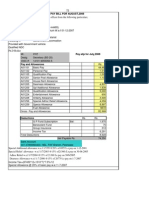

Criteria For Advance para

Criteria For Advance para

You might also like

- Allotment LetterDocument7 pagesAllotment LetterDharma Tej ReddyNo ratings yet

- Award: Diploma in Management Award: Executive Diploma in ManagementDocument4 pagesAward: Diploma in Management Award: Executive Diploma in Managementsheetal.kakar5338No ratings yet

- Notification-UPPER PRIMARY-2016 Web PDFDocument12 pagesNotification-UPPER PRIMARY-2016 Web PDFNitai Chandra GangulyNo ratings yet

- Review Engagements Section General Review Standards: Scope and DefinitionsDocument7 pagesReview Engagements Section General Review Standards: Scope and DefinitionsFallon LoboNo ratings yet

- Gilgit Baltistan System of Financial Control 2009Document55 pagesGilgit Baltistan System of Financial Control 2009Muhammad ShakirNo ratings yet

- Robinhood:Buying A Stock As Quickly As You'd Post An Instagram PhotoDocument3 pagesRobinhood:Buying A Stock As Quickly As You'd Post An Instagram PhotoHarshil JhaveriNo ratings yet

- BPM - Practice Exercise For Final ExamDocument3 pagesBPM - Practice Exercise For Final ExamAmit KumarNo ratings yet

- Refinery Operating Cost: Chapter NineteenDocument10 pagesRefinery Operating Cost: Chapter NineteenJuan Manuel FigueroaNo ratings yet

- Acturarial Mathematics - BowersDocument780 pagesActurarial Mathematics - BowersEstefanía Luna Flores100% (1)

- AEOs JDs & KPIsDocument9 pagesAEOs JDs & KPIsRashid0% (1)

- HRMIS FormDocument1 pageHRMIS FormShaloom TVNo ratings yet

- Revised Promotion Policy DAGP Govt - of PakistanDocument3 pagesRevised Promotion Policy DAGP Govt - of PakistanKhurram SherazNo ratings yet

- New Rules SOPE 2015Document8 pagesNew Rules SOPE 2015Farrukh Shoukat Ali100% (1)

- Wad ManualDocument123 pagesWad Manualmuhammad yasirNo ratings yet

- Consolidated AR DEA DGA 2018-19 31.01.19 (Printed)Document811 pagesConsolidated AR DEA DGA 2018-19 31.01.19 (Printed)Abc DefNo ratings yet

- Leave RegulationsDocument182 pagesLeave RegulationsanilpalacherlaNo ratings yet

- NCDDP Revised CBPM Volume One Ver Oct25 - 2014Document149 pagesNCDDP Revised CBPM Volume One Ver Oct25 - 2014ARTHUR R MARCONo ratings yet

- BISCAST AOM 2018-010 (2018) JanitorialDocument3 pagesBISCAST AOM 2018-010 (2018) Janitorialjaymark camachoNo ratings yet

- Cadre Review ReportDocument14 pagesCadre Review ReportvadrevusriNo ratings yet

- LetterDocument3 pagesLetterlovetolife95No ratings yet

- KP Delegation of Financial Power Rules 2018Document47 pagesKP Delegation of Financial Power Rules 2018Abdul Rab NishterNo ratings yet

- Wafaqi Mohtasib RulesDocument43 pagesWafaqi Mohtasib Ruleshumayunnawaz75% (4)

- Sample Tender DraftDocument50 pagesSample Tender DraftDr-Kamal ArifNo ratings yet

- Guidelines SOP ACcounting SystemDocument5 pagesGuidelines SOP ACcounting SystemDr-Kamal ArifNo ratings yet

- (PRC) Professional Regulation Commission HistoryDocument4 pages(PRC) Professional Regulation Commission HistoryElizabeth SulitNo ratings yet

- Internship Report RimshaDocument23 pagesInternship Report RimshaRimsha ButtNo ratings yet

- Case Bannerman Royal BankDocument4 pagesCase Bannerman Royal BankFatinah HusnaNo ratings yet

- CPD Guideline PDFDocument16 pagesCPD Guideline PDFLy Lo OnNo ratings yet

- 1 Auditing Standards, Statements and Guidance Notes - An Overview PDFDocument24 pages1 Auditing Standards, Statements and Guidance Notes - An Overview PDFnavyaNo ratings yet

