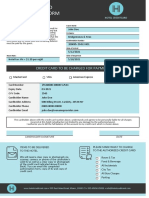

Debit Card and Credit Card

Debit Card and Credit Card

You might also like

- Credit Card Authorization Form Sra. LIDIA S. 2023-FIRMA PDFDocument1 pageCredit Card Authorization Form Sra. LIDIA S. 2023-FIRMA PDFAna Velasqz100% (1)

- Test Card CreditDocument32 pagesTest Card CreditHerard Gravi100% (4)

- 1050 Credit Card LabDocument8 pages1050 Credit Card Labapi-287131007No ratings yet

- Credit Card Number Generator & ValidatorDocument2 pagesCredit Card Number Generator & ValidatorMacho100% (2)

- CitikeyDocument54 pagesCitikeyJacob PochinNo ratings yet

- Ant Financial Case StudyDocument42 pagesAnt Financial Case StudytungfptNo ratings yet

- Credit Card Generator: Plagiarism Checker DA Checker Paraphrasing Tool Guest Post Service Premium Plans Register LoginDocument7 pagesCredit Card Generator: Plagiarism Checker DA Checker Paraphrasing Tool Guest Post Service Premium Plans Register Logingel gel60% (5)

- Bulk Credit Card DetailsDocument1 pageBulk Credit Card Detailsja100% (3)

- CC Strip ExplainedDocument11 pagesCC Strip ExplainedBlakeNo ratings yet

- Debit CardDocument22 pagesDebit CardDivya GoelNo ratings yet

- Hotel Credit Card Authorization Form 01Document2 pagesHotel Credit Card Authorization Form 01Liza wong100% (1)

- Employee Credit Card Authorization FormDocument2 pagesEmployee Credit Card Authorization FormLiza wongNo ratings yet

- How Hackers Hack Credit Cards or Debit Cards Password OnlineDocument9 pagesHow Hackers Hack Credit Cards or Debit Cards Password OnlineWalsy Sissoko100% (1)

- Debit Cards - All You Need To KnowDocument48 pagesDebit Cards - All You Need To KnowDavid Ramirez100% (1)

- Biometrics in Credit Cards: AnewwaytopayDocument31 pagesBiometrics in Credit Cards: AnewwaytopayRam Prasad Reddy SadiNo ratings yet

- Credit CardDocument100 pagesCredit CardSonia DuttNo ratings yet

- BinDocument3 pagesBincarlos50% (2)

- Credit CardDocument32 pagesCredit CardMasih Saab100% (2)

- How To Hack Websites, Passwords, Everything Step by STDocument3 pagesHow To Hack Websites, Passwords, Everything Step by STVivex2k1967% (9)

- Statistics Skittles ProjectDocument7 pagesStatistics Skittles Projectapi-302339334No ratings yet

- Beer GameDocument8 pagesBeer Gamelay fengNo ratings yet

- Domain Certifications Credit CardsDocument65 pagesDomain Certifications Credit Cardspratham_greatNo ratings yet

- Debit Cards & Credit CardsDocument28 pagesDebit Cards & Credit CardsullasNo ratings yet

- Process Credit Card AuthorizationDocument2 pagesProcess Credit Card AuthorizationJian GabatNo ratings yet

- Achieve Instant Approval and Issuance of Credit Cards Using Bizagi - NividousDocument1 pageAchieve Instant Approval and Issuance of Credit Cards Using Bizagi - NividousNividousNo ratings yet

- Safari - Oct 13, 2020 at 6:15 PMDocument1 pageSafari - Oct 13, 2020 at 6:15 PMJaboris JohnNo ratings yet

- HDFC Bank Credit Card Customer Care Number - 24x7Document5 pagesHDFC Bank Credit Card Customer Care Number - 24x7Baswamy CseNo ratings yet

- 6 Credit CardsDocument77 pages6 Credit CardsKartik BhartiaNo ratings yet

- Mitc For Amazon Pay Credit CardDocument7 pagesMitc For Amazon Pay Credit CardBlain Santhosh FernandesNo ratings yet

