Download as pdf or txt

You might also like

- Series 65 Exam Practice Question Workbook: 700+ Comprehensive Practice Questions (2023 Edition)From EverandSeries 65 Exam Practice Question Workbook: 700+ Comprehensive Practice Questions (2023 Edition)No ratings yet

- T.S. Grewal Book Part 3Document189 pagesT.S. Grewal Book Part 3Thami K96% (25)

- Chapter 7 Notes Question Amp SolutionsDocument7 pagesChapter 7 Notes Question Amp SolutionsPankhuri SinghalNo ratings yet

- 74618bos60479 FND cp7 Annex1Document17 pages74618bos60479 FND cp7 Annex1rajdeepsingh886691No ratings yet

- Assignment 4: PART 1 - Balance SheetDocument3 pagesAssignment 4: PART 1 - Balance SheetGauravTiwariNo ratings yet

- Form 060503Document5 pagesForm 060503deepakgupta.arNo ratings yet

- PT B Acc NotesDocument7 pagesPT B Acc Notesfathima hamnaNo ratings yet

- Summary of IVth Schedule - Companies Ordinance 1984Document17 pagesSummary of IVth Schedule - Companies Ordinance 1984Platonic50% (2)

- Attachments - Rainbow RowellDocument29 pagesAttachments - Rainbow RowellAlvin Yerc0% (1)

- Comparative Schedule VIDocument23 pagesComparative Schedule VIRajkumar MathurNo ratings yet

- Pas 32Document19 pagesPas 32abeladelmundosuarezNo ratings yet

- Financial Instrument NotesDocument3 pagesFinancial Instrument NotesKrishna AdhikariNo ratings yet

- Far210 Topic 4 MFRS 9 ReceivablesDocument83 pagesFar210 Topic 4 MFRS 9 ReceivablesNUR AYUNI BALQISH AHMAD MULIADINo ratings yet

- Contemproray AccountingDocument15 pagesContemproray Accountingprathamprabhakar100No ratings yet

- Gen 009 P1 ReviewerDocument2 pagesGen 009 P1 ReviewerShane QuintoNo ratings yet

- Financial InstrumentsDocument13 pagesFinancial InstrumentsMarvin MercadoNo ratings yet

- On Sch-III Ucc - Division-IDocument58 pagesOn Sch-III Ucc - Division-IAman MiddhaNo ratings yet

- FAR.2830 Financial Liabilities Summary DIY.Document7 pagesFAR.2830 Financial Liabilities Summary DIY.Lynssej BarbonNo ratings yet

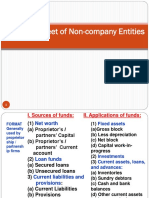

- Balance Sheet of Non-Company EntitiesDocument31 pagesBalance Sheet of Non-Company EntitiesChevuri Sudha MohanNo ratings yet

- Final Accounts of CompaniesDocument67 pagesFinal Accounts of Companiesnemewep527No ratings yet

- SV. Topic 2. Cong Cu Tai ChinhDocument123 pagesSV. Topic 2. Cong Cu Tai Chinhmaily08061507No ratings yet

- Final Accounts of CompaniesDocument66 pagesFinal Accounts of CompaniesLakshmi Sowjanya AkurathiNo ratings yet

- Chapter 2 - FI-ADocument43 pagesChapter 2 - FI-AKhanh LinhNo ratings yet

- Financial Accounting 3 ConceptsDocument8 pagesFinancial Accounting 3 ConceptsWafah HadjisalicNo ratings yet

- FAR.2926 Financial Assets Summary DIY PDFDocument11 pagesFAR.2926 Financial Assets Summary DIY PDFNah HamzaNo ratings yet

- A. B. Money Orders C.: D. IousDocument10 pagesA. B. Money Orders C.: D. IousRobert GarlandNo ratings yet

- Cfas 2ND Term Finals PDFDocument16 pagesCfas 2ND Term Finals PDFPam LlanetaNo ratings yet

- Exercise 6 - 1 Multiple Choice QuestionsDocument3 pagesExercise 6 - 1 Multiple Choice QuestionsYrica100% (1)

- Issue of Debentures (H.W)Document8 pagesIssue of Debentures (H.W)krisshlohia5No ratings yet

- Revised Schedule VIDocument89 pagesRevised Schedule VIChirag MalhotraNo ratings yet

- Excel 01Document6 pagesExcel 01shivamsahniji750No ratings yet

- Quiz No. 06: Financial InstrumentsDocument2 pagesQuiz No. 06: Financial InstrumentsPHI NGUYEN HOANGNo ratings yet

- Ts GrewalDocument92 pagesTs GrewalShyamal NarangNo ratings yet

- Book 3 CH 1Document5 pagesBook 3 CH 1TanayNo ratings yet

- Scdedule IIIDocument4 pagesScdedule IIIAryan VermaNo ratings yet

- Financial Asset at Fair Value - 1S - SY1819 PDFDocument3 pagesFinancial Asset at Fair Value - 1S - SY1819 PDFPea Del Monte AñanaNo ratings yet

