Download as pdf or txt

You might also like

- Bank Transfers For Beginners 2015 PDFDocument6 pagesBank Transfers For Beginners 2015 PDFPaulo Exto85% (13)

- WU Transfer Carding CircleDocument5 pagesWU Transfer Carding CircleBruce Stebbins78% (9)

- Bitcoin Carding Tutorial ?Document1 pageBitcoin Carding Tutorial ?mwaddle0% (1)

- Bypass PayPal Login Verification With 100% Working Method Phone Verification BypassDocument2 pagesBypass PayPal Login Verification With 100% Working Method Phone Verification BypassZertz Official75% (4)

- OTP Bypass Using Burp Suite: Aamir AhmadDocument4 pagesOTP Bypass Using Burp Suite: Aamir AhmadAnibal CarrascoNo ratings yet

- CC To BTCDocument1 pageCC To BTCernest issy100% (1)

- Carding Tips For Noobs - Your HackerDocument2 pagesCarding Tips For Noobs - Your HackerashuuuuuuuuuuuuuuuNo ratings yet

- Otp BypassDocument2 pagesOtp Bypassjajaj monese0% (1)

- Cvvmethods1 GuideDocument1 pageCvvmethods1 GuideJesse LarteyNo ratings yet

- CC Paypal Cashout MethodDocument1 pageCC Paypal Cashout MethodFestival ScoobyNo ratings yet

- Hacking Dominos Coupon Generator - Free Dominos Pizza Coupons & Discounts Pro HackDocument5 pagesHacking Dominos Coupon Generator - Free Dominos Pizza Coupons & Discounts Pro HackYashika Arora100% (1)

- How To Convert Paypal To Bitcoins PDFDocument3 pagesHow To Convert Paypal To Bitcoins PDFAndroid Trigger67% (3)

- UK Fire BinsDocument1 pageUK Fire BinsmwaddleNo ratings yet

- How To Get A 911.re AccountDocument17 pagesHow To Get A 911.re AccountPaul VercherNo ratings yet

- Carding Tutorial by Doodhwala Part 1Document7 pagesCarding Tutorial by Doodhwala Part 1Paul VercherNo ratings yet

- MailerDocument3 pagesMaileranon-152178100% (17)

- Continue: Fraud Bible Teejayx6 PDFDocument2 pagesContinue: Fraud Bible Teejayx6 PDFYT F1R3xS1NN3RNo ratings yet

- How To Cashout CC's With Anon Credit Card (Confirmed Working)Document1 pageHow To Cashout CC's With Anon Credit Card (Confirmed Working)Jorge MercadoNo ratings yet

- Good Paypal MethodDocument1 pageGood Paypal MethodJuan Pablo CarrascoNo ratings yet

- Quick Guide for Obtaining Free Remote Desktop Protocol (RDP) ServicesFrom EverandQuick Guide for Obtaining Free Remote Desktop Protocol (RDP) ServicesNo ratings yet

- (Group 4) 4.2.2.13 Lab - Configuring and Verifying Extended ACLsDocument8 pages(Group 4) 4.2.2.13 Lab - Configuring and Verifying Extended ACLsGlendel Carmen33% (3)

- Software Engineering IIDocument12 pagesSoftware Engineering IIM Yasin Memon100% (1)

- HOW TO HACK ALL TYPE OF WIFI Carders - Ws Carding Forum - Carders ForumDocument14 pagesHOW TO HACK ALL TYPE OF WIFI Carders - Ws Carding Forum - Carders ForumSacculus SaccNo ratings yet

- ? T&T Method ?Document1 page? T&T Method ?mwaddle100% (1)

- FreeRDP User Manual 4Document2 pagesFreeRDP User Manual 4vijayNo ratings yet

- Hacking Web PagesDocument5 pagesHacking Web Pagessrikanthm44No ratings yet

- How To Receive SMS Otp Verification Online in 5 Min. (2021)Document15 pagesHow To Receive SMS Otp Verification Online in 5 Min. (2021)dirocafNo ratings yet

- Direct Deposit Tutorial 2022Document8 pagesDirect Deposit Tutorial 2022Mario J. Neither0% (1)

- Changing The MAC AddressDocument6 pagesChanging The MAC AddressMurtuzaKazmiNo ratings yet

- Unlimited RDPDocument2 pagesUnlimited RDPHectorLaMarche100% (2)