- Credit Card PDFDocument7 pagesCredit Card PDFhmsonawane100% (1)

- Credit CardsDocument10 pagesCredit CardsMadhur GuptaNo ratings yet

- Credit Card FraudsDocument63 pagesCredit Card FraudsAnaghaPuranikNo ratings yet

- Credit Cards: Personal FinanceDocument36 pagesCredit Cards: Personal FinanceAmara MaduagwuNo ratings yet

- Credit Card Management Information SysteDocument9 pagesCredit Card Management Information SysteAnant JainNo ratings yet

- Payments in Order Management in R12 (Doc ID 1164613.1) : Applies ToDocument33 pagesPayments in Order Management in R12 (Doc ID 1164613.1) : Applies ToManoj100% (1)

- Credit Card HackingDocument2 pagesCredit Card Hackingmadarauchiha50% (2)

- Supervisory Policy Manual: CR-S-5 Credit Card BusinessDocument43 pagesSupervisory Policy Manual: CR-S-5 Credit Card BusinessccnmiNo ratings yet

- Buy Now Pay Later BNPLOn Your Credit CardDocument26 pagesBuy Now Pay Later BNPLOn Your Credit CardShivaniNo ratings yet

- Credit CardDocument65 pagesCredit CardKrishana ThakurNo ratings yet

- Credit Card Processing GlossaryDocument14 pagesCredit Card Processing Glossarykintirgum100% (1)

- e BankingDocument61 pagese BankingRiSHI KeSH GawaINo ratings yet

- Credit Card Verification Procedures - V2Document8 pagesCredit Card Verification Procedures - V2Yess GuzmánNo ratings yet

- Credit Card ClientsDocument943 pagesCredit Card ClientsMamadou SowNo ratings yet

- Debit Card - Project Wark PDFDocument158 pagesDebit Card - Project Wark PDFManisha GuptaNo ratings yet

- Credit CardsDocument22 pagesCredit CardsEti Prince BajajNo ratings yet

- TransFirst - Merchant - Card Processing - Operating - Guide - v6-0915Document139 pagesTransFirst - Merchant - Card Processing - Operating - Guide - v6-0915sreejaNo ratings yet

- Corporation Bank Credit CardsDocument7 pagesCorporation Bank Credit CardsSuriya KJ100% (1)

- Cards: March XX, 2010Document57 pagesCards: March XX, 2010Keerti MannanNo ratings yet

- Vanilla Visa Gift Card BalanceDocument1 pageVanilla Visa Gift Card BalanceSamridhi Rai0% (1)

- Credit CardDocument6 pagesCredit Cardvj1414100% (1)

- WL WLDocument3 pagesWL WLsoumya pattanaikNo ratings yet

- BD Gold Visa Mastercard Credit Card v1Document14 pagesBD Gold Visa Mastercard Credit Card v1sajjad147No ratings yet

- Ideposit Merchant ApplicationDocument4 pagesIdeposit Merchant Applicationcris4455No ratings yet

- Credit Card Industry in IndiaDocument28 pagesCredit Card Industry in IndiaAk SahNo ratings yet

- How To Cash Out From Stolen Credit CardsDocument1 pageHow To Cash Out From Stolen Credit Cardsjohn100% (1)

- Bank Account Name & NumberDocument20 pagesBank Account Name & NumberNayeem AhmedNo ratings yet

- Credit CardDocument51 pagesCredit CardSmita JainNo ratings yet

- How Credit Cards Work: A Bit of HistoryDocument18 pagesHow Credit Cards Work: A Bit of HistoryVishal Kumar ShawNo ratings yet

- Visa HackDocument2 pagesVisa Hackheadpnc75% (4)

- Credit CardDocument77 pagesCredit CardSamuel DavisNo ratings yet

- Debit Card Info PDFDocument18 pagesDebit Card Info PDFjack meoffNo ratings yet

- RTG CPRed Jumpstart HSGCharsDocument6 pagesRTG CPRed Jumpstart HSGCharsOrlando SaallNo ratings yet

