Download as docx, pdf, or txt

You might also like

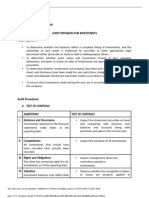

- Audit Program For InvestmentDocument3 pagesAudit Program For InvestmentHannah Tudio100% (1)

- Audit Programme Trade Payables Name of Client Sheridan AV Year-End Name of Auditor (S)Document5 pagesAudit Programme Trade Payables Name of Client Sheridan AV Year-End Name of Auditor (S)Miljane PerdizoNo ratings yet

- D AP InvestmentDocument8 pagesD AP InvestmentAung Zaw HtweNo ratings yet

- Audit Program Npo Grouptask ManaigmercadosalvioDocument5 pagesAudit Program Npo Grouptask Manaigmercadosalvio[AP-Alumni] Sean Xavier SacullesNo ratings yet

- Audit Scope Accounts Involved Audit ProcedureDocument12 pagesAudit Scope Accounts Involved Audit Procedurekarenmae intangNo ratings yet

- 12 Substantive Tests of InvestmentsDocument18 pages12 Substantive Tests of Investmentsashley100% (2)

- Chapter 10 Verification of Balance Sheet Items: 1. ObjectivesDocument23 pagesChapter 10 Verification of Balance Sheet Items: 1. ObjectivesSyed RizviNo ratings yet

- Audit Assertions For Loans Receivables An SCRDocument12 pagesAudit Assertions For Loans Receivables An SCRHygie AlocodNo ratings yet

- Internal Controls Relevant To Financing CycleDocument3 pagesInternal Controls Relevant To Financing CycleEll VNo ratings yet

- Audit Procedures For Liabilities and InvestmentsDocument3 pagesAudit Procedures For Liabilities and InvestmentsDanaNo ratings yet

- Chapter10 - AnswerDocument21 pagesChapter10 - Answershanerikim100% (1)

- 6.4 Assignment - Concept MapDocument3 pages6.4 Assignment - Concept Mapjoint accountNo ratings yet

- A. Key Internal Control B. Transaction Related Audit Objectives C. Test of Control D. Substantive Test of TransactionDocument5 pagesA. Key Internal Control B. Transaction Related Audit Objectives C. Test of Control D. Substantive Test of TransactionRosanaDíazNo ratings yet

- Intangible Assets: Assertions Audit Objectives Audit Procedures I. Existence/ OccurrenceDocument1 pageIntangible Assets: Assertions Audit Objectives Audit Procedures I. Existence/ OccurrencekrizzmaaaayNo ratings yet

- 358763050Document15 pages358763050kristelle0marisseNo ratings yet

- Audit AssertionsDocument1 pageAudit AssertionsDevice Factory UnlockNo ratings yet

- Audit of Item of Financial StatementDocument20 pagesAudit of Item of Financial StatementKushagra BurmanNo ratings yet

- DocxDocument15 pagesDocxjhouvanNo ratings yet

- Audit of Non-Current AssetsDocument15 pagesAudit of Non-Current AssetsArlyn Pearl PradoNo ratings yet

- GROUP 2: Audit of Expenditure Cycle: Tests of Controls and Substantive Tests of Transactions - I by CabreraDocument3 pagesGROUP 2: Audit of Expenditure Cycle: Tests of Controls and Substantive Tests of Transactions - I by Cabreratankofdoom 4No ratings yet

- Audit Program Npo Grouptask ManaigmercadosalvioDocument5 pagesAudit Program Npo Grouptask Manaigmercadosalvio[AP-Alumni] Sean Xavier SacullesNo ratings yet

- CaroDocument12 pagesCaroAbhay KumarNo ratings yet

- Audit Program: Property Plant and EquipmentDocument8 pagesAudit Program: Property Plant and EquipmentAqib Sheikh100% (3)

- Ada Iii Audit of Fixed AssetsDocument6 pagesAda Iii Audit of Fixed AssetsOmega MwakalikamoNo ratings yet

- 3.1 Audit of Purchases and PayablesDocument1 page3.1 Audit of Purchases and PayablesNavsNo ratings yet

- T A T I: Investing Cycle Learning ObjectivesDocument15 pagesT A T I: Investing Cycle Learning ObjectivesAngelo PayawalNo ratings yet

- Audit Program-Accrued ExpensesDocument10 pagesAudit Program-Accrued ExpensesPutu Adi NugrahaNo ratings yet

- 7 Cation Vmuation OF Assets and Liabilities Ii: StructureDocument6 pages7 Cation Vmuation OF Assets and Liabilities Ii: StructureApoorva BhardwajNo ratings yet

- Module 6 INVESTMENT IN FINANCIAL INSTRUMENTS PDFDocument8 pagesModule 6 INVESTMENT IN FINANCIAL INSTRUMENTS PDFNiño Mendoza MabatoNo ratings yet

- 19k (12-00) Develop The Audit Program - EquityDocument2 pages19k (12-00) Develop The Audit Program - EquityAnh Tuấn TrầnNo ratings yet

- Verification of Asset and Liability Que AuditDocument28 pagesVerification of Asset and Liability Que AuditAhisjNo ratings yet