- EKS TaxSlayer FSA - Foreign Students (Non-India)Document91 pagesEKS TaxSlayer FSA - Foreign Students (Non-India)Documentation JunkieNo ratings yet

- 51526470766Document2 pages51526470766Allen RachelNo ratings yet

- VBV FaqDocument3 pagesVBV FaqCS NarayanaNo ratings yet

- Money Making Machine 100$ Per Day Cyber. Dude PDFDocument4 pagesMoney Making Machine 100$ Per Day Cyber. Dude PDFalexNo ratings yet

- LogDocument86 pagesLogEkosNo ratings yet

- Socks 5Document551 pagesSocks 5jhonNo ratings yet

- $100 Amazon Gift Card Generator 2019Document1 page$100 Amazon Gift Card Generator 2019Dr. Midas50% (2)

- Hack Otp From Working MethodologiesDocument2 pagesHack Otp From Working Methodologiesamirul lex100% (1)

- Shopwithscript Tut LuciferDocument13 pagesShopwithscript Tut LuciferMike Bitner100% (2)

- Learn Daddy YeahDocument1 pageLearn Daddy YeahFnātîc Jūstînē HøvënNo ratings yet

- Cashout Through ExchangeDocument2 pagesCashout Through ExchangeDustin HallNo ratings yet

- Internet Bank FraudDocument3 pagesInternet Bank FraudJaison M.JohnNo ratings yet

- Iphone Release NotesDocument3 pagesIphone Release NotesJavier RodriguezNo ratings yet

- Swipe 4 BeginnersDocument4 pagesSwipe 4 BeginnersJakub S.No ratings yet

- CVV Carding To BTC Safe and Easy 2020Document2 pagesCVV Carding To BTC Safe and Easy 2020Tunde IbrahimNo ratings yet

- CC Bin ActivatorDocument4 pagesCC Bin ActivatorzamburittiNo ratings yet

- HotelsDocument1 pageHotelsTMNo ratings yet

- Dump-Networking-2022 0423 190231 StopDocument481 pagesDump-Networking-2022 0423 190231 StopivanNo ratings yet

- 2、贝宝转账流程 - 英文Document11 pages2、贝宝转账流程 - 英文Andri Anto100% (1)

- READMEDocument4 pagesREADMEGdjfrrfr67% (3)

- Methods PDFDocument2 pagesMethods PDFNahid HasanNo ratings yet

- Spam Tools DownloadDocument2 pagesSpam Tools Downloadfouzi bnebd0% (1)

- FGGVDocument2 pagesFGGVEmmanuel Chase0% (1)

- CashoutPro PDFDocument34 pagesCashoutPro PDFVansh Mayatra67% (3)

- DumpsDocument727 pagesDumpsRakesh HNo ratings yet

- Detail InfoDocument4 pagesDetail InfoBjoy EdenNo ratings yet

- Socks Proxy ServerDocument5 pagesSocks Proxy Servertrezeguet3767% (3)

- Review of Some SMS Verification Services and Virtual Debit/Credit Cards Services for Online Accounts VerificationsFrom EverandReview of Some SMS Verification Services and Virtual Debit/Credit Cards Services for Online Accounts VerificationsRating: 5 out of 5 stars5/5 (2)

- Evaluation of Some SMS Verification Services and Virtual Credit Cards Services for Online Accounts VerificationsFrom EverandEvaluation of Some SMS Verification Services and Virtual Credit Cards Services for Online Accounts VerificationsRating: 5 out of 5 stars5/5 (2)

- Slide Thu Thập Và Phân Tích Thông Tin ANMDocument235 pagesSlide Thu Thập Và Phân Tích Thông Tin ANMViệt VđNo ratings yet

- Comando Teltonica FMB y FMCDocument22 pagesComando Teltonica FMB y FMCSynthesis-group GpsNo ratings yet

- Design and Performance Analysis of LoRa LPWAN Antenna For IoT ApplicationsDocument4 pagesDesign and Performance Analysis of LoRa LPWAN Antenna For IoT ApplicationsSỹ RonNo ratings yet

- 2023-04 Nokia - Understanding - ROADM - Add - Drop - Architectures - White - Paper - ENDocument11 pages2023-04 Nokia - Understanding - ROADM - Add - Drop - Architectures - White - Paper - ENEuncheol ParkNo ratings yet

- NOJA-565-14 SCADA Interface Description - 0Document67 pagesNOJA-565-14 SCADA Interface Description - 0astorzeroNo ratings yet

