MA - Case Analysis - Group12

MA - Case Analysis - Group12

You might also like

- Ethics For Engineers by Martin Peterson Full ChapterDocument41 pagesEthics For Engineers by Martin Peterson Full Chapterashley.torres627100% (26)

- Cafes Monte BiancoDocument6 pagesCafes Monte Biancogulrukhhina38% (8)

- A1.2 Roic TreeDocument9 pagesA1.2 Roic TreemonemNo ratings yet

- Case 1 Spreadsheet - EI DuPontDocument6 pagesCase 1 Spreadsheet - EI DuPontSamuel BishopNo ratings yet

- Right To Travel or DriveDocument6 pagesRight To Travel or DriveShawn100% (10)

- Cafes Monte Bianco TableDocument2 pagesCafes Monte Bianco Tablemcg1350% (2)

- Cafes Monte Bianco MemoDocument4 pagesCafes Monte Bianco Memocatspajamas 1167% (6)

- This Spreadsheet Supports STUDENT Analysis of The Case "Bob's Baloney" (UVA-F-1942)Document4 pagesThis Spreadsheet Supports STUDENT Analysis of The Case "Bob's Baloney" (UVA-F-1942)LAWZ1017No ratings yet

- Group Assignment Cafes Monte Bianco Final V2Document13 pagesGroup Assignment Cafes Monte Bianco Final V2Linh Chi Trịnh T.No ratings yet

- Cafés Monte Bianco - Questions and Additional DataDocument1 pageCafés Monte Bianco - Questions and Additional DataMarco BolzonelloNo ratings yet

- Mystic SportsDocument34 pagesMystic SportshelloNo ratings yet

- "Case Analysis-Cafés Monte Blanco: Building A Profit Plan": Managerial AccountingDocument8 pages"Case Analysis-Cafés Monte Blanco: Building A Profit Plan": Managerial Accountingvipul tutejaNo ratings yet

- Cafes Monte Bianco Cash Flow HLC PDFDocument1 pageCafes Monte Bianco Cash Flow HLC PDFLuis CastroNo ratings yet

- Tire City Spreadsheet SolutionDocument7 pagesTire City Spreadsheet SolutionSyed Ali MurtuzaNo ratings yet

- Phuket Beach Case SolutionDocument8 pagesPhuket Beach Case SolutionGmitNo ratings yet

- Tire City-Spread SheetDocument6 pagesTire City-Spread SheetVibhusha SinghNo ratings yet

- Tire - City AnalysisDocument17 pagesTire - City AnalysisJustin HoNo ratings yet

- Toy World Case ExhibitsDocument24 pagesToy World Case ExhibitsFrancisco Aguilar PuyolNo ratings yet

- Horizontal Analysis: Grace Corporation Comparative Profit and Loss Statement For The Years Ended March 31, 19X2 and 19X1Document6 pagesHorizontal Analysis: Grace Corporation Comparative Profit and Loss Statement For The Years Ended March 31, 19X2 and 19X1rachit2383No ratings yet

- Ameritrade Case SolutionDocument39 pagesAmeritrade Case SolutionShivani KarkeraNo ratings yet

- Clarkson Lumber Case AnalysisDocument7 pagesClarkson Lumber Case Analysispawangadiya1210No ratings yet

- Erie Steel Case Presentation: Decision Making With AnalyticsDocument4 pagesErie Steel Case Presentation: Decision Making With AnalyticsFiyinfoluwa OyewoNo ratings yet

- Hampton Machine Tool CompanyDocument6 pagesHampton Machine Tool CompanyClaudia Torres50% (2)

- 148 The Ultimate Guide To Off Page SEO PDFDocument6 pages148 The Ultimate Guide To Off Page SEO PDFTanisha AgarwalNo ratings yet

- 323-1211-090 About The TN-16X Documentation Suite R5Document82 pages323-1211-090 About The TN-16X Documentation Suite R5Trilha Do Rock100% (2)

- Determining The Ratio of Specific Heats of Slash Slash Gases Using Adiabatic OscillationsDocument9 pagesDetermining The Ratio of Specific Heats of Slash Slash Gases Using Adiabatic OscillationsEralyn DorolNo ratings yet

