Download as docx, pdf, or txt

You might also like

- Contemporary Auditing 10th Edition Knapp Solutions Manual 1Document8 pagesContemporary Auditing 10th Edition Knapp Solutions Manual 1consuelo100% (37)

- Consignment Sales 2Document22 pagesConsignment Sales 2Mhelka Tiodianco33% (3)

- Consignment Sales 2Document22 pagesConsignment Sales 2Mhelka Tiodianco33% (3)

- Consignment Sales 2Document22 pagesConsignment Sales 2Mhelka Tiodianco33% (3)

- The Rise and Fall of Phar-Mor Inc.Document14 pagesThe Rise and Fall of Phar-Mor Inc.Louis Lebron100% (1)

- Consignment SalesDocument10 pagesConsignment SalesMhelka TiodiancoNo ratings yet

- Phar Mor Case StudyDocument7 pagesPhar Mor Case Studypragun jainNo ratings yet

- Case StudyDocument5 pagesCase Studynovac18No ratings yet

- Happiness Express, IncDocument6 pagesHappiness Express, Inclulupuspitaa50% (2)

- MW FrauducationWhitePaperDocument20 pagesMW FrauducationWhitePapermattdoughNo ratings yet

- Financial ScandalsDocument26 pagesFinancial ScandalsReina Nina Camano25% (4)

- GlaucusResearch-National Beverage-Short-Nasdaq FIZZ Sept 28 2016Document51 pagesGlaucusResearch-National Beverage-Short-Nasdaq FIZZ Sept 28 2016chasingthevigNo ratings yet

- Enron Company Reaction PaperDocument7 pagesEnron Company Reaction PaperJames Lorenz FelizarteNo ratings yet

- Investment in Equity Securities 2Document26 pagesInvestment in Equity Securities 2Mhelka Tiodianco0% (1)

- Summary of Leslie Fay Company StudyDocument5 pagesSummary of Leslie Fay Company StudyMhelka TiodiancoNo ratings yet

- Leslie Fay CaseDocument10 pagesLeslie Fay CaseSalman J. Syed50% (2)

- Dwnload Full Contemporary Auditing 10th Edition Knapp Solutions Manual PDFDocument35 pagesDwnload Full Contemporary Auditing 10th Edition Knapp Solutions Manual PDFfurmediatetbpwnk100% (20)

- Contemporary Auditing 10th Edition Knapp Solutions ManualDocument35 pagesContemporary Auditing 10th Edition Knapp Solutions Manualchardskyishqb88100% (24)

- Contemporary Auditing 10th Edition Knapp Solutions ManualDocument82 pagesContemporary Auditing 10th Edition Knapp Solutions Manualreneewiserqacpeofik100% (12)

- Leslie FayDocument6 pagesLeslie FayNovah Mae Begaso Samar100% (2)

- Group 05 Slide - The Lesley Fay CompanyDocument33 pagesGroup 05 Slide - The Lesley Fay CompanyNazmulNo ratings yet

- Solution Manual For Contemporary Auditing 10th Edition by Knapp ISBN 9781285066608Document36 pagesSolution Manual For Contemporary Auditing 10th Edition by Knapp ISBN 9781285066608kylescottokjfxibrqy100% (24)

- Solution Manual For Ethical Obligations and Decision Making in Accounting Text and Cases 4th EditionDocument36 pagesSolution Manual For Ethical Obligations and Decision Making in Accounting Text and Cases 4th Editionbemasterdurga.qkgo100% (53)

- White Collar CrimesDocument9 pagesWhite Collar CrimesandrewNo ratings yet

- Contemporary Auditing 10th Edition Knapp Solutions Manual 1Document36 pagesContemporary Auditing 10th Edition Knapp Solutions Manual 1theodorelambnqcdaxswim100% (31)

- Business Ethics Case StudiesDocument2 pagesBusiness Ethics Case StudiesajmaheshNo ratings yet

- Phar MoreDocument25 pagesPhar MoreAlexandrei OrioNo ratings yet

- Case Analysis InfoactDocument6 pagesCase Analysis InfoactMichaela KowalskiNo ratings yet

- Compilation of Accounting ScandalsDocument7 pagesCompilation of Accounting ScandalsYelyah HipolitoNo ratings yet

- Scandal FRAPPTDocument31 pagesScandal FRAPPTUtkarsh SinghNo ratings yet

- The 10 Worst Corporate Accounting Scandals of All TimeDocument4 pagesThe 10 Worst Corporate Accounting Scandals of All TimeNadie LrdNo ratings yet

- Cases Involving Auditors' NegligenceDocument5 pagesCases Involving Auditors' NegligenceJaden EuNo ratings yet

- Reading Assignment 8 (Royal Bank of Scotland)Document14 pagesReading Assignment 8 (Royal Bank of Scotland)Valentine AyiviNo ratings yet

- United States Court of Appeals, Third CircuitDocument16 pagesUnited States Court of Appeals, Third CircuitScribd Government DocsNo ratings yet

- TOP 10 Corporate Scandal: Chronological OrderDocument11 pagesTOP 10 Corporate Scandal: Chronological OrderNiken PratiwiNo ratings yet

