Download as pdf or txt

You might also like

- BIR Ruling (DA - (C-005) 023-08) (Condonation of Debt)Document5 pagesBIR Ruling (DA - (C-005) 023-08) (Condonation of Debt)Archie Guevarra100% (3)

- M32 5G InvoiceDocument1 pageM32 5G InvoiceYugam VermaNo ratings yet

- Elective Ourse in Commerce ECO-11 Elements of Income TaxDocument12 pagesElective Ourse in Commerce ECO-11 Elements of Income TaxJai GorakhNo ratings yet

- Tax Laws Practice New Syl Lab Us 06032024Document54 pagesTax Laws Practice New Syl Lab Us 06032024coolboydeepak4No ratings yet

- 51198bos40905 cp4 PDFDocument41 pages51198bos40905 cp4 PDFShubham VyasNo ratings yet

- Bos 32722 P 4Document37 pagesBos 32722 P 4CmaChanduNo ratings yet

- Etd 2012 3 17 37Document1 pageEtd 2012 3 17 37nosdam7No ratings yet

- S - Viii: Bba - LL.B (Hons) Corporate LawsDocument20 pagesS - Viii: Bba - LL.B (Hons) Corporate LawsSalonee NayakNo ratings yet

- Part I: Statutory Update: © The Institute of Chartered Accountants of IndiaDocument41 pagesPart I: Statutory Update: © The Institute of Chartered Accountants of IndiaApeksha ChilwalNo ratings yet

- 43B (H)Document16 pages43B (H)anascrrNo ratings yet

- Memorandum On Federal & Provincial Finance Acts, 2017Document90 pagesMemorandum On Federal & Provincial Finance Acts, 2017Rehan FarhatNo ratings yet

- Tax PlanningDocument51 pagesTax PlanningSatyajeet MohantyNo ratings yet

- Income Deemed To Be Accrue or Arise in IndiaDocument17 pagesIncome Deemed To Be Accrue or Arise in IndiaVicky DNo ratings yet

- Income Deemed To Be Accrue or Arise inDocument41 pagesIncome Deemed To Be Accrue or Arise inPJ 123No ratings yet

- Tds Amendements Via Finance Bill 2020Document12 pagesTds Amendements Via Finance Bill 2020ABHISHEKNo ratings yet

- Direct Tax Proposals 2019 (No. 2) - 1Document16 pagesDirect Tax Proposals 2019 (No. 2) - 1Namita Agarwal KediaNo ratings yet

- Export of Services in GST RegimeDocument5 pagesExport of Services in GST RegimeNM JHANWAR & ASSOCIATESNo ratings yet

- CBDT Issues Thresholds For Triggering Significant Economic Presence in IndiaDocument5 pagesCBDT Issues Thresholds For Triggering Significant Economic Presence in IndiaZOYA ZAFAR SIDDIQUINo ratings yet

- ITAD BIR Ruling No. 311-14Document9 pagesITAD BIR Ruling No. 311-14cool_peachNo ratings yet

- Union Budget 2013-14 - Highlights of Direct Tax ProposalsDocument5 pagesUnion Budget 2013-14 - Highlights of Direct Tax Proposalsankit403No ratings yet

- OL 4 - BLT Study Text Suppliment 2021 - On New Tax AmmendmentsDocument28 pagesOL 4 - BLT Study Text Suppliment 2021 - On New Tax Ammendmentshte19031No ratings yet

- Tax Memorandum 2011finalDocument42 pagesTax Memorandum 2011finalbazitNo ratings yet

- Special Economic ZoneDocument4 pagesSpecial Economic ZoneDhruvesh ModiNo ratings yet

- BDO Budget Snapshot - 2012-13Document9 pagesBDO Budget Snapshot - 2012-13Pulluri Ravikumar YugandarNo ratings yet

- Part I: Statutory Update: © The Institute of Chartered Accountants of IndiaDocument4 pagesPart I: Statutory Update: © The Institute of Chartered Accountants of IndiaRamanNo ratings yet

- Nov 2019Document39 pagesNov 2019amitha g.sNo ratings yet

- Exemption 10AA Notes-1Document9 pagesExemption 10AA Notes-1SanaNo ratings yet

- Ey Budget Connect 2023 Start UpsDocument6 pagesEy Budget Connect 2023 Start Upsgv.vidyadharNo ratings yet

- Limitation On Interest Deduction (Section 94B of Income Tax Act, 1961)Document9 pagesLimitation On Interest Deduction (Section 94B of Income Tax Act, 1961)Taxpert Professionals Private LimitedNo ratings yet