- ShakeDocument4 pagesShakesafak100% (3)

- Cafe Monte BiancoDocument21 pagesCafe Monte BiancoWilliam Torrez OrozcoNo ratings yet

- Cafés Monte Blanco: Building A Profit PlanDocument11 pagesCafés Monte Blanco: Building A Profit Planvipul tutejaNo ratings yet

- Cafes Monte Biance Sol SelfDocument2 pagesCafes Monte Biance Sol SelfahsanzmNo ratings yet

- Monte BiancoDocument10 pagesMonte BiancoJeanine Benjamin100% (4)

- Material Complementario - Cafes Monte BiancoDocument20 pagesMaterial Complementario - Cafes Monte BiancoGlenda ChiquilloNo ratings yet

- MonteBianco-Solution - With Comments and AlternativesDocument27 pagesMonteBianco-Solution - With Comments and AlternativesGiudittaBiancaLuràNo ratings yet

- Hassan Tariq Ghani Syed Saad Shah Syed Muhammad Hamza Syed Ather Waqar Syed Fayyaz Hasnain Case Presentation - Accounting For Decision MakingDocument21 pagesHassan Tariq Ghani Syed Saad Shah Syed Muhammad Hamza Syed Ather Waqar Syed Fayyaz Hasnain Case Presentation - Accounting For Decision Makingchacha_420100% (2)

- Tire City Case AnalysisDocument10 pagesTire City Case AnalysisVASANTADA SRIKANTH (PGP 2016-18)No ratings yet

- Tire City AssignmentDocument6 pagesTire City AssignmentderronsNo ratings yet

- XLS915-XLS-ENG DesarrolladoDocument10 pagesXLS915-XLS-ENG DesarrolladoYessu Amhed Condori RavichaguaNo ratings yet

- Otago's MuseumDocument5 pagesOtago's Museumyecika50% (2)

- Tire City AssignmentDocument6 pagesTire City AssignmentXRiloXNo ratings yet

- Polar Sports X Ls StudentDocument9 pagesPolar Sports X Ls StudentBilal Ahmed Shaikh0% (1)

- The Home Depot: QuestionsDocument13 pagesThe Home Depot: Questions凱爾思No ratings yet

- 1233 NeheteKushal BAV Assignment1Document12 pages1233 NeheteKushal BAV Assignment1Anjali BhatiaNo ratings yet

- New Heritage DoolDocument9 pagesNew Heritage DoolVidya Sagar KonaNo ratings yet

- Butler Lumber CoDocument2 pagesButler Lumber Cokumarsharma123No ratings yet

- JHT Case ExcelDocument4 pagesJHT Case Excelanup akasheNo ratings yet

- Chemalite Cash Flow StatementDocument2 pagesChemalite Cash Flow Statementrishika rshNo ratings yet

- World Wide Paper CompanyDocument2 pagesWorld Wide Paper CompanyAshwinKumarNo ratings yet

- Sampa Video Case ExhibitsDocument1 pageSampa Video Case ExhibitsOnal RautNo ratings yet

- Evaluacion Salud FinancieraDocument17 pagesEvaluacion Salud FinancieraWilliam VicuñaNo ratings yet

- Lady M Exercises-3Document6 pagesLady M Exercises-3MOHIT MARHATTANo ratings yet

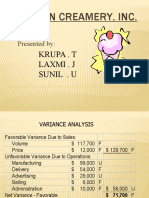

- Boston Creamery CaseDocument9 pagesBoston Creamery Caselion_heart3001100% (1)

- Manac Asn3 Software AssociatesDocument6 pagesManac Asn3 Software AssociatesNikhil JindalNo ratings yet

- Seagate NewDocument22 pagesSeagate NewKaran VasheeNo ratings yet

- Air Thread Excel FileDocument7 pagesAir Thread Excel FileAlex Wilson0% (1)

- Cash Flow Excercise Questions-Set-2Document2 pagesCash Flow Excercise Questions-Set-2AgANo ratings yet

