Download as pdf or txt

You might also like

- Why Have These Three Firms Chosen To Grow by AcquisitionsDocument2 pagesWhy Have These Three Firms Chosen To Grow by AcquisitionsMuhammad Imran Bhatti100% (1)

- Case 22 Victoria Chemicals PLC (A)Document2 pagesCase 22 Victoria Chemicals PLC (A)tipo_de_incognito75% (4)

- Corporate Finance 11Th Edition Ross Solutions Manual Full Chapter PDFDocument35 pagesCorporate Finance 11Th Edition Ross Solutions Manual Full Chapter PDFvernon.amundson153100% (10)

- Solution Manual For Fundamentals of Investment Management 10th Edition by HirtDocument21 pagesSolution Manual For Fundamentals of Investment Management 10th Edition by HirtBriannaPerryjdwr100% (41)

- Private Equity Case StudyDocument11 pagesPrivate Equity Case StudyAmineBekkalNo ratings yet

- # PMP Tricky QuestionsDocument44 pages# PMP Tricky QuestionsI Kailash Rao100% (4)

- Wise Money: Using the Endowment Investment Approach to Minimize Volatility and Increase ControlFrom EverandWise Money: Using the Endowment Investment Approach to Minimize Volatility and Increase ControlNo ratings yet

- Iacademy Basicfin: Basic Finance and Financial Management Final RequirementDocument5 pagesIacademy Basicfin: Basic Finance and Financial Management Final RequirementClarisse AlimotNo ratings yet

- Written Assignment Unit 6Document8 pagesWritten Assignment Unit 6rony alexander75% (4)

- ISec Business Presentation Investor Conference November 2019Document49 pagesISec Business Presentation Investor Conference November 2019Bhagwan BachaiNo ratings yet

- JM Small Cap Fund - Leaflet-2Document2 pagesJM Small Cap Fund - Leaflet-2manan_sshahNo ratings yet

- Gain - Pro Report - Private Equity vs. Independently HeldDocument36 pagesGain - Pro Report - Private Equity vs. Independently HeldLegonNo ratings yet

- We Have Been You Mr. Bond - CMT Smart BriefDocument5 pagesWe Have Been You Mr. Bond - CMT Smart BriefKrishna SamhithaNo ratings yet

- Income and Growth FundDocument4 pagesIncome and Growth FundKent LimNo ratings yet

- ISec Business Presentation Investor Conference August 2019Document35 pagesISec Business Presentation Investor Conference August 2019Bhagwan BachaiNo ratings yet

- Wipro Vs InfosysDocument27 pagesWipro Vs Infosysshoeb75% (4)

- FPT Fundamental of Financial Management ReportDocument29 pagesFPT Fundamental of Financial Management ReportTrần Phương Quỳnh TrangNo ratings yet

- Financial Management Unit - 3Document22 pagesFinancial Management Unit - 3nallspalanikNo ratings yet

- Presentation by Malcolm Wagget, Chief Operating Officer HSBC Global Resourcing, South AsiaDocument25 pagesPresentation by Malcolm Wagget, Chief Operating Officer HSBC Global Resourcing, South AsiaAmit Kumar PandeyNo ratings yet

- Credit Suisse Resiliency-Q1-2019Document24 pagesCredit Suisse Resiliency-Q1-2019sentoubudo1647No ratings yet

- Palm ValleyDocument12 pagesPalm ValleyholdencNo ratings yet

- Fundamental Analysis of InfosysDocument4 pagesFundamental Analysis of InfosysVASANTADA SRIKANTH (PGP 2016-18)No ratings yet

- Value DriversDocument28 pagesValue DriversAbhishek SachdevaNo ratings yet

- Ac Asing by SushilDocument6 pagesAc Asing by SushilSUSHIL MEGHANINo ratings yet

- Investment Companies Made Simple 2023Document20 pagesInvestment Companies Made Simple 2023quantridoanhnghiep360No ratings yet

- Using Multiples For ValuationDocument26 pagesUsing Multiples For ValuationGuillermo LyNo ratings yet

- 259 - ETP Factsheet Oct 2022Document2 pages259 - ETP Factsheet Oct 2022Sundaresan MunuswamyNo ratings yet

- IFII Research Report Vincent TjoeDocument4 pagesIFII Research Report Vincent TjoeVincent TjoeNo ratings yet

- Financial Structure RatioDocument7 pagesFinancial Structure RatioEthan Jiro LegaspiNo ratings yet

- Capital Structure and LeverageDocument31 pagesCapital Structure and Leveragechandel08No ratings yet