- Company Accounts-Issue of Debentures: Meaning of Key Terms Used in The ChapterDocument9 pagesCompany Accounts-Issue of Debentures: Meaning of Key Terms Used in The ChapterKanakpreetNo ratings yet

- Seatwork 02 InvestmentsDocument2 pagesSeatwork 02 InvestmentsJella Mae YcalinaNo ratings yet

- Chapter 11 - Disclosure RequirementDocument22 pagesChapter 11 - Disclosure Requirementhitendrapatil6778No ratings yet

- (D) The Liability Is Payable To A Specifically Identified PayeeDocument13 pages(D) The Liability Is Payable To A Specifically Identified PayeeAngela Luz de LimaNo ratings yet

- Corporate Financial Reporting: Preparing and Understanding Balance SheetDocument76 pagesCorporate Financial Reporting: Preparing and Understanding Balance SheetArty Drill100% (1)

- INTRODUCTION TO INVESTMENTS MaterialDocument9 pagesINTRODUCTION TO INVESTMENTS MaterialKathleen Tabasa ManuelNo ratings yet

- Issue of Debentures (Key-Terms)Document3 pagesIssue of Debentures (Key-Terms)Aman HussainNo ratings yet

- Chapter 7sDocument96 pagesChapter 7ssgangwar2005sgNo ratings yet

- Review 105 - Day 10 Theory of AccountsDocument11 pagesReview 105 - Day 10 Theory of AccountsCharmine de la CruzNo ratings yet

- FINANCIAL INSTRUMENTS MCQNDocument3 pagesFINANCIAL INSTRUMENTS MCQNJoelo De Vera100% (1)

- Balance Sheet and Profit and Loss Account - FinalDocument20 pagesBalance Sheet and Profit and Loss Account - FinalKartikey Mishra100% (1)

- Document From Adhu-2 PDFDocument26 pagesDocument From Adhu-2 PDFBasavaraj S PNo ratings yet

- Balance Sheet of XYZ LTD.: (SRM) S R M (Fanci Dress Le Lo) (TICI) T I C IDocument4 pagesBalance Sheet of XYZ LTD.: (SRM) S R M (Fanci Dress Le Lo) (TICI) T I C ISampada Bassi100% (1)

- SV - Topic 2. Cong Cu Tai ChinhDocument56 pagesSV - Topic 2. Cong Cu Tai ChinhPhương DiNo ratings yet

- Full Ebook of Analysis of Financial Statements The Content Is From The CD Not The Book 2023 Edition Edition T S Grewal Online PDF All ChapterDocument69 pagesFull Ebook of Analysis of Financial Statements The Content Is From The CD Not The Book 2023 Edition Edition T S Grewal Online PDF All Chaptercblliefelidae153100% (9)

- 18.liquidation of Companies PDFDocument6 pages18.liquidation of Companies PDFAngelinaGupta50% (2)

- Chapter 21 Financial Instruments (Students)Document49 pagesChapter 21 Financial Instruments (Students)Kelvin Chu JYNo ratings yet

- Accounts ReceivableDocument43 pagesAccounts ReceivableZee 24No ratings yet

- Com203 - Final Accounts of Insurance CompaniesDocument23 pagesCom203 - Final Accounts of Insurance CompaniesSanaullah M SultanpurNo ratings yet

- Key-Terms and Chapter Summary-1Document11 pagesKey-Terms and Chapter Summary-1Neel DudhatNo ratings yet

- FinancialInstruments IARev RLPDocument1 pageFinancialInstruments IARev RLPBrian Daniel BayotNo ratings yet

- Current LiabilitiesDocument2 pagesCurrent LiabilitiesAvox EverdeenNo ratings yet

- Financial Instruments: Classification, Recognition and MeasurementDocument105 pagesFinancial Instruments: Classification, Recognition and MeasurementĐỗ Thụy Minh ThưNo ratings yet

- Revised Schedule VI RequirementsDocument23 pagesRevised Schedule VI RequirementsBharadwaj GollapudiNo ratings yet

- MA 2.1-Financial StatementDocument57 pagesMA 2.1-Financial Statementvini2710100% (1)

- Stock Beta Value Retuen Capm X 0 5.50% 5.5 y 1.25 23% 11.5 Z - 0.85 7.50% 1.42 P 0.95 17% 10.06 Q 1.02 20% 10.39Document2 pagesStock Beta Value Retuen Capm X 0 5.50% 5.5 y 1.25 23% 11.5 Z - 0.85 7.50% 1.42 P 0.95 17% 10.06 Q 1.02 20% 10.39Akankshya PanigrahiNo ratings yet