- Otago MuseumDocument19 pagesOtago MuseumFoamdomeNo ratings yet

- Dokumen - Tips - Cafe Monte BiancoDocument21 pagesDokumen - Tips - Cafe Monte Biancobboit031No ratings yet

- Just Group Research Report 05.15.21 - v2Document4 pagesJust Group Research Report 05.15.21 - v2Ralph SuarezNo ratings yet

- Brief Overview of I2Document7 pagesBrief Overview of I2api-3716851No ratings yet

- Module 3 Exercises 1. Pro Forma Income Statements: Scenario AnalysisDocument7 pagesModule 3 Exercises 1. Pro Forma Income Statements: Scenario AnalysisJARED DARREN ONGNo ratings yet

- 3.5 ExercisesDocument13 pages3.5 ExercisesGeorgios MilitsisNo ratings yet

- Mercury QuestionsDocument6 pagesMercury Questionsapi-239586293No ratings yet

- Accounting For Manager - Module 9Document7 pagesAccounting For Manager - Module 9Godz gAMERNo ratings yet

- Bsbfim601 FNDocument19 pagesBsbfim601 FNKitpipoj PornnongsaenNo ratings yet

- Q4 FY 10 Investor UpdateDocument5 pagesQ4 FY 10 Investor UpdateshahvinNo ratings yet

- Finance Assignment 1Document7 pagesFinance Assignment 1Nienke OzingaNo ratings yet

- Module 2 - SEVEN Elements of Principled Negotiation PDFDocument7 pagesModule 2 - SEVEN Elements of Principled Negotiation PDFTanisha AgarwalNo ratings yet

- Consumer Behaviours ModelsDocument3 pagesConsumer Behaviours ModelsTanisha AgarwalNo ratings yet

- Key Influence Factors For Ocean Freight Forwarders Selecting Container Shipping Lines Using The Revised Dematel ApproachDocument12 pagesKey Influence Factors For Ocean Freight Forwarders Selecting Container Shipping Lines Using The Revised Dematel ApproachTanisha AgarwalNo ratings yet

- Consumer Behaviours Towards Online Buying NotesDocument2 pagesConsumer Behaviours Towards Online Buying NotesTanisha AgarwalNo ratings yet

- AbhsjDocument1 pageAbhsjTanisha Agarwal100% (1)

- Social Media Marketing: WebsiteDocument10 pagesSocial Media Marketing: WebsiteTanisha AgarwalNo ratings yet

- Social Media Marketing: Opportunities and Challenges: April 2019Document13 pagesSocial Media Marketing: Opportunities and Challenges: April 2019Tanisha AgarwalNo ratings yet

- Functions of Attitudes: Attitude NotesDocument2 pagesFunctions of Attitudes: Attitude NotesTanisha AgarwalNo ratings yet

- Off Page SEO and Link Building General S PDFDocument13 pagesOff Page SEO and Link Building General S PDFTanisha AgarwalNo ratings yet

- Web Analytics - MetricsDocument87 pagesWeb Analytics - MetricsTanisha AgarwalNo ratings yet

- International News ChinsDocument1 pageInternational News ChinsTanisha AgarwalNo ratings yet

- Retail Store ManagementDocument11 pagesRetail Store ManagementTanisha AgarwalNo ratings yet

- Queen of Cold CallingDocument2 pagesQueen of Cold CallingTanisha AgarwalNo ratings yet

- Individual Mid Term Review SEODocument2 pagesIndividual Mid Term Review SEOTanisha AgarwalNo ratings yet

- 2019 Annual Report PDFDocument181 pages2019 Annual Report PDFTanisha AgarwalNo ratings yet

- Individual Performance EvaluationDocument2 pagesIndividual Performance EvaluationTanisha AgarwalNo ratings yet

- TA Tax AnalysisDocument10 pagesTA Tax AnalysisTanisha AgarwalNo ratings yet

- Freight Calculation - FCL - SolutionDocument4 pagesFreight Calculation - FCL - SolutionTanisha AgarwalNo ratings yet