- All Revenues Are Not Equal: India InternetDocument8 pagesAll Revenues Are Not Equal: India InternetAnu BNo ratings yet

- Investments-Fixed IncomeDocument5 pagesInvestments-Fixed IncomevenugopallNo ratings yet

- Operating Ratios of Software CompaniesDocument16 pagesOperating Ratios of Software CompaniesMyExamPlanNo ratings yet

- Leibowitz 1990Document19 pagesLeibowitz 1990Inceif KmcNo ratings yet

- Auto ZoneDocument3 pagesAuto ZoneGeorgina AlpertNo ratings yet

- How To Buy, Sell and Value Shares in Stock ExchangesDocument85 pagesHow To Buy, Sell and Value Shares in Stock Exchangesagrawal.minNo ratings yet

- HDFC Manufacturing Fund - NFO - Leaflet - HDFC BankDocument2 pagesHDFC Manufacturing Fund - NFO - Leaflet - HDFC Bankyeheji8177No ratings yet

- Aditya Birla Capital: Equentis Scale 1 2 3 4 5 Below Avg. Avg. Good Very Good ExcellentDocument2 pagesAditya Birla Capital: Equentis Scale 1 2 3 4 5 Below Avg. Avg. Good Very Good Excellentsayuj83No ratings yet

- Fin 201 WordDocument17 pagesFin 201 Wordsayara.akhter08No ratings yet

- Infosys: "Power of Talent"Document25 pagesInfosys: "Power of Talent"Amarjeet JadejaNo ratings yet

- Increasing Market Share Profitably ForDocument16 pagesIncreasing Market Share Profitably ForDarshit GandhiNo ratings yet

- SBI International Access US Equity FoFDocument26 pagesSBI International Access US Equity FoFRoshanR.NawaleNo ratings yet

- Balancing ROIC and Growth To Build ValueDocument8 pagesBalancing ROIC and Growth To Build ValueLuis Daniel Napa TorresNo ratings yet

- Fidelity Funds - China Opportunities Fund: 31 July 2018 年年7⽉月31⽇日Document2 pagesFidelity Funds - China Opportunities Fund: 31 July 2018 年年7⽉月31⽇日silver lauNo ratings yet

- Project Omega (Presentation)Document16 pagesProject Omega (Presentation)kotharik52No ratings yet

- Impress PMS - Jan 24 - Anand Rathi PMSDocument19 pagesImpress PMS - Jan 24 - Anand Rathi PMSshivamsundaram794No ratings yet

- Aditya Birla Sun AMCDocument31 pagesAditya Birla Sun AMCkrishna_buntyNo ratings yet

- Bluebay Multi Asset Credit Jan23Document7 pagesBluebay Multi Asset Credit Jan23Ali ImranNo ratings yet

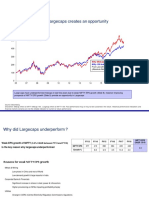

- Equity Markets Review Underperformance of Largecaps Creates An OpportunityDocument8 pagesEquity Markets Review Underperformance of Largecaps Creates An OpportunitysumeetNo ratings yet

- ch12 3Document27 pagesch12 3hind.thamer.2002No ratings yet

- Fin Mid Quiz FinalDocument44 pagesFin Mid Quiz FinalAtik MahbubNo ratings yet

- BA449 - Chap005 - Fall 2020Document49 pagesBA449 - Chap005 - Fall 2020mashalerahNo ratings yet

- Infosys Fundamental Analysis and Future OutlookDocument10 pagesInfosys Fundamental Analysis and Future OutlookMayank TeotiaNo ratings yet

- Assignment - Corporate FinanceDocument9 pagesAssignment - Corporate FinanceShivam GoelNo ratings yet

- SolutionsDocument4 pagesSolutionsTamar PkhakadzeNo ratings yet

- EPS or ROEDocument2 pagesEPS or ROEsabharwal.sunnyNo ratings yet

- The Case For Emerging Markets Private Equity: V.10 May 2012Document33 pagesThe Case For Emerging Markets Private Equity: V.10 May 2012Bryan LiNo ratings yet

- FAQs - SBI Dividend Yield FundDocument8 pagesFAQs - SBI Dividend Yield FundAnil Kumar Reddy ChinthaNo ratings yet

- Capital Appreciation - All Equity PortfolioDocument2 pagesCapital Appreciation - All Equity PortfolioDwi Rizki Anisa PandiaNo ratings yet

- Presentation 1Document5 pagesPresentation 1taruncoc102030400No ratings yet

- Strategic Bond Fund (59) : Fixed Income Investment GradeDocument2 pagesStrategic Bond Fund (59) : Fixed Income Investment GradeHayston DezmenNo ratings yet

