Lecture Notes On Quasi-Reorganization

Lecture Notes On Quasi-Reorganization

You might also like

- Accounting For Biological Assets: ObjectivesDocument14 pagesAccounting For Biological Assets: Objectivesrajmeet75% (4)

- Amex STMTDocument1 pageAmex STMTMark GalantyNo ratings yet

- Investment in Equity SecuritiesDocument3 pagesInvestment in Equity Securitiesmiss independentNo ratings yet

- Statement of Financial PositionDocument36 pagesStatement of Financial PositionAbdulmajed Unda MimbantasNo ratings yet

- Shareholders' Equity - Contributed Capital: Part A: The Nature of Shareholders' Equity I. Sources of Shareholders' EquityDocument12 pagesShareholders' Equity - Contributed Capital: Part A: The Nature of Shareholders' Equity I. Sources of Shareholders' Equitycriszel4sobejanaNo ratings yet

- Far Eastern University - Makati: Discussion ProblemsDocument2 pagesFar Eastern University - Makati: Discussion ProblemsMarielle SidayonNo ratings yet

- Accounting 404BDocument2 pagesAccounting 404BMelicah Chantel SantosNo ratings yet

- Shareholders' Equity: Intermediate Accounting 3Document22 pagesShareholders' Equity: Intermediate Accounting 3Aga Mathew Mayuga100% (1)

- Ia1 5a Investments 15 FVDocument55 pagesIa1 5a Investments 15 FVJm SevallaNo ratings yet

- Chapter 2Document12 pagesChapter 2Cassandra KarolinaNo ratings yet

- Break-Even Analysis: Cost-Volume-Profit AnalysisDocument64 pagesBreak-Even Analysis: Cost-Volume-Profit AnalysisKelvin LeongNo ratings yet

- Week 4 - Lesson 4 Cash and Cash EquivalentsDocument21 pagesWeek 4 - Lesson 4 Cash and Cash EquivalentsRose RaboNo ratings yet

- CAE 10 CG Strategic Cost ManagementDocument23 pagesCAE 10 CG Strategic Cost ManagementAmie Jane MirandaNo ratings yet

- Exam in Accounting-FinalsDocument5 pagesExam in Accounting-FinalsIyarna YasraNo ratings yet

- PUP Review Handout 1 OfficialDocument3 pagesPUP Review Handout 1 OfficialDonalyn CalipusNo ratings yet

- As 12 - Full Notes For Accounting For Government GrantDocument6 pagesAs 12 - Full Notes For Accounting For Government GrantShrey KunjNo ratings yet

- Quali - ReviewDocument32 pagesQuali - ReviewLA M AENo ratings yet

- 2nd Sem 2021 Acctg 5a NCADocument7 pages2nd Sem 2021 Acctg 5a NCARUNEL J. PACOTNo ratings yet

- Investment in Equity Securities Intacc1Document3 pagesInvestment in Equity Securities Intacc1GIRLNo ratings yet

- Borrowing Costs That Are Directly Attributable To The Acquisition, Construction orDocument4 pagesBorrowing Costs That Are Directly Attributable To The Acquisition, Construction orJustine VeralloNo ratings yet

- Direct Method or Cost of Goods Sold MethodDocument2 pagesDirect Method or Cost of Goods Sold MethodNa Dem DolotallasNo ratings yet

- Management Accounting: Instructors' ManualDocument11 pagesManagement Accounting: Instructors' ManualJane Michelle EmanNo ratings yet

- Chapter 25: Property, Plant & Equipment: Gross MethodDocument17 pagesChapter 25: Property, Plant & Equipment: Gross MethodJohnPaulDMirasolNo ratings yet

- Module 3 - Compound Financial Instruments and Debt RestructuringDocument21 pagesModule 3 - Compound Financial Instruments and Debt RestructuringAga Mathew MayugaNo ratings yet

- Financial InstrumentsDocument93 pagesFinancial InstrumentsLuisa Janelle BoquirenNo ratings yet

- PFRS 3, Business CombinationsDocument39 pagesPFRS 3, Business Combinationsjulia4razoNo ratings yet

- Aud Prob Part 1Document106 pagesAud Prob Part 1Ma. Hazel Donita DiazNo ratings yet