- Muhammad Syahrin Bin Zulkefly 2019848422 BA242 5B FIN657 Sir Mohd Husnin Bin Mat YusofDocument3 pagesMuhammad Syahrin Bin Zulkefly 2019848422 BA242 5B FIN657 Sir Mohd Husnin Bin Mat YusofsyahrinNo ratings yet

- Auditing and Corporate Governance: Group No. - 6Document13 pagesAuditing and Corporate Governance: Group No. - 6Sonali ChauhanNo ratings yet

- II SR Jim Chanos Masterclass Dec 14Document16 pagesII SR Jim Chanos Masterclass Dec 14Hedge Fund ConversationsNo ratings yet

- The 10 Worst Corporate Accounting Scandals of All TimeDocument5 pagesThe 10 Worst Corporate Accounting Scandals of All TimePrince RyanNo ratings yet

- Madoff FinalDocument20 pagesMadoff FinalnishithathiNo ratings yet

- Assignment 3Document7 pagesAssignment 3Dawna Lee BerryNo ratings yet

- United States Attorney Southern District of New York: Bernard L. Madoff Charged in Eleven-Count Criminal InformationDocument39 pagesUnited States Attorney Southern District of New York: Bernard L. Madoff Charged in Eleven-Count Criminal InformationChrisNo ratings yet

- The 10 Worst Corporate Accounting Scandals of All TimeDocument4 pagesThe 10 Worst Corporate Accounting Scandals of All TimeFarris Althaf PratamaNo ratings yet

- Who Are The Key Players?Document2 pagesWho Are The Key Players?ke liuNo ratings yet

- American Growth Funding II LLC and Ralph Johnson Financial Fraud ChargesDocument6 pagesAmerican Growth Funding II LLC and Ralph Johnson Financial Fraud ChargesFraudLawyersNo ratings yet

- Accounting Scandals Enron Scandal (2001)Document3 pagesAccounting Scandals Enron Scandal (2001)TRÂN PHẠM NGỌC BẢONo ratings yet

- Lehman Brothers BankruptcyDocument8 pagesLehman Brothers BankruptcyOmar EshanNo ratings yet

- Bernard Lawrence Bernie MadoffDocument12 pagesBernard Lawrence Bernie MadoffKevin Tomaszewski100% (1)

- Translate Case 1.5 (The Leslie Fay Companies)Document10 pagesTranslate Case 1.5 (The Leslie Fay Companies)ranywNo ratings yet

- Accounting Fraud Colonial Bank FraudDocument17 pagesAccounting Fraud Colonial Bank FraudJulie Pearl GuarinNo ratings yet

- Case Analysis 2Document15 pagesCase Analysis 2Mohammad HizamNo ratings yet

- Report On Corporate FraudDocument16 pagesReport On Corporate FraudShivani SharmaNo ratings yet

- Dha Suffa University: Course Title: AUDITING Course Code: MS-2701Document4 pagesDha Suffa University: Course Title: AUDITING Course Code: MS-2701Sunain RizwanNo ratings yet

- Crazy Eddie (Revisited) : TH STDocument4 pagesCrazy Eddie (Revisited) : TH STRudy NgNo ratings yet

- Case 1.8Document4 pagesCase 1.8Ian Chen100% (1)

- Bernie Madoff CaseDocument15 pagesBernie Madoff CaseSaud AlnoohNo ratings yet

- Report Writing ManualDocument12 pagesReport Writing ManualshaniahNo ratings yet

- Mes/index - Html?inline Nyt-Classifier: #1 Ponzi SchemesDocument5 pagesMes/index - Html?inline Nyt-Classifier: #1 Ponzi SchemesAdatu JuNo ratings yet

- The 10 Worst Corporate Accounting Scandals of All Time..Document5 pagesThe 10 Worst Corporate Accounting Scandals of All Time..Tamirat Eshetu Wolde100% (1)

- Seminar Audit - EnglishDocument3 pagesSeminar Audit - EnglishDikdik MaulanaNo ratings yet

- 25 Biggest Corporate Scandals EverDocument5 pages25 Biggest Corporate Scandals EverSilvia Ahmad KhattakNo ratings yet

- American Insurance Group ScandalDocument3 pagesAmerican Insurance Group ScandalMartin Stojanovic75% (4)

- Crisis of Character: Building Corporate Reputation in the Age of SkepticismFrom EverandCrisis of Character: Building Corporate Reputation in the Age of SkepticismNo ratings yet

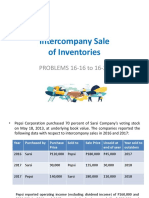

- Intercompany Sales - Inventories ProblemsDocument13 pagesIntercompany Sales - Inventories ProblemsMhelka Tiodianco100% (2)

- Intercompany Sales - Inventories ProblemsDocument13 pagesIntercompany Sales - Inventories ProblemsMhelka Tiodianco100% (2)

- FAR - Specific Intangible AssetsDocument22 pagesFAR - Specific Intangible AssetsMhelka TiodiancoNo ratings yet

- Rocky Mount Undergarment SynthesisDocument7 pagesRocky Mount Undergarment SynthesisMhelka TiodiancoNo ratings yet