo ratings yet

- SIM - Variable and Absorption Costing - 0Document5 pagesSIM - Variable and Absorption Costing - 0lilienesieraNo ratings yet

- Acctg 402Document9 pagesAcctg 402Marriah Izzabelle Suarez RamadaNo ratings yet

- Lecture Notes - Chapter 6Document3 pagesLecture Notes - Chapter 6Saint BakemonoNo ratings yet

- 08-Foh Cost VarianceDocument21 pages08-Foh Cost VariancePutri Dwi KartiniNo ratings yet

- Summary FinalDocument28 pagesSummary FinalJackNo ratings yet

- MS Absorption-and-Variable-CostingDocument2 pagesMS Absorption-and-Variable-Costingkalloni.zoeNo ratings yet

- Mas 07Document14 pagesMas 07Christine Jane AbangNo ratings yet

- Variable Production Overhead Variance (VPOH)Document9 pagesVariable Production Overhead Variance (VPOH)Wee Han ChiangNo ratings yet

- Flexible Budgets, Direct-Cost, Overhead Variances, and ManagementDocument30 pagesFlexible Budgets, Direct-Cost, Overhead Variances, and ManagementAmit DeyNo ratings yet

- Strat Cost Notes (Prelims)Document2 pagesStrat Cost Notes (Prelims)Raf Ezekiel MayaoNo ratings yet

- Gino Miguel M. Enso Strategic Cost Management - BSA 2B - B48 Standard CostingDocument5 pagesGino Miguel M. Enso Strategic Cost Management - BSA 2B - B48 Standard CostingMr. XenonNo ratings yet

- OR Cost of Inventory: Absorption Costing Variable CostingDocument2 pagesOR Cost of Inventory: Absorption Costing Variable CostingKim TaehyungNo ratings yet

- MAS-42G (Standard Costing With GP Variance Analysis)Document14 pagesMAS-42G (Standard Costing With GP Variance Analysis)Bernadette PanicanNo ratings yet

- Material VariancesDocument2 pagesMaterial VariancestygurNo ratings yet

- STANDARD COSTING and Variance AnalysisDocument30 pagesSTANDARD COSTING and Variance AnalysisAlthon JayNo ratings yet

- MAS - FormulasDocument17 pagesMAS - Formulasrichelle ann rodriguezNo ratings yet

- Absorption and Variable CostingDocument3 pagesAbsorption and Variable CostingDhona Mae FidelNo ratings yet

- Absorption and Variable Costing NotesDocument4 pagesAbsorption and Variable Costing NotesGerald Nitz PonceNo ratings yet

- Variance FormulasDocument5 pagesVariance Formulaskhanmohnoor550No ratings yet

- Flexible Budgets, Overhead Cost VariancesDocument17 pagesFlexible Budgets, Overhead Cost VariancesReshu BediaNo ratings yet

- 5-Standard Costing and GP Variance AnalysisDocument16 pages5-Standard Costing and GP Variance AnalysisMelybelle LaurelNo ratings yet

- Factory Overhead VariancesDocument5 pagesFactory Overhead VariancesJACKILYN LAVIÑANo ratings yet

- Module 4 Absorption Variable Throughput CostingDocument3 pagesModule 4 Absorption Variable Throughput CostingSky SoronoiNo ratings yet

- Module 4 Absorption Variable Throughput CostingDocument3 pagesModule 4 Absorption Variable Throughput CostingSky Soronoi100% (1)

- Standart Costing PDFDocument3 pagesStandart Costing PDFVIHARI DNo ratings yet

- Notes VarianceDocument37 pagesNotes Variancezms240No ratings yet

- Chap 4 MNGT Acctng PDFDocument4 pagesChap 4 MNGT Acctng PDFRose Ann YaboraNo ratings yet

- Mas: Variable and Absorption Costing Concept Summary: Comparison As To Treatment of Operating CostsDocument3 pagesMas: Variable and Absorption Costing Concept Summary: Comparison As To Treatment of Operating CostsClyde RamosNo ratings yet