- Accrued Liabilities: Problem 3-1 (AICPA Adapted)Document15 pagesAccrued Liabilities: Problem 3-1 (AICPA Adapted)Nila FranciaNo ratings yet

- Postemployment BenefitsDocument3 pagesPostemployment BenefitsChristian John PardoNo ratings yet

- Cash & Cash Equivalents Composition & Other Topics CashDocument5 pagesCash & Cash Equivalents Composition & Other Topics CashEurich Gibarr Gavina EstradaNo ratings yet

- June 9-Acquisition of PPEDocument2 pagesJune 9-Acquisition of PPEJolo RomanNo ratings yet

- Chapter 33 - Financial Asset at Amortized Cost (Fair Value Option)Document1 pageChapter 33 - Financial Asset at Amortized Cost (Fair Value Option)Ianna ManieboNo ratings yet

- Working Capital and CashDocument41 pagesWorking Capital and CashasunaNo ratings yet

- Financial Assets at Fair Value (Investments) Basic ConceptsDocument2 pagesFinancial Assets at Fair Value (Investments) Basic ConceptsMonica Monica0% (1)

- Module 12 PAS 36Document6 pagesModule 12 PAS 36Jan JanNo ratings yet

- Chapter 29 SheDocument126 pagesChapter 29 SheAiraNo ratings yet

- Jamolod - Unit 1 - General Features of Financial StatementDocument8 pagesJamolod - Unit 1 - General Features of Financial StatementJatha JamolodNo ratings yet

- First Time Adoption of PFRSDocument5 pagesFirst Time Adoption of PFRSPia ArellanoNo ratings yet

- Employee Benefits P201Document17 pagesEmployee Benefits P201krisha milloNo ratings yet

- Fostering CommitmentDocument11 pagesFostering CommitmentLeah VeralloNo ratings yet

- Intangibles and Wasting AssetDocument8 pagesIntangibles and Wasting AssetVandix100% (1)

- 0f926440 1614316682621Document20 pages0f926440 1614316682621Abby NavarroNo ratings yet

- Activities - Cash Payments To Acquire PropertyDocument2 pagesActivities - Cash Payments To Acquire PropertyPrecious ViterboNo ratings yet

- M1 Introduction To Transfer Taxaion Students PDFDocument20 pagesM1 Introduction To Transfer Taxaion Students PDFTokis SabaNo ratings yet

- Accounting For Income Tax: Technical KnowledgeDocument42 pagesAccounting For Income Tax: Technical KnowledgeAngela Miles DizonNo ratings yet

- Investments 1 PDFDocument98 pagesInvestments 1 PDFAbby NavarroNo ratings yet

- Chapter 17 - Financial Asset at Amortized CostDocument2 pagesChapter 17 - Financial Asset at Amortized Costlooter198100% (1)

- Chapter 18 Shareholders Equity - Docx-1Document14 pagesChapter 18 Shareholders Equity - Docx-1kanroji1923No ratings yet

- Ch08 Property, Plant & EquipmentDocument6 pagesCh08 Property, Plant & EquipmentralphalonzoNo ratings yet

- Multiple Choice Questions 1 A Method That Excludes Residual Value FromDocument1 pageMultiple Choice Questions 1 A Method That Excludes Residual Value FromHassan JanNo ratings yet

- Chapter 3 Corporate Liquidation and Reorganization-PROFE01Document3 pagesChapter 3 Corporate Liquidation and Reorganization-PROFE01Steffany RoqueNo ratings yet

- Chapter 5Document11 pagesChapter 5Ro-Anne LozadaNo ratings yet

- ToA - 03 - Inventories - StudentDocument7 pagesToA - 03 - Inventories - StudentAce Desabille100% (1)

- Chapter 21 - Reclassification of Financial Asset PDFDocument9 pagesChapter 21 - Reclassification of Financial Asset PDFTurksNo ratings yet

- Statement of Comprehensive Income: Irene Mae C. Guerra, CPA, CTTDocument21 pagesStatement of Comprehensive Income: Irene Mae C. Guerra, CPA, CTTRuaya AilynNo ratings yet

- 4 Probability AnalysisDocument11 pages4 Probability AnalysisLyca TudtudNo ratings yet

- 2 Inventory Cost Flow Intermediate Accounting ReviewerDocument3 pages2 Inventory Cost Flow Intermediate Accounting ReviewerDalia ElarabyNo ratings yet