- Course Outline-CF-I PDFDocument3 pagesCourse Outline-CF-I PDFAkankshya PanigrahiNo ratings yet

- Brand ArchitectureDocument15 pagesBrand ArchitectureAkankshya PanigrahiNo ratings yet

- Beta ValueDocument3 pagesBeta ValueAkankshya PanigrahiNo ratings yet

- C&maDocument96 pagesC&maAkankshya PanigrahiNo ratings yet

- Consumer PerceptionDocument5 pagesConsumer PerceptionAkankshya PanigrahiNo ratings yet

- Mba-IV-project, Appraisal, Planning & Control (12mbafm425) - NotesDocument77 pagesMba-IV-project, Appraisal, Planning & Control (12mbafm425) - Notesghostriderr29No ratings yet

- Mfis ProjectDocument46 pagesMfis ProjectHitesh SharmaNo ratings yet

- Financial Analysis of Wipro LTD PDFDocument101 pagesFinancial Analysis of Wipro LTD PDFAnonymous f7wV1lQKRNo ratings yet

- Basel Committee On Banking Supervision: MAR Calculation of RWA For Market RiskDocument187 pagesBasel Committee On Banking Supervision: MAR Calculation of RWA For Market RiskSaad RahoutiNo ratings yet

- A Study of Capital Structure ManagementDocument94 pagesA Study of Capital Structure ManagementBijaya DhakalNo ratings yet

- Advance Financial Management 1Document36 pagesAdvance Financial Management 1Indrajeet KoleNo ratings yet

- Chapter 5 Financial Decisions Capital Structure-1Document33 pagesChapter 5 Financial Decisions Capital Structure-1Aejaz MohamedNo ratings yet

- Advanced Financial Accounting Christensen 10th Edition Solutions ManualDocument42 pagesAdvanced Financial Accounting Christensen 10th Edition Solutions ManualMariaDaviesqrbg100% (44)

- HSC Business Studies FinanceDocument30 pagesHSC Business Studies FinanceUttkarsh AroraNo ratings yet

- Course Objectives: Course Name: Financial Management - 1Document4 pagesCourse Objectives: Course Name: Financial Management - 1Aninda DuttaNo ratings yet

- AbsharDocument23 pagesAbsharAbsharNo ratings yet

- How To Apply For Loan Through TiicDocument2 pagesHow To Apply For Loan Through TiicNagaraja SNo ratings yet

- Finance Topic ListDocument12 pagesFinance Topic ListAMRITHANo ratings yet

- BFM CH 31 PDFDocument21 pagesBFM CH 31 PDFAnurag SinghNo ratings yet

- MGT 201 Financial ManagementDocument93 pagesMGT 201 Financial ManagementMrs.Tariq KhanNo ratings yet

- Chapter 15 PPT - Holthausen & Zmijewski 2019Document100 pagesChapter 15 PPT - Holthausen & Zmijewski 2019royNo ratings yet

- PARTNERSHIPDocument8 pagesPARTNERSHIPShayne BenaweNo ratings yet

- Ch. 15 - Capital Structure & LeverageDocument45 pagesCh. 15 - Capital Structure & LeverageLara FloresNo ratings yet

- FMSM - Secret Superstar Notes - All in One-Executive-RevisionDocument419 pagesFMSM - Secret Superstar Notes - All in One-Executive-RevisionSiddhant SoniNo ratings yet

- REND DEED SM and KANCHAN BHATIA 2023 (8) - CompressedDocument6 pagesREND DEED SM and KANCHAN BHATIA 2023 (8) - Compressedtaxqoof1No ratings yet

- Question BankDocument18 pagesQuestion BankTitus ClementNo ratings yet

- Minor Project ReportDocument69 pagesMinor Project ReportrimpaNo ratings yet

- Dwnload Full Financial Reporting and Analysis 5th Edition Revsine Solutions Manual PDFDocument35 pagesDwnload Full Financial Reporting and Analysis 5th Edition Revsine Solutions Manual PDFinactionwantwit.a8i0100% (16)

- Philippine School of Business Administration R. Papa ST., Sampaloc, ManilaDocument15 pagesPhilippine School of Business Administration R. Papa ST., Sampaloc, ManilaNaiomi NicasioNo ratings yet

- Performance Evaluation of JP Morgan Chase Bank: Sadia ZamanDocument17 pagesPerformance Evaluation of JP Morgan Chase Bank: Sadia ZamanAjith VNo ratings yet

- Capital StuctureDocument40 pagesCapital Stuctureridhib100% (2)

- Module - 2 Informal Risk Capital & Venture CapitalDocument26 pagesModule - 2 Informal Risk Capital & Venture Capitalpvsagar2001No ratings yet

- Accounts Assignment - Accounting RatiosDocument12 pagesAccounts Assignment - Accounting RatiosnovairafNo ratings yet

- Capital StructureDocument2 pagesCapital StructureSahil RupaniNo ratings yet