Download as pdf or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5835)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (903)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (350)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (824)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (405)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Loney v. People, G.R. No. 152644, February 10, 2006Document2 pagesLoney v. People, G.R. No. 152644, February 10, 2006Pamela Camille Barredo0% (1)

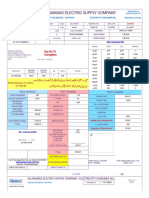

- Iesco Online BillDocument1 pageIesco Online BillRocky BhaiNo ratings yet

- Chapter 4Document42 pagesChapter 4kartik kasniaNo ratings yet

- Respondent Memo UOIDocument9 pagesRespondent Memo UOIHeena ShaikhNo ratings yet

- Caram v. Segui (Digest)Document2 pagesCaram v. Segui (Digest)Arellano Aure100% (2)

- Josip Broz Tito: Jump To Navigation Jump To SearchDocument66 pagesJosip Broz Tito: Jump To Navigation Jump To SearchJan BaricevacNo ratings yet

- Chapter 2 Oblicon ReviewerDocument7 pagesChapter 2 Oblicon ReviewerPetrelle RodrigoNo ratings yet

- Bare Acts Live: U.P. Co-Operative and Panchayat Audit Service Rules, 1979 (UP336.HTM#0)Document10 pagesBare Acts Live: U.P. Co-Operative and Panchayat Audit Service Rules, 1979 (UP336.HTM#0)Anonymous Q3golGNo ratings yet

- Parties To Court Actions in Saga Age Ice PDFDocument246 pagesParties To Court Actions in Saga Age Ice PDFRodrigo HkyNo ratings yet

- TaxDocument13 pagesTaxPinky SalvadorNo ratings yet

- 911 Disarm FinalreportDocument49 pages911 Disarm FinalreportMike-bastard Sanchez Dope-krazyNo ratings yet

- IGR Presentation-1Document20 pagesIGR Presentation-1Alma L. LamilaNo ratings yet

- Gonzales v. Intermediate Appellate Court, G.R. No. 69622, January 29, 1988Document7 pagesGonzales v. Intermediate Appellate Court, G.R. No. 69622, January 29, 1988Christopher Julian ArellanoNo ratings yet

- STPMDocument219 pagesSTPMDon CamuaNo ratings yet

- Is India A Soft NationDocument2 pagesIs India A Soft Nationantra vNo ratings yet

- GR226405 DigestDocument1 pageGR226405 DigestLito Lagunday (litlag)No ratings yet

- Kilosbayan Vs MoratoDocument1 pageKilosbayan Vs MoratoCarlo Jose BactolNo ratings yet

- Minor Operations Consent Form GP v1 0 250116Document3 pagesMinor Operations Consent Form GP v1 0 250116rockkk45No ratings yet

- Sources English LawDocument45 pagesSources English Lawzafar gharshinNo ratings yet

- Royster Company v. United States, 479 F.2d 387, 4th Cir. (1973)Document7 pagesRoyster Company v. United States, 479 F.2d 387, 4th Cir. (1973)Scribd Government DocsNo ratings yet

- Why Do We Need Political Parties?Document3 pagesWhy Do We Need Political Parties?AdyaNo ratings yet

- Performance Securing Declaration 2021Document2 pagesPerformance Securing Declaration 2021Mike Francis F GubuanNo ratings yet

- 'Most Immediate' Reminder Government of Telangana Irrigation and Cad DepartmentDocument5 pages'Most Immediate' Reminder Government of Telangana Irrigation and Cad DepartmentMaheshbabu SarellaNo ratings yet

- 2015 01.15 App Permission File Second HabeasDocument54 pages2015 01.15 App Permission File Second HabeascbsradionewsNo ratings yet

- Class IV Regional Mental Hospital Pune 1Document76 pagesClass IV Regional Mental Hospital Pune 1mophcvaduth1No ratings yet

- Final Memorial PetitionerDocument34 pagesFinal Memorial PetitionerasjaNo ratings yet

- Civil Procedure Code Revision QuizDocument4 pagesCivil Procedure Code Revision QuizKunal KantNo ratings yet

- CIPP:A Blueprint PDFDocument2 pagesCIPP:A Blueprint PDFroruangNo ratings yet

- Minutes of The 21st UPCSC MeetingDocument6 pagesMinutes of The 21st UPCSC MeetingUPCebuStudentCouncilNo ratings yet

- DE BORJA V. DE BORJA (G.R. No. L-28611 August 18, 1972)Document2 pagesDE BORJA V. DE BORJA (G.R. No. L-28611 August 18, 1972)MhareyNo ratings yet