- Discounting Notes ReceivableDocument3 pagesDiscounting Notes ReceivablerockerNo ratings yet

- Reviewer - Accounting FOR Labor Reviewer - Accounting FOR LaborDocument3 pagesReviewer - Accounting FOR Labor Reviewer - Accounting FOR LaborJuan FrivaldoNo ratings yet

- IntAcc 3 Non-Financial LiabilitiesDocument10 pagesIntAcc 3 Non-Financial LiabilitiesKim EllaNo ratings yet

- Fund Flow:: Working CapitalDocument19 pagesFund Flow:: Working CapitalAlex JayachandranNo ratings yet

- Republic of The Philippines Court of Tax Appeals Quezon CityDocument27 pagesRepublic of The Philippines Court of Tax Appeals Quezon CityalyssaNo ratings yet

- AudTheo Salosagcol 2018ed Ansv1Document13 pagesAudTheo Salosagcol 2018ed Ansv1alyssaNo ratings yet

- Chapter 6 - EntrepreneurshipDocument21 pagesChapter 6 - EntrepreneurshipalyssaNo ratings yet

- Cta Eb CV 01024 M 2016mar09 AssDocument9 pagesCta Eb CV 01024 M 2016mar09 AssalyssaNo ratings yet

- Republic of The Philippines Court of Tax Appeals Quezon CityDocument19 pagesRepublic of The Philippines Court of Tax Appeals Quezon CityalyssaNo ratings yet

- Republic of The Philippines Court of Tax Appeals Quezon CityDocument31 pagesRepublic of The Philippines Court of Tax Appeals Quezon CityalyssaNo ratings yet

- Republic of Philippines Court of Tax Appeals Quezon City: Archipelago Motor No. 1258Document12 pagesRepublic of Philippines Court of Tax Appeals Quezon City: Archipelago Motor No. 1258alyssaNo ratings yet

- Enbanc: Republic of The Philippines Court of Tax Appeals Quezon CityDocument10 pagesEnbanc: Republic of The Philippines Court of Tax Appeals Quezon CityalyssaNo ratings yet

- Enbanc: Republic of The Philippines Court of Tax Appeals QuezonDocument5 pagesEnbanc: Republic of The Philippines Court of Tax Appeals QuezonalyssaNo ratings yet

- Court Oft Ax Appeals: en BaneDocument6 pagesCourt Oft Ax Appeals: en BanealyssaNo ratings yet

- Business PlanDocument38 pagesBusiness PlanHONEY SHEN BULADACONo ratings yet

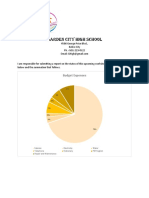

- Garden City High School: Budget ExpensesDocument3 pagesGarden City High School: Budget ExpensesKyjuan T. KingNo ratings yet

- Cash Requirements For A Small StartupDocument12 pagesCash Requirements For A Small StartupArturo VillaseñorNo ratings yet

- Secretarial Compliance Certificate RulesDocument6 pagesSecretarial Compliance Certificate RulesjdonNo ratings yet

- Mehta Auto MobilesDocument1 pageMehta Auto MobilesAman Pandey100% (1)

- Brown POQDocument4 pagesBrown POQJonas GonzalesNo ratings yet

- Deccan Cements - Rating Rationale PDFDocument6 pagesDeccan Cements - Rating Rationale PDFAkashNo ratings yet

- NFJPIA - Mockboard 2011 - AP PDFDocument6 pagesNFJPIA - Mockboard 2011 - AP PDFaizaNo ratings yet

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument7 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalancesknagarNo ratings yet

- 1.covering MaybankDocument1 page1.covering MaybankNgan ThaoNo ratings yet

- IDFC Indian Infrastructure - ChallengesDocument18 pagesIDFC Indian Infrastructure - ChallengesSudarshan SubhashNo ratings yet

- Inbt211 ReviewerDocument13 pagesInbt211 ReviewerSydney Miles MahinayNo ratings yet

- Mmo Most Important Question SolutionDocument4 pagesMmo Most Important Question SolutionAshish GoelNo ratings yet

- Money (Part II) Please Go Over The Following Terms and Their DefinitionsDocument4 pagesMoney (Part II) Please Go Over The Following Terms and Their DefinitionsDelia LupascuNo ratings yet