- Fortimail Cli Reference 524Document385 pagesFortimail Cli Reference 524Ernesto BubriskiNo ratings yet

- Grid Installation Guide (Dell) v2 3 3 BrianDocument127 pagesGrid Installation Guide (Dell) v2 3 3 Brianivanpgnic6337No ratings yet

- Makerere University: College of Computing & Information SciencesDocument5 pagesMakerere University: College of Computing & Information SciencesMunya RushambwaNo ratings yet

- ATSC Digital Television Standard (A/53) Revision EDocument101 pagesATSC Digital Television Standard (A/53) Revision EGaby RocíoNo ratings yet

- SONET - Clock Based FramingDocument6 pagesSONET - Clock Based FramingmaryNo ratings yet

- VSN700 DATA LOGGER - BCD.00387 - EN - RevHDocument4 pagesVSN700 DATA LOGGER - BCD.00387 - EN - RevHGillianne Mae VargasNo ratings yet

- OEB902101 USN9810 V900R001 System Overview-20110914-A - ISSUE1.30Document66 pagesOEB902101 USN9810 V900R001 System Overview-20110914-A - ISSUE1.30WalterLooKungVizurragaNo ratings yet

- IST4060 Telecommunications and Networks - Lesson 1Document49 pagesIST4060 Telecommunications and Networks - Lesson 1Rush KirubiNo ratings yet

- 2.3 Ficha Técnica DS-6904UDIB-Decoder V2.6.1 20210115Document4 pages2.3 Ficha Técnica DS-6904UDIB-Decoder V2.6.1 20210115Fernando SepúlvedaNo ratings yet

- EE477 - mt1 - Fall2020 SolutionDocument10 pagesEE477 - mt1 - Fall2020 SolutionÖmer Faruk AtalayNo ratings yet

- UtstarDocument18 pagesUtstarkmari1973No ratings yet

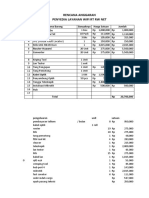

- Rencana Anggaran Penyedia Layanan Wifi RT RW NetDocument9 pagesRencana Anggaran Penyedia Layanan Wifi RT RW NetFazar SambasNo ratings yet

- Adaptive Delta ModulationDocument11 pagesAdaptive Delta ModulationUrvashi GuptaNo ratings yet

- FTTH Personal ResearchDocument19 pagesFTTH Personal ResearchYves Mathurin Nzietchueng100% (1)

- OTN - Overview - G709 - Optical Transport NetworkDocument15 pagesOTN - Overview - G709 - Optical Transport Networkchristal MIAKOUKILANo ratings yet

- Wired Wireless Communications in EV Battery Management 1690514167Document7 pagesWired Wireless Communications in EV Battery Management 1690514167GaneshNo ratings yet

- 62 AND 63 Tools of EcommerceDocument20 pages62 AND 63 Tools of EcommerceHaRsimran MalhotraNo ratings yet

- 3GPP R8 LTE Overview: 조봉열, Bong Youl (Brian) ChoDocument143 pages3GPP R8 LTE Overview: 조봉열, Bong Youl (Brian) ChoyhkoNo ratings yet

- MSTSI Channel Line-UpDocument2 pagesMSTSI Channel Line-UpJesper John Cordero Arceo0% (1)

- DataSheet Enterprise Security Gateway and Network Appliance With 10G SFP+ Ubiquiti UniFi Dream Machine PRO UDM-PRO PDFDocument7 pagesDataSheet Enterprise Security Gateway and Network Appliance With 10G SFP+ Ubiquiti UniFi Dream Machine PRO UDM-PRO PDFPlanetNo ratings yet

- F. 38 64 80 6 38 64 80 7 38 64 80 8 38 64 80 5 38 64 80 9 q67w92Document68 pagesF. 38 64 80 6 38 64 80 7 38 64 80 8 38 64 80 5 38 64 80 9 q67w92Nirdesh RayaNo ratings yet

- C3000 SD Analog PTZ Camera StationDocument4 pagesC3000 SD Analog PTZ Camera StationArca MakmurNo ratings yet

- Review of Congestion Control Algorithms For Performance Evaluation of WCDMADocument4 pagesReview of Congestion Control Algorithms For Performance Evaluation of WCDMAabhi749434No ratings yet

- Blackberry Curve 8900 FactSheetDocument1 pageBlackberry Curve 8900 FactSheetWayne Schulz100% (2)