- Business and Economic EnvironmentDocument6 pagesBusiness and Economic EnvironmentTanisha AgarwalNo ratings yet

- BA 503-Financial AnalyticsDocument8 pagesBA 503-Financial AnalyticsTanisha AgarwalNo ratings yet

- Demand and Supply StudyDocument13 pagesDemand and Supply StudyTanisha AgarwalNo ratings yet

- HUL's Net Sales Rise by 7% in First Quarter - The Economic TimesDocument1 pageHUL's Net Sales Rise by 7% in First Quarter - The Economic TimesTanisha AgarwalNo ratings yet

- ABC Builders - LookupDocument2 pagesABC Builders - LookupTanisha AgarwalNo ratings yet

- BA 501-Text AnalyticsDocument2 pagesBA 501-Text AnalyticsTanisha AgarwalNo ratings yet

- DLL MAPEH7 - 3rd QuarterDocument69 pagesDLL MAPEH7 - 3rd QuarterArah May RobosaNo ratings yet

- Ic 2003Document21 pagesIc 2003Dinesh KumarNo ratings yet

- Mi-171A1 RFM Part-IDocument310 pagesMi-171A1 RFM Part-IJulio Mello50% (2)

- Seismic Upgrade of Existing Buildings With Fluid Viscous Dampers: Design Methodologies and Case StudyDocument12 pagesSeismic Upgrade of Existing Buildings With Fluid Viscous Dampers: Design Methodologies and Case StudyHimanshu WasterNo ratings yet

- Homework Practice OnlineDocument6 pagesHomework Practice Onlineh681x9gn100% (1)

- Paramout 446Document13 pagesParamout 446Srtç TyNo ratings yet

- Show All Work For Credit. Leave All Answers As Simplified FractionsDocument10 pagesShow All Work For Credit. Leave All Answers As Simplified FractionsAliRazaNo ratings yet

- Bla BlaDocument8 pagesBla BladharwinNo ratings yet

- Essay On Ratan Tata ...Document3 pagesEssay On Ratan Tata ...GAURAV JAINNo ratings yet

- Prism ExperimentDocument31 pagesPrism ExperimentFred100% (1)

- Onion AgmarkDocument33 pagesOnion Agmarkseeralan balakrishnanNo ratings yet

- Trading PlanDocument12 pagesTrading Planpeterhash5No ratings yet

- TPFEPL Company BrochureDocument18 pagesTPFEPL Company BrochurepadeepNo ratings yet

- Luyện tập ĐỌCDocument5 pagesLuyện tập ĐỌCvuhai110394No ratings yet

- Demand For Documents, Citing ContemptDocument53 pagesDemand For Documents, Citing ContemptJoel Banner BairdNo ratings yet

- Preferences Environment Variables Reference PLM TeamcenterDocument1,157 pagesPreferences Environment Variables Reference PLM TeamcenterBHUVANA SATEESHNo ratings yet

- Solution Manual Advanced Financial Accounting 8th Edition Baker Chap007 PDFDocument77 pagesSolution Manual Advanced Financial Accounting 8th Edition Baker Chap007 PDFYopie ChandraNo ratings yet

- EL - 124 Electronic Devices & Circuits: Experiment # 04Document6 pagesEL - 124 Electronic Devices & Circuits: Experiment # 04Jawwad IqbalNo ratings yet

- CNS - Module 2.1-AESDocument17 pagesCNS - Module 2.1-AESNIKSHITH SHETTYNo ratings yet

- Industrial Internship ReportDocument62 pagesIndustrial Internship ReportHairi MurNo ratings yet

- Set de Instrucciones HC12Document32 pagesSet de Instrucciones HC12carlosNo ratings yet

- Daily Coal Inventory 211220 PDFDocument1 pageDaily Coal Inventory 211220 PDFDedi SetyawanNo ratings yet

- Ray Optics_04-06-24Document13 pagesRay Optics_04-06-24cbajpai29No ratings yet

- SP Brief Description1Document12 pagesSP Brief Description1Creative MindsNo ratings yet