- BUS 201 Midterm Answer (19104022, Sec 7)Document7 pagesBUS 201 Midterm Answer (19104022, Sec 7)Redwan Afrid AvinNo ratings yet

- MaxLife Fraud AwarenessDocument1 pageMaxLife Fraud Awarenessbhavnapal74No ratings yet

- High Power CommitteeDocument39 pagesHigh Power CommitteeJaya PrabhaNo ratings yet

- Ora Linux InstallationDocument2 pagesOra Linux InstallationhenpuneNo ratings yet

- JCB Oil, JCB Genuine OilDocument2 pagesJCB Oil, JCB Genuine OilIgorNo ratings yet

- ZDFDocument54 pagesZDFAbhinav JainNo ratings yet

- Application of Nanotechnology in Agriculture: Pragati Pramanik P. KrishnanDocument33 pagesApplication of Nanotechnology in Agriculture: Pragati Pramanik P. KrishnanMinh NguyễnNo ratings yet

- City of Waco Landfill, Parts I-II General Application Requirement (Admin Complete 09-14-18)Document264 pagesCity of Waco Landfill, Parts I-II General Application Requirement (Admin Complete 09-14-18)KCEN Channel 6No ratings yet

- 2V0 21 PDFDocument24 pages2V0 21 PDFMoe KaungkinNo ratings yet

- Comparative Study of Hindustan and Dainikjagran Hindi Daily NewspaperDocument67 pagesComparative Study of Hindustan and Dainikjagran Hindi Daily NewspaperAditya ParmarNo ratings yet

- Activity Based Costing HCCDocument8 pagesActivity Based Costing HCCIhsan danishNo ratings yet

- LiquifloCatalog 2009 EngineeringDocument67 pagesLiquifloCatalog 2009 Engineeringleo cejaNo ratings yet

- Claw HammerDocument15 pagesClaw HammerkhalifawhanNo ratings yet

- The Treatment of Wrist Instability: Instructional CourseDocument7 pagesThe Treatment of Wrist Instability: Instructional CourseBasmah Al-DhafarNo ratings yet

- Nova Fórmula de Gessagem Caires e GuimaraesDocument9 pagesNova Fórmula de Gessagem Caires e GuimaraesJefrejan Souza RezendeNo ratings yet

- @5 - Review of C++Document4 pages@5 - Review of C++Chutvinder LanduliyaNo ratings yet

- Full Text CasesDocument239 pagesFull Text CasesAngel EiliseNo ratings yet

- Abhijit Murlidhar Gurav LHTNE00001290914 ENGDocument1 pageAbhijit Murlidhar Gurav LHTNE00001290914 ENGacc.managermarkNo ratings yet

- Kingdom of Saudi Arabia: Engineer: Contractors Joint VentureDocument1 pageKingdom of Saudi Arabia: Engineer: Contractors Joint VentureMohamed BukhamsinNo ratings yet

- CHERRY BLOSSOM LTD V MATIKOLA N and ORS 2020 SCJ 2Document10 pagesCHERRY BLOSSOM LTD V MATIKOLA N and ORS 2020 SCJ 2GirishNo ratings yet

- IS Code 6Document7 pagesIS Code 6Varun DwivediNo ratings yet

- Debug Programming: Table (1) The Debug CommandDocument3 pagesDebug Programming: Table (1) The Debug CommandAyhan AbdulAzizNo ratings yet

- Civil Law Jurist Lecture Notes ReducedDocument21 pagesCivil Law Jurist Lecture Notes ReducedRio AborkaNo ratings yet

- Tecoya Trend 18 August 2021Document4 pagesTecoya Trend 18 August 2021Mohamed NaeimNo ratings yet

- Chapter - III Financial System and Non-Banking Financial Companies - The Structure and Status ProfileDocument55 pagesChapter - III Financial System and Non-Banking Financial Companies - The Structure and Status Profilechirag10pnNo ratings yet