- Taussig, Principles of Economics, Vol. 1Document600 pagesTaussig, Principles of Economics, Vol. 1quintus14100% (1)

- Career Camp May22 Training AgreementDocument15 pagesCareer Camp May22 Training AgreementSudhanshu Shekhar SinglaNo ratings yet

- CIR V Central LuzonDocument2 pagesCIR V Central LuzonAgnes FranciscoNo ratings yet

- Customer Journey Non LienDocument9 pagesCustomer Journey Non LienaslamzohaibNo ratings yet

- R.A Act No.1400 Land Reform Act of 1955Document8 pagesR.A Act No.1400 Land Reform Act of 1955Nadine FrogosoNo ratings yet

- E Stamping Application FormDocument4 pagesE Stamping Application FormSales & Marketing Residential & CommercialNo ratings yet

- MGT201 Final Term Subjective Solved With Reference 2014Document18 pagesMGT201 Final Term Subjective Solved With Reference 2014maryamNo ratings yet

- Department of Finance Budget PresentationDocument9 pagesDepartment of Finance Budget PresentationWVXU NewsNo ratings yet

- LISING RemDocument5 pagesLISING RemEduard MantacNo ratings yet

- A Study of Financial Derivatives (Futures and Options)Document128 pagesA Study of Financial Derivatives (Futures and Options)tanvirNo ratings yet

- Christ (Deemed To Be University) School of Business and Management Assignment BriefDocument5 pagesChrist (Deemed To Be University) School of Business and Management Assignment BriefLatha JosephNo ratings yet

- Intermediate Accounting Vol 1 Canadian 3Rd Edition Lo Test Bank Full Chapter PDFDocument68 pagesIntermediate Accounting Vol 1 Canadian 3Rd Edition Lo Test Bank Full Chapter PDFwilliambrowntdoypjmnrc100% (12)

- Module 35 BV Per Share and Quasi TheoryDocument2 pagesModule 35 BV Per Share and Quasi TheoryThalia UyNo ratings yet

- Transaction History c08Document1 pageTransaction History c08Nabiel RHNo ratings yet

- Bookshop Business PlanDocument29 pagesBookshop Business PlanAbdullah Al-RafiNo ratings yet

Download as pdf or txt

You might also like

- Accounting For Biological Assets: ObjectivesDocument14 pagesAccounting For Biological Assets: Objectivesrajmeet75% (4)

- Amex STMTDocument1 pageAmex STMTMark GalantyNo ratings yet

- Investment in Equity SecuritiesDocument3 pagesInvestment in Equity Securitiesmiss independentNo ratings yet

- Statement of Financial PositionDocument36 pagesStatement of Financial PositionAbdulmajed Unda MimbantasNo ratings yet

- Shareholders' Equity - Contributed Capital: Part A: The Nature of Shareholders' Equity I. Sources of Shareholders' EquityDocument12 pagesShareholders' Equity - Contributed Capital: Part A: The Nature of Shareholders' Equity I. Sources of Shareholders' Equitycriszel4sobejanaNo ratings yet

- Far Eastern University - Makati: Discussion ProblemsDocument2 pagesFar Eastern University - Makati: Discussion ProblemsMarielle SidayonNo ratings yet

- Accounting 404BDocument2 pagesAccounting 404BMelicah Chantel SantosNo ratings yet

- Shareholders' Equity: Intermediate Accounting 3Document22 pagesShareholders' Equity: Intermediate Accounting 3Aga Mathew Mayuga100% (1)

- Ia1 5a Investments 15 FVDocument55 pagesIa1 5a Investments 15 FVJm SevallaNo ratings yet

- Chapter 2Document12 pagesChapter 2Cassandra KarolinaNo ratings yet

- Break-Even Analysis: Cost-Volume-Profit AnalysisDocument64 pagesBreak-Even Analysis: Cost-Volume-Profit AnalysisKelvin LeongNo ratings yet

- Week 4 - Lesson 4 Cash and Cash EquivalentsDocument21 pagesWeek 4 - Lesson 4 Cash and Cash EquivalentsRose RaboNo ratings yet

- CAE 10 CG Strategic Cost ManagementDocument23 pagesCAE 10 CG Strategic Cost ManagementAmie Jane MirandaNo ratings yet