- Q3 Assessment Wk3&4Document3 pagesQ3 Assessment Wk3&4Jaybie TejadaNo ratings yet

Download as docx, pdf, or txt

You might also like

- Ethics For Engineers by Martin Peterson Full ChapterDocument41 pagesEthics For Engineers by Martin Peterson Full Chapterashley.torres627100% (26)

- Cafes Monte BiancoDocument6 pagesCafes Monte Biancogulrukhhina38% (8)

- A1.2 Roic TreeDocument9 pagesA1.2 Roic TreemonemNo ratings yet

- Case 1 Spreadsheet - EI DuPontDocument6 pagesCase 1 Spreadsheet - EI DuPontSamuel BishopNo ratings yet

- Right To Travel or DriveDocument6 pagesRight To Travel or DriveShawn100% (10)

- Cafes Monte Bianco TableDocument2 pagesCafes Monte Bianco Tablemcg1350% (2)

- Cafes Monte Bianco MemoDocument4 pagesCafes Monte Bianco Memocatspajamas 1167% (6)

- This Spreadsheet Supports STUDENT Analysis of The Case "Bob's Baloney" (UVA-F-1942)Document4 pagesThis Spreadsheet Supports STUDENT Analysis of The Case "Bob's Baloney" (UVA-F-1942)LAWZ1017No ratings yet

- Group Assignment Cafes Monte Bianco Final V2Document13 pagesGroup Assignment Cafes Monte Bianco Final V2Linh Chi Trịnh T.No ratings yet

- Cafés Monte Bianco - Questions and Additional DataDocument1 pageCafés Monte Bianco - Questions and Additional DataMarco BolzonelloNo ratings yet

- Mystic SportsDocument34 pagesMystic SportshelloNo ratings yet

- "Case Analysis-Cafés Monte Blanco: Building A Profit Plan": Managerial AccountingDocument8 pages"Case Analysis-Cafés Monte Blanco: Building A Profit Plan": Managerial Accountingvipul tutejaNo ratings yet

- Cafes Monte Bianco Cash Flow HLC PDFDocument1 pageCafes Monte Bianco Cash Flow HLC PDFLuis CastroNo ratings yet

- Tire City Spreadsheet SolutionDocument7 pagesTire City Spreadsheet SolutionSyed Ali MurtuzaNo ratings yet

- Phuket Beach Case SolutionDocument8 pagesPhuket Beach Case SolutionGmitNo ratings yet

- Tire City-Spread SheetDocument6 pagesTire City-Spread SheetVibhusha SinghNo ratings yet

- Tire - City AnalysisDocument17 pagesTire - City AnalysisJustin HoNo ratings yet

- Toy World Case ExhibitsDocument24 pagesToy World Case ExhibitsFrancisco Aguilar PuyolNo ratings yet

- Horizontal Analysis: Grace Corporation Comparative Profit and Loss Statement For The Years Ended March 31, 19X2 and 19X1Document6 pagesHorizontal Analysis: Grace Corporation Comparative Profit and Loss Statement For The Years Ended March 31, 19X2 and 19X1rachit2383No ratings yet

- Ameritrade Case SolutionDocument39 pagesAmeritrade Case SolutionShivani KarkeraNo ratings yet

- Clarkson Lumber Case AnalysisDocument7 pagesClarkson Lumber Case Analysispawangadiya1210No ratings yet

- Erie Steel Case Presentation: Decision Making With AnalyticsDocument4 pagesErie Steel Case Presentation: Decision Making With AnalyticsFiyinfoluwa OyewoNo ratings yet

- Hampton Machine Tool CompanyDocument6 pagesHampton Machine Tool CompanyClaudia Torres50% (2)

- 148 The Ultimate Guide To Off Page SEO PDFDocument6 pages148 The Ultimate Guide To Off Page SEO PDFTanisha AgarwalNo ratings yet

- 323-1211-090 About The TN-16X Documentation Suite R5Document82 pages323-1211-090 About The TN-16X Documentation Suite R5Trilha Do Rock100% (2)