- Fixed AssetsDocument10 pagesFixed AssetsMikka JoyNo ratings yet

- Audit Program-Fixed AssetsDocument7 pagesAudit Program-Fixed AssetsNaomiNo ratings yet

- Audit of Trade Receivables and Sales BalancesDocument2 pagesAudit of Trade Receivables and Sales BalancesDiane VillarmaNo ratings yet

- Audit SlideDocument22 pagesAudit SlideVaradan K RajendranNo ratings yet

- Trade-Payable DiscussionsDocument7 pagesTrade-Payable DiscussionsShena RieNo ratings yet

- Problem CH 6,7,8 - Amelia Zulaikha Pratiwi - MAKSI43BDocument4 pagesProblem CH 6,7,8 - Amelia Zulaikha Pratiwi - MAKSI43Bamelia zulaikhaNo ratings yet

- AP - Property, Plant and EquipmentDocument6 pagesAP - Property, Plant and EquipmentRhuejane Gay MaquilingNo ratings yet

- IFC TXT Glossary 2021 12 EN V01 PDFDocument24 pagesIFC TXT Glossary 2021 12 EN V01 PDFNiayesh AsgariNo ratings yet

- Acctng 9.4 Substantive Tests of Assets (Summary)Document6 pagesAcctng 9.4 Substantive Tests of Assets (Summary)03LJNo ratings yet

- AP.3406 Audit of InvestmentsDocument5 pagesAP.3406 Audit of InvestmentsMonica GarciaNo ratings yet

- Audit of InvestmentsDocument6 pagesAudit of InvestmentsGille Rosa AbajarNo ratings yet

- Possible Potential Misstatement in The Process of Audit: Ra1. Process Flow DiagramDocument10 pagesPossible Potential Misstatement in The Process of Audit: Ra1. Process Flow DiagramKhyla DivinagraciaNo ratings yet

- AP.2906 InvestmentsDocument6 pagesAP.2906 InvestmentsmoNo ratings yet

- Audit of SHEDocument7 pagesAudit of SHEGille Rosa AbajarNo ratings yet

- Audit of Investment-LectureDocument15 pagesAudit of Investment-LecturemoNo ratings yet

- Audit-Report-Sena KaylanDocument50 pagesAudit-Report-Sena KaylanSohag AMLNo ratings yet

- Audit 2, AEC-64 AUDIT PPEDocument5 pagesAudit 2, AEC-64 AUDIT PPEShaz NagaNo ratings yet

- SUBJECT: Accounting 13 NC Descriptive Title: Auditing and Assurance Concepts and Applications 1Document12 pagesSUBJECT: Accounting 13 NC Descriptive Title: Auditing and Assurance Concepts and Applications 1Prince CalicaNo ratings yet

- Audit of Trade Receivables and Sales BalancesDocument3 pagesAudit of Trade Receivables and Sales BalancesdidiaenNo ratings yet

- Audit of Trade Receivables and Sales BalancesDocument3 pagesAudit of Trade Receivables and Sales BalancesdidiaenNo ratings yet

- Audit of Trade Receivables and Sales BalancesDocument3 pagesAudit of Trade Receivables and Sales BalancesdidiaenNo ratings yet

- Audit Program For Other IncomeDocument3 pagesAudit Program For Other IncomeCollins O.71% (7)

- Substantive Tests and Audit ProgramDocument35 pagesSubstantive Tests and Audit ProgramPamimoomimap Rufila100% (1)

- Applicable To Accounts Receivables Assertion Category (CREV) Audit Objectives Audit ProceduresDocument3 pagesApplicable To Accounts Receivables Assertion Category (CREV) Audit Objectives Audit ProceduresRosept ParnesNo ratings yet

- For Each Class of Share Capital (Different Classes of Preference Shares To Be Treated Separately)Document19 pagesFor Each Class of Share Capital (Different Classes of Preference Shares To Be Treated Separately)abhishek dalwaniNo ratings yet

- Investment Pricing Methods: A Guide for Accounting and Financial ProfessionalsFrom EverandInvestment Pricing Methods: A Guide for Accounting and Financial ProfessionalsNo ratings yet

- How to Select Investment Managers and Evaluate Performance: A Guide for Pension Funds, Endowments, Foundations, and TrustsFrom EverandHow to Select Investment Managers and Evaluate Performance: A Guide for Pension Funds, Endowments, Foundations, and TrustsNo ratings yet

- About FRSC and PIC: A Chairman and MembersDocument2 pagesAbout FRSC and PIC: A Chairman and MembersChristian PerezNo ratings yet

- Spanish Romantic Panorama:: Romanticism RomanticismDocument3 pagesSpanish Romantic Panorama:: Romanticism RomanticismChristian PerezNo ratings yet

- CISDocument5 pagesCISChristian PerezNo ratings yet

- ArnisDocument2 pagesArnisChristian PerezNo ratings yet

- Substantive Procedures For Evaluation of LoansDocument3 pagesSubstantive Procedures For Evaluation of LoansChristian PerezNo ratings yet