- Algebra Test No. 5Document1 pageAlgebra Test No. 5AMIN BUHARI ABDUL KHADERNo ratings yet

Download as docx, pdf, or txt

You might also like

- Credit Card Authorization Form Sra. LIDIA S. 2023-FIRMA PDFDocument1 pageCredit Card Authorization Form Sra. LIDIA S. 2023-FIRMA PDFAna Velasqz100% (1)

- Test Card CreditDocument32 pagesTest Card CreditHerard Gravi100% (4)

- 1050 Credit Card LabDocument8 pages1050 Credit Card Labapi-287131007No ratings yet

- Credit Card Number Generator & ValidatorDocument2 pagesCredit Card Number Generator & ValidatorMacho100% (2)

- CitikeyDocument54 pagesCitikeyJacob PochinNo ratings yet

- Ant Financial Case StudyDocument42 pagesAnt Financial Case StudytungfptNo ratings yet

- Credit Card Generator: Plagiarism Checker DA Checker Paraphrasing Tool Guest Post Service Premium Plans Register LoginDocument7 pagesCredit Card Generator: Plagiarism Checker DA Checker Paraphrasing Tool Guest Post Service Premium Plans Register Logingel gel60% (5)

- Bulk Credit Card DetailsDocument1 pageBulk Credit Card Detailsja100% (3)

- CC Strip ExplainedDocument11 pagesCC Strip ExplainedBlakeNo ratings yet

- Debit CardDocument22 pagesDebit CardDivya GoelNo ratings yet

- Hotel Credit Card Authorization Form 01Document2 pagesHotel Credit Card Authorization Form 01Liza wong100% (1)

- Employee Credit Card Authorization FormDocument2 pagesEmployee Credit Card Authorization FormLiza wongNo ratings yet

- How Hackers Hack Credit Cards or Debit Cards Password OnlineDocument9 pagesHow Hackers Hack Credit Cards or Debit Cards Password OnlineWalsy Sissoko100% (1)

- Debit Cards - All You Need To KnowDocument48 pagesDebit Cards - All You Need To KnowDavid Ramirez100% (1)

- Biometrics in Credit Cards: AnewwaytopayDocument31 pagesBiometrics in Credit Cards: AnewwaytopayRam Prasad Reddy SadiNo ratings yet

- Credit CardDocument100 pagesCredit CardSonia DuttNo ratings yet

- BinDocument3 pagesBincarlos50% (2)

- Credit CardDocument32 pagesCredit CardMasih Saab100% (2)

- How To Hack Websites, Passwords, Everything Step by STDocument3 pagesHow To Hack Websites, Passwords, Everything Step by STVivex2k1967% (9)

- Statistics Skittles ProjectDocument7 pagesStatistics Skittles Projectapi-302339334No ratings yet

- Beer GameDocument8 pagesBeer Gamelay fengNo ratings yet

- Domain Certifications Credit CardsDocument65 pagesDomain Certifications Credit Cardspratham_greatNo ratings yet

- Debit Cards & Credit CardsDocument28 pagesDebit Cards & Credit CardsullasNo ratings yet

- Process Credit Card AuthorizationDocument2 pagesProcess Credit Card AuthorizationJian GabatNo ratings yet

- Achieve Instant Approval and Issuance of Credit Cards Using Bizagi - NividousDocument1 pageAchieve Instant Approval and Issuance of Credit Cards Using Bizagi - NividousNividousNo ratings yet

- Safari - Oct 13, 2020 at 6:15 PMDocument1 pageSafari - Oct 13, 2020 at 6:15 PMJaboris JohnNo ratings yet

- HDFC Bank Credit Card Customer Care Number - 24x7Document5 pagesHDFC Bank Credit Card Customer Care Number - 24x7Baswamy CseNo ratings yet

- 6 Credit CardsDocument77 pages6 Credit CardsKartik BhartiaNo ratings yet

- Mitc For Amazon Pay Credit CardDocument7 pagesMitc For Amazon Pay Credit CardBlain Santhosh FernandesNo ratings yet

