Download as pdf or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5825)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (903)

- Gun Trust TemplateDocument26 pagesGun Trust TemplateKoop Got Da Keys62% (13)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (823)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Assignment - Proposal Writting Assignment July 20Document2 pagesAssignment - Proposal Writting Assignment July 20Digital Era0% (1)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Mayor Vs TiuDocument1 pageMayor Vs TiuLara Cacal50% (4)

- MTN CRBT Contract PDFDocument4 pagesMTN CRBT Contract PDFAEG EntertainmentNo ratings yet

- 11 & 12Document10 pages11 & 12AnandNo ratings yet

- Alumnus Poster PDFDocument1 pageAlumnus Poster PDFAnandNo ratings yet

- Alumnus PosterDocument1 pageAlumnus PosterAnandNo ratings yet

- December: Sunday Monday Tuesday Wednesday Thursday Friday SaturdayDocument1 pageDecember: Sunday Monday Tuesday Wednesday Thursday Friday SaturdayAnandNo ratings yet

- Horizontal Integration: Submitted by Arundhathi V K 18382007 Aswin T R 18382008Document8 pagesHorizontal Integration: Submitted by Arundhathi V K 18382007 Aswin T R 18382008AnandNo ratings yet

- Vertical Integration: BY Anand Mallik Arjun M.SDocument16 pagesVertical Integration: BY Anand Mallik Arjun M.SAnandNo ratings yet

- OppoDocument4 pagesOppoAnandNo ratings yet

- 03 & 04Document11 pages03 & 04AnandNo ratings yet

- Incoterms 2020: Key Changes in Incoterms® 2020 Dat Is Changed To DpuDocument3 pagesIncoterms 2020: Key Changes in Incoterms® 2020 Dat Is Changed To DpuAnandNo ratings yet

- International Strategic Management: BrandingDocument15 pagesInternational Strategic Management: BrandingAnandNo ratings yet

- General Journal FormatDocument2 pagesGeneral Journal FormatAnandNo ratings yet

- Annual Report 2018Document80 pagesAnnual Report 2018Anand0% (1)

- General Journal FormatDocument2 pagesGeneral Journal FormatAnandNo ratings yet

- FL1 & 2 Long Answers PDFDocument9 pagesFL1 & 2 Long Answers PDFVasanth KumarNo ratings yet

- Rite Aid Bankrutpcy Store Closing List 6-17-24Document73 pagesRite Aid Bankrutpcy Store Closing List 6-17-24WXYZ-TV Channel 7 DetroitNo ratings yet

- Contract - Sma A17 000456Document6 pagesContract - Sma A17 000456Dirty RatsNo ratings yet

- Contract of Lease JilDocument2 pagesContract of Lease JilYaj CruzadaNo ratings yet

- Ebook Critical Concepts of Canadian Business Law 6Th Edition Smyth Test Bank Full Chapter PDFDocument41 pagesEbook Critical Concepts of Canadian Business Law 6Th Edition Smyth Test Bank Full Chapter PDFMrScottPowelltgry100% (12)

- Agreement For HSBC Time Draft 30mDocument13 pagesAgreement For HSBC Time Draft 30msathyaji100% (2)

- Consulting AgreementDocument6 pagesConsulting AgreementRocketLawyer80% (10)

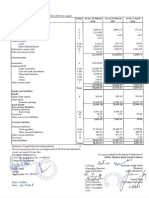

- BSMC Model Fsa 2023-24Document14 pagesBSMC Model Fsa 2023-24in.raunaqNo ratings yet

- Purchase America Course BookDocument90 pagesPurchase America Course BookA Dwight Hill100% (2)

- Elmar Case G.R. No. 162580Document2 pagesElmar Case G.R. No. 162580Lu CasNo ratings yet

- (Nov 2020) Latest Safecustody ListingDocument923 pages(Nov 2020) Latest Safecustody Listingcinta amaniNo ratings yet

- OMCC Board ResolutionDocument1 pageOMCC Board ResolutionOrient MansionNo ratings yet

- 5B. Purchase Order (Equipment Rental)Document2 pages5B. Purchase Order (Equipment Rental)Bdak B. IbiasNo ratings yet

- Agreement - A Contract To Arbitrate A: ApplicationDocument12 pagesAgreement - A Contract To Arbitrate A: ApplicationGelo MVNo ratings yet

- Slinkard File 2Document12 pagesSlinkard File 2the kingfishNo ratings yet

- Department of Labor: RBC Actions Dec07Document6 pagesDepartment of Labor: RBC Actions Dec07USA_DepartmentOfLaborNo ratings yet

- 2022 TZHC 1110Document9 pages2022 TZHC 1110LameckNo ratings yet

- BookDocument235 pagesBookSyed HamdanNo ratings yet

- Omega Case Mba HRDocument1 pageOmega Case Mba HRSIDHANT KHULLARNo ratings yet

- General Power of AttorneyDocument2 pagesGeneral Power of Attorneysaqib nawazNo ratings yet

- Henry Vs Madison Aerie No. 623Document3 pagesHenry Vs Madison Aerie No. 623Jullianne Micaell CarlayNo ratings yet

- Metropolitan Bank Vs Junnel S MarketingDocument2 pagesMetropolitan Bank Vs Junnel S MarketingMary Angelica SangalangNo ratings yet

- Copying - SpelunkyDocument2 pagesCopying - SpelunkyVincent MastonNo ratings yet

- Case Compilation OBLICON Civil Law Review 2 Atty Uribe Part1 PDFDocument24 pagesCase Compilation OBLICON Civil Law Review 2 Atty Uribe Part1 PDFJamaila jimeno DagcutanNo ratings yet

- Truth in Lending Act - Data BankDocument2 pagesTruth in Lending Act - Data Bankjeongchaeng no jam brotherNo ratings yet

- LEGMED Rosit Vs Davao Doctor HospitalDocument1 pageLEGMED Rosit Vs Davao Doctor HospitalsarmientoelizabethNo ratings yet