- Substantive Procedures For ReceivablesDocument3 pagesSubstantive Procedures For ReceivablesChristian PerezNo ratings yet

- Substantive Testing For Deposit LiabilitiesDocument3 pagesSubstantive Testing For Deposit LiabilitiesChristian PerezNo ratings yet

- Substantive Testing For Deposit LiabilitiesDocument3 pagesSubstantive Testing For Deposit LiabilitiesChristian PerezNo ratings yet

- Applications of Plant Genetic EngineeringDocument3 pagesApplications of Plant Genetic EngineeringChristian PerezNo ratings yet

- Evaluate Vendor LTSADocument2 pagesEvaluate Vendor LTSAApri Kartiwan100% (1)

- Terraria Official Lore PDFDocument3 pagesTerraria Official Lore PDFCavalo SebosoNo ratings yet

- LevellingDocument11 pagesLevellingetikaf50% (2)

- Smietanka v. First Trust & Savings Bank: 257 U.S. 602 (1922) : Justia US Supreme Court CenterDocument1 pageSmietanka v. First Trust & Savings Bank: 257 U.S. 602 (1922) : Justia US Supreme Court CenterChou TakahiroNo ratings yet

- Energy and Energy Transformations: Energy Makes Things HappenDocument8 pagesEnergy and Energy Transformations: Energy Makes Things HappenLabeenaNo ratings yet

- CCC Question Paper 2017 With Answer PDF Online Test For Computer - Current Affairs Recruitment News TodayDocument6 pagesCCC Question Paper 2017 With Answer PDF Online Test For Computer - Current Affairs Recruitment News Todayjit19942007No ratings yet

- Warman Slurry Correction Factors HR and ER Pump Power: MPC H S S L Q PDocument2 pagesWarman Slurry Correction Factors HR and ER Pump Power: MPC H S S L Q Pyoel cueva arquinigoNo ratings yet

- Cartilla Didactica de Negocios y ContabilidadDocument118 pagesCartilla Didactica de Negocios y ContabilidadJesus Angel SalvadorNo ratings yet

- WVA Consulting Engineers PVT LTD: Analsyis and Design of Steel Watch TowerDocument23 pagesWVA Consulting Engineers PVT LTD: Analsyis and Design of Steel Watch TowerRomyMohanNo ratings yet

- 3500 Most Common Chinese CharactersDocument2 pages3500 Most Common Chinese CharactersSub 2 PewdsNo ratings yet

- Server Poweredge t610 Tech Guidebook PDFDocument65 pagesServer Poweredge t610 Tech Guidebook PDFMarouani AmorNo ratings yet

- CH 01 Wooldridge 5e PPTDocument23 pagesCH 01 Wooldridge 5e PPTKrithiga Soundrajan100% (1)

- Applied Physics On Spectros PDFDocument71 pagesApplied Physics On Spectros PDFKaskus FourusNo ratings yet

- MUXDocument5 pagesMUXAmit SahaNo ratings yet

- 4ipnet Solution HotelDocument27 pages4ipnet Solution HotelAdrian Gamboa MarcellanaNo ratings yet

- Zipatile ManualDocument16 pagesZipatile ManualdacrysNo ratings yet

- 5) BL Corrector y Manifiesto de CargaDocument3 pages5) BL Corrector y Manifiesto de CargaKevin Yair FerrerNo ratings yet

- EE210 Hoja Datos SensovantDocument5 pagesEE210 Hoja Datos SensovantCoco SanchezNo ratings yet

- Endurance Test Sit UpDocument2 pagesEndurance Test Sit UpDinyoga Bima WaskitoNo ratings yet

- Boli Interne Vol I Partea 1Document454 pagesBoli Interne Vol I Partea 1Murariu Diana100% (2)

- Aprovel TabletDocument7 pagesAprovel Tabletramesh4321No ratings yet

- MonotropismQuestionnaire 230510Document5 pagesMonotropismQuestionnaire 230510Javiera AlarconNo ratings yet

- W2AEW Videos (Apr 29, 2017) : Topics Listed NumericallyDocument12 pagesW2AEW Videos (Apr 29, 2017) : Topics Listed Numericallyamol1agarwalNo ratings yet

- Lecturers HO No. 9 2023 Pre Week in Commercial LawDocument94 pagesLecturers HO No. 9 2023 Pre Week in Commercial LawElle WoodsNo ratings yet

- Paint Data Sheet - National Synthetic Enamel Gloss IDocument3 pagesPaint Data Sheet - National Synthetic Enamel Gloss Iaakh0% (1)

- 20220725Document39 pages20220725Zenon CondoriNo ratings yet

- Power EPC ConsultantsDocument189 pagesPower EPC Consultantsanooppellissery20097159100% (1)

- Residence Time Distribution For Chemical ReactorsDocument71 pagesResidence Time Distribution For Chemical ReactorsJuan Carlos Serrano MedranoNo ratings yet

- KMA CVDocument5 pagesKMA CVKhandoker Mostak AhamedNo ratings yet

- 400 Bad Request 400 Bad Request Nginx/1.2.9Document13 pages400 Bad Request 400 Bad Request Nginx/1.2.9USAFVOSBNo ratings yet