- HDFC PPT FinalDocument12 pagesHDFC PPT FinalRISHABH RAJ-DM 21DM237No ratings yet

- DIVIDEND INVESTING: Maximizing Returns while Minimizing Risk through Selective Stock Selection and Diversification (2023 Guide for Beginners)From EverandDIVIDEND INVESTING: Maximizing Returns while Minimizing Risk through Selective Stock Selection and Diversification (2023 Guide for Beginners)No ratings yet

- Studi Kelayakan Bisnis Bengkel Bubut Cipta Teknik Mandiri (Studi Kasus Di Perumnas Tangerang Banten)Document8 pagesStudi Kelayakan Bisnis Bengkel Bubut Cipta Teknik Mandiri (Studi Kasus Di Perumnas Tangerang Banten)Billy AdityaNo ratings yet

- Case StudyDocument136 pagesCase StudyNadeem AhmadNo ratings yet

- Investment Office ANRS: Project Profile On The Establishment of Electrical Dividers and Other Accessories Making PlantDocument26 pagesInvestment Office ANRS: Project Profile On The Establishment of Electrical Dividers and Other Accessories Making PlantJohn100% (2)

- Corporate FinanceDocument4 pagesCorporate FinanceSaurabh Singh RawatNo ratings yet

- Last Assignment December 2022Document77 pagesLast Assignment December 2022DavidNo ratings yet

- Which Type of Benchmarking Is The Company Using?Document20 pagesWhich Type of Benchmarking Is The Company Using?Aslam SiddiqNo ratings yet

- Test Bank For Succeeding in Business With Microsoft Excel 2013 A Problem Solving Approach 1st EditionDocument21 pagesTest Bank For Succeeding in Business With Microsoft Excel 2013 A Problem Solving Approach 1st Editionmarysmithywzbmapscd100% (23)

- Project Finance Question PaperDocument3 pagesProject Finance Question PaperBhavna0% (1)

- LEMBAR JAWABAN CH.10 (Capital Budgeting Techniques)Document4 pagesLEMBAR JAWABAN CH.10 (Capital Budgeting Techniques)Cindy PNo ratings yet

- Noreen5e Ch07Document81 pagesNoreen5e Ch07algokar999No ratings yet

- Preparation of Feasibility Study PDFDocument4 pagesPreparation of Feasibility Study PDFDipak PatelNo ratings yet

- Final FIN 200 (All Chapters) FIXEDDocument65 pagesFinal FIN 200 (All Chapters) FIXEDMunNo ratings yet

- IRR Calculations Exercise - SolutionDocument6 pagesIRR Calculations Exercise - SolutionArnav DadaNo ratings yet

- Chapt 13 Capital Investment DecisionsDocument28 pagesChapt 13 Capital Investment DecisionsDebi Fitra YandaNo ratings yet

- Business Studies Pre U PDFDocument35 pagesBusiness Studies Pre U PDFSamihaSaanNo ratings yet

- 5 - Risk and Return: Past and PrologueDocument39 pages5 - Risk and Return: Past and PrologueA_StudentsNo ratings yet

- Comparing Projects With Unequal LivesDocument3 pagesComparing Projects With Unequal LivesdzazeenNo ratings yet

- FM Examiner's Report March June 2022Document24 pagesFM Examiner's Report March June 2022leylaNo ratings yet

- Chapter 6 KT322HDocument25 pagesChapter 6 KT322HDuong Gia Linh B2112435No ratings yet

- Cumulative Cash Flow Discounted Cash Flow Cum Discounted Cash FlowDocument173 pagesCumulative Cash Flow Discounted Cash Flow Cum Discounted Cash FlowAditi OholNo ratings yet

- Feasibility Report of BakeryDocument43 pagesFeasibility Report of BakeryEdz Medina50% (2)

- Er - 6 - Guideline For Detailed Budget and Financial Forecast - Ro - Version 4 - Ro Energy sgs4Document3 pagesEr - 6 - Guideline For Detailed Budget and Financial Forecast - Ro - Version 4 - Ro Energy sgs4nicoclau2005No ratings yet

- Case Primus Automation Division 2002Document16 pagesCase Primus Automation Division 2002Sasha Khalishah50% (2)

- Bravo Cross Asset Manager Presentation PDFDocument32 pagesBravo Cross Asset Manager Presentation PDFakarastNo ratings yet

- Semester 2-Question Bank For VivaDocument49 pagesSemester 2-Question Bank For Vivareckkit benckiserNo ratings yet