- RSM India Union Budget 2021 HighlightsDocument132 pagesRSM India Union Budget 2021 HighlightsSunil KumarNo ratings yet

- Decoding Indian Union BudgetDocument6 pagesDecoding Indian Union BudgetkumarNo ratings yet

- Benefits Available To Non ResidentsDocument16 pagesBenefits Available To Non ResidentsArchita TiwariNo ratings yet

- Amendments: May 2011 ExamsDocument13 pagesAmendments: May 2011 ExamsKanth RaaveeNo ratings yet

- 56212rtpfinaloldnov19 p7Document52 pages56212rtpfinaloldnov19 p7naveen kumarNo ratings yet

- Latest Circulars, Notifications and Press Releases: 2. This Notification Shall Come Into Force From The 1Document0 pagesLatest Circulars, Notifications and Press Releases: 2. This Notification Shall Come Into Force From The 1Ketan ThakkarNo ratings yet

- Bos 45290Document23 pagesBos 45290CA Kashish MittalNo ratings yet

- 34564rtp Nov14 Ipcc-4Document59 pages34564rtp Nov14 Ipcc-4Deepal DhamejaNo ratings yet

- Revenue Regulations No. 34-2020Document3 pagesRevenue Regulations No. 34-2020zelayneNo ratings yet

- Indirect Tax - Budget 2019Document43 pagesIndirect Tax - Budget 2019Brijesh PitrodaNo ratings yet

- FAQ On Payment of Bonus ActDocument4 pagesFAQ On Payment of Bonus Actchirag bhojakNo ratings yet

- International Taxation in India - Recent Developments & Outlook (Part - Ii)Document6 pagesInternational Taxation in India - Recent Developments & Outlook (Part - Ii)ManishJainNo ratings yet

- Tax PlanningDocument28 pagesTax PlanningDishaNo ratings yet

- Mat and Amt: Objective of Levying MATDocument17 pagesMat and Amt: Objective of Levying MATNitin ChoudharyNo ratings yet

- Income From Capital Gains (2017 IT Act)Document9 pagesIncome From Capital Gains (2017 IT Act)AjayNo ratings yet

- Mat and Amt: Objective of Levying MATDocument17 pagesMat and Amt: Objective of Levying MATSamuel AnthrayoseNo ratings yet

- GST - Input Tax Credit - Edition 5Document17 pagesGST - Input Tax Credit - Edition 5Vineet PandeyNo ratings yet

- Corporate Recovery and Tax Incentives For EnterprisesDocument5 pagesCorporate Recovery and Tax Incentives For EnterprisesIvy BoseNo ratings yet

- Corporate and Other Law Amendment Notes 1690271793Document12 pagesCorporate and Other Law Amendment Notes 1690271793AbhiNo ratings yet

- Statutory Updates For Nov-21 ExamsDocument50 pagesStatutory Updates For Nov-21 ExamsShodasakshari VidyaNo ratings yet

- Amendments: May 2011 ExamsDocument13 pagesAmendments: May 2011 ExamsshrutishindeNo ratings yet

- 53993bos43369interrtpmay19 p4 PDFDocument40 pages53993bos43369interrtpmay19 p4 PDFsaurabh feteNo ratings yet

- Special Provisions Applicable To Companies AY 2021-22Document6 pagesSpecial Provisions Applicable To Companies AY 2021-22harishragavendhra7No ratings yet

- Regional Operating Headquarters TaxDocument3 pagesRegional Operating Headquarters TaxutaknghenyoNo ratings yet

- Rates of Tax:-: Individual/HUF/AOP/Artificial Juridical PersonDocument8 pagesRates of Tax:-: Individual/HUF/AOP/Artificial Juridical PersonKiran KumarNo ratings yet

- Petron PDFDocument71 pagesPetron PDFEliza MapaNo ratings yet

- 35 FAQs On Section 43B Disallowance of The Sum Payable To Micro or Small Enterprises 35 FAQDocument11 pages35 FAQs On Section 43B Disallowance of The Sum Payable To Micro or Small Enterprises 35 FAQmvsarmaNo ratings yet

- 06 A Idt Ammentments 2 in 1Document33 pages06 A Idt Ammentments 2 in 1Venkat RamanaNo ratings yet

- Law of TaxationDocument3 pagesLaw of TaxationmangalagowrirudrappaNo ratings yet

- Direct Taxes Code 2010Document14 pagesDirect Taxes Code 2010musti_shahNo ratings yet