- Credit Card PDFDocument7 pagesCredit Card PDFhmsonawane100% (1)

- Credit CardsDocument10 pagesCredit CardsMadhur GuptaNo ratings yet

- Credit Card FraudsDocument63 pagesCredit Card FraudsAnaghaPuranikNo ratings yet

- Credit Cards: Personal FinanceDocument36 pagesCredit Cards: Personal FinanceAmara MaduagwuNo ratings yet

- Credit Card Management Information SysteDocument9 pagesCredit Card Management Information SysteAnant JainNo ratings yet

- Payments in Order Management in R12 (Doc ID 1164613.1) : Applies ToDocument33 pagesPayments in Order Management in R12 (Doc ID 1164613.1) : Applies ToManoj100% (1)

- Credit Card HackingDocument2 pagesCredit Card Hackingmadarauchiha50% (2)

- Supervisory Policy Manual: CR-S-5 Credit Card BusinessDocument43 pagesSupervisory Policy Manual: CR-S-5 Credit Card BusinessccnmiNo ratings yet

- Buy Now Pay Later BNPLOn Your Credit CardDocument26 pagesBuy Now Pay Later BNPLOn Your Credit CardShivaniNo ratings yet

- Credit CardDocument65 pagesCredit CardKrishana ThakurNo ratings yet

- Credit Card Processing GlossaryDocument14 pagesCredit Card Processing Glossarykintirgum100% (1)

- e BankingDocument61 pagese BankingRiSHI KeSH GawaINo ratings yet

- Credit Card Verification Procedures - V2Document8 pagesCredit Card Verification Procedures - V2Yess GuzmánNo ratings yet

- Credit Card ClientsDocument943 pagesCredit Card ClientsMamadou SowNo ratings yet

- Debit Card - Project Wark PDFDocument158 pagesDebit Card - Project Wark PDFManisha GuptaNo ratings yet

- Credit CardsDocument22 pagesCredit CardsEti Prince BajajNo ratings yet

- TransFirst - Merchant - Card Processing - Operating - Guide - v6-0915Document139 pagesTransFirst - Merchant - Card Processing - Operating - Guide - v6-0915sreejaNo ratings yet

- Corporation Bank Credit CardsDocument7 pagesCorporation Bank Credit CardsSuriya KJ100% (1)

- Cards: March XX, 2010Document57 pagesCards: March XX, 2010Keerti MannanNo ratings yet

- Vanilla Visa Gift Card BalanceDocument1 pageVanilla Visa Gift Card BalanceSamridhi Rai0% (1)

- Credit CardDocument6 pagesCredit Cardvj1414100% (1)

- WL WLDocument3 pagesWL WLsoumya pattanaikNo ratings yet

- BD Gold Visa Mastercard Credit Card v1Document14 pagesBD Gold Visa Mastercard Credit Card v1sajjad147No ratings yet

- Ideposit Merchant ApplicationDocument4 pagesIdeposit Merchant Applicationcris4455No ratings yet

- Credit Card Industry in IndiaDocument28 pagesCredit Card Industry in IndiaAk SahNo ratings yet

- How To Cash Out From Stolen Credit CardsDocument1 pageHow To Cash Out From Stolen Credit Cardsjohn100% (1)

- Bank Account Name & NumberDocument20 pagesBank Account Name & NumberNayeem AhmedNo ratings yet

- Credit CardDocument51 pagesCredit CardSmita JainNo ratings yet

- How Credit Cards Work: A Bit of HistoryDocument18 pagesHow Credit Cards Work: A Bit of HistoryVishal Kumar ShawNo ratings yet

- Visa HackDocument2 pagesVisa Hackheadpnc75% (4)

- Credit CardDocument77 pagesCredit CardSamuel DavisNo ratings yet

- Debit Card Info PDFDocument18 pagesDebit Card Info PDFjack meoffNo ratings yet

- RTG CPRed Jumpstart HSGCharsDocument6 pagesRTG CPRed Jumpstart HSGCharsOrlando SaallNo ratings yet