- Exam in Accounting-FinalsDocument5 pagesExam in Accounting-FinalsIyarna YasraNo ratings yet

- PUP Review Handout 1 OfficialDocument3 pagesPUP Review Handout 1 OfficialDonalyn CalipusNo ratings yet

- As 12 - Full Notes For Accounting For Government GrantDocument6 pagesAs 12 - Full Notes For Accounting For Government GrantShrey KunjNo ratings yet

- Quali - ReviewDocument32 pagesQuali - ReviewLA M AENo ratings yet

- 2nd Sem 2021 Acctg 5a NCADocument7 pages2nd Sem 2021 Acctg 5a NCARUNEL J. PACOTNo ratings yet

- Investment in Equity Securities Intacc1Document3 pagesInvestment in Equity Securities Intacc1GIRLNo ratings yet

- Borrowing Costs That Are Directly Attributable To The Acquisition, Construction orDocument4 pagesBorrowing Costs That Are Directly Attributable To The Acquisition, Construction orJustine VeralloNo ratings yet

- Direct Method or Cost of Goods Sold MethodDocument2 pagesDirect Method or Cost of Goods Sold MethodNa Dem DolotallasNo ratings yet

- Management Accounting: Instructors' ManualDocument11 pagesManagement Accounting: Instructors' ManualJane Michelle EmanNo ratings yet

- Chapter 25: Property, Plant & Equipment: Gross MethodDocument17 pagesChapter 25: Property, Plant & Equipment: Gross MethodJohnPaulDMirasolNo ratings yet

- Module 3 - Compound Financial Instruments and Debt RestructuringDocument21 pagesModule 3 - Compound Financial Instruments and Debt RestructuringAga Mathew MayugaNo ratings yet

- Financial InstrumentsDocument93 pagesFinancial InstrumentsLuisa Janelle BoquirenNo ratings yet

- PFRS 3, Business CombinationsDocument39 pagesPFRS 3, Business Combinationsjulia4razoNo ratings yet

- Aud Prob Part 1Document106 pagesAud Prob Part 1Ma. Hazel Donita DiazNo ratings yet

- Accrued Liabilities: Problem 3-1 (AICPA Adapted)Document15 pagesAccrued Liabilities: Problem 3-1 (AICPA Adapted)Nila FranciaNo ratings yet

- Postemployment BenefitsDocument3 pagesPostemployment BenefitsChristian John PardoNo ratings yet

- Cash & Cash Equivalents Composition & Other Topics CashDocument5 pagesCash & Cash Equivalents Composition & Other Topics CashEurich Gibarr Gavina EstradaNo ratings yet

- June 9-Acquisition of PPEDocument2 pagesJune 9-Acquisition of PPEJolo RomanNo ratings yet

- Chapter 33 - Financial Asset at Amortized Cost (Fair Value Option)Document1 pageChapter 33 - Financial Asset at Amortized Cost (Fair Value Option)Ianna ManieboNo ratings yet

- Working Capital and CashDocument41 pagesWorking Capital and CashasunaNo ratings yet

- Financial Assets at Fair Value (Investments) Basic ConceptsDocument2 pagesFinancial Assets at Fair Value (Investments) Basic ConceptsMonica Monica0% (1)

- Module 12 PAS 36Document6 pagesModule 12 PAS 36Jan JanNo ratings yet

- Chapter 29 SheDocument126 pagesChapter 29 SheAiraNo ratings yet

- Jamolod - Unit 1 - General Features of Financial StatementDocument8 pagesJamolod - Unit 1 - General Features of Financial StatementJatha JamolodNo ratings yet

- First Time Adoption of PFRSDocument5 pagesFirst Time Adoption of PFRSPia ArellanoNo ratings yet

- Employee Benefits P201Document17 pagesEmployee Benefits P201krisha milloNo ratings yet

- Fostering CommitmentDocument11 pagesFostering CommitmentLeah VeralloNo ratings yet

- Intangibles and Wasting AssetDocument8 pagesIntangibles and Wasting AssetVandix100% (1)

- 0f926440 1614316682621Document20 pages0f926440 1614316682621Abby NavarroNo ratings yet

- Activities - Cash Payments To Acquire PropertyDocument2 pagesActivities - Cash Payments To Acquire PropertyPrecious ViterboNo ratings yet