- Write-Up CITIRA BillDocument3 pagesWrite-Up CITIRA BillMaeJoNo ratings yet

- Budget 2018Document5 pagesBudget 2018Srushti BhattNo ratings yet

- Industrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisFrom EverandIndustrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisNo ratings yet

- Appeal Rules PDFDocument3 pagesAppeal Rules PDFManoj GuptaNo ratings yet

- Income Tax NotesDocument221 pagesIncome Tax NotesManoj GuptaNo ratings yet

- Banning of Unregulated Deposit SchemeDocument20 pagesBanning of Unregulated Deposit SchemeManoj GuptaNo ratings yet

- Volume I (BGM 16 04 2019) PDFDocument870 pagesVolume I (BGM 16 04 2019) PDFManoj GuptaNo ratings yet

- Tax Return Project - Kdiep and DivanovaDocument9 pagesTax Return Project - Kdiep and Divanovaapi-380347096No ratings yet

- IESCO Bill Safdar SBDocument2 pagesIESCO Bill Safdar SBumairsaifNo ratings yet

- Bryce 1902Document1 pageBryce 1902rusmah10No ratings yet

- Bir Form 2551Q (2018)Document2 pagesBir Form 2551Q (2018)Obin Tambasacan Baggayan33% (3)

- Train LawDocument41 pagesTrain LawJoana Lyn GalisimNo ratings yet

- Batch 3 - Taxation 1 / Atty. Dante MarananDocument9 pagesBatch 3 - Taxation 1 / Atty. Dante MarananJNo ratings yet

- Invoice Karan MBDocument1 pageInvoice Karan MBRAHUL GUPTANo ratings yet

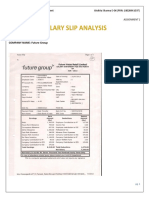

- Sector: Retail COMPANY NAME: Future GroupDocument3 pagesSector: Retail COMPANY NAME: Future GroupAkshita SharmaNo ratings yet

- Solving Equations Foundation Questions MMEDocument6 pagesSolving Equations Foundation Questions MMEZoheb RehanNo ratings yet

- PWC - Deferred Tax On Foreign SubsidiairesDocument4 pagesPWC - Deferred Tax On Foreign SubsidiairesSanath FernandoNo ratings yet

- Income Tax On Dollar To InrDocument1 pageIncome Tax On Dollar To InrApki mautNo ratings yet

- 4 Income Tax Tables Final PDFDocument8 pages4 Income Tax Tables Final PDFwilliam091090No ratings yet

- Annex C RR 11-2018Document1 pageAnnex C RR 11-2018JeZkYNo ratings yet

- FIN515 Homework1Document4 pagesFIN515 Homework1Natasha DeclanNo ratings yet

- Esa 990Document48 pagesEsa 990Brian Crecente100% (1)

- Accounting Ethic Chapter 9Document2 pagesAccounting Ethic Chapter 9nabila IkaNo ratings yet

- GST PPT TaxguruDocument30 pagesGST PPT Taxguru50raj506019No ratings yet

- AFM Capital Budgeting AssignmentDocument5 pagesAFM Capital Budgeting Assignmentmahendrabpatel100% (1)

- Offences and Penalties Under Goods and Service Tax Act 2017 - An AnalysisDocument16 pagesOffences and Penalties Under Goods and Service Tax Act 2017 - An AnalysisRupal GuptaNo ratings yet

- Solution ManualDocument30 pagesSolution ManualLakber MandNo ratings yet

- Sum On House PropertyDocument9 pagesSum On House PropertyVaishnaviNo ratings yet

- HB1465Document6 pagesHB1465Madison HardcastleNo ratings yet

- Book 1Document6 pagesBook 1Jitendra kumarNo ratings yet

- QGov Your Payslip ExplainedDocument2 pagesQGov Your Payslip ExplainedbradrimmNo ratings yet

- CHP 3Document23 pagesCHP 3Laiba SadafNo ratings yet

- VVR Spices GST 22-23-65Document1 pageVVR Spices GST 22-23-65Usha Hasini VelagapudiNo ratings yet

- Income Tax Calculator Ay 2015-16 For Resident Individuals & HufsDocument3 pagesIncome Tax Calculator Ay 2015-16 For Resident Individuals & HufsVasan GovindNo ratings yet

- Foundations of Education 12th Edition Ornstein Test BankDocument10 pagesFoundations of Education 12th Edition Ornstein Test Bankbriandung7m3e100% (36)