- QMF Approved and CirculatedDocument78 pagesQMF Approved and CirculatedMuhammad Amir Usman100% (1)

- WWW Apspsc Gov inDocument16 pagesWWW Apspsc Gov inkeerthymamidiNo ratings yet

- PC 22 Point Wise - MSO (Audit) - 1Document19 pagesPC 22 Point Wise - MSO (Audit) - 1manoj sainiNo ratings yet

- AGP Power FunctionDocument20 pagesAGP Power FunctionFayaz KhanNo ratings yet

- Re-Certification Audit of Iso 9001:2015: ST NDDocument4 pagesRe-Certification Audit of Iso 9001:2015: ST NDLiaqatNo ratings yet

- HBL Scheme For StaffDocument5 pagesHBL Scheme For Staffhimadri_bhattacharjeNo ratings yet

- PQA Service Rules-77uDocument90 pagesPQA Service Rules-77uabdul basit100% (1)

- Leave Rules1Document13 pagesLeave Rules1Bhabani Shankar NaikNo ratings yet

- Application For Appearing in The DAO ExaminationDocument1 pageApplication For Appearing in The DAO ExaminationmmubashariqbalNo ratings yet

- Faculty-Merit-System ReferenceDocument31 pagesFaculty-Merit-System ReferenceLavander BlushNo ratings yet

- CA Inter SM Chapter 7 Nov.21Document37 pagesCA Inter SM Chapter 7 Nov.21vipulNo ratings yet

- LGU-NGAS TableofContentsVol1Document6 pagesLGU-NGAS TableofContentsVol1Pee-Jay Inigo UlitaNo ratings yet

- Regulations UET LHRDocument11 pagesRegulations UET LHRMuhammad TausifNo ratings yet

- Status of Unliquidated Cash Advance, Fund Transfers, and Other ReceivablesDocument9 pagesStatus of Unliquidated Cash Advance, Fund Transfers, and Other ReceivablesRD MomoNo ratings yet

- PRTCDocument25 pagesPRTCJasmandeep brarNo ratings yet

- Pà Áðlpà Àpáðgà: Á Àðd Pà Àauàæºàuéuà À°È Ágàzà Àðpàvé Pá Äzé, 1999Document15 pagesPà Áðlpà Àpáðgà: Á Àðd Pà Àauàæºàuéuà À°È Ágàzà Àðpàvé Pá Äzé, 1999SjNo ratings yet

- Probation Rules PDFDocument7 pagesProbation Rules PDFSulekha BhattacherjeeNo ratings yet

- Cross-Functional Information Systems: Presented By: Khurram Sheraz Gondal Roll # 508194692Document26 pagesCross-Functional Information Systems: Presented By: Khurram Sheraz Gondal Roll # 508194692Khurram SherazNo ratings yet

- General Provident Fund Rules PDFDocument65 pagesGeneral Provident Fund Rules PDFMuhammad ImranNo ratings yet

- Faqs NfuDocument16 pagesFaqs NfuhagdincloobleNo ratings yet

- Rules For Affiliation N.T.BDocument6 pagesRules For Affiliation N.T.BMuhammad SajidNo ratings yet

- A Hand Book of DDO'sDocument472 pagesA Hand Book of DDO'sRizwan HaiderNo ratings yet

- Power To Arrest For The Purposes of InvestigationDocument3 pagesPower To Arrest For The Purposes of InvestigationEsha HarizanNo ratings yet

- Surplus Rules 2002Document33 pagesSurplus Rules 2002adhityaNo ratings yet

- PSC Circular 52 - Graduate Trainee Scheme Policy in The Public Service PDFDocument9 pagesPSC Circular 52 - Graduate Trainee Scheme Policy in The Public Service PDFManoa Nagatalevu TupouNo ratings yet

- ParangalDocument34 pagesParangalMarc Benedict TalamayanNo ratings yet

- SOP Part 2Document267 pagesSOP Part 2Ajoydeep DasNo ratings yet

- Audit CodeDocument140 pagesAudit CodeKhurram SherazNo ratings yet

- Bofp 2022Document149 pagesBofp 2022ali shahNo ratings yet

- Project HR Practices in Wapda: Submitted To Riaz Toor Subject HR Course MBA - 2 (N) Submitted by Rana Faisal AliDocument50 pagesProject HR Practices in Wapda: Submitted To Riaz Toor Subject HR Course MBA - 2 (N) Submitted by Rana Faisal AliSyeda DilawaizNo ratings yet