- Determining The Ratio of Specific Heats of Slash Slash Gases Using Adiabatic OscillationsDocument9 pagesDetermining The Ratio of Specific Heats of Slash Slash Gases Using Adiabatic OscillationsEralyn DorolNo ratings yet

- ShakeDocument4 pagesShakesafak100% (3)

- Cafe Monte BiancoDocument21 pagesCafe Monte BiancoWilliam Torrez OrozcoNo ratings yet

- Cafés Monte Blanco: Building A Profit PlanDocument11 pagesCafés Monte Blanco: Building A Profit Planvipul tutejaNo ratings yet

- Cafes Monte Biance Sol SelfDocument2 pagesCafes Monte Biance Sol SelfahsanzmNo ratings yet

- Monte BiancoDocument10 pagesMonte BiancoJeanine Benjamin100% (4)

- Material Complementario - Cafes Monte BiancoDocument20 pagesMaterial Complementario - Cafes Monte BiancoGlenda ChiquilloNo ratings yet

- MonteBianco-Solution - With Comments and AlternativesDocument27 pagesMonteBianco-Solution - With Comments and AlternativesGiudittaBiancaLuràNo ratings yet

- Hassan Tariq Ghani Syed Saad Shah Syed Muhammad Hamza Syed Ather Waqar Syed Fayyaz Hasnain Case Presentation - Accounting For Decision MakingDocument21 pagesHassan Tariq Ghani Syed Saad Shah Syed Muhammad Hamza Syed Ather Waqar Syed Fayyaz Hasnain Case Presentation - Accounting For Decision Makingchacha_420100% (2)

- Tire City Case AnalysisDocument10 pagesTire City Case AnalysisVASANTADA SRIKANTH (PGP 2016-18)No ratings yet

- Tire City AssignmentDocument6 pagesTire City AssignmentderronsNo ratings yet

- XLS915-XLS-ENG DesarrolladoDocument10 pagesXLS915-XLS-ENG DesarrolladoYessu Amhed Condori RavichaguaNo ratings yet

- Otago's MuseumDocument5 pagesOtago's Museumyecika50% (2)

- Tire City AssignmentDocument6 pagesTire City AssignmentXRiloXNo ratings yet

- Polar Sports X Ls StudentDocument9 pagesPolar Sports X Ls StudentBilal Ahmed Shaikh0% (1)

- The Home Depot: QuestionsDocument13 pagesThe Home Depot: Questions凱爾思No ratings yet

- 1233 NeheteKushal BAV Assignment1Document12 pages1233 NeheteKushal BAV Assignment1Anjali BhatiaNo ratings yet

- New Heritage DoolDocument9 pagesNew Heritage DoolVidya Sagar KonaNo ratings yet

- Butler Lumber CoDocument2 pagesButler Lumber Cokumarsharma123No ratings yet

- JHT Case ExcelDocument4 pagesJHT Case Excelanup akasheNo ratings yet

- Chemalite Cash Flow StatementDocument2 pagesChemalite Cash Flow Statementrishika rshNo ratings yet

- World Wide Paper CompanyDocument2 pagesWorld Wide Paper CompanyAshwinKumarNo ratings yet

- Sampa Video Case ExhibitsDocument1 pageSampa Video Case ExhibitsOnal RautNo ratings yet

- Evaluacion Salud FinancieraDocument17 pagesEvaluacion Salud FinancieraWilliam VicuñaNo ratings yet

- Lady M Exercises-3Document6 pagesLady M Exercises-3MOHIT MARHATTANo ratings yet

- Boston Creamery CaseDocument9 pagesBoston Creamery Caselion_heart3001100% (1)

- Manac Asn3 Software AssociatesDocument6 pagesManac Asn3 Software AssociatesNikhil JindalNo ratings yet

- Seagate NewDocument22 pagesSeagate NewKaran VasheeNo ratings yet

- Air Thread Excel FileDocument7 pagesAir Thread Excel FileAlex Wilson0% (1)

- Cash Flow Excercise Questions-Set-2Document2 pagesCash Flow Excercise Questions-Set-2AgANo ratings yet