- M1 Introduction To Transfer Taxaion Students PDFDocument20 pagesM1 Introduction To Transfer Taxaion Students PDFTokis SabaNo ratings yet

- Accounting For Income Tax: Technical KnowledgeDocument42 pagesAccounting For Income Tax: Technical KnowledgeAngela Miles DizonNo ratings yet

- Investments 1 PDFDocument98 pagesInvestments 1 PDFAbby NavarroNo ratings yet

- Chapter 17 - Financial Asset at Amortized CostDocument2 pagesChapter 17 - Financial Asset at Amortized Costlooter198100% (1)

- Chapter 18 Shareholders Equity - Docx-1Document14 pagesChapter 18 Shareholders Equity - Docx-1kanroji1923No ratings yet

- Ch08 Property, Plant & EquipmentDocument6 pagesCh08 Property, Plant & EquipmentralphalonzoNo ratings yet

- Multiple Choice Questions 1 A Method That Excludes Residual Value FromDocument1 pageMultiple Choice Questions 1 A Method That Excludes Residual Value FromHassan JanNo ratings yet

- Chapter 3 Corporate Liquidation and Reorganization-PROFE01Document3 pagesChapter 3 Corporate Liquidation and Reorganization-PROFE01Steffany RoqueNo ratings yet

- Chapter 5Document11 pagesChapter 5Ro-Anne LozadaNo ratings yet

- ToA - 03 - Inventories - StudentDocument7 pagesToA - 03 - Inventories - StudentAce Desabille100% (1)

- Chapter 21 - Reclassification of Financial Asset PDFDocument9 pagesChapter 21 - Reclassification of Financial Asset PDFTurksNo ratings yet

- Statement of Comprehensive Income: Irene Mae C. Guerra, CPA, CTTDocument21 pagesStatement of Comprehensive Income: Irene Mae C. Guerra, CPA, CTTRuaya AilynNo ratings yet

- 4 Probability AnalysisDocument11 pages4 Probability AnalysisLyca TudtudNo ratings yet

- 2 Inventory Cost Flow Intermediate Accounting ReviewerDocument3 pages2 Inventory Cost Flow Intermediate Accounting ReviewerDalia ElarabyNo ratings yet

- Discounting Notes ReceivableDocument3 pagesDiscounting Notes ReceivablerockerNo ratings yet

- Reviewer - Accounting FOR Labor Reviewer - Accounting FOR LaborDocument3 pagesReviewer - Accounting FOR Labor Reviewer - Accounting FOR LaborJuan FrivaldoNo ratings yet

- IntAcc 3 Non-Financial LiabilitiesDocument10 pagesIntAcc 3 Non-Financial LiabilitiesKim EllaNo ratings yet

- Fund Flow:: Working CapitalDocument19 pagesFund Flow:: Working CapitalAlex JayachandranNo ratings yet

- Republic of The Philippines Court of Tax Appeals Quezon CityDocument27 pagesRepublic of The Philippines Court of Tax Appeals Quezon CityalyssaNo ratings yet

- AudTheo Salosagcol 2018ed Ansv1Document13 pagesAudTheo Salosagcol 2018ed Ansv1alyssaNo ratings yet

- Chapter 6 - EntrepreneurshipDocument21 pagesChapter 6 - EntrepreneurshipalyssaNo ratings yet

- Cta Eb CV 01024 M 2016mar09 AssDocument9 pagesCta Eb CV 01024 M 2016mar09 AssalyssaNo ratings yet

- Republic of The Philippines Court of Tax Appeals Quezon CityDocument19 pagesRepublic of The Philippines Court of Tax Appeals Quezon CityalyssaNo ratings yet

- Republic of The Philippines Court of Tax Appeals Quezon CityDocument31 pagesRepublic of The Philippines Court of Tax Appeals Quezon CityalyssaNo ratings yet

- Republic of Philippines Court of Tax Appeals Quezon City: Archipelago Motor No. 1258Document12 pagesRepublic of Philippines Court of Tax Appeals Quezon City: Archipelago Motor No. 1258alyssaNo ratings yet

- Enbanc: Republic of The Philippines Court of Tax Appeals Quezon CityDocument10 pagesEnbanc: Republic of The Philippines Court of Tax Appeals Quezon CityalyssaNo ratings yet