- Cost Concepts P-1Document3 pagesCost Concepts P-1Ibeth Bello De CastroNo ratings yet

- Lecture 19CAs20Document22 pagesLecture 19CAs20mzNo ratings yet

- Standard Costing: Management Advisory ServicesDocument16 pagesStandard Costing: Management Advisory Servicesdavie andradeNo ratings yet

- Standard Costing: Output (Eg. Pieces Per Unit)Document4 pagesStandard Costing: Output (Eg. Pieces Per Unit)glcpaNo ratings yet

- Managerial Accounting FormulasDocument6 pagesManagerial Accounting FormulasKristine Esplana ToraldeNo ratings yet

- Standard Costing and Variance Analysis As Applied ToDocument39 pagesStandard Costing and Variance Analysis As Applied TorhearomefranciscoNo ratings yet

- Absorption and Variable CostingDocument15 pagesAbsorption and Variable CostingApril Pearl VenezuelaNo ratings yet

- Management Advisory Services NotesDocument2 pagesManagement Advisory Services NotesKyla RoxasNo ratings yet

- SummaryDocument8 pagesSummarySittiehaina GalmanNo ratings yet

- Mix and Yield VariancesDocument12 pagesMix and Yield VariancesVashisht SewsaransingNo ratings yet

- Joint & by ProductsDocument10 pagesJoint & by Productsharry severino0% (1)

- ACT121 - Topic 5Document5 pagesACT121 - Topic 5Juan FrivaldoNo ratings yet

- Mas 1304Document5 pagesMas 1304Vel JuneNo ratings yet

- D - Absorption and Variable CostingDocument5 pagesD - Absorption and Variable Costingian dizonNo ratings yet

- 09 Standard CostingDocument5 pages09 Standard CostingabcdefgNo ratings yet

- Block 4 MCO 5 Unit 2Document32 pagesBlock 4 MCO 5 Unit 2Tushar SharmaNo ratings yet

- Variance Analysis - Basic Formulas: 1) Material, Labour, Variable Overhead VariancesDocument3 pagesVariance Analysis - Basic Formulas: 1) Material, Labour, Variable Overhead VariancesAslam SiddiqNo ratings yet

- Management Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageFrom EverandManagement Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageRating: 5 out of 5 stars5/5 (1)

- Chapter 3 - Growth and The Asian ExperienceDocument55 pagesChapter 3 - Growth and The Asian ExperienceNors PataytayNo ratings yet

- History Og The Accommodation SectorDocument34 pagesHistory Og The Accommodation SectorNors PataytayNo ratings yet

- Company BackgroundDocument2 pagesCompany BackgroundNors PataytayNo ratings yet

- Ac2102 RaDocument9 pagesAc2102 RaNors PataytayNo ratings yet

- Ac2102 TPDocument6 pagesAc2102 TPNors PataytayNo ratings yet

- 19 - Revaluation and ImpairmentDocument3 pages19 - Revaluation and Impairmentjaymark canayaNo ratings yet

- Cebu Unemployment TrendDocument5 pagesCebu Unemployment TrendNors PataytayNo ratings yet

- The Following Data For Karen Company Are Available For Your AnalysisDocument7 pagesThe Following Data For Karen Company Are Available For Your AnalysisNors PataytayNo ratings yet

- The Relationship of Science, Religion and Ethics: Ethical Significance From Laudato SiDocument3 pagesThe Relationship of Science, Religion and Ethics: Ethical Significance From Laudato SiNors PataytayNo ratings yet

- Bank Reconciliation EditedDocument1 pageBank Reconciliation EditedNors PataytayNo ratings yet

- Job Order CostingDocument25 pagesJob Order CostingNors PataytayNo ratings yet

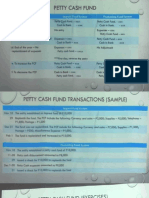

- Petty Cash Fund NotesDocument6 pagesPetty Cash Fund NotesNors Pataytay0% (1)

