Download as pdf or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5834)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (903)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (350)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (824)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Ein Letter RyanDocument2 pagesEin Letter Ryanphillip davisNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (405)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- IPPIS - Oracle E-Business Suite: Federal Government of NigeriaDocument18 pagesIPPIS - Oracle E-Business Suite: Federal Government of Nigeriamustapha kamilu100% (1)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Emotional Intelligence and Leadership Effectiveness: The Mediating Influence of Collaborative BehaviorsDocument30 pagesEmotional Intelligence and Leadership Effectiveness: The Mediating Influence of Collaborative Behaviorsaadil002No ratings yet

- Pro Omer MasoodDocument73 pagesPro Omer Masoodaadil002No ratings yet

- Sales Tax Act, 1990Document122 pagesSales Tax Act, 1990aadil002100% (1)

- Import Policy Order, 2008Document112 pagesImport Policy Order, 2008Asad SultaniNo ratings yet

- ESSO v. CIR, 175 SCRA 149 (1989)Document13 pagesESSO v. CIR, 175 SCRA 149 (1989)citizenNo ratings yet

- Airtel Broadband Bill - DecDocument1 pageAirtel Broadband Bill - DecSubhani NaniNo ratings yet

- Etaxguide - Cit - Tax Exemption Under Section 13 (12) - (8th Edition)Document34 pagesEtaxguide - Cit - Tax Exemption Under Section 13 (12) - (8th Edition)LomomivNo ratings yet

- Upgrade MID Non HNW Classic Customer Version PDFDocument2 pagesUpgrade MID Non HNW Classic Customer Version PDFRamboNo ratings yet

- Pointers To Review BUSINESS TAXATIONDocument4 pagesPointers To Review BUSINESS TAXATIONFaizal MutiaNo ratings yet

- Biologicla Assets PDFDocument2 pagesBiologicla Assets PDFMjhayeNo ratings yet

- Indwdhi 20231031Document9 pagesIndwdhi 20231031AKMA SAUPINo ratings yet

- Environmental Services Inc Performs Various Tests On Wells and SepticDocument1 pageEnvironmental Services Inc Performs Various Tests On Wells and Septictrilocksp SinghNo ratings yet

- Congratulations On The Bonus Accrued!: Gajbhiye AmitkumarDocument2 pagesCongratulations On The Bonus Accrued!: Gajbhiye Amitkumaramit gajbhiyeNo ratings yet

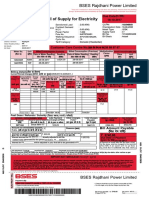

- Bill of Supply For Electricity: BSES Rajdhani Power LimitedDocument4 pagesBill of Supply For Electricity: BSES Rajdhani Power LimitedHema KatiyarNo ratings yet

- Scan 3 Mar 2020Document1 pageScan 3 Mar 2020Sandeep ChoudharyNo ratings yet

- Section A: 40, Main Street, GeorgetownDocument1 pageSection A: 40, Main Street, GeorgetownKatty DeFreitasNo ratings yet

- VAT-Computation 2Document28 pagesVAT-Computation 2Alvin Dagohoy100% (1)

- This Study Resource Was: F, Sold The Following Capital AssetsDocument2 pagesThis Study Resource Was: F, Sold The Following Capital AssetsDheyreil Eden Kaylah ParaisoNo ratings yet

- Message Grammar School Message Grammar School Message Grammar SchoolDocument1 pageMessage Grammar School Message Grammar School Message Grammar SchoolUMW BrosNo ratings yet

- Tax Planning and ManagementDocument23 pagesTax Planning and Managementarchana_anuragi100% (1)

- Tax InvoiceDocument1 pageTax InvoiceAsif IqbalNo ratings yet

- URSP - Billing Invoice - Homeworld Surveillance 2021Document1 pageURSP - Billing Invoice - Homeworld Surveillance 2021Julie Ann TolosaNo ratings yet

- CitiBank-Statement Jan01-Jan30Document2 pagesCitiBank-Statement Jan01-Jan30hzservices70No ratings yet

- Government Accounting: Accounting For Income and Other Cash ReceiptsDocument18 pagesGovernment Accounting: Accounting For Income and Other Cash ReceiptsJoan May PeraltaNo ratings yet

- Akhil June ExpenseDocument4 pagesAkhil June ExpenseNitinkiet103No ratings yet

- IBBL Contact Center: Born To SmileDocument1 pageIBBL Contact Center: Born To SmilerubelNo ratings yet

- AP-AR Netting SetupDocument45 pagesAP-AR Netting Setupchandra_wakarNo ratings yet

- DJBBill 098235179545Document3 pagesDJBBill 098235179545Arijit paulNo ratings yet

- May 2018 SGV SDGSDDocument26 pagesMay 2018 SGV SDGSDBien Bowie A. CortezNo ratings yet

- Bill To / Ship To:: Qty Gross Amount Discount Other Charges Taxable Amount CGST SGST/ Ugst Igst Cess Total AmountDocument1 pageBill To / Ship To:: Qty Gross Amount Discount Other Charges Taxable Amount CGST SGST/ Ugst Igst Cess Total AmountRahul Giri (Logistics)No ratings yet

- The Good, The Bad, and The UglyDocument13 pagesThe Good, The Bad, and The UglyTanvir AhmedNo ratings yet

- SAP BPC Dimensions MembersDocument22 pagesSAP BPC Dimensions MembersMahesh Reddy MNo ratings yet