- Otago MuseumDocument19 pagesOtago MuseumFoamdomeNo ratings yet

- Dokumen - Tips - Cafe Monte BiancoDocument21 pagesDokumen - Tips - Cafe Monte Biancobboit031No ratings yet

- Just Group Research Report 05.15.21 - v2Document4 pagesJust Group Research Report 05.15.21 - v2Ralph SuarezNo ratings yet

- Brief Overview of I2Document7 pagesBrief Overview of I2api-3716851No ratings yet

- Module 3 Exercises 1. Pro Forma Income Statements: Scenario AnalysisDocument7 pagesModule 3 Exercises 1. Pro Forma Income Statements: Scenario AnalysisJARED DARREN ONGNo ratings yet

- 3.5 ExercisesDocument13 pages3.5 ExercisesGeorgios MilitsisNo ratings yet

- Mercury QuestionsDocument6 pagesMercury Questionsapi-239586293No ratings yet

- Accounting For Manager - Module 9Document7 pagesAccounting For Manager - Module 9Godz gAMERNo ratings yet

- Bsbfim601 FNDocument19 pagesBsbfim601 FNKitpipoj PornnongsaenNo ratings yet

- Q4 FY 10 Investor UpdateDocument5 pagesQ4 FY 10 Investor UpdateshahvinNo ratings yet

- Finance Assignment 1Document7 pagesFinance Assignment 1Nienke OzingaNo ratings yet

- Module 2 - SEVEN Elements of Principled Negotiation PDFDocument7 pagesModule 2 - SEVEN Elements of Principled Negotiation PDFTanisha AgarwalNo ratings yet

- Consumer Behaviours ModelsDocument3 pagesConsumer Behaviours ModelsTanisha AgarwalNo ratings yet

- Key Influence Factors For Ocean Freight Forwarders Selecting Container Shipping Lines Using The Revised Dematel ApproachDocument12 pagesKey Influence Factors For Ocean Freight Forwarders Selecting Container Shipping Lines Using The Revised Dematel ApproachTanisha AgarwalNo ratings yet

- Consumer Behaviours Towards Online Buying NotesDocument2 pagesConsumer Behaviours Towards Online Buying NotesTanisha AgarwalNo ratings yet

- AbhsjDocument1 pageAbhsjTanisha Agarwal100% (1)

- Social Media Marketing: WebsiteDocument10 pagesSocial Media Marketing: WebsiteTanisha AgarwalNo ratings yet

- Social Media Marketing: Opportunities and Challenges: April 2019Document13 pagesSocial Media Marketing: Opportunities and Challenges: April 2019Tanisha AgarwalNo ratings yet

- Functions of Attitudes: Attitude NotesDocument2 pagesFunctions of Attitudes: Attitude NotesTanisha AgarwalNo ratings yet

- Off Page SEO and Link Building General S PDFDocument13 pagesOff Page SEO and Link Building General S PDFTanisha AgarwalNo ratings yet

- Web Analytics - MetricsDocument87 pagesWeb Analytics - MetricsTanisha AgarwalNo ratings yet

- International News ChinsDocument1 pageInternational News ChinsTanisha AgarwalNo ratings yet

- Retail Store ManagementDocument11 pagesRetail Store ManagementTanisha AgarwalNo ratings yet

- Queen of Cold CallingDocument2 pagesQueen of Cold CallingTanisha AgarwalNo ratings yet

- Individual Mid Term Review SEODocument2 pagesIndividual Mid Term Review SEOTanisha AgarwalNo ratings yet

- 2019 Annual Report PDFDocument181 pages2019 Annual Report PDFTanisha AgarwalNo ratings yet

- Individual Performance EvaluationDocument2 pagesIndividual Performance EvaluationTanisha AgarwalNo ratings yet

- TA Tax AnalysisDocument10 pagesTA Tax AnalysisTanisha AgarwalNo ratings yet

- Freight Calculation - FCL - SolutionDocument4 pagesFreight Calculation - FCL - SolutionTanisha AgarwalNo ratings yet

- Business and Economic EnvironmentDocument6 pagesBusiness and Economic EnvironmentTanisha AgarwalNo ratings yet