- BUS 201 Midterm Answer (19104022, Sec 7)Document7 pagesBUS 201 Midterm Answer (19104022, Sec 7)Redwan Afrid AvinNo ratings yet

- MaxLife Fraud AwarenessDocument1 pageMaxLife Fraud Awarenessbhavnapal74No ratings yet

- High Power CommitteeDocument39 pagesHigh Power CommitteeJaya PrabhaNo ratings yet

- Ora Linux InstallationDocument2 pagesOra Linux InstallationhenpuneNo ratings yet

- JCB Oil, JCB Genuine OilDocument2 pagesJCB Oil, JCB Genuine OilIgorNo ratings yet

- ZDFDocument54 pagesZDFAbhinav JainNo ratings yet

- Application of Nanotechnology in Agriculture: Pragati Pramanik P. KrishnanDocument33 pagesApplication of Nanotechnology in Agriculture: Pragati Pramanik P. KrishnanMinh NguyễnNo ratings yet

- City of Waco Landfill, Parts I-II General Application Requirement (Admin Complete 09-14-18)Document264 pagesCity of Waco Landfill, Parts I-II General Application Requirement (Admin Complete 09-14-18)KCEN Channel 6No ratings yet

- 2V0 21 PDFDocument24 pages2V0 21 PDFMoe KaungkinNo ratings yet

- Comparative Study of Hindustan and Dainikjagran Hindi Daily NewspaperDocument67 pagesComparative Study of Hindustan and Dainikjagran Hindi Daily NewspaperAditya ParmarNo ratings yet

- Activity Based Costing HCCDocument8 pagesActivity Based Costing HCCIhsan danishNo ratings yet

- LiquifloCatalog 2009 EngineeringDocument67 pagesLiquifloCatalog 2009 Engineeringleo cejaNo ratings yet

- Claw HammerDocument15 pagesClaw HammerkhalifawhanNo ratings yet

- The Treatment of Wrist Instability: Instructional CourseDocument7 pagesThe Treatment of Wrist Instability: Instructional CourseBasmah Al-DhafarNo ratings yet

- Nova Fórmula de Gessagem Caires e GuimaraesDocument9 pagesNova Fórmula de Gessagem Caires e GuimaraesJefrejan Souza RezendeNo ratings yet

- @5 - Review of C++Document4 pages@5 - Review of C++Chutvinder LanduliyaNo ratings yet

- Full Text CasesDocument239 pagesFull Text CasesAngel EiliseNo ratings yet

- Abhijit Murlidhar Gurav LHTNE00001290914 ENGDocument1 pageAbhijit Murlidhar Gurav LHTNE00001290914 ENGacc.managermarkNo ratings yet

- Kingdom of Saudi Arabia: Engineer: Contractors Joint VentureDocument1 pageKingdom of Saudi Arabia: Engineer: Contractors Joint VentureMohamed BukhamsinNo ratings yet

- CHERRY BLOSSOM LTD V MATIKOLA N and ORS 2020 SCJ 2Document10 pagesCHERRY BLOSSOM LTD V MATIKOLA N and ORS 2020 SCJ 2GirishNo ratings yet

- IS Code 6Document7 pagesIS Code 6Varun DwivediNo ratings yet

- Debug Programming: Table (1) The Debug CommandDocument3 pagesDebug Programming: Table (1) The Debug CommandAyhan AbdulAzizNo ratings yet

- Civil Law Jurist Lecture Notes ReducedDocument21 pagesCivil Law Jurist Lecture Notes ReducedRio AborkaNo ratings yet

- Tecoya Trend 18 August 2021Document4 pagesTecoya Trend 18 August 2021Mohamed NaeimNo ratings yet

- Chapter - III Financial System and Non-Banking Financial Companies - The Structure and Status ProfileDocument55 pagesChapter - III Financial System and Non-Banking Financial Companies - The Structure and Status Profilechirag10pnNo ratings yet

- Algebra Test No. 5Document1 pageAlgebra Test No. 5AMIN BUHARI ABDUL KHADERNo ratings yet