- Enbanc: Republic of The Philippines Court of Tax Appeals QuezonDocument5 pagesEnbanc: Republic of The Philippines Court of Tax Appeals QuezonalyssaNo ratings yet

- Court Oft Ax Appeals: en BaneDocument6 pagesCourt Oft Ax Appeals: en BanealyssaNo ratings yet

- Business PlanDocument38 pagesBusiness PlanHONEY SHEN BULADACONo ratings yet

- Garden City High School: Budget ExpensesDocument3 pagesGarden City High School: Budget ExpensesKyjuan T. KingNo ratings yet

- Cash Requirements For A Small StartupDocument12 pagesCash Requirements For A Small StartupArturo VillaseñorNo ratings yet

- Secretarial Compliance Certificate RulesDocument6 pagesSecretarial Compliance Certificate RulesjdonNo ratings yet

- Mehta Auto MobilesDocument1 pageMehta Auto MobilesAman Pandey100% (1)

- Brown POQDocument4 pagesBrown POQJonas GonzalesNo ratings yet

- Deccan Cements - Rating Rationale PDFDocument6 pagesDeccan Cements - Rating Rationale PDFAkashNo ratings yet

- NFJPIA - Mockboard 2011 - AP PDFDocument6 pagesNFJPIA - Mockboard 2011 - AP PDFaizaNo ratings yet

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument7 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalancesknagarNo ratings yet

- 1.covering MaybankDocument1 page1.covering MaybankNgan ThaoNo ratings yet

- IDFC Indian Infrastructure - ChallengesDocument18 pagesIDFC Indian Infrastructure - ChallengesSudarshan SubhashNo ratings yet

- Inbt211 ReviewerDocument13 pagesInbt211 ReviewerSydney Miles MahinayNo ratings yet

- Mmo Most Important Question SolutionDocument4 pagesMmo Most Important Question SolutionAshish GoelNo ratings yet

- Money (Part II) Please Go Over The Following Terms and Their DefinitionsDocument4 pagesMoney (Part II) Please Go Over The Following Terms and Their DefinitionsDelia LupascuNo ratings yet

- Taussig, Principles of Economics, Vol. 1Document600 pagesTaussig, Principles of Economics, Vol. 1quintus14100% (1)

- Career Camp May22 Training AgreementDocument15 pagesCareer Camp May22 Training AgreementSudhanshu Shekhar SinglaNo ratings yet

- CIR V Central LuzonDocument2 pagesCIR V Central LuzonAgnes FranciscoNo ratings yet

- Customer Journey Non LienDocument9 pagesCustomer Journey Non LienaslamzohaibNo ratings yet

- R.A Act No.1400 Land Reform Act of 1955Document8 pagesR.A Act No.1400 Land Reform Act of 1955Nadine FrogosoNo ratings yet

- E Stamping Application FormDocument4 pagesE Stamping Application FormSales & Marketing Residential & CommercialNo ratings yet

- MGT201 Final Term Subjective Solved With Reference 2014Document18 pagesMGT201 Final Term Subjective Solved With Reference 2014maryamNo ratings yet

- Department of Finance Budget PresentationDocument9 pagesDepartment of Finance Budget PresentationWVXU NewsNo ratings yet

- LISING RemDocument5 pagesLISING RemEduard MantacNo ratings yet

- A Study of Financial Derivatives (Futures and Options)Document128 pagesA Study of Financial Derivatives (Futures and Options)tanvirNo ratings yet

- Christ (Deemed To Be University) School of Business and Management Assignment BriefDocument5 pagesChrist (Deemed To Be University) School of Business and Management Assignment BriefLatha JosephNo ratings yet

- Intermediate Accounting Vol 1 Canadian 3Rd Edition Lo Test Bank Full Chapter PDFDocument68 pagesIntermediate Accounting Vol 1 Canadian 3Rd Edition Lo Test Bank Full Chapter PDFwilliambrowntdoypjmnrc100% (12)

- Module 35 BV Per Share and Quasi TheoryDocument2 pagesModule 35 BV Per Share and Quasi TheoryThalia UyNo ratings yet

- Transaction History c08Document1 pageTransaction History c08Nabiel RHNo ratings yet

- Bookshop Business PlanDocument29 pagesBookshop Business PlanAbdullah Al-RafiNo ratings yet