- At A Glance - Annual-14Document131 pagesAt A Glance - Annual-14dvgtexNo ratings yet

- Student Pass Application Format 0 PDFDocument1 pageStudent Pass Application Format 0 PDFmanojnaNo ratings yet

- System of Financial Control & Budgeting 2006 (Updated October 2018)Document51 pagesSystem of Financial Control & Budgeting 2006 (Updated October 2018)usman ziaNo ratings yet

- MPFCV 1 CH 2Document10 pagesMPFCV 1 CH 2mahendra singhNo ratings yet

- Financial Code Reading Material Final (1)Document68 pagesFinancial Code Reading Material Final (1)sumedhNo ratings yet

- Applications - English GrammarDocument7 pagesApplications - English GrammarFayaz Khan100% (3)

- Minutes of 41 BoD Meeting PDFDocument27 pagesMinutes of 41 BoD Meeting PDFFayaz KhanNo ratings yet

- UntitledDocument10 pagesUntitledFayaz KhanNo ratings yet

- BS-20 Seniority List 01-01-2022Document7 pagesBS-20 Seniority List 01-01-2022Fayaz KhanNo ratings yet

- Advertisment of Driver ForwardingDocument1 pageAdvertisment of Driver ForwardingFayaz KhanNo ratings yet

- UntitledDocument7 pagesUntitledFayaz KhanNo ratings yet

- Advance para 113Document10 pagesAdvance para 113Fayaz KhanNo ratings yet

- BS-19 Seniority List 01 - 01 - 2022Document8 pagesBS-19 Seniority List 01 - 01 - 2022Fayaz KhanNo ratings yet

- Audit Note ChitralDocument23 pagesAudit Note ChitralFayaz KhanNo ratings yet

- Receipt Payment: Detail of Closing BalanceDocument2 pagesReceipt Payment: Detail of Closing BalanceFayaz KhanNo ratings yet

- Kahi DimolishDocument2 pagesKahi DimolishFayaz KhanNo ratings yet

- 2651 of CWDocument9 pages2651 of CWFayaz KhanNo ratings yet

- Phe Batagram Payroll 01-2021Document97 pagesPhe Batagram Payroll 01-2021Fayaz KhanNo ratings yet

- Demand For Fund Under ADP No. 516Document1 pageDemand For Fund Under ADP No. 516Fayaz KhanNo ratings yet

- GPF FinalpmtDocument4 pagesGPF FinalpmtFayaz KhanNo ratings yet

- GPF FinalpmtDocument4 pagesGPF FinalpmtFayaz KhanNo ratings yet

- Age CalculationDocument2 pagesAge CalculationFayaz KhanNo ratings yet

- IN Case OF Death: ApplicationDocument1 pageIN Case OF Death: ApplicationFayaz KhanNo ratings yet

- Pay BillDocument1 pagePay BillFayaz KhanNo ratings yet

- TG TG 9780195979688 2Document149 pagesTG TG 9780195979688 2Fayaz KhanNo ratings yet

- Zahid New CVDocument6 pagesZahid New CVzahid khanNo ratings yet

- Cook Vernice - AC 404 Accounting Info SystemDocument2 pagesCook Vernice - AC 404 Accounting Info SystemVernice LutoNo ratings yet

- A Industrial Visit Report On Diamond Beverages Pvt. LTD.: Diploma in Mechanical EngineeringDocument17 pagesA Industrial Visit Report On Diamond Beverages Pvt. LTD.: Diploma in Mechanical EngineeringAryan Kumar100% (1)

- Business Law Course Work 4 816020005Document9 pagesBusiness Law Course Work 4 816020005Christian SteeleNo ratings yet

- Audit Reviewer Sample 2Document13 pagesAudit Reviewer Sample 2ChinNo ratings yet

- Chapter 8Document17 pagesChapter 8Jamaica DavidNo ratings yet

- Real Estate Economics PDFDocument88 pagesReal Estate Economics PDFTekeba BirhaneNo ratings yet

- Purple White Bold Modern Digital Marketer CVDocument2 pagesPurple White Bold Modern Digital Marketer CVPurnima Swami (Lecturer & Promoter)No ratings yet

- Drywall Feasibility Study 1Document31 pagesDrywall Feasibility Study 1Firas AbsaNo ratings yet

- EStatement 2020 08 27 78283Document5 pagesEStatement 2020 08 27 78283abalaibemeNo ratings yet

- FJFJFJFJDocument12 pagesFJFJFJFJnuravcool76No ratings yet

- 3M India Limited - Annual Report 2015-16Document144 pages3M India Limited - Annual Report 2015-16Ishpreet singhNo ratings yet

- Ningbo L & M International Trading Co., LTDDocument1 pageNingbo L & M International Trading Co., LTDوليد سالمNo ratings yet

- Calculator New Pay ScaleDocument4 pagesCalculator New Pay Scalerocky_ecNo ratings yet

- Tizon vs. Valdez & Morales, 48 Phil 910Document3 pagesTizon vs. Valdez & Morales, 48 Phil 910Al Jay MejosNo ratings yet

- Tut - Week 3.v2Document16 pagesTut - Week 3.v2peter kongNo ratings yet

- Delivery Hero SE - Trading Update Q1 2024Document47 pagesDelivery Hero SE - Trading Update Q1 2024koteshchoudaryNo ratings yet

- AUSL Bar Operations 2017 LMT Property EditedDocument6 pagesAUSL Bar Operations 2017 LMT Property EditedEron Roi Centina-gacutanNo ratings yet

- 2016 Nomura Summer Internship ProgramDocument25 pages2016 Nomura Summer Internship ProgramTing-An KuoNo ratings yet

- 46793bosinter p8 Seca cp5 PDFDocument42 pages46793bosinter p8 Seca cp5 PDFIsavic AlsinaNo ratings yet

- Saving AcDocument5 pagesSaving AcRohit raagNo ratings yet

- Problems On Flexible BudgetDocument3 pagesProblems On Flexible BudgetsafwanhossainNo ratings yet

- Financial Model Template by SlidebeanDocument363 pagesFinancial Model Template by SlidebeanYargop AnalyticsNo ratings yet

- Test Bank For Macroeconomics 2nd Edition Full DownloadDocument48 pagesTest Bank For Macroeconomics 2nd Edition Full Downloadmichaelbirdgznspejbwa100% (22)

- Caf-8 Mindmaps-69Document19 pagesCaf-8 Mindmaps-69Muhammad ImranNo ratings yet

- Test Bank: Corporate RestructuringDocument3 pagesTest Bank: Corporate RestructuringYoukayzeeNo ratings yet

Download as doc, pdf, or txt

You might also like

- Allotment LetterDocument7 pagesAllotment LetterDharma Tej ReddyNo ratings yet

- Award: Diploma in Management Award: Executive Diploma in ManagementDocument4 pagesAward: Diploma in Management Award: Executive Diploma in Managementsheetal.kakar5338No ratings yet

- Notification-UPPER PRIMARY-2016 Web PDFDocument12 pagesNotification-UPPER PRIMARY-2016 Web PDFNitai Chandra GangulyNo ratings yet

- Review Engagements Section General Review Standards: Scope and DefinitionsDocument7 pagesReview Engagements Section General Review Standards: Scope and DefinitionsFallon LoboNo ratings yet

- Gilgit Baltistan System of Financial Control 2009Document55 pagesGilgit Baltistan System of Financial Control 2009Muhammad ShakirNo ratings yet

- Robinhood:Buying A Stock As Quickly As You'd Post An Instagram PhotoDocument3 pagesRobinhood:Buying A Stock As Quickly As You'd Post An Instagram PhotoHarshil JhaveriNo ratings yet

- BPM - Practice Exercise For Final ExamDocument3 pagesBPM - Practice Exercise For Final ExamAmit KumarNo ratings yet

- Refinery Operating Cost: Chapter NineteenDocument10 pagesRefinery Operating Cost: Chapter NineteenJuan Manuel FigueroaNo ratings yet

- Acturarial Mathematics - BowersDocument780 pagesActurarial Mathematics - BowersEstefanía Luna Flores100% (1)

- AEOs JDs & KPIsDocument9 pagesAEOs JDs & KPIsRashid0% (1)

- HRMIS FormDocument1 pageHRMIS FormShaloom TVNo ratings yet

- Revised Promotion Policy DAGP Govt - of PakistanDocument3 pagesRevised Promotion Policy DAGP Govt - of PakistanKhurram SherazNo ratings yet

- New Rules SOPE 2015Document8 pagesNew Rules SOPE 2015Farrukh Shoukat Ali100% (1)

- Wad ManualDocument123 pagesWad Manualmuhammad yasirNo ratings yet

- Consolidated AR DEA DGA 2018-19 31.01.19 (Printed)Document811 pagesConsolidated AR DEA DGA 2018-19 31.01.19 (Printed)Abc DefNo ratings yet

- Leave RegulationsDocument182 pagesLeave RegulationsanilpalacherlaNo ratings yet

- NCDDP Revised CBPM Volume One Ver Oct25 - 2014Document149 pagesNCDDP Revised CBPM Volume One Ver Oct25 - 2014ARTHUR R MARCONo ratings yet

- BISCAST AOM 2018-010 (2018) JanitorialDocument3 pagesBISCAST AOM 2018-010 (2018) Janitorialjaymark camachoNo ratings yet

- Cadre Review ReportDocument14 pagesCadre Review ReportvadrevusriNo ratings yet

- LetterDocument3 pagesLetterlovetolife95No ratings yet

- KP Delegation of Financial Power Rules 2018Document47 pagesKP Delegation of Financial Power Rules 2018Abdul Rab NishterNo ratings yet

- Wafaqi Mohtasib RulesDocument43 pagesWafaqi Mohtasib Ruleshumayunnawaz75% (4)

- Sample Tender DraftDocument50 pagesSample Tender DraftDr-Kamal ArifNo ratings yet

- Guidelines SOP ACcounting SystemDocument5 pagesGuidelines SOP ACcounting SystemDr-Kamal ArifNo ratings yet

- (PRC) Professional Regulation Commission HistoryDocument4 pages(PRC) Professional Regulation Commission HistoryElizabeth SulitNo ratings yet

- Internship Report RimshaDocument23 pagesInternship Report RimshaRimsha ButtNo ratings yet

- Case Bannerman Royal BankDocument4 pagesCase Bannerman Royal BankFatinah HusnaNo ratings yet

- CPD Guideline PDFDocument16 pagesCPD Guideline PDFLy Lo OnNo ratings yet

- 1 Auditing Standards, Statements and Guidance Notes - An Overview PDFDocument24 pages1 Auditing Standards, Statements and Guidance Notes - An Overview PDFnavyaNo ratings yet

- QMF Approved and CirculatedDocument78 pagesQMF Approved and CirculatedMuhammad Amir Usman100% (1)

- WWW Apspsc Gov inDocument16 pagesWWW Apspsc Gov inkeerthymamidiNo ratings yet

- PC 22 Point Wise - MSO (Audit) - 1Document19 pagesPC 22 Point Wise - MSO (Audit) - 1manoj sainiNo ratings yet

- AGP Power FunctionDocument20 pagesAGP Power FunctionFayaz KhanNo ratings yet

- Re-Certification Audit of Iso 9001:2015: ST NDDocument4 pagesRe-Certification Audit of Iso 9001:2015: ST NDLiaqatNo ratings yet

- HBL Scheme For StaffDocument5 pagesHBL Scheme For Staffhimadri_bhattacharjeNo ratings yet

- PQA Service Rules-77uDocument90 pagesPQA Service Rules-77uabdul basit100% (1)

- Leave Rules1Document13 pagesLeave Rules1Bhabani Shankar NaikNo ratings yet

- Application For Appearing in The DAO ExaminationDocument1 pageApplication For Appearing in The DAO ExaminationmmubashariqbalNo ratings yet

- Faculty-Merit-System ReferenceDocument31 pagesFaculty-Merit-System ReferenceLavander BlushNo ratings yet

- CA Inter SM Chapter 7 Nov.21Document37 pagesCA Inter SM Chapter 7 Nov.21vipulNo ratings yet

- LGU-NGAS TableofContentsVol1Document6 pagesLGU-NGAS TableofContentsVol1Pee-Jay Inigo UlitaNo ratings yet

- Regulations UET LHRDocument11 pagesRegulations UET LHRMuhammad TausifNo ratings yet

- Status of Unliquidated Cash Advance, Fund Transfers, and Other ReceivablesDocument9 pagesStatus of Unliquidated Cash Advance, Fund Transfers, and Other ReceivablesRD MomoNo ratings yet

- PRTCDocument25 pagesPRTCJasmandeep brarNo ratings yet

- Pà Áðlpà Àpáðgà: Á Àðd Pà Àauàæºàuéuà À°È Ágàzà Àðpàvé Pá Äzé, 1999Document15 pagesPà Áðlpà Àpáðgà: Á Àðd Pà Àauàæºàuéuà À°È Ágàzà Àðpàvé Pá Äzé, 1999SjNo ratings yet

- Probation Rules PDFDocument7 pagesProbation Rules PDFSulekha BhattacherjeeNo ratings yet

- Cross-Functional Information Systems: Presented By: Khurram Sheraz Gondal Roll # 508194692Document26 pagesCross-Functional Information Systems: Presented By: Khurram Sheraz Gondal Roll # 508194692Khurram SherazNo ratings yet

- General Provident Fund Rules PDFDocument65 pagesGeneral Provident Fund Rules PDFMuhammad ImranNo ratings yet

- Faqs NfuDocument16 pagesFaqs NfuhagdincloobleNo ratings yet

- Rules For Affiliation N.T.BDocument6 pagesRules For Affiliation N.T.BMuhammad SajidNo ratings yet

- A Hand Book of DDO'sDocument472 pagesA Hand Book of DDO'sRizwan HaiderNo ratings yet

- Power To Arrest For The Purposes of InvestigationDocument3 pagesPower To Arrest For The Purposes of InvestigationEsha HarizanNo ratings yet

- Surplus Rules 2002Document33 pagesSurplus Rules 2002adhityaNo ratings yet

- PSC Circular 52 - Graduate Trainee Scheme Policy in The Public Service PDFDocument9 pagesPSC Circular 52 - Graduate Trainee Scheme Policy in The Public Service PDFManoa Nagatalevu TupouNo ratings yet

- ParangalDocument34 pagesParangalMarc Benedict TalamayanNo ratings yet

- SOP Part 2Document267 pagesSOP Part 2Ajoydeep DasNo ratings yet

- Audit CodeDocument140 pagesAudit CodeKhurram SherazNo ratings yet

- Bofp 2022Document149 pagesBofp 2022ali shahNo ratings yet

- Project HR Practices in Wapda: Submitted To Riaz Toor Subject HR Course MBA - 2 (N) Submitted by Rana Faisal AliDocument50 pagesProject HR Practices in Wapda: Submitted To Riaz Toor Subject HR Course MBA - 2 (N) Submitted by Rana Faisal AliSyeda DilawaizNo ratings yet

- At A Glance - Annual-14Document131 pagesAt A Glance - Annual-14dvgtexNo ratings yet

- Student Pass Application Format 0 PDFDocument1 pageStudent Pass Application Format 0 PDFmanojnaNo ratings yet

- System of Financial Control & Budgeting 2006 (Updated October 2018)Document51 pagesSystem of Financial Control & Budgeting 2006 (Updated October 2018)usman ziaNo ratings yet

- MPFCV 1 CH 2Document10 pagesMPFCV 1 CH 2mahendra singhNo ratings yet

- Financial Code Reading Material Final (1)Document68 pagesFinancial Code Reading Material Final (1)sumedhNo ratings yet

- Applications - English GrammarDocument7 pagesApplications - English GrammarFayaz Khan100% (3)

- Minutes of 41 BoD Meeting PDFDocument27 pagesMinutes of 41 BoD Meeting PDFFayaz KhanNo ratings yet

- UntitledDocument10 pagesUntitledFayaz KhanNo ratings yet

- BS-20 Seniority List 01-01-2022Document7 pagesBS-20 Seniority List 01-01-2022Fayaz KhanNo ratings yet

- Advertisment of Driver ForwardingDocument1 pageAdvertisment of Driver ForwardingFayaz KhanNo ratings yet

- UntitledDocument7 pagesUntitledFayaz KhanNo ratings yet

- Advance para 113Document10 pagesAdvance para 113Fayaz KhanNo ratings yet

- BS-19 Seniority List 01 - 01 - 2022Document8 pagesBS-19 Seniority List 01 - 01 - 2022Fayaz KhanNo ratings yet

- Audit Note ChitralDocument23 pagesAudit Note ChitralFayaz KhanNo ratings yet

- Receipt Payment: Detail of Closing BalanceDocument2 pagesReceipt Payment: Detail of Closing BalanceFayaz KhanNo ratings yet

- Kahi DimolishDocument2 pagesKahi DimolishFayaz KhanNo ratings yet

- 2651 of CWDocument9 pages2651 of CWFayaz KhanNo ratings yet

- Phe Batagram Payroll 01-2021Document97 pagesPhe Batagram Payroll 01-2021Fayaz KhanNo ratings yet

- Demand For Fund Under ADP No. 516Document1 pageDemand For Fund Under ADP No. 516Fayaz KhanNo ratings yet

- GPF FinalpmtDocument4 pagesGPF FinalpmtFayaz KhanNo ratings yet

- GPF FinalpmtDocument4 pagesGPF FinalpmtFayaz KhanNo ratings yet

- Age CalculationDocument2 pagesAge CalculationFayaz KhanNo ratings yet

- IN Case OF Death: ApplicationDocument1 pageIN Case OF Death: ApplicationFayaz KhanNo ratings yet

- Pay BillDocument1 pagePay BillFayaz KhanNo ratings yet

- TG TG 9780195979688 2Document149 pagesTG TG 9780195979688 2Fayaz KhanNo ratings yet

- Zahid New CVDocument6 pagesZahid New CVzahid khanNo ratings yet

- Cook Vernice - AC 404 Accounting Info SystemDocument2 pagesCook Vernice - AC 404 Accounting Info SystemVernice LutoNo ratings yet

- A Industrial Visit Report On Diamond Beverages Pvt. LTD.: Diploma in Mechanical EngineeringDocument17 pagesA Industrial Visit Report On Diamond Beverages Pvt. LTD.: Diploma in Mechanical EngineeringAryan Kumar100% (1)

- Business Law Course Work 4 816020005Document9 pagesBusiness Law Course Work 4 816020005Christian SteeleNo ratings yet

- Audit Reviewer Sample 2Document13 pagesAudit Reviewer Sample 2ChinNo ratings yet

- Chapter 8Document17 pagesChapter 8Jamaica DavidNo ratings yet

- Real Estate Economics PDFDocument88 pagesReal Estate Economics PDFTekeba BirhaneNo ratings yet

- Purple White Bold Modern Digital Marketer CVDocument2 pagesPurple White Bold Modern Digital Marketer CVPurnima Swami (Lecturer & Promoter)No ratings yet

- Drywall Feasibility Study 1Document31 pagesDrywall Feasibility Study 1Firas AbsaNo ratings yet

- EStatement 2020 08 27 78283Document5 pagesEStatement 2020 08 27 78283abalaibemeNo ratings yet

- FJFJFJFJDocument12 pagesFJFJFJFJnuravcool76No ratings yet

- 3M India Limited - Annual Report 2015-16Document144 pages3M India Limited - Annual Report 2015-16Ishpreet singhNo ratings yet

- Ningbo L & M International Trading Co., LTDDocument1 pageNingbo L & M International Trading Co., LTDوليد سالمNo ratings yet

- Calculator New Pay ScaleDocument4 pagesCalculator New Pay Scalerocky_ecNo ratings yet

- Tizon vs. Valdez & Morales, 48 Phil 910Document3 pagesTizon vs. Valdez & Morales, 48 Phil 910Al Jay MejosNo ratings yet

- Tut - Week 3.v2Document16 pagesTut - Week 3.v2peter kongNo ratings yet

- Delivery Hero SE - Trading Update Q1 2024Document47 pagesDelivery Hero SE - Trading Update Q1 2024koteshchoudaryNo ratings yet

- AUSL Bar Operations 2017 LMT Property EditedDocument6 pagesAUSL Bar Operations 2017 LMT Property EditedEron Roi Centina-gacutanNo ratings yet

- 2016 Nomura Summer Internship ProgramDocument25 pages2016 Nomura Summer Internship ProgramTing-An KuoNo ratings yet

- 46793bosinter p8 Seca cp5 PDFDocument42 pages46793bosinter p8 Seca cp5 PDFIsavic AlsinaNo ratings yet

- Saving AcDocument5 pagesSaving AcRohit raagNo ratings yet

- Problems On Flexible BudgetDocument3 pagesProblems On Flexible BudgetsafwanhossainNo ratings yet

- Financial Model Template by SlidebeanDocument363 pagesFinancial Model Template by SlidebeanYargop AnalyticsNo ratings yet

- Test Bank For Macroeconomics 2nd Edition Full DownloadDocument48 pagesTest Bank For Macroeconomics 2nd Edition Full Downloadmichaelbirdgznspejbwa100% (22)

- Caf-8 Mindmaps-69Document19 pagesCaf-8 Mindmaps-69Muhammad ImranNo ratings yet

- Test Bank: Corporate RestructuringDocument3 pagesTest Bank: Corporate RestructuringYoukayzeeNo ratings yet