- The Standard Normal DistributionDocument23 pagesThe Standard Normal DistributionNors PataytayNo ratings yet

- DAY6 Freely English Translation LyricsDocument3 pagesDAY6 Freely English Translation LyricsNors PataytayNo ratings yet

- Installment BuyingDocument33 pagesInstallment BuyingNors PataytayNo ratings yet

- Simplified RA 9504Document3 pagesSimplified RA 9504thepurplehazeNo ratings yet

- Mandate Form and UndertakingDocument2 pagesMandate Form and Undertakingmeditation spirtual guruNo ratings yet

- Teme Diplome Gerta BletaDocument14 pagesTeme Diplome Gerta BletaKlea KikaNo ratings yet

- CHRLKW FinanceDocument132 pagesCHRLKW FinancenargesNo ratings yet

- 77Document2 pages77Arian AmuraoNo ratings yet

- January TribuneDocument16 pagesJanuary TribuneAnonymous KMKk9Msn5No ratings yet

- Baskoro Riyanto - 023001800063 - Latihan Soal AKL IIDocument4 pagesBaskoro Riyanto - 023001800063 - Latihan Soal AKL IIBaskoro RiyantoNo ratings yet

- Raising Dough IntroductionDocument10 pagesRaising Dough IntroductionChelsea Green PublishingNo ratings yet

- Exercise E3-10 and E3-22Document4 pagesExercise E3-10 and E3-22api-269347566No ratings yet

- Chapter 5 - Building Profit PlanDocument28 pagesChapter 5 - Building Profit Plansiyeni100% (2)

- Levine Smume7 Bonus Ch02Document2 pagesLevine Smume7 Bonus Ch02Kiran SoniNo ratings yet

- Bien Dịch 1Document30 pagesBien Dịch 1Gia AnhNo ratings yet

- Lic Under SiegeDocument4 pagesLic Under SiegeAjay Narang0% (1)

- Firms - Entry Tests and Interviews Guidelines (WWW - Gcaofficial.tk)Document13 pagesFirms - Entry Tests and Interviews Guidelines (WWW - Gcaofficial.tk)Munira SheraliNo ratings yet

- Policy ScheduleDocument4 pagesPolicy ScheduleacrajeshNo ratings yet

- Bir Ruling Un 041 95Document2 pagesBir Ruling Un 041 95mikmgonzalesNo ratings yet

- Types of Budgeting Techniques: Topic 4Document59 pagesTypes of Budgeting Techniques: Topic 4Sullivan LyaNo ratings yet

- Oregon Income Tax Instructions and SchedulesDocument36 pagesOregon Income Tax Instructions and SchedulesStatesman JournalNo ratings yet

- Audit of LiabilitiesDocument5 pagesAudit of LiabilitiesGille Rosa Abajar100% (1)

- Chapter 20 Additional Assurance Services Other InformationDocument26 pagesChapter 20 Additional Assurance Services Other InformationburzumagnusNo ratings yet

- Crocs Case StudyDocument15 pagesCrocs Case StudyNida Amri100% (1)

- The Homeowners Guide To A Winning FC Defense-1Document107 pagesThe Homeowners Guide To A Winning FC Defense-1Helpin HandNo ratings yet

- Chapter 1 - Statement of Financial Position - UnlockedDocument2 pagesChapter 1 - Statement of Financial Position - UnlockedJerome_JadeNo ratings yet

- Dissertation On Commercial BanksDocument4 pagesDissertation On Commercial BanksNeedHelpWithPaperSingapore100% (1)

- Math CalculatorsDocument77 pagesMath Calculatorsmizanur rahmanNo ratings yet

- 10 Facts About Sahara India PariwarDocument4 pages10 Facts About Sahara India PariwarRK DeepakNo ratings yet

- ADB Report DISCO Tranche 1Document261 pagesADB Report DISCO Tranche 1Javed RashidNo ratings yet