- BA 503-Financial AnalyticsDocument8 pagesBA 503-Financial AnalyticsTanisha AgarwalNo ratings yet

- Demand and Supply StudyDocument13 pagesDemand and Supply StudyTanisha AgarwalNo ratings yet

- HUL's Net Sales Rise by 7% in First Quarter - The Economic TimesDocument1 pageHUL's Net Sales Rise by 7% in First Quarter - The Economic TimesTanisha AgarwalNo ratings yet

- ABC Builders - LookupDocument2 pagesABC Builders - LookupTanisha AgarwalNo ratings yet

- BA 501-Text AnalyticsDocument2 pagesBA 501-Text AnalyticsTanisha AgarwalNo ratings yet

- DLL MAPEH7 - 3rd QuarterDocument69 pagesDLL MAPEH7 - 3rd QuarterArah May RobosaNo ratings yet

- Ic 2003Document21 pagesIc 2003Dinesh KumarNo ratings yet

- Mi-171A1 RFM Part-IDocument310 pagesMi-171A1 RFM Part-IJulio Mello50% (2)

- Seismic Upgrade of Existing Buildings With Fluid Viscous Dampers: Design Methodologies and Case StudyDocument12 pagesSeismic Upgrade of Existing Buildings With Fluid Viscous Dampers: Design Methodologies and Case StudyHimanshu WasterNo ratings yet

- Homework Practice OnlineDocument6 pagesHomework Practice Onlineh681x9gn100% (1)

- Paramout 446Document13 pagesParamout 446Srtç TyNo ratings yet

- Show All Work For Credit. Leave All Answers As Simplified FractionsDocument10 pagesShow All Work For Credit. Leave All Answers As Simplified FractionsAliRazaNo ratings yet

- Bla BlaDocument8 pagesBla BladharwinNo ratings yet

- Essay On Ratan Tata ...Document3 pagesEssay On Ratan Tata ...GAURAV JAINNo ratings yet

- Prism ExperimentDocument31 pagesPrism ExperimentFred100% (1)

- Onion AgmarkDocument33 pagesOnion Agmarkseeralan balakrishnanNo ratings yet

- Trading PlanDocument12 pagesTrading Planpeterhash5No ratings yet

- TPFEPL Company BrochureDocument18 pagesTPFEPL Company BrochurepadeepNo ratings yet

- Luyện tập ĐỌCDocument5 pagesLuyện tập ĐỌCvuhai110394No ratings yet

- Demand For Documents, Citing ContemptDocument53 pagesDemand For Documents, Citing ContemptJoel Banner BairdNo ratings yet

- Preferences Environment Variables Reference PLM TeamcenterDocument1,157 pagesPreferences Environment Variables Reference PLM TeamcenterBHUVANA SATEESHNo ratings yet

- Solution Manual Advanced Financial Accounting 8th Edition Baker Chap007 PDFDocument77 pagesSolution Manual Advanced Financial Accounting 8th Edition Baker Chap007 PDFYopie ChandraNo ratings yet

- EL - 124 Electronic Devices & Circuits: Experiment # 04Document6 pagesEL - 124 Electronic Devices & Circuits: Experiment # 04Jawwad IqbalNo ratings yet

- CNS - Module 2.1-AESDocument17 pagesCNS - Module 2.1-AESNIKSHITH SHETTYNo ratings yet

- Industrial Internship ReportDocument62 pagesIndustrial Internship ReportHairi MurNo ratings yet

- Set de Instrucciones HC12Document32 pagesSet de Instrucciones HC12carlosNo ratings yet

- Daily Coal Inventory 211220 PDFDocument1 pageDaily Coal Inventory 211220 PDFDedi SetyawanNo ratings yet

- Ray Optics_04-06-24Document13 pagesRay Optics_04-06-24cbajpai29No ratings yet

- SP Brief Description1Document12 pagesSP Brief Description1Creative MindsNo ratings yet

- Q3 Assessment Wk3&4Document3 pagesQ3 Assessment Wk3&4Jaybie